THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S. GOVERNMENT POLICY GAIN Report Number:

Farmgate prices for rice and corn are under downward pressure as MY2017/18 supplies enter the market. The government is considering additional measures to protect domestic corn farmers. Lower rice prices will continue to assist Thai rice exports which are on track to reach a record 11 million metric tons.

Ponnarong Prasertsri, Agricultural Specialist Paul Welcher, Agricultural Attaché

October 2017

Grain and Feed Update

Thailand

Post:

Executive Summary:

Rice prices are under downward pressure as supplies of MY2017/18 main crop rice enter the market. This will help maintain Thai rice exports in the last quarter of 2017 as Thai rice export prices have converged with other competitors. The government has proposed a soft loan program for farmer institutions to purchase domestic corn at a recommended price that is 37 percent above the market price. The government is also considering increasing the import tariff on feed wheat to help protect corn farmers.

Post’s supply and demand forecast for rice, corn, and wheat remains unchanged from the previous

forecast in September 2017.

1. Rice Update 1.1 Production

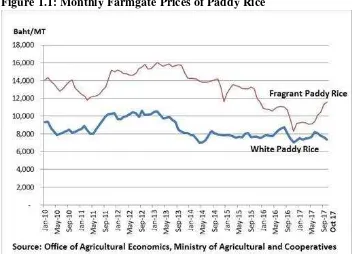

Rice prices are under downward pressure as supplies of MY2017/18 main crop rice enter the market. In October 2017, farmgate prices for white paddy rice declined 3-4 percent from the previous month (Figure 1.1). Farmgate prices for fragrant paddy rice leveled off in October, ending the trend of rising prices that occurred between July to September 2017. According to the Geo-Informatics and Space

Technology Development Agency’s (GISTDA) estimate, approximately 80 percent of MY2017/18 main crop rice production will be harvested between mid-November and mid-December 2017. The Ministry of Agriculture and Cooperative estimates that damage from flooding between July – October 2017 will be minimal at around 1.4 million rai (224,000 hectares), accounting for approximately 2 percent of the total main crop rice planted area.

Post’s forecast for MY2017/18 rice production remains unchanged at 20.4 million metric tons. This is approximately a 6 percent increase from MY2016/17. Additionally, MY2017/18 off-season rice production is expected to increase 5 percent from the previous year due to sufficient water supplies. The Royal Irrigation Department reported on October 25, 2017, that water supplies in the major

reservoirs totaled 13.7 billion cubic meters, which is 46 percent above last year’s water levels (Figure

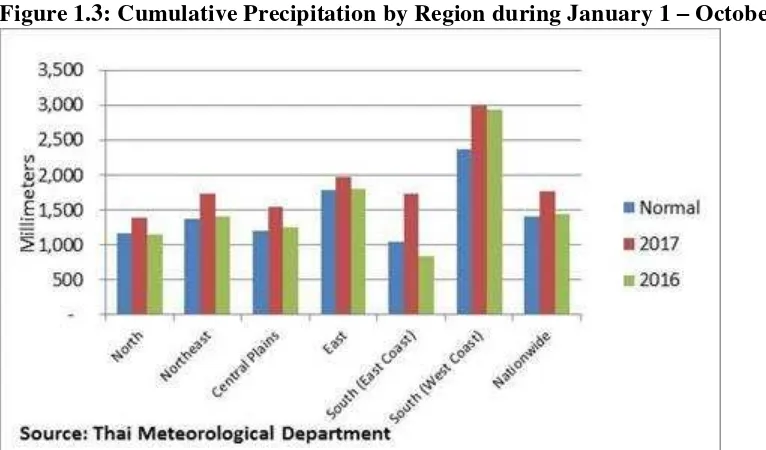

1.2). According to the Thai Meteorological Department, cumulative precipitation during January – October 2017 is 27 percent above the normal average and 23 percent above last year’s rainfall levels (Figure 1.3).

Figure 1.2: Water Supplies in Major Reservoirs

1.2 Trade

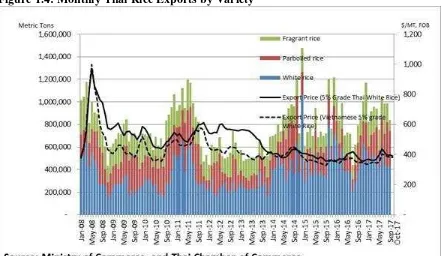

According to the Ministry of Commerce, Thai rice exports from January – September 2017 totaled approximately 8.2 million metric tons, up 20 percent from the same period last year due mainly to increased parboiled rice exports to Africa and the Middle East. During this time span, parboiled rice exports totaled 2.2 million metric tons, up 51 percent from the same period last year. The recovery in MY2016/17 off-season white rice production has caused Thai parboiled rice to be competitive with Indian rice. Also, fragrant and white rice exports increased approximately 10 percent from the same period last year, totaling 3.7 and 2.0 million metric tons respectively, due to the sale of government rice stocks.

