1

kang

INDONESIA’S

BALANCE OF PAYMENTS

REPORT

SECOND QUARTER 2009

2

Contact Address

Balance of Payments Bureau

Directorate of Economic and Monetary Statistics Bank Indonesia

Sjafruddin Prawiranegara Tower, 16th Floor Jl. M.H. Thamrin No. 2

Jakarta 10350

Phone : (021) 3817088

Fax : (021) 3800134

E-mail : [email protected]

3

INDONESIA’S

BALANCE OF PAYMENTS

REPORT

SECOND QUARTER 2009

1

RINGKASAN ……… 1

SUMMARY INDONESIA’S BALANCE OF PAYMENTS IN Q2/2009 AND ITS CONTRIBUTING FACTORS ……… ……… 1 3 CURRENT ACCOUNT 1. Non-Oil and Gas Trade Balance ……… 7

1.1. Non-Oil and Gas Exports ……… 8

1.2. Non-Oil and Gas Imports ……… 14

2. Oil and Gas Trade Balance ……… 16

2.1. Oil ……… 16

2.2. Gas ……… 17

3. Services Account ……… 18

4. Income Account ……… 19

5. Current Transfers ……… 20

CAPITAL AND FINANCIAL ACCOUNT 1. Capital Account ……… 21

2. Financial Account ……… 21

2.1. Public Sector ……… 22

2.2. Private Sector ……… 26

RESERVE ASSETS ……… 31

INDICATORS OF EXTERNAL SUSTAINABILITY ……… 33

2

LIST OF TABLES

Page Page

Table 1 Indonesia’s Balance of Payments and Several Economic Indicators in Q2/2009

5 Table 13 Major Non-Oil and Gas Commodities Imported from Major Countries of Origin

14

Table 2 Major Non-Oil and Gas Commodities Exported to Major Countries of Destination

8 Table 14 Import Value of Raw Materials Based on Country of Origin (C&F)

15

Table 3 Coal Export Value to Major Countries of Destination 9 Table 15 Import Value of Consumption Goods Based on Country of Origin (C&F)

15

Table 4 Machinery & Mechanical Appliances Export Value to Major Countries of Destination

9 Table 16 Import Value of Capital Goods Based on Country of Origin (C&F)

15

Table 5 Electronics Export Value to Several Major Countries of Destination

10 Table 17 Growth of 15 Major Import Commodities 15

Table 6 Value of Rubber Exports to Several Major Countries of Destination

10 Table 18 Oil Exports and Imports 16

Table 7 Value of Shrimp Exports to Several Major Countries of Destination

11 Table 19 Demand and Supply of World Oil 16

Table 8 Copper Export Value to Several Major Countries of Destination

11 Table 20 Exports of LNG, LPG, and Natural Gas 17

Table 9 Nickel Export Value to Several Major Countries of Destination

12 Table 21 Indonesia’s Gas Reserves (billion cubic feet) 18

Table 10 TTP Export Value to Several Major Countries of Destination

12 Table 22 Non-Investment Grant 20

Table 11 Export Value of Chemical Product to Several Major Countries of Destination

13 Table 23 Investment Grant 21

Table 12 CPO Export Value

to Several Major Countries of Destination

14 Table 24 Indicator of External Sustainability 33

LIST OF CHARTS

Page Page

Chart 1 Current Account 7 Chart 10 World CPO Price 13

Chart 2 Non-Oil and Gas Trade Balance 8 Chart 11 Shares of Non-Oil and Gas Imports Based on Major Countries of Origin

14

Chart 3 Shares of Non-Oil and Gas Exports Based on Major Countries of Destination

8 Chart 12 World Oil Prices 17

Chart 4 Coal Unit Price 9 Chart 13 Oil Consumption 17

Chart 5 World Rubber Price 10 Chart 14 Services Account 18

Chart 6 World Shrimp Price 11 Chart 15 Travel Services 19

Chart 7 World Copper Price 11 Chart 16 Income Account 19

Chart 8 World Nickel Price 12 Chart 17 Workers’ Remittances 20

Chart 9 Volume Of Textile and Textile Product (TTP) Exports to Several Major Countries of Destination

12 Chart 18 Capital and Financial Account by Type of Investment

3

LIST OF CHARTS

Page Page

Chart 19 Capital and Financial Account by Sector 22 Chart 29 Government Foreign Loan Position 26

Chart 20 Financial Account of Public Sector 22 Chart 30 Financial Account of Private Sector 27

Chart 21 Yield of Indonesian Global Bond and US T-Note 23 Chart 31 Direct Investment in Indonesia 27

Chart 22 BI Rate and Fed Rate 24 Chart 32 Foreign Direct Investment Inflows in Oil and Gas

Sector

27

Chart 23 SUN & SBI Owned by Foreign Investors 24 Chart 33 Net Foreign Direct Investment in Non-Oil and Gas Sector Based on Country

27

Chart 24 Disbursement and Repayment of Government Loan 24 Chart 34 Net Foreign Direct Investment in Non-Oil and Gas By Sector

28

Chart 25 Program Loan Disbursement 25 Chart 35 Foreign Transactions in IDX and IHSG 28

Chart 26 Project Loan Disbursement 25 Chart 36 Debt Securities Issued by Private Sector 29

Chart 27 Loan Position by Major Creditor Countries 26 Chart 37 Loan Disbursement of Private Sector 29

1

SUMMARY

During Q2/2009, Indonesia's current account posted a US$3.1 billion surplus, up from the US$2.9 billion

surplus in Q1/2009. This surplus more than compensated for the deficit on the capital and financial account,

bringing the overall balance of payments surplus to US$1.1 billion. In response, international reserves climbed

further to US$57.6 billion at end Q2/2009, equivalent to about 5.5 months of imports and official debt service

payments.

The current account surplus was bolstered by more robust surpluses in non-oil and gas trade balance, oil

and gas trade balance and current transfers, with the surpluses in these accounts outweighing the escalation in the

income and services account deficit. The strongest improvement over the preceding quarter was recorded in the

non-oil and gas trade balance, with non-oil and gas exports posted a larger quarterly increase than non-oil and gas

imports. An improving trend in non-oil and gas export performance was also visible in its annual growth (y.o.y),

recorded at negative 17.3% in Q2/2009, a milder decline than in Q1/2009. Contrasting this was the negative 30.6%

growth in non-oil and gas imports during Q2/2009, representing steeper decline compared to Q1/2009 performance

of negative 28.8%. The significant improvement in non-oil and gas exports over the earlier quarter is explained

primarily by persistent strong demand from some Asian economies and further increases in international market

prices for key export products, led by primary commodities such as coal, copper and CPO. On the other hand,

recovery in non-oil and gas imports was constrained by a slowing down in domestic demand growth.

In Q2/2009, the capital and financial account posted a US$2.4 billion deficit following the US$1.8 billion

surplus of the preceding quarter. This deficit resulted from reduced inflows of foreign direct investment, increased

domestic bank and non-bank placements in non-resident banks and higher levels of servicing of official external

debt. The drop in foreign direct investment was consistent with the slowdown in domestic economic growth, while

the rise in servicing of official external debt was due to seasonal factor. The increase in domestic bank and non-bank

placements in non-resident banks should not be considered as a negative development as this condition took place

when the current account recorded a surplus, portfolio capital inflow increased and the demand for foreign

exchange was still limited. In other words, this was a reflection of the growing foreign exchange liquidity and the

anticipation towards a higher demand for foreign exchange in Q2/2009 in line with the expectation of an improving

domestic demand. The capital and financial account received a significant boost in Q2/2009 from portfolio

investment, which recorded an increased surplus over the preceding quarter. Among the factors bolstering the

portfolio investment performance were renewed investor confidence in Indonesia's economic stability and the calm,

orderly national elections.

