ix

Inventory Model With Gamma Distribution Hadi Sumadibrata, Ismail

Bin Mohd

642

Accuracy Analysis Of Naive Bayesian

Anti-Spam Filter

Ruslam, Armin Lawi, And Sri Astuti Thamrin

649

A New Method For Generating Fuzzy Rules From Training Data And Its Application In Financial Problems

Agus Maman Abadi, Subanar, Widodo, Samsubar Saleh

655

The Application Of Laws Of Large Numbers In Convergence Concept In Probability And Distribution

Georgina M. Tinungki 662

An Empirical Bayes Approach for Binary Response Data in Small Area Estimation

Dian Handayani, Noor Akma Ibrahim, Khairil A. Notodiputro, MOhd. Bakri Adam

669

Statistical Models For Small Area Estimation Khairil A Notodiputro, Anang Kurnia, and Kusman Sadik

677

Maximum Likelihood Estimation For The Non-Separable Spatial Unilateral Autoregressive Model

Norhashidah Awang, Mahendran Shitan

685

Small Area Estimation Using Natural Exponential Families With Quadratic Variance Function (Nef-Qvf) For Binary Data

Kismiantini 691

Using An Extended And Ensemble Kalman Filter Algorithm For The Training Of Feedforward Neural Network In Time Series Forecasting

Zaqiatud Darojah, M. Isa Irawan, And Erna Apriliani

696

Estimation Of Outstanding Claims Liability And Sensitivity Analysis: Probabilistic Trend Family (PTF) Model

Arif Herlambang, Dumaria R Tampubolon

704

Expected Value Of Shot Noise Processes Suyono 711

Modelling Malaysian Wind Speed Data Via Two Paramaters Weibull

Nur Arina Basilah Kamisan, Yong Zulina Zubairi, Abdul Ghapor Hussin, Mohd. Sahar Yahya

718

Application Of Latin Hypercube Sampling And Monte Carlo Simulation Methods: Case Study The Reliability Of Stress Intensity Factor And Energy Release Rate Of Indonesian Hardwoods

Yosafat Aji Pranata And Pricillia Sofyan Tanuwijaya

726

The Development Of Markov Chain Monte Carlo (Mcmc) Algorithm For Autologistic Regression Parameters Estimation

Suci Astutik, Rahma Fitriani, Umu Sa’adah, And Agustin Iskandar

734

A Note About Dh-Fever Estimation With ARIMAX Models Elly Ana, Dwi Atmono Agus W

741

Evaluation Of Additive-Innovational Outlier Identification Procedure For Some Bilinear Models

I

smail, M.I., Mohamed, I.B., Yahya, M.S.

xi

Model By Spectral Regression Methods Iriawan, Suhartono

Application Of Cluster Analysis To Developing Core Collection In Plant Genetic Resources

Sutoro 875

Small Area Estimation With Time And Area Effects Using A Dynamic Linear Model

Kusman Sadik And Khairil Anwar Notodiputro

880

Statistical Analysis Of Wind Direction Data Ahmad Mahir Razali, Arfah Ahmad, Azami Zaharim And Kamaruzzaman Sopian

886

Generalized Additive Mixed Models in Small Area Estimation Anang Kurnia, Khairil A. Notodiputro, Asep Saefuddin, I Wayan Mangku

891

Kernel Principal Component Analysis In Data Visualization Ismail Djakaria, Suryo Guritno, Sri Haryatmi

898

GARCH Models And The Simulations Nelson Nainggolan, Budi

Nurani Ruchjana And Sutawanir Darwis

906

Rainfall Prediction Using Bayesian Network Hera Faizal Rachmat, Aji Hamim Wigena, and Erfiani

911

Identifying Item Bias Using The Simple Volume Indices And Multidimensional Item Response Theory Likelihood Ratio (Irt-Lr) Test

Heri Retnawati 916

Ordinary Kriging And Inverse Distance Weighting For Mapping Soil Phosphorus In Paddy Field