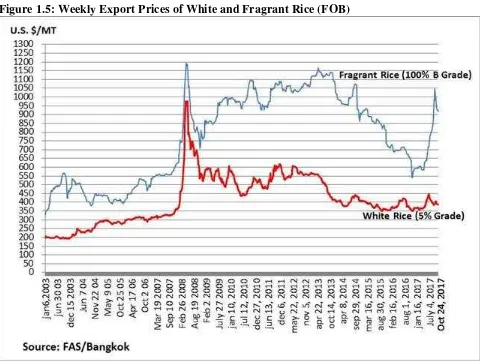

Downward pressure on Thai rice prices from new main crop rice supplies has caused Thai rice prices to converge with competitors (Figure 1.4). As a result, Thai rice will likely continue to be competitive in foreign markets and traders expect that Thailand will continue to export a monthly average of 0.9 million metric tons in the last quarter of 2017. In October 2017, export prices of Thai rice are U.S. $920-940/MT for fragrant rice and U.S. $355-390/MT for white rice, compared to respectively U.S. $980-1,000/MT and U.S. $360-400/MT in the previous month (Figure 1.5).

Figure 1.4: Monthly Thai Rice Exports by Variety

Figure 1.5: Weekly Export Prices of White and Fragrant Rice (FOB)

2. Corn Update

The government is considering a 45 billion baht (U.S $1.4 billion) soft loan program for farmer

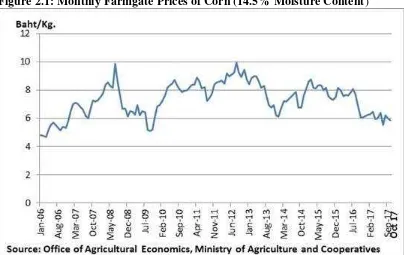

institutions (agricultural cooperatives) to purchase domestic corn at 8 baht per kilogram (U.S. $240/MT) which is 37 percent above current market prices. The proposed soft loan program’s objective would be to raise the domestic price of corn, but there are concerns over the proposed program’s effectiveness as the difference between the purchase price and the market price is greater than the reduced interest rate. In October 2017, farmgate prices of corn declined to 5.9 baht per kilogram (U.S. $178/MT), down 3 percent from the same period last year (Figure 2.1).

Figure 2.1: Monthly Farmgate Prices of Corn (14.5% Moisture Content)

3. Wheat Update

Appendix Tables

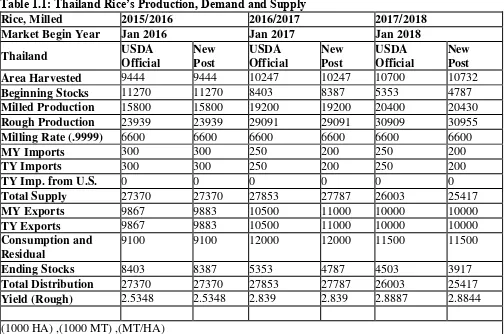

Table 1.1: Thailand Rice’s Production, Demand and Supply

Rice, Milled 2015/2016 2016/2017 2017/2018

Market Begin Year Jan 2016 Jan 2017 Jan 2018

Thailand USDA

Official

Milled Production 15800 15800 19200 19200 20400 20430

Rough Production 23939 23939 29091 29091 30909 30955

Milling Rate (.9999) 6600 6600 6600 6600 6600 6600

Total Distribution 27370 27370 27853 27787 26003 25417

Yield (Rough) 2.5348 2.5348 2.839 2.839 2.8887 2.8844

(1000 HA) ,(1000 MT) ,(MT/HA)

Table 1.2: Thailand’s Rice Area, Production and Yield

Table 2: Thailand’s Corn Production, Demand and Supply

Corn 2015/2016 2016/2017 2017/2018

Market Begin

Thailand USDA

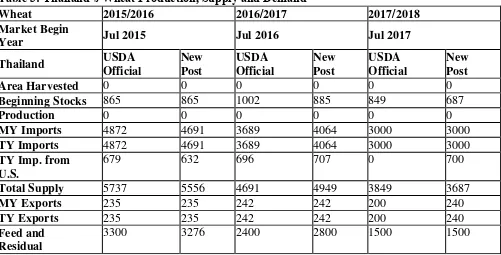

Table 3: Thailand’s Wheat Production, Supply and Demand

Wheat 2015/2016 2016/2017 2017/2018

Market Begin

Year Jul 2015 Jul 2016 Jul 2017

Thailand USDA

FSI

Consumption

1200 1160 1200 1220 1300 1300

Total

Consumption

4500 4436 3600 4020 2800 2800

Ending Stocks 1002 885 849 687 849 647

Total

Distribution

5737 5556 4691 4949 3849 3687

Yield 0 0 0 0 0 0

(1000 HA) ,(1000 MT) ,(MT/HA)

End of report.