3

Indonesia’s Balance of Payments (BOP) in Q2/2009 recorded a surplus of USD1.1 billion. The main

contributor was the current account with a surplus of USD3.1 billion. Meanwhile, the capital and financial accounts

posted a deficit of USD2.4 billion. The current account surplus increased compared to the preceding quarter. The

improved performance of current account was stemming from the increased surplus on non-oil and gas trade

balance, oil and gas trade balance, and current transfers, with the surpluses in these accounts compensating the

deficits on services and income account. The capital and financial account was in deficit, after registering a surplus in

the previous quarter, due to the drop of direct investment inflows, the increased of domestic bank and non-bank

placements in overseas banks, and higher levels of servicing of official external debt. Meanwhile portfolio investment

posted a surplus related to the higher investor confidence in economic condition and security matters in Indonesia.

In line with the overall BOP development, the amount of foreign reserves at the end of the period rose to USD57.6

billion or equivalent to 5.5 months of imports and official debt service payments.

Several fundamental factors contributed to the Indonesia’s Balance of Payments during Q2/2009, both

stemming from domestic and foreign aspects, such as:

Despite the fact that several developed countries that are the major trade partners of Indonesia—such as the US, Japan, and the European Union—were still recording negative growth, some Asian trade partners such as

China and India posted positive growth contributing a positive impact to the demand and prices of several

Indonesian prime export commodities. In the meantime, the slowing down of domestic demand in many

countries contributed to inflation pressure that showed a declining tendency. Consequently most of monetary

authorities continued to implement the policy of declining interest rate to sufficiently low level. This situation

provoked investors to place their funds in countries providing high yield such as Indonesia.

The prospect for global economic recovery supported the increased demand for several key non oil and gas

export commodities, such as Crude Palm Oil (CPO), copper and rubber, which then induced the rise of the price

of the said commodities compared to the previous quarter.

The average oil prices (export unit price) rose to USD56.9/bl in Q2/2009 from USD41.8/bl in Q1/2009. This rise in prices was related to the expectation of world’s demand recovery, especially in developed countries such as

the US, European countries, and Japan. Furthermore, the impact of the weakened USD exchange rate against

other main currencies also boosted oil price to a higher level. In line with the world’s oil price development, the

price of gas (LNG) also rose from USD5.5/MBTU in Q1/2009 to USD6.5/MBTU during reporting period.

Indonesian economy grew by 4.0% (y.o.y) during Q2/2009, lower than 4.4% in Q1/2009. From demand side,

the slowing rate was related to the crawling condition of all domestic demand components especially

household consumption. This situation was considered pertaining to the lower expenses of Presidential election

compared to those of legislative election. The slow growth of domestic economy and the decline of exports

became the contributing factors maintaining low import growth rate.

INDONESIA

’

S BALANCE OF PAYMENTS IN Q2/2009 AND ITS

4

Indonesian inflation rate was 3.7% during the reporting period, lower than the preceding quarter (7.9%). This condition was in line with the weakening of domestic demand and the decrease of world commodity price. In

terms of foreign exchange, rupiah strengthened during the reporting quarter with an average rate of

Rp10,531/USD compared to the previous rate of Rp11,631/USD. In line with the low inflation rate and the

strengthening of rupiah against USD and supporting the efforts to boost domestic economic growth, Bank

Indonesia loosened its monetary policy by lowering BI interest rate.

Oil production declined despite the improving oil price. Indonesian oil production in Q2/2009 reached 0.947

million barrels per day, lower than 0.962 million barrels per day in the preceding quarter. In addition to the

natural declining phenomenon, several technical problems on site were contributing to the downturn of oil

production. During the same period, the gas (LNG) export volume lessened from 256.8 MBTU in Q1/2009 to

228.1 MBTU in Q2/2009. Likewise, natural gas export volume decreased from 77.6 MBTU to 76.8 MBTU

during the reporting quarter. Meanwhile oil consumption reached 84.9 million barrels in Q2/2009, higher than

80.7 million barrels in the preceding quarter. The increasing oil demand was related to domestic economic

activities that recorded higher level than the previous quarter, despite its slowing growth. It was also

considered related to the election activities absorbing considerable demand for energy especially in

5

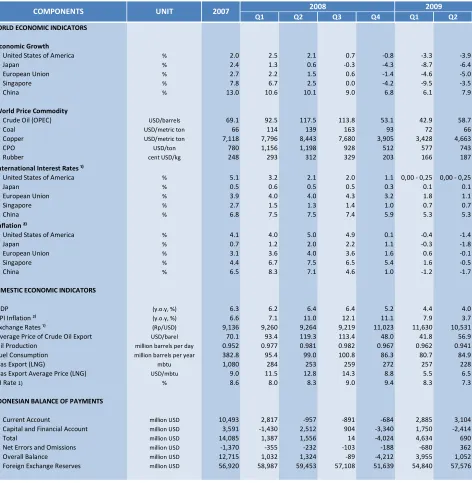

Table 1

Indonesia’s Balance of Payments and

Several Economic Indicators in Q2/2009

Q1 Q2 Q3 Q4 Q1 Q2

WORLD ECONOMIC INDICATORS

Economic Growth

‐ United States of America % 2.0 2.5 2.1 0.7 ‐0.8 ‐3.3 ‐3.9

‐ Japan % 2.4 1.3 0.6 ‐0.3 ‐4.3 ‐8.7 ‐6.4

‐ European Union % 2.7 2.2 1.5 0.6 ‐1.4 ‐4.6 ‐5.0

‐ Singapore % 7.8 6.7 2.5 0.0 ‐4.2 ‐9.5 ‐3.5

‐ China % 13.0 10.6 10.1 9.0 6.8 6.1 7.9

World Price Commodity

‐ Crude Oil (OPEC) USD/barrels 69.1 92.5 117.5 113.8 53.1 42.9 58.7

‐ Coal USD/metric ton 66 114 139 163 93 72 66

‐ Copper USD/metric ton 7,118 7,796 8,443 7,680 3,905 3,428 4,663

‐ CPO USD/ton 780 1,156 1,198 928 512 577 743

‐ Rubber cent USD/kg 248 293 312 329 203 166 187

International Interest Rates ¹⁾

‐ United States of America % 5.1 3.2 2.1 2.0 1.1 0,00 ‐ 0,25 0,00 ‐ 0,25

‐ Japan % 0.5 0.6 0.5 0.5 0.3 0.1 0.1

‐ European Union % 3.9 4.0 4.0 4.3 3.2 1.8 1.1

‐ Singapore % 2.7 1.5 1.3 1.4 1.0 0.7 0.7

‐ China % 6.8 7.5 7.5 7.4 5.9 5.3 5.3

Inflation ²⁾

‐ United States of America % 4.1 4.0 5.0 4.9 0.1 ‐0.4 ‐1.4

‐ Japan % 0.7 1.2 2.0 2.2 1.1 ‐0.3 ‐1.8

‐ European Union % 3.1 3.6 4.0 3.6 1.6 0.6 ‐0.1

‐ Singapore % 4.4 6.7 7.5 6.5 5.4 1.6 ‐0.5

‐ China % 6.5 8.3 7.1 4.6 1.0 ‐1.2 ‐1.7

DOMESTIC ECONOMIC INDICATORS

GDP (y.o.y, %) 6.3 6.2 6.4 6.4 5.2 4.4 4.0 CPI Inflation ²⁾ (y.o.y, %) 6.6 7.1 11.0 12.1 11.1 7.9 3.7 Exchange Rates ¹⁾ (Rp/USD) 9,136 9,260 9,264 9,219 11,023 11,630 10,531 Average Price of Crude Oil Export USD/barel 70.1 93.4 119.3 113.4 48.0 41.8 56.9 Oil Production million barrels per day 0.952 0.977 0.981 0.982 0.967 0.962 0.941 Fuel Consumption million barrels per year 382.8 95.4 99.0 100.8 86.3 80.7 84.9 Gas Export (LNG) mbtu 1,080 284 253 259 272 257 228 Gas Export Average Price (LNG) USD/mbtu 9.0 11.5 12.8 14.3 8.8 5.5 6.5 BI Rate 1) % 8.6 8.0 8.3 9.0 9.4 8.3 7.3

INDONESIAN BALANCE OF PAYMENTS

‐ Current Account million USD 10,493 2,817 ‐957 ‐891 ‐684 2,885 3,104

‐ Capital and Financial Account million USD 3,591 ‐1,430 2,512 904 ‐3,340 1,750 ‐2,414

‐ Total million USD 14,085 1,387 1,556 14 ‐4,024 4,634 690

‐ Net Errors and Omissions million USD ‐1,370 ‐355 ‐232 ‐103 ‐188 ‐680 362

‐ Overall Balance million USD 12,715 1,032 1,324 ‐89 ‐4,212 3,955 1,052

‐ Foreign Exchange Reserves million USD 56,920 58,987 59,453 57,108 51,639 54,840 57,576

Source: CEIC, IMF, World Bank, Bank Indonesia, and other sources ¹⁾ average

²⁾ end‐month position of the relevant quarter

*) temporary data from Forecast Consensus August 2009

7

The current account in Q2/2009 posted a

surplus of USD3.1 billion, higher than a surplus of

USD2.9 billion in Q1/2009. The improved performance

of current account was supported by the increasing

surpluses on non-oil and gas trade balance, oil and gas

trade balance, and current transfers. The larger

surpluses in these three balances exceeded the

increased deficits on services and income accounts.