Mohammad Masjkur, Muhammad Nuraidi and Chichi Noviant

924

K-Means Clustering Visualization On Agriculture Potential Data

For Villages In Bogor Using Mapserver

Imas S. Sitanggang, Henri Harianja, and Lailan Syaufina

932

Some Methods To Estimate The Number Of Components In A Mixture

M. A. Satyawan, A. H. Wigena, Erfiani

941

A Probabilistic Model For Finding A Repeat Triplet Region In DNA Sequence

Tigor Nauli 947

Application Of Spherical Harmonics In Determination Of Tec Using Gps Observable

Mardina Abdullah, Siti Aminah Bahari, Baharudin Yatim, Azami Zaharim, Ahmad Mahir Razali

954

Testing Structure Correlation Of Global Market By Statistic Vvsv Erna Tri Herdiani, and Maman A. Djauhari

961

Exploring the MAUP from a spatial perspective Gandhi Pawitan 967

Estimation of RCA(1) Model using EF: A new procedure and its robustness

1Norli Anida Abdullah, 2Ibrahim Mohamed, 3Shelton Peiris

996

Second Order Linear Elliptic Operators In The Unit Square

xii

POSTERStudy Of Fractional Factorial Split-Plot Experiment Sri Winarni, Budi Susetyo, and Bagus Sartono

1012

Improving Model Performance For Predicting Poverty Village Category Using Neighborhood Information In Bogor

Bagus Sartono, Utami Dyah S, and Zulhelmi Thaib

1019

Ammi Models On Count Data: Log-Bilinear Models Alfian Futuhul Hadi H. Ahmad Ansori Mattjik I Made Sumertajaya Halimatus Sa’diyah

1026

Prediction Of Oil Production Using Non Linear Regression By Sdpro Software

(Special Program Package)*)

Budi Nurani R , and Kartlos J. Kachiashvili

1038

An Implementation Of Spatial Data Mining Using Spatial Autoregressive (Sar) Model For Education Quality Mapping At West Java*)

Atje Setiawan A. , Retantyo Wardoyo , Sri Hartati , and Agus Harjoko

1045

Validation Of Training Model For Robust Tests Of Spread

Teh Sin Yin, and Abdul Rahman Othman

1056

Spectral Approach For Time Series Analysis Kusman Sadik 1063

The ACE Algorithm for Optimal Transformations in Multiple Regression

Kusman Sadik 1066

The Relation Between The Students’ Interaction And The Construction Of Mathematical Knowledge

Rini Setianingsih 1069

Application of Auto Logistic Regression Spatial Model using Variogram Based Weighting Matrix to Predict Poverty Village Category

Utami Dyah Syafitri, Bagus Sartono, Vinda Pratama

1063

The 3"* International Conference on Mathematics and Statistics (ICoMS-3) Institut Pertanian Bogor, Indonesia, 5-6 August 2008

SPECTRAL APPROACH FOR TIME SERIES ANALYSIS

Kusman Sadik

Department of Statistics, Institut Pertanian Bogor Jl. Meranti, Wing 22 Level 4, Kampus IPB Darmaga, Bogor 16680 – Indonesia

e-mail : kusmans(a),ipb.ac.id

Key Words

: Spectral analysis, seasonal adjustment procedures, cross spectral, fuzzy logic systems, input signals,

fourier transform, fractal space-time.

1.

Introduction

The first appearance of spectral analysis in the study of macroeconomic time series dates motivated by the

requirement of a more insightful knowledge of the series structure and supported by the contemporaneous

progress in spectral estimation and computation. The first works focused on the problem of seasonal

adjustment procedures and on the general spectral structure of economic data. Cross spectral methods were

pointed out from the outset as being important in discovering and interpreting the relationships between

economic variables. After the early years, the range of application of such analysis was extended to the study of

other econometric issues, among which the controversial trend-cycle separation, the related problem of

business cycles extraction and the analysis of co-movements among series, usefiil in the study of international

business cycles. In particular, cross spectral analysis allows a detailed study of the correlation among series. An

empirical investigation about the possibility that the market is in a self-organized critical state (SOC) show a

power law behaviour in the avalanche size, duration and laminar times during high activity period (Bartolozzi,

Leinweber and Thomas, 2005).

2.

