Refer to Important disclosures in the last page of this report

Stock DataTarget price (Rp) Rp2,700

Prior TP (Rp) Rp2,700

Shareprice (Rp) Rp1,870

Upside/downside (%) +44.4

Sharesoutstanding (m) 3,561

Marketcap. (US$ m) 479

Government of Indonesia 51.0%

Public 49.0%

Estimate Change; Vs. Consensus 2018 2019 PT Indo Premier Sekuritas joey.faustian@ipc.co.id +62 21 5793 1168

Unusually high burn rate in 1Q18

Earnings of Rp73bn in 1Q18 (+283% yoy)

Achieved 13%/14% of our/company’s FY18 new contract target.

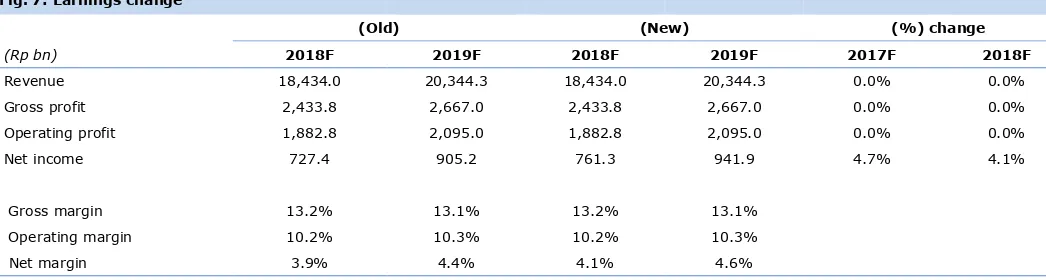

Revise up earnings forecast by 4.7/4.1% for FY18-FY19F

Maintain Buy with unchanged TP of Rp2,700.

1Q18 earnings above historical performance in the last 5 years.

ADHI

reported earnings of Rp73bn (+283% yoy) in 1Q18, representing 10/9% of

our/consensus’ FY18 estimate. This strong achievement in 1Q18 is ADHI’s best 1Q

performance in the last 5 years, which has average of 3% contribution of 1Q to

ADHI’s full year earnings. Revenue was Rp3.1tn (+40% yoy) in 1Q18, cumulating

17/16% of our/consensus’ FY18 target, which also higher than ADHI’s 1Q

historical performance in the last 5 years of 7.2-16.6%. There were margin

expansion all across the board with gross, operating, and net margin stands at

13.7%, 9.9%, and 2.3% (1Q17: 10.6%, 7.0%, and 0.9%) due to increase

revenue portion from LRT Jabodebek and real estate segment which has better

gross margin of 15% and 19%, respectively.

Achieved 14% of our FY18 new contract target of Rp21tn.

ADHI booked

new contract of Rp3tn (-19% yoy) in 1Q18, which represent 14/13% of

our/company’s FY18 target of Rp21/23tn. ADHI is currently planning to have a

joint operation with Acset Indonusa to join tender process for Jakarta-Cikampek

and Serpong-Balaraja toll road, with contract worth of Rp900bn and Rp3.8tn,

FY19F forecast by 4.7/4.1% for FY18-FY19F given increase revenue portion of LRT

Jabodebek and real estate segment to 50% and 5.2% (1Q17: 33% and 4.3%)

which has better gross margin. In addition, we also apply better margin for EPC

segment which has positive gross margin of 14.2% in 1Q17, after booking a

negative 13.1% in 1Q17.

Maintain Buy with unchanged TP of Rp2,700.

We continue to like ADHI given

its better outlook given better certainty on LRT Jabodebek project, supported by

ongoing TOD projects which have shown increase contribution towards ADHI’s

revenue. We believe TOD’s segment will be ADHI’s driving growth for the next

Source: ADHI, IndoPremier Share Price Closing as of : 20-April-2018

2

Refer to Important disclosures in the last page of this report

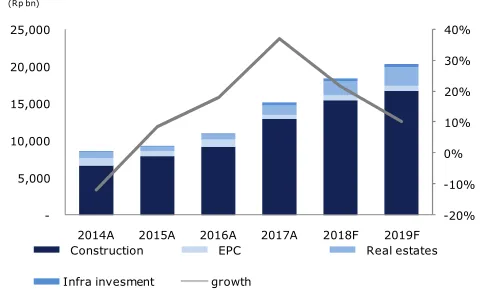

Fig. 1: Net profit to grow by 35% CAGR FY17-FY19F Fig. 2: Revenue to grow by 15% CAGR FY17-FY19F

Source: Company, IndoPremier Source: Company, IndoPremier

Fig. 3: Revenue by segment in 1Q18 Fig. 4: Positive operating cash flow in 1Q18

Source: Company, IndoPremier Source: Company, IndoPremier

Fig. 5: New contract of Rp3tn in 1Q18 Fig. 6: Net margin improvement FY17-FY19F

Source: Company, IndoPremier Source: Company, IndoPremier

-21%

2014A 2015A 2016A 2017A 2018F 2019F

(Rp bn)

Net profit growth

-20%

2014A 2015A 2016A 2017A 2018F 2019F

Construction EPC Real estates

Infra invesment growth

2012A 2013A 2014A 2015A 2016A 2017A 2018F

(Rp bn)