-5,000 -3,000 -1,000 1,000 3,000 5,000 7,000 9,000

Q.1 Q.2 Q.3 Q.4 Q.1 Q.2 Q.3 Q.4 Q.1 Q.2

2007 2008* 2009**

million USD

Services Income Trade Balance Current Trans. Current Account

Chart 1 Current Account

The increased surplus on non-oil and gas trade

balance compared to the preceding quarter was

resulted from the higher increase in non-oil and gas

exports than the increase in non-oil and gas imports.

Higher increase was recorded in the exports of

natural-based commodities with low import content. In the

midst of weakening domestic demand, such export

profile would consequently impede import of non-oil

and gas.

Meanwhile, the oil trade balance improved. It was

due to the fact that the rise of oil export price was

higher than the increase in oil import price. Despite

falling gas export volume, the surplus of gas trade

balance increased supported by the gas price increase

following the rise of oil price. The current transfers also

improved as a result of a considerable inflow of

workers’ remittances specifically from the Middle East.

On the other side, the increase deficit on services

account was driven among others, by the increase in

import freights. The rise in deficit of the income account

was originated from the increased dividend payments of

foreign direct investment companies, interest/coupon

payments of securities, and the interest payments of

external debt.

1.

Non-Oil and Gas Trade Balance

In Q2/2009 the non-oil and gas trade balance

recorded a surplus of USD6.6 billion, higher than

USD5.3 billion surplus in Q1/2009. The improved

performance of non oil and gas exports was also

reflected in its annual growth (y.o.y) which improved to

negative 17.3% in Q2/2009 compared to negative 22.2

% in Q1/2009. On the contrary, non oil and gas

imports posted a negative growth of 30.6% in

Q2/2009, steeper than minus 28.8% in Q1/2009.

The improvement in non-oil and gas exports

compared to Q1/2009 was mainly due to the

considerable demand from several Asian countries and

the sustained increase in prices of several key export

products in international market such as coal, copper

and CPO. At the same time, the increase in non-oil and

gas imports was hampered by the slowing growth of

domestic demand.

8

1,000 2,000 3,000 4,000 5,000 6,000 7,000 8,000

3,000 8,000 13,000 18,000 23,000 28,000 33,000 38,000

Q.1 Q.2 Q.3 Q.4 Q.1 Q.2 Q.3 Q.4 Q.1 Q.2

2007 2008* 2009**

juta USD juta USD

Export Import Trade Balance (RA)

Chart 2

Non-Oil and Gas Trade Balance

1.1. Non-Oil and Gas Exports

The non-oil and gas exports rose to USD23.1

billion in Q2/2009 compared to USD20.5 billion in

Q1/2009. The strong demand for natural-based

commodities such as mining products (coal) and

manufacturing products (CPO) from several Asian

countries had succeeded to raise export value. Amidst

the ongoing global recession, Indonesian exports were

concentrated in five major countries of destination

namely the US (10.6%), Japan (10.3%), the European

Union (10.1%), China (9.2%) and India (8.0%) with the

following main commodities: clothing to the US and the

European Union, metalliferous ores & metal scrub to

Japan, fixed vegetable oils & fats to China and India.

0.00 3.00 6.00 9.00 12.00 15.00 18.00

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

2007 2008 2009*

Sg Jpn EU USA India

(%)

Chart 3

Shares of Non-Oil and Gas Exports Based on Major Countries of Destination

Despite sustaining a negative annual growth,

non-oil and gas exports showed a slowing rate of decline

which was contributed as well by the improved export

performance of most of major commodities.

Performance of natural based commodities (SDA) such

as rubber, copper, nickel, coal, CPO and chemical

products improved significantly. Nevertheless, exports of

several non-SDA manufacturing commodities such as

electrical equipment and machinery & mechanical

appliances also improved.

Table 2

Major Non-Oil and Gas Commodities Exported to Major Countries of Destination

(based on 2digits SITC code, as a % shares of total non-oil and gas exports)

Commodity Share Commodity Share Commodity Share Commodity Share Commodity Share

Clothing 3.4 Metal Ore & scrub 1.6 Clothing 1.5 Vegetable Fats and Oils 2.0 Vegetable Fats and Oils 3.4

Telecommunication Device 1.0 Coal, Coke and Briquettes 1.5 Vegetable Fats and Oils 1.4 Coal, Coke and Briquettes 1.4 Coal, Coke and Briquettes 2.4

Fish and Shrimp 0.8 Non-Iron Metals 1.0 Footwear 1.0 Other Transportation Vehicles 1.0 Metal Ore & scrub 0.9

Coffee, Tea, Cocoa, and Spice 0.6 Electronic Machines 0.7 Telecommunication Device 0.7 Raw Rubber 1.0 Raw Rubber 0.2

9

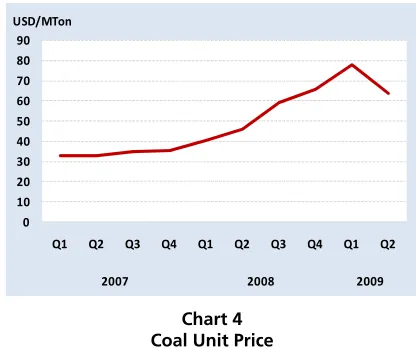

Coal

Coal exports reached USD2.9 billion in Q2/2009 or

increased by 15.3% (y.o.y), slowing down compared to

40.1% increase in Q1/2009 following a weakening

price. Despite the tardy annual growth of this export

commodity, this result still showed an increase of

13.1% (q.t.q) compared to Q1/2009.

0 10 20 30 40 50 60 70 80 90

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

2007 2008 2009

USD/MTon

Chart 4 Coal Unit Price

Most Coal exports were based on long term

contracts. Consequently, despite a slight decline in

volume, Indonesian coal still gained a considerable

demand especially from Asian countries such as India,

Taiwan, South Korea, and Malaysia. This demand was

relatively stable due to the use of coal as a source of

energy. The main destinations of coal exports were

India (18.7%), Taiwan (18.6%), South Korea (14.9%),

and Japan (11.5%).

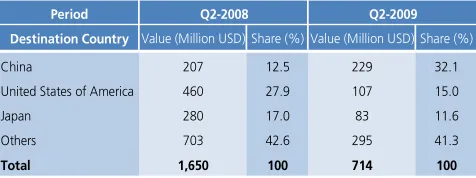

Table 3 Coal Export Value to Major Countries of Destination

Period

Destination Country Value (Million USD) Share (%) Value (Million USD) Share (%)

India 280 11.2 571 19.9

Taiwan 365 14.6 568 19.8

South Korea 325 13.0 455 15.8

Japan 450 18.1 350 12.2

Others 1,072 43.0 928 32.3

Total 2,492 100 2,872 100

Quarter II-2008 Quarter II-2009

Machinery & Mechanical Appliances

Exports of machinery & mechanical appliances was

USD2.2 billion in Q2/2009 or grew by 5.5% (y.o.y),

higher than minus 18.6% in Q1/2009. The improved

exports of machinery & mechanical appliances especially

automotive (road vehicle) to Japan succeeded in

supporting export value. The export destinations of

machinery & mechanical appliances were mainly

Singapore (40.5%), China (11.3%), and Japan (7.9%).