Mathematical Models for Fractal Fluctuations and Deterministic

The larger scale fluctuations incorporate the smaller scale fluctuations as intemal fine scale structure and

may be visualized as a continuum of eddies (waves). Dynamical systems in nature are basically fiizzy logic

systems integrating a unified v^ole communicating network of input signals (perturbations) with

self-organized ordered two-way information transpot between the larger and smaller scales. Self-similar

structures are generated by iteration (repetition) of simple rules for growth processes on all scales of space and

time. Such iterative processes are simulated mathematically by numerical computations such as

X„+i

= F(^«)

where

X„+i

the value of the variable X at (« + i f " computational step is a fiinction F of its earlier value

X„.

The

spectrum of { x }

is defined to be the Fourier transform of

Yx(/^),3. Model Concepts of Universal Spectrum of Fluctuations

A general systems theory was first developed to quantify the observed fractal space-time fluctuations in

turbulent fluid flows. The model concepts are independent of the exact details of the physical, chemical or

other properties and therefore applicable to all dynamical systems. The observed inverse power law form for

power spectra implies that the fi-actal fluctuations can be visualized to result from a hierarchical eddy

continuum structure for the overall pattern. Starting from this simple basic concept that large scale eddies

form as envelopes of intemal small scale eddy circulations the following important model predictions are

derived.

1064

Let Z

tis time series stationer process with autocorrelation

γ

k. Its Fourier

transformation is (Yujima, 1998) :

∑

∞ −∞ =−

= k

iwk ke

w

f γ

π

2 1 ) (

Function

f(w)

is continu function non-negative that representative of spectrum for

autocorrelation function

γ

k. Spectrum of

f(w)

and autocorrelation function

γ

kare unique

Fourier transformation. Generally, spectrum of ARMA(p,q) process can be written

(West, 1999):

) ( ) ( 2

) ( ) ( ) (

2

iw p iw p

iw p iw q a

e e

e e w

f

φ πφ

θ θ σ

− −

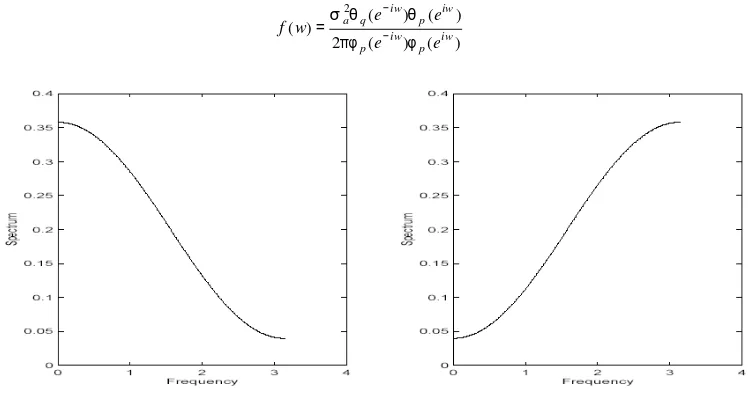

[image:6.595.90.467.218.419.2]=

Figure 1: Plots of the spectrum of MA(1) processes (0 = 0.5 for the left figure and 0 = - 0.5 for the right figure) – Simulated Data

Figure 1 plots the spectrum of MA(1) processes with positive and negative coefficients. When 0 > 0, we see that the spectrum is high for low frequencies and low for high frequencies. When 0 < 0, we observe the opposite. This is because when 0 is positive, we have positive one lag correlation which makes the series smooth with only small contribution from high frequency (say, day to day) components. When 0 is negative, we have negative one lag correlation, therefore the series fluctuates rapidly about its mean value.

Figure 3: Window Functions and Their Frequency Response (Simulated Data). The rectangular

[image:6.595.73.473.535.712.2]1065

respective Fourier transforms (right panel). For the latter, the number of points N = 15 has been chosen rather small to emphasize the differences. Note in the zoom (right panel, inset) the reduced side lobe amplitude and leakage of the Hanning and Hamming windows with respect to the rectangular one, the Hamming window performing better in the first side lobe.

The only way to prevent this effect, would be to choose T (or equivalently N) as a multiple of the largest period that is likely to occur. Unfortunately, this is feasible only if we have some idea of the frequencies involved in the process and would in any case entail some loss of data at one or both sample ends. As for the cutoff fr equencies νl= kl/(N∆t) and νh= kh/(N∆t), given the value of N,

they must be chosen to be multiples of T −1

,otherwise the filter does not completely remove the zero frequency component (i.e. the signal mean) and cannot help in eliminating unit roots.