An examination of the electronic

market hypothesis in the US home

mortgage industry

A deductive case study

Sutirtha Chatterjee

Management, Entrepreneurship, and Technology, University of Nevada,

Las Vegas, Las Vegas, Nevada, USA

Jeffrey W. Merhout

Information Systems & Analytics, Miami University, Oxford, Ohio, USA

Suprateek Sarker

Management, Information Systems, and Entrepreneurship,

Washington State University, Pullman, Washington, USA, and

Allen S. Lee

Information Systems, Virginia Commonwealth University, Richmond,

Virginia, USA

Abstract

Purpose– The purpose of this paper is