In the framework of enhancing exports of machinery &

mechanical appliances especially automotive products,

Gaikindo will set up collaboration with Australia as the

potential market for automotive industry.

Table 4

Machinery & Mechanical Appliances Export Value to Major Countries of Destination

Period

Destination Country Value (Million USD) Share (%) Value (Million USD) Share (%)

Singapore 457 21.7 972 43.7

China 44 2.1 271 12.2

Japan 268 12.7 190 8.5

Others 1,338 63.5 790 35.5

Total 2,107 100 2,223 100

Q2-2008 Q2-2009

Electronics

Export of electronic products stood at USD2.4

billion or grew by 4.9% (y.o.y). It was improved

compared to minus 4.5% in Q1/2009. The increased

exports were mainly driven by the exports of electronic

goods from Batam to Singapore. Electronic goods

exported by Indonesia were not classified as high-end

products. Therefore, their demand were relatively stable

despite the decrease of purchasing power of the

importing country. The major destinations of

electronics exports were Singapore (24.4%), the US

10

Table 5

Electronics Export Value

to Several Major Countries of Destination

Period

Destination Country Value (Million USD) Share (%) Value (Million USD) Share (%)

Singapore 730 31.5 547 22.5

United States of America 193 8.3 308 12.7

European Union 186 8.0 259 10.7

Japan 367 15.9 229 9.4

Others 839 36.2 1,085 44.7

Total 2,315 100 2,428 100

Q2-2008 Q2-2009

In line with the positive growth of electronics

exports, the government plans to disperse the location

of electronic industries. Currently electronic industries

are concentrated in Java and Batam. In order to reach

the growth target of 7% in 2009, various incentives

had been implemented such as lowering Luxury Tax and

tightening of import procedures. Furthermore, the

Ministry of Industry will enhance product

standardization as a strategy in facing the free trade

era.

Rubber

Rubber exports was USD714 million in Q2/2009 or

recorded a negative growth of 56.7% (y.o.y) compared

to minus 57.9% in Q1/2009. The negative growth was

in line with the decreasing export volume by 16% and

the declining price by 40.0%.

However, compared to the preceding quarter, the

rubber price improved as reflected in the climbing price

in Q2/2009 to USD187.0 cent/kg compared to

USD165.8 cent/kg in Q1/2009. The rise in rubber price

was contributed by the high demand from China as the

major consumer in the world for raw material of tire. In

addition, the political turbulence in Thailand also driven

a price rise due to the uneasiness of investors caused by

the delay in rubber supply from this country, one of the

largest rubber producers in the world.

0 50 100 150 200 250 300 350

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

2007 2008 2009

c/kg

Chart 5 World Rubber Price

The main destinations of rubber exports in

Q2/2009 were China, the US, and Japan with market

shares of 32.2%, 15%, and 11.6% respectively.

Table 6

Value of Rubber Exports to Major Countries of Destination

Period

Destination Country Value (Million USD) Share (%) Value (Million USD) Share (%)

China 207 12.5 229 32.1

United States of America 460 27.9 107 15.0

Japan 280 17.0 83 11.6

Others 703 42.6 295 41.3

Total 1,650 100 714 100

Q2-2008 Q2-2009

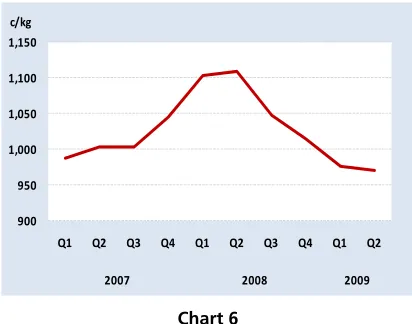

Shrimp

In Q2/2009 the shrimp exports was USD154

million or recorded a negative growth by 35.6% (y.o.y)

compared to minus 16.8% in Q1/2009. The decline of

shrimp exports was in line with the decreasing volume

of 73.6%. In addition, the ongoing slumping down of

shrimp price in the world market also contributed to the

decline of export value. In Q2/2009 shrimp price was

USD970 cent/kg, lower than USD1,112 cent/kg in

Q2/2008 and was also inferior to USD976 cent/kg in

11 900

950 1,000 1,050 1,100 1,150

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

2007 2008 2009

c/kg

Chart 6 World Shrimp Price

The major destinations of shrimp exports were

Japan (share 41.1%), the US (36.6%), and the

European Union (14%).

Table 7

Value of Shrimp Exports

to Several Major Countries of Destination

Period

Destination Country Value (Million USD) Share (%) Value (Million USD) Share (%)

Japan 81 33.9 64 41.6

United Staes of America 100 41.8 57 37.0

European Union 35 14.6 22 14.3

Others 23 9.6 11 7.1

Total 239 100 154 100

Q2-2008 Q2-2009

Copper

In Q2/2009 copper exports stood at USD1.4 billion

or grew by 3.8% (y.o.y), lower than 14.1% in Q1/2009.

The slowing down of copper export growth was caused

by, albeit starting to increase, lower price compared to

the previous year price. The copper price was

USD4,663/MTon in Q2/2009 contracted by 44.8% from

the previous year price (USD8,443/MTon).

3,000 4,000 5,000 6,000 7,000 8,000 9,000

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

2007 2008 2009

USD/MTon

Chart 7 World Copper Price

From demand side, copper exports were still

promising and marked with the increase in its export

volume by 48.1%. The demands mainly came from

Japan (30.9%), South Korea (15.1%), and India

(13.2%).

Table 8 Copper Export Value

to Several to Major Countries of Destination

Period

Destination Country Value (Million USD) Share (%) Value (Million USD) Share (%)

Japan 380 27.0 572 42.2

South Korea 193 13.7 230 17.0

India 2 0.1 202 14.9

Malaysia 153 10.9 122 9.0

Others 679 48.3 228 16.8

Total 1,407 100 1,354 100

Q2-2008 Q2-2009

Nickel

In Q2/2009 nickel exports was USD149 million or

contracted by 68.5% (y.o.y), better than minus 73.4%

in Q1/2009. This improvement was mainly supported

by the price rise to USD12,920/MTon, higher than

USD10.471/MTon in the preceding quarter. However, it

was still inferior to the price in Q2/2008

12 0 10,000 20,000 30,000 40,000 50,000 60,000

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

2007 2008 2009

USD/MTon

Chart 8 World Nickel Price

A discourse has currently been developed in nickel

market pertaining to the European Union resolution to

classify nickel as one of dangerous substances. By

putting pressures to the market of nickel, it seems that

this issue was brought up with the objective of

protecting the environment, people and products

manufactured by the countries in the region. Since

2008, a certification is required for nickel exports to the

European Union countries. Presently this discourse has

been submitted for the validation of the WTO. It is

petrified that this validation will affect the prospect of

Indonesia nickel exports considering that the European

Union is the potential market for nickel commodity

despite its still insignificant share. Other destination

countries for nickel exports were Japan (33.1%), China

(13.9%), and South Korea (10.9%).

Table 9

Nickel Export Value to Several Major Countries of Destination

Period

Destination Country Value (Million USD) Share (%) Value (Million USD) Share (%)

Japan 246 52.0 67 45.0

China 98 20.7 28 18.8

South Korea 33 7.0 22 14.8

Others 96 20.3 32 21.5

Total 473 100 149 100

Q2-2008 Q2-2009

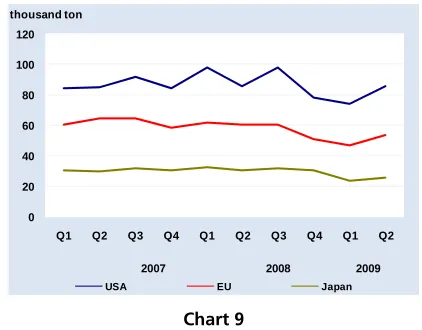

Textile and Textile Products

In Q2/2009 the export value of Textile and Textile

Product (TTP) was USD2.4 billion or negatively grew by

11.6% (y.o.y), improving compared to negative 13.9%

in Q1/2009. Despite the sharp drop in terms of value,

the volume only contracted by 1%. It was a result of

the switch of the demand for TTP of the US, the

European Union, and Japan from China to Indonesia.

