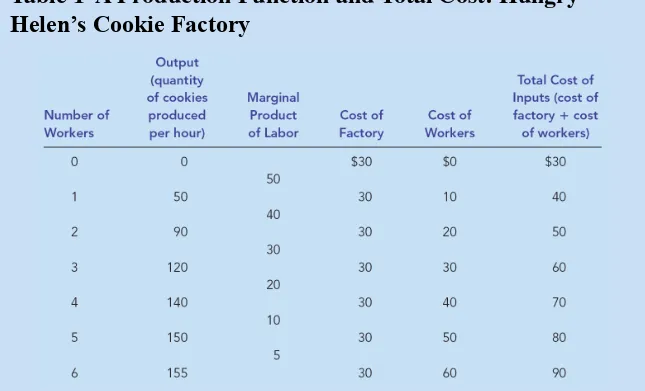

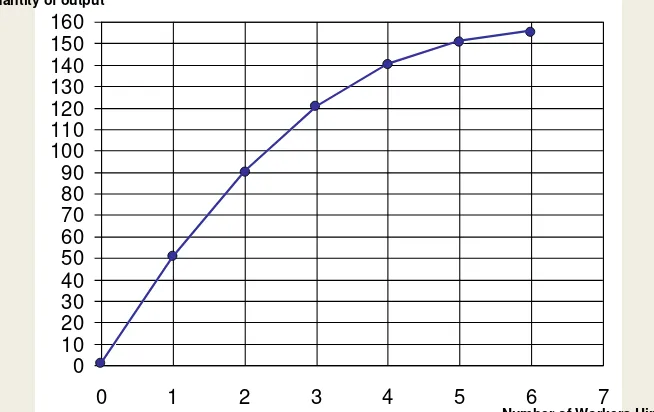

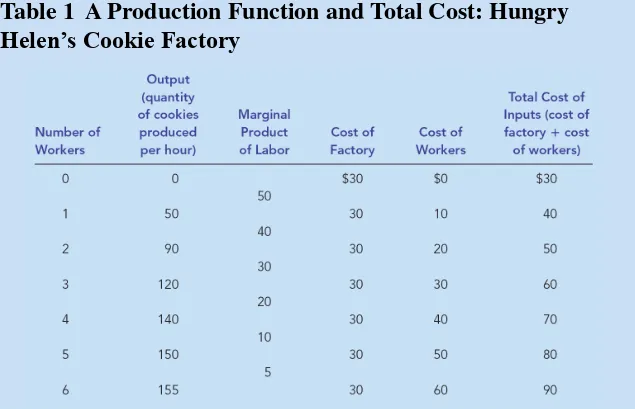

The Costs of Production

Teks penuh

Gambar

Dokumen terkait

In a training program, an athlete must eat 154 eggs, during a period of time from November 8th till November 14th.. Every day in this period he must eat 6 more eggs than the

Pada penelitian ini, digunakan untuk mengetahui seberapa besar hubungan antara variabel fasilitas, kualitas layanan, dan potongan harga terhadap variabel kepuasan konsumen..

Hal ini akan membantu perekonomian Indonesia, agar tidak mengandalkan Negara lain untuk memproduksi barang jadi dan jika terjadi turbulensi ekonomi glogal tidak berpengaruh

Menurut Konvensi Jenewa 1958 istilah yang digunakan bukan pesawat udara sipil dan pesawat udara negara, melainkan pesawat udara militer atau pesawat udara dinas pemerintah

Skripsi pada Jurusan Pendidikan Bahasa dan Sastra Indonesia, FPBS

2) Secara umum siswa di SMA Negeri 1 Bulukumba belum memiliki perencanaan karir yang baik. 3) SMA Negeri 1 Bulukumba memiliki wifi yang dapat dimanfaatkan oleh para

[r]

Pada tulisan in i dibatasi pembahasan mengenai efisiensi dengan adanya perubahan tegangan lenninal akibat perubahan beban pada generator sinkron 3 fasa rotor salient