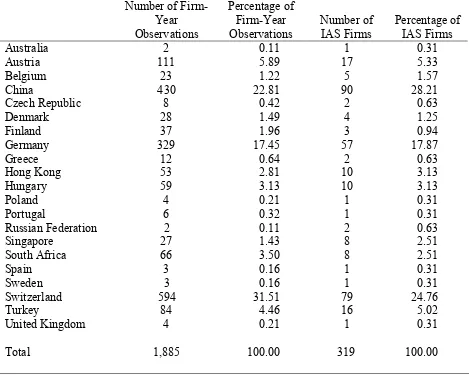

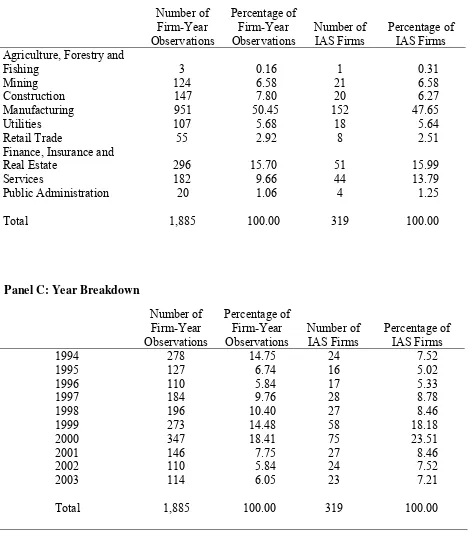

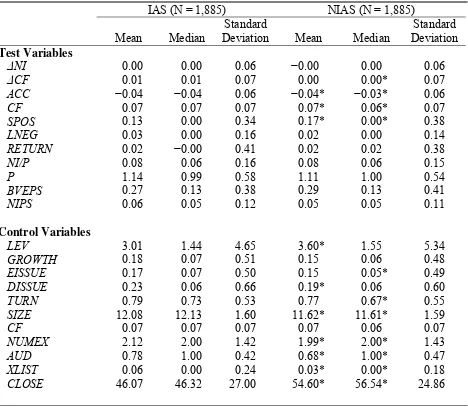

International Accounting Standards and Accounting Quality

Teks penuh

Gambar

Dokumen terkait

I went to their house, terri ed I would not be a good interviewer and that they wouldn’t like me, and they took me in, patted my back, and talked to me as if they’d known me for

Alhamdulillah berkat doa dan semua dukungan yang eyang beri ke Bram, Bram dapat menyelesaikan skripsi ini dengan lancar ( selama 4 tahun ) Eyang Kakung dan Eyang Ti adalah

Pilihlah jawaban yang saudara anggap paling benar dengan cara menghitamkan salah satu huruf a, b, c atau d pada lembar jawaban dari kalimat pernyataan dibawah ini..

ANALISIS NERACA AIR (WATER BALANCE) PADA DAERAH ALIRAN SUNGAI (DAS) CIKAPUNDUNG.. Universitas Pendidikan Indonesia | repository.upi.edu | perpustakaan.upi.edu

[r]

Kode Etik Profesi Akuntan Publik adalah aturan etika yang harus diterapkan oleh anggota Institut Akuntan Publik Indonesia (IAPI) yang sebelumnya dinamakan Ikatan

Tujuan dari penelitian ini adalah : (1) Untuk mengkategorisasikan pola komunikasi lintas budaya yang dilakukan oleh para pedagang lokal dengan wisatawan asing di

dengan ditanggapi aktif oleh peserta didik dari kelompok lainnya sehingga diperoleh sebuah pengetahuan baru yang dapat dijadikan sebagai bahan diskusi