0 20 40 60 80 100 120

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

2007 2008 2009

thousand ton

USA EU Japan

Chart 9

Volume of Textile and Textile Product (TTP) Exports to Several Major Countries of Destination

In order to increase export value, TTP industries

started to direct their export destinations toward the

high potential market of ASEAN countries. ASEAN

market currently absorbs 7% of Indonesian textile

products and therefore opportunities exist to be

developed. The major countries of destination for

Indonesian TTP were the US (35.8%), the European

Union (18%), and Japan (4.6%).

Table 10

TTP Export Value to Several Major Countries of Destination

Period

Destination Country Value (Million USD) Share (%) Value (Million USD) Share (%)

United States of America 971 36.4 845 35.8

European Union 479 17.9 425 18.0

Japan 132 4.9 109 4.6

Others 1,089 40.8 983 41.6

Total 2,671 100 2,362 100

Q2-2008 Q2-2009

With the objective of enhancing the performance

of Indonesian TTP industries, the government launched

a restructuring program of textile machinery. The

registration of this program started on April 1, 2009 up

to June 30, 2009. The mechanism of program

disbursement is classified into 2 (two) schemes. Scheme

I concerns the provision of discount facility in

purchasing machinery/equipment for TTP company

13

Scheme II is related to the low interest credit facility

through startup capital. According to the Director

General of Metal, Machinery, Textile and Multifarious

Industries, the Ministry of Industry allocated a budget of

Rp240 billion, divided into Rp213 billion for Scheme I

and Rp27 billion for Scheme II. In Scheme I, a 10%

discount will be provided for the total machinery price,

while assistance in Scheme II is related to financing loan

that will be provided under the condition that each

participating company makes an investment of

minimum Rp100 million and maximum Rp5 billion. The

source of financing will be as follows: 70% from the

Ministry of Industry, 10% from Lembaga Pengelola

Program (LPP), and 20% self financing, with 7%

interest during 5-years term. The number of companies

targeted to participate in this program is 200. If this

target is achieved it is expected that job opportunities

will be available for 22,000 people and the TTP

industries will be more efficient especially in energy

consumption.

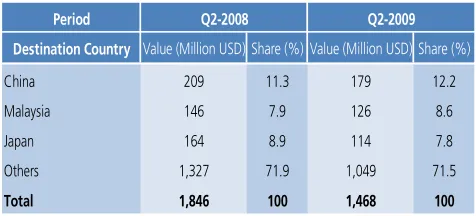

Chemical Products

In Q2/2009 export of chemical products was

USD1.5 billion or contracted by 20.5% (y.o.y), better

than minus 27.3% growth in Q1/2009. These falling

exports were in line with the sharp decrease of volume

by 40.6%. The reduced demand for chemical products

was mainly stemmed from China, Malaysia, and Japan.

Table 11

Export Value of Chemical Products to Several Major Countries of Destination

Period

Destination Country Value (Million USD) Share (%) Value (Million USD) Share (%)

China 209 11.3 179 12.2

Malaysia 146 7.9 126 8.6

Japan 164 8.9 114 7.8

Others 1,327 71.9 1,049 71.5

Total 1,846 100 1,468 100

Q2-2008 Q2-2009

Crude Palm Oil (CPO)

In Q2/2009 exports of CPO stood at USD2.1 billion

or contracted by 36.5% (y.o.y), better than minus

50.9% growth in Q1/2009. These falling exports were

due to the remain low price of CPO, while the volume

increased by 14.4%.

CPO price was USD744/MTon in Q2/2009, higher

than USD577/MTon in Q1/2009 but still lower than the

previous year (USD1,198/MTon). The strengthening

CPO price was mainly supported by the increased

demand from China and India as well as the increased

crude oil price in international market.

0 200 400 600 800 1,000 1,200 1,400

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

2007 2008 2009

USD/MTon

Chart 10 World CPO Price

In response to the strengthening of CPO price

during this period, the government set up an Export

Standard Price (HPE) of USD700/MTon with an export

duty of 3% starting from June 1, 2009. This export

duty will be valid for one month and subject to

reevaluation in the following month.

Export volume rose by 14.4%. Despite the

decreased exports to Pakistan and the European Union,

this situation was compensated by the considerable

demand from China and India. Drop of exports to

Pakistan were due to the import duty which was

applied higher for Indonesian CPO (10%) than CPO

from Malaysia (5%). In solving this problem, the

government tried to negotiate on a Preferential Trade

Agreement (PTA) with Pakistan with the objective of

enhancing CPO export volume to that country.

Table 12

14

to Several Major Countries of Destination

Period

Destination Country Value (Million USD) Share (%) Value (Million USD) Share (%)

India 1,081 32.7 769 36.6

China 393 11.9 361 17.2

European Union 478 14.5 246 11.7

Others 1,354 41.0 723 34.4

Total 3,306 100 2,099 100

Q2-2008 Q2-2009

1.2.

Non-Oil and Gas Imports

In Q2/2009 imports of non-oil and gas rose to

USD16.5 billion or higher than USD15.2 billion in

Q1/2009. Nevertheless, non-oil and gas imports during

this period posted a sharper negative annual growth of

30.6% compared to minus 28.8% in Q1/2009.

Imports of raw material posted the steepest

negative annual growth followed by imports of

consumption goods and capital goods. The decrease of

non-oil and gas imports was mostly caused by the

contracted volume as a consequence of the weakening

real domestic demand in Q2/2009.

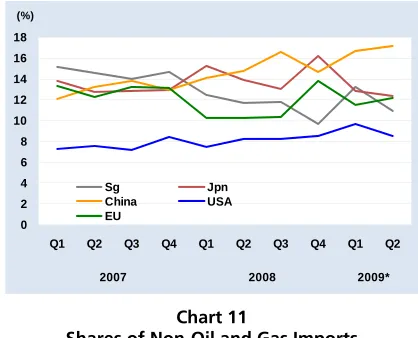

In Q2/2009 imports of non-oil and gas were mainly

originated from China (16.9%), Singapore (12.5%),

Japan (11.8%), the European Union (8.6%), and the US

(8.4%). Major imported commodities were

telecommunication equipment from China, electronics

equipment from Singapore, road vehicles from Japan,

and other means of transportation from the European

Union and the United States.

0 2 4 6 8 10 12 14 16 18

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

2007 2008 2009*

Sg Jpn

China USA

EU (%)

Chart 11

Shares of Non-Oil and Gas Imports Based on Major Countries of Origin

The imports of raw material were USD11.7 billion

in Q2/2009 or drop by 36.7% from the previous year

(Q1/2009: -36.9%). This negative growth signaled the

still weak demand for imports of raw materials for

exports and domestic consumption that put pressure to

import value in this period.

Table 13

Major Non-Oil and Gas Commodities Imported from Major Countries of Origin (based on 2digit SITC code, as a% shares of total non-oil and gas imports)

Commodity Share Commodity Share Commodity Share Commodity Share Commodity Share

Telecommunication Device 2.4 Electronic Machines 1.8 Vehicles 2.1 Other Transportation Vehicles 1.7 Other Transportation Vehicles 1.9

Electronic Machines 1.5 Other Transportation Vehicles 1.2 Iron and Steel 1.3 Public Industrial Machines 1.0 Nuts & Oil Seeds 0.8

yarn, fabrics, and textile produc 1.2 Paper 1.1 Public Industrial Machines 1.2 Certain Industrial Machines 0.7 Public Industrial Machines 0.6

Energy Generating Machine 1.2 Public Industrial Machines 1.0 Certain Industrial Machines 1.0 Electronic Machines 0.5 Textile Fibers 0.5

15

Imports of raw materials were generally from

China (13.7%), Singapore (13.2%), and Japan (12.6%).

Table 14

Import Value of Raw Materials Based on Country of Origin (C&F)

Period

Destination Country Value (Million USD) Share (%) Value (Million USD) Share (%)

China 2,353 12.7 1,612 13.7

Singapore 2,261 12.2 1,550 13.2

Japan 2,567 13.8 1,479 12.6

Others 11,376 61.3 7,104 60.5

Total 18,557 100 11,745 100

Q2-2008 Q2-2009

In Q2/2009 imports of consumption goods was

USD1.6 billion (C&F) or grew negatively by 31.3%

(y.o.y) compared to minus 39.8% in Q1/2009. The

decline in imports of consumption goods was in line

with the weak domestic demand. Imports of

consumption goods were mainly from China (31.6%),

Thailand (12.9%), and India (6.5%).