2014A 2015A 2016A 2017A 2018A 2019F

3

Refer to Important disclosures in the last page of this report

Fig. 7: Earnings change

(Old) (New) (%) change

(Rp bn) 2018F 2019F 2018F 2019F 2017F 2018F

Revenue 18,434.0 20,344.3 18,434.0 20,344.3 0.0% 0.0%

Gross profit 2,433.8 2,667.0 2,433.8 2,667.0 0.0% 0.0%

Operating profit 1,882.8 2,095.0 1,882.8 2,095.0 0.0% 0.0%

Net income 727.4 905.2 761.3 941.9 4.7% 4.1%

Gross margin 13.2% 13.1% 13.2% 13.1%

Operating margin 10.2% 10.3% 10.2% 10.3%

Net margin 3.9% 4.4% 4.1% 4.6%

4

Refer to Important disclosures in the last page of this report

Year To 31 Dec (RpBn) 2016A 2017A 2018F 2019F 2020F

Income Statement

Net Revenue 11,064 15,156 18,434 20,344 23,313

Cost of Sales (9,949) (13,098) (16,000) (17,640) (20,347)

Gross Profit 1,115 2,058 2,434 2,704 2,966

SG&A Expenses (456) (581) (772) (799) (927)

Operating Profit 659 1,477 1,662 1,905 2,039

Net Interest (95) (341) (453) (449) (492)

Forex Gain (Loss) 64 7 0 0 0

Others-Net (15) (185) 93 91 156

Pre-Tax Income 613 957 1,302 1,547 1,703

Income Tax (298) (440) (538) (602) (692)

Minorities (2) (2) (2) (3) (3)

Net Income 313 515 761 942 1,008

Balance Sheet

Cash & Equivalent 3,365 4,131 4,798 4,274 4,366

Receivable 3,970 3,739 4,170 4,610 5,228

Inventory 131 3,683 3,669 3,878 4,247

Other Current Assets 9,368 13,264 15,070 17,016 19,101

Total Current Assets 16,835 24,818 27,707 29,779 32,942

Fixed Assets - Net 1,814 1,876 3,677 4,850 5,434

Goodwill 0 0 0 0 0

Non Current Assets 1,446 1,639 1,696 1,847 2,025

Total Assets 20,095 28,333 33,080 36,476 40,402

ST Loans 2,344 3,537 5,069 5,595 6,411

Payable 8,373 11,611 0 13,947 16,136

Other Payables 1,828 2,235 2,527 2,754 3,239

Current Portion of LT Loans 500 250 250 500 0

Total Current Liab. 13,044 17,633 19,763 22,796 25,786

Long Term Loans 1,428 4,665 6,625 6,242 6,423

Other LT Liab. 180 164 214 246 273

Total Liabilities 14,653 22,463 26,602 29,284 32,482

Equity 3,415 3,413 3,413 3,413 3,413

Retained Earnings 1,997 2,446 3,038 3,751 4,477

Minority Interest 10 11 12 13 14

Total SHE + Minority Int. 5,422 5,869 6,462 7,177 7,904

Total Liabilities & Equity 20,075 28,332 33,064 36,460 40,386

5

Refer to Important disclosures in the last page of this report

Year to 31 Dec 2016A 2017A 2018F 2019F 2020F

Cash Flow

Net Income (Excl.Extraordinary&Min.Int) 315 517 764 945 1,011

Depr. & Amortization 66 131 208 332 421

Changes in Working Capital 2,074 191 (241) 1,374 1,280

Others (301) (3,124) (3,412) (877) (1,108)

Cash Flow From Operating 2,154 (2,285) (2,682) 1,774 1,605

Capital Expenditure (1,257) (386) (2,066) (1,656) (1,183)

Others 163 104 145 168 150

Cash Flow From Investing (1,094) (283) (1,922) (1,488) (1,034)

Loans 1,153 4,181 3,492 392 497

Equity 1 0 0 0 0

Dividends (94) (94) (155) (228) (283)

Others (195) (447) (559) (594) (625)

Cash Flow From Financing 866 3,640 2,778 (431) (410)

Changes in Cash 1,926 1,072 (1,826) (146) 161

Financial Ratios

Gross Margin (%) 10.1 13.6 13.2 13.3 12.7

Operating Margin (%) 6.0 9.7 9.0 9.4 8.7

Pre-Tax Margin (%) 5.5 6.3 7.1 7.6 7.3

Net Margin (%) 2.8 3.4 4.1 4.6 4.3

ROA (%) 1.7 2.1 2.5 2.7 2.6

ROE (%) 5.9 9.1 12.3 13.8 13.4

ROIC (%) 5.2 5.2 5.5 5.9 5.8

Acct. Receivables TO (days) 84.8 70.2 60.9 60.9 59.3

Acct. Receivables - Other TO (days) 35.4 22.6 17.4 17.8 17.7

Inventory TO (days) 67.8 6.9 4.4 4.7 5.0

Payable TO (days) 272.6 278.4 268.4 267.6 269.8

Acct. Payables - Other TO (days) 0.0 0.0 0.0 0.0 0.0

Debt to Equity (%) 78.8 144.0 184.8 171.9 162.4

Interest Coverage Ratio (x) 0.4 0.3 0.4 0.3 0.3

Net Gearing (%) 16.7 73.6 110.6 112.3 107.1

Head Office

PT INDO PREMIER SEKURITAS

Wisma GKBI 7/F Suite 718

Jl. Jend. Sudirman No.28

Jakarta 10210 - Indonesia

p +62.21.5793.1168

f +62.21.5793.1167

INVESTMENT RATINGS

BUY : Expected total return of 10% or more within a 12-month period HOLD : Expected total return between -10% and 10% within a 12-month period SELL : Expected total return of -10% or worse within a 12-month period

ANALYSTS CERTIFICATION.

The views expressed in this research report accurately reflect the analysts personal views about any and all of the subject securities or issuers; and no part of the research analyst's compensation was, is, or will be, directly or indirectly, related to the specific recommendations or views expressed in the report.

DISCLAIMERS