Table 15

Import Value of Consumption Goods Based on Countries of Origin (C&F)

Period

Destination Country Value (Million USD) Share (%) Value (Million USD) Share (%)

China 629 38.7 645 39.7

Thailand 480 29.5 263 16.2

India 75 4.6 132 8.1

Others 441 27.1 585 36.0

Total 1,625 100 1,625 100

Q2-2008 Q2-2009

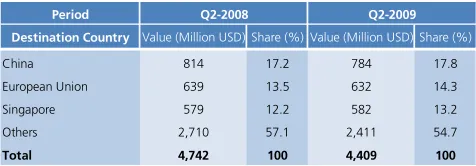

Meanwhile imports of capital goods were USD4.4

billion in Q2/2009 or contracted by 7% compared to

6.6% in Q1/2009. Despite this negative growth, the

decrease was slower than the contraction of other

group of products. This situation was contributed by

the high imports of air transportation and automotive

equipment. Imports of capital goods were mainly from

China (18.8%), the European Union (15.2%), and

Singapore (14%).

Table 16

Import Value of Capital Goods Based on Country of Origin (C&F)

Period

Destination Country Value (Million USD) Share (%) Value (Million USD) Share (%)

China 814 17.2 784 17.8

European Union 639 13.5 632 14.3

Singapore 579 12.2 582 13.2

Others 2,710 57.1 2,411 54.7

Total 4,742 100 4,409 100

Q2-2008 Q2-2009

Almost all of the 15 biggest non-oil and gas import

products recorded negative growth except airplane and

its equipment. Several products recorded negative

import growth rate higher than Q1/2009 such as

telecommunication equipment, processed steel

products, construction/civil engineering equipment, and

electrical equipment.

Table 17

16

2. Oil and Gas Trade Balance

In Q2/2009 the oil and gas trade balance recorded

a surplus of USD2.1 billion, higher than a USD1.6 billion

surplus in Q1/2009. Both oil trade balance and gas

trade balance improved. After experiencing deficit for a

long time, oil trade balance posted a surplus of USD69

million.

The surplus on gas trade balance was higher due

to the trend of increasing gas price pursuant to the

world oil price movement. The positive price effect was

much stronger than the negative volume effect in which

demand for gas weakened in response to the world

economic slowdown.

2.1. Oil

The increasing oil prices started to bring an

advantageous effect to the oil trade balance in

Q2/2009. In the reporting period the oil trade balance

recorded a USD69 million surplus compared to USD155

million deficit in Q1/2009. The surplus was mainly

resulted from the increase in crude oil exports.

Table 18 Oil Exports and Imports

Export 41.2 1,817 41.5 2,405

Crude Oil 31.5 1,328 42.2 31.6 1,775 56.2

Refinery Products 9.8 490 50.1 9.9 630 63.9

Import 39.6 1,973 40.1 2,337

Crude Oil 18.7 744 39.8 17.3 857 49.4

Refinery Products 20.9 1,228 58.7 22.8 1,480 65.0

Oil Trade Balance ‐155 69

Source: BPMigas and PT Pertamina (processed) Volume (mbbl)

Value (million USD)

Price (USD/barrel) Details 2009 Q1 Q2 Volume (mbbl) Value (million USD)

Price (USD/barrel)

Oil exports during the reporting period rose to

USD2.4 billion or increased by 33.2% compared to the

preceding quarter (USD1.8 billion). As previously

stated, the higher oil exports were primarily affected by

oil price. This was reflected from the slight increase in

oil export volume but in terms of value recorded a

relatively considerable increase. Based on types of

export product, crude oil export volume increased from

31.5 million barrel in Q1/2009 to 31.6 million barrel in

Q2/2009. Exports of oil product increased from 9.8

million barrel in Q1/2009 to 9.9 million barrel in

Q2/2009.

Indonesian crude oil export destinations (with share

of 70% of total oil exports) were mainly Japan,

Australia, Singapore, and Korea. Among the existing

48 types of domestic crude oil, the largest export

volumes were SLC, Duri, Senipah and Belanak.

From import side, oil value in Q2/2009 was USD2.3

billion, also higher than the preceding quarter value of

USD2.0 billion. Similar to the export trend, this increase

was also contributed by the rise in oil prices. In average

oil import1

price increased from USD49.2/barrel to

USD65.3/barrel and oil import volume showed a slight

increase from 39.6 million barrel to 40.1 million barrel.

Imports of crude oil for refinery intake were mainly

originated from Saudi Arabia with ALC (Arab Light

Crude) oil type and followed by crude oil from Brunei,

Africa and Malaysia. These types of oil were used for

the need of Cilacap refinery as well as refineries in

Balikpapan and Balongan.

Table 19

Demand and Supply of World Oil

Q1 Q2 Q3 Q4 Q1 Q2

Oil Demand

North America 25.5 24.8 24.5 23.7 24.1 23.5 22.9

China 7.6 8.0 8.2 8.1 7.7 7.6 8.3

West Europe 15.3 15.2 14.9 15.4 15.3 14.9 14.4

Others 37.5 38.7 37.8 37.8 38.1 37.9 37.4

Total Oil Demand 85.9 86.7 85.4 85.0 85.2 83.9 83.0

Oil Supply

OPEC 30.1 31.2 31.2 31.5 30.3 28.3 28.4

Non OPEC 54.5 55.0 55.0 54.2 54.9 55.6 55.0

Total Oil Supply 84.6 86.3 86.3 85.7 85.2 83.9 83.4

Netto Demand ‐ Supply ‐1.2 ‐0.4 0.9 0.8 0.0 0.0 0.4

Source: OPEC

Details (in mbpd) 2007

2008 2009

With reference to the oil price, the rise in

Indonesian crude oil export price was closely linked to

the average development of OPEC and WTI basket

crude oil prices in which both reaching USD42.9 per

barrel, higher than the preceding quarter. Several

international institutions projected that the improved

world economic condition in 2010 and the decreased

production of world oil supported the hike in oil prices.

17 30 40 50 60 70 80 90 100 110 120 130 140

J J A S O N D J F M A M J J A S O N D J F M A M J

2007 2008 2009

USD/barel

SLC Export Price WTI OPEC

Source: OPEC, Ditjen Migas

Chart 12 World Oil Prices

The average of Indonesian oil production reached

0.941 million barrel per day, lower than the average

production of the preceding quarter (0.962 million

barrel per day). The average production was below the

target stated in the 2009 government budget or

APBN-P 2009 (0.960 million barrel per day).

Oil consumption during Q2/2009 increased (84.9

million barrels) compared to Q1/2009 (80.7 million

barrels). Pertaining to user sectors, the rise in oil

consumption were registered in industrial, electrical,

and transportation sectors while the use in household

sector showed a decrease. The oil consumption did not

increase sharply due to the ongoing conversion

program to replace fuels with LPG and coal and the

slowing domestic economy.

7.2 7.4 7.6 7.8 8.0 8.2 8.4 8.6 0.0 0.5 1.0 1.5 2.0 2.5 3.0 3.5

Q1 Q2 Q3 Q4 Q1 Q2 2008 2009 Household

Industry Electricity Transportation (RHS)

billion litre billion litre

Sumber: Pertamina

Chart 13 Oil Consumption

2.2. Gas

A surplus on gas trade balance increased to

USD2.0 billion from USD1.9 billion in Q1/2009. The

higher surplus was driven by the growing trend of gas

price as reflected by the gas export price at the end of

June 2009 that had already increased by 32.3%2

compared to the price in March 2009.

Table 20

Exports of LNG, LPG and Natural Gas

Q1 Q2 Q3 Q4 Q1 Q2

LNG

Volume (mmbtu) 1,080 284 253 259 272 257 228 Value (million USD) 9,723 3,275 3,462 3,699 2,350 1,417 1,483 Price (USD/mmbtu) 9 12 13 14 9 5 6

LPG

Volume (000 metric ton) 337 66 35 0 0 0 0 Value (million USD) 210 51 28 0 0 0 0 Price (USD/MTon) 605 777 802 0 0 0 0

Natural Gas

Volume (mmbtu) 293 69 78 84 74 78 77 Value (million USD) 2,443 747 978 1,164 580 441 565 Price (USD/mmbtu) 8 11 12 14 8 6 7

Gas Trade Balance 12,407 4,073 4,501 4,945 3,000 1,926 2,048

Export (million USD) 12,376 4,073 4,468 4,863 2,929 1,858 2,048 Import (million USD) ‐31 0 ‐34 ‐82 ‐70 ‐67 0

Source: BPMigas

Details 2007 2008 2009

The impact of global crisis on the demand for gas

from the major destination countries (Japan, Korea, and

Taiwan) decreased LNG export volume from 256.8

mbtu to 228.1 mbtu.

Gas exports still maintained its high potential due

to Indonesia’s current gas reserves of 170.1 TSCF

(trillion standard cubic feet) which consist of 112.5 TSCF

of proven reserves and 57.7 TSCF of potential reserves.

Gas reserves in 2008 was higher compared to 2007.

18

Table 21

Indonesia’s Gas Reserves (billion cubic feet) Year

Reserves

Proven 91 91 97 94 106 113 Potential 87 98 89 93 59 58 Total 178 188 186 187 165 170

2007 2008

2003 2004 2005 2006

3. Services Account

The deficit on services account in Q2/2009 reached

USD3.2 billion, higher than the deficit in the preceding

quarter (deficit of USD2.5 billion). The increased deficit

was mainly triggered by the increase in import freights

and was consistent with the increase in imports

compared to the previous quarter. In addition, several

other services imports still showed an increase

compared to Q1/2009 such as construction services and

computer and information services. Meanwhile, net

travel services still managed to maintain the same level

of surplus as the preceding quarter.

-3500 -3000 -2500 -2000 -1500 -1000 -500 0 500 1000

Q.1 Q.2 Q.3 Q.4 Q.1 Q.2 Q.3 Q.4 Q.1 Q.2

2007 2008* 2009**

Transportation Travel Other services Services, net

million USD

Chart 14 Services Account

Transportation services recorded a higher deficit of

USD1.9 billion than that in Q1/2009 (USD1.7 billion).

This increased deficit was originated from freight

services rising from USD1.5 billion to USD1.7 billion in

line with the hike in import volume. The high deficit on

transportation services was related to the domination of

foreign fleet in transportation of import products. The

empowerment of national shipping industry in

supporting international trade through the obligation to

use domestic fleet in shipping national commodities

was still difficult to be implemented.

Tourism sector (travel services) remained at the

same rate as in Q1/2009 by posting a surplus of USD0.3

billion in Q2/2009. The surplus was contributed by the

foreign exchange receipts from international travelers

climbing from USD1.4 billion to USD1.6 billion. This

increased surplus, however, was offset by foreign

exchange expenses by Indonesian travelers abroad

mounting from USD1.1 billion to USD1.3 billion.

The number of international travelers visiting

Indonesia (inbound) reached 1,590 thousand people

increased from 1,464 thousand people in Q1/2009. This

increase reflected that Indonesia was still an interesting

travel destination amidst the slowing global economic

growth. Several international tourism agenda also

supported the growth of international travelers such as

the World Ocean Congress (WOC), the Coral Triangle

Initiatives, and the 42nd

Annual General Meeting of

Asian Development Bank (ADB) in Bali, that all took

place in May 2009.

In Q2/2009 the countries of origin of international

travelers were still dominated by Singapore (18%),

Malaysia (16%), Australia (10%), Japan (7%), and

China (6%). Three out of these five countries namely

Malaysia, Australia, and China showed a positive

growth during the reporting period. Travelers from

Saudi Arabia and France grew significantly by 40%

(y.o.y) albeit their shares were still relatively small.

The main destinations of travelers visiting

Indonesia were Bali with 44% share, followed by

Jakarta (26%), and Batam (18%). The countries having

the largest number of travelers visiting Bali were

Australia (17%), Japan (13%), China (8%), and France

19 -600 -400 -200 0 200 400 600 800 -600 -500 -400 -300 -200 -100 0 100 200 300 400 500 600 700

J F M A M J J A S O N D J F M A M J J A S O N D J F M A M J

2007 2008 2009

million USD

Inbound (thousand people) Outbound (thousand people)

Trav. Balance (thousand people) Inflows (million USD) RHS

Trav. Balance (million USD) RHS Outflows (million USD) RHS thousand people

Chart 15 Travel Services

The number of Indonesians going abroad also

grew to 1,289 thousand people or higher 13% than

the preceding quarter (1,142 thousand people). This

rise was followed by an increase in foreign exchange

travel expenses to USD1.2 billion, from USD1.1 billion in

the previous quarter.

Neighbouring ASEAN countries still remained the

main destination of Indonesian travelers such as

Singapore (44%), Malaysia (25%), and Thailand (4%).

While Australia (6%) and the US (4%) were the main

destination of Indonesian travelers outside ASEAN

countries. The annual growth of Indonesian travelers

visiting Singapore contracted in May 2009 while those

visiting Malaysia increased.

According to the information from Malaysia

Tourism Promotion Board (MTPB), the number of

Indonesian tourists visiting Malaysia slightly increased by

3.1% (y.o.y) reaching 195 thousand from a total of

1.89 million. Singapore Tourism Board reported that the

number of Indonesian tourists decreased by 5.9%

(y.o.y) reaching 129 thousand from a total of 725

thousand.

4. Income Account

In Q2/2009 the income account recorded a USD3.7

billion deficit, higher than USD2.7 billion deficit in

Q1/2009. Deficit on income account reflected a higher

resident’s liabilities to non-resident than resident’s

claims on non-resident. The higher deficit was

contributed by the increased deficits on other

investment income, portfolio investment income as well

as direct investment income.

-6,000 -5,000 -4,000 -3,000 -2,000 -1,000 0

Q.1 Q.2 Q.3 Q.4 Q.1 Q.2 Q.3 Q.4 Q.1 Q.2

2007 2008* 2009**

Income, net Inv. Income DI Income PI Income OI Income

million USD

Chart 16 Income Account

Other investment income posted a deficit of

USD0.9 billion, higher than USD0.4 billion in the

preceding quarter. This deficit was triggered by a

scheduled increase in interest payments of government

external debt.

The deficit on net portfolio investment income rose

to USD0.7 billion from USD0.4 billion deficit in

Q1/2009. This increased deficit was as a result of a rise

in dividend payments on securities owned by foreign

investors to USD0.4 billion from USD0.1 billion. The

increased payments of dividend were consistent with

the growth of foreign ownership of domestic shares in

the previous periods.

The deficit on direct investment income also

widened to USD2.1 billion from USD1.7 billion in

Q1/2009. This higher deficit was due to the increased

profit transfers reported by oil and gas companies

(Contractor of Production Sharing Contract) from

USD0.6 billion to USD0.8 billion.

5. Current Transfers

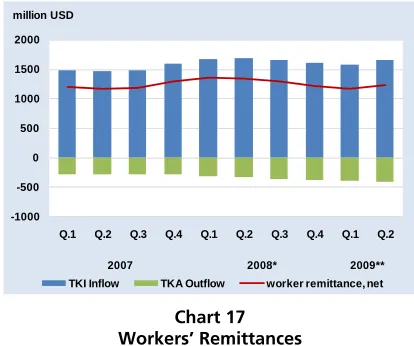

The current transfers in Q2/2009 posted a USD1.2

billion surplus, slightly higher than USD1.1 billion in

20

contributed by remittances from Indonesian workers

abroad amounting to USD1.8 billion, slightly increased

from USD1.7 billion in the preceding period. Outflows

of remittances by foreigners working in Indonesia

reached USD423 million in Q2/2009, higher than

USD404 million in Q1/2009.

-1000 -500 0 500 1000 1500 2000

Q.1 Q.2 Q.3 Q.4 Q.1 Q.2 Q.3 Q.4 Q.1 Q.2

2007 2008* 2009**

TKI Inflow TKA Outflow worker remittance, net million USD

Chart 17 Workers’ Remittances

The placement of Indonesian workers abroad

reached 158.2 thousand people in Q2/2009, 1.5%

lower than the placement in Q1/2009. This was as a

result of a fall in demand for Indonesian workers

especially from countries in Asia-Pacific region such as

Malaysia, Singapore, and Taiwan. On the contrary, the

placement of Indonesian workers in the Middle East

region especially in Saudi Arabia and Bahrain increased.

The number of Indonesian workers abroad at the

end of Q2/2009 were 4.39 million, lower than 4.42

million at the end of Q1/2009. This decrease was driven

by the falls in total placements of both formal and

informal workers. Placement of formal Indonesian

workers posted a steep drop compared to informal

workers. This was considered as a result of global

financial crisis negatively affecting the economy of the

placement destination especially in the Asia-Pacific

region.

The other component contributing to the surplus of

current transfers was the inflows of non-investment

grants in the form of aids of non-durable goods such as

food, clothes and medicines. Inflows of grants reached

USD32 million, lower than USD73 million in Q1/2009.

The grants received by the Government amounting to

USD15 million, higher than USD4 million in the

preceding quarter. The grants received by NGO was

USD17 million, lower than USD69 million in the

previous quarter.

In Q2/2009 several activities financed by foreign

grants were, among others, technical assistance from

Norway with an agreement signed at the end of April

2009 for the implementation of capacity building in

Fisheries and Aquaculture. Technical assistance from

ADB related to the bureaucracy reformation of central

and regional government was agreed in April 2009.

Table 22 Non-Investment Grant

(million USD)

Investment Grants

(Capital Transfer)

Total 17 61 186 29 19 29

Public (Govt.) 4 6 7 3 2 3

Private (NGO) 13 55 179 26 17 26

Source: Indonesian Ministry of Finance, United Nations

2008* 2009**

21

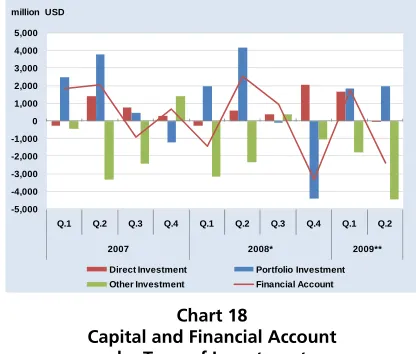

The capital and financial account posted a USD2.4

billion deficit in Q2/2009 after recording a USD1.8

billion surplus in Q1/2009. This deficit was stemmed

from decreased inflows of direct investment, increased

domestic bank and bank placements in

non-resident banks abroad, and the increase in external debt

repayments by the government. The falls in direct

investment inflows were consistent with the slowing

growth of domestic economy.

Within the capital and financial account, the

portfolio investment still recorded a robust surplus

compared to the previous quarter. The renewed

investor confidence in Indonesian economic stability and

the calm, orderly national elections were several factors

contributing to the improved performance of portfolio

investment.

-5,000 -4,000 -3,000 -2,000 -1,000 0 1,000 2,000 3,000 4,000 5,000

Q.1 Q.2 Q.3 Q.4 Q.1 Q.2 Q.3 Q.4 Q.1 Q.2

2007 2008* 2009**

Direct Investment Portfolio Investment

Other Investment Financial Account

million USD

Chart 18

Capital and Financial Account by Type of Investment

1.

Capital Account

The capital account in Q2/2009 recorded a USD29

million surplus, higher than a surplus of USD19 million

in the previous quarter. This surplus was contributed by

the investment grants, such as those for construction of

housing, bridges, roads, schools, and others. The entire

grants were provided in the framework of aids for

natural disaster’s victims in several locations of

Indonesia. Most of the grants (90%) were distributed

through private sector (NGO) amounting to USD26

million, while the rest were through public sector

(government) amounting to USD3 million.

The investment grants were represented among

others by the aid from Global Partnership on

Output-Based Aid (GPOBA) through the World Bank for the

development of internet access for the people living in

isolated areas in Java and Sumatera which was signed in

April 2009 between GPOBA and Indonesian

government (Ministry of Communication and

Information).

Table 23 Investment Grant

(million USD) Investment Grants

(Capital Transfer)

Total 17 61 186 29 19 29

Public (Govt.) 4 6 7 3 2 3

Private (NGO) 13 55 179 26 17 26

Source: Indonesian Ministry of Finance, United Nations

2008* 2009**

Q1 Q2 Q3 Q4 Q1 Q2

2.

Financial Account

The financial account in Q2/2009 posted a deficit

of USD2.4 billion compared to a surplus of USD1.7

billion in Q1/2009. This was due to the deficits on other

investment and direct investment while portfolio

investment still posted a surplus.

The financial account deficit was primarily due to a

low direct investment inflows and increased domestic

bank and non-bank placements in non-resident banks

abroad as well as a scheduled rise in the government’s

foreign debt repayments. The slowing down of

22

domestic economic growth resulted on the low demand

for foreign financing.

The surplus on portfolio investment account in

Q2/2009 was contributed by the issuance of

Government Sharia Securities (SBSN) or Government

Sukuk in foreign currency. Moreover, there were

renewed foreign investor interest in

denominated securities, especially the

rupiah-denominated Government Bonds, Bank Indonesia

Certificates (SBIs), and domestic shares.

-4,000 -3,000 -2,000 -1,000 0 1,000 2,000 3,000 4,000

Q.1 Q.2 Q.3 Q.4 Q.1 Q.2 Q.3 Q.4 Q.1 Q.2

2007 2008* 2009**

Public sector Private sector Capital & financial account

million USD

Chart 19

Capital and Financial Account by Sector

2.1 Public Sector

Public sector’s financial account recorded a USD0.3

billion deficit during Q2/2009, in contrast with a

USD2.8 billion surplus in the preceding quarter. The

deficit was as a result of public other investment deficit

that was exceeded the surplus of public portfolio

investment.

Although posted a lower surplus than the

preceding period (USD2.8 billion), portfolio investment

of public sector during the reporting period still

managed to record a surplus of USD1.8 billion. This

surplus was resulted from the increase in foreign

investment inflows through the purchase of

rupiah-denominated government bonds (SUN) and Certificate

of Bank Indonesia (SBI) as well as the issuance of

government Sukuk in foreign currency.

The ongoing inflows of portfolio investment in

Q2/2009 were consistent with the increase in credit

rating outlook by Moody’s from stable to positive.

Moody’s underlined several contributing factors to this

situation such as the strong prospect of economic

growth, effective policy framework that mitigated the

impact of economic turbulence and sustained economic

resilience, internal political stability, improved credit

fundamental as reflected in the falling external debt

figures, positive trade balance, external financing

sustainability as well as banking liquidity adequacy and

adequate capital support.

The purchases of public sector

rupiah-denominated securities (SBI and SUN) by foreign

investors recorded net surplus during the reporting

period. Foreign investment transactions on SBI posted a

net surplus of USD420 million, lower than the net

surplus of the preceding period (USD700 million). SUN

transactions by foreign investors also recorded a net

surplus of USD743 million, in contrast with the net

deficit occurred in the preceding period (USD 809

million). -4000 -3000 -2000 -1000 0 1000 2000 3000 4000 5000

Q.1 Q.2 Q.3 Q.4 Q.1 Q.2 Q.3 Q.4 Q.1 Q.2

2007 2008* 2009**

Portfolio Investment Other Investment Financial Account

million USD

Chart 20

Financial Account of Public Sector

The strengthened portfolio investment transactions

by foreign investors were inseparable from the

improving condition of global financial sector. Liquidity

squeeze continued to ease supported by liquidity

injection following the quantitative easing policy

23

performed by the central banks such as the Fed, the

BOE, the BOJ, and the ECB was successful to ease credit

market squeeze as reflected by a decline of the spread

between Libor and Overnight Index Swap (OIS) to the

level before Lehman Brother’s bankruptcy. The financial

sector improvement was also shown by the Fed’s stress

test result concluding that the US banking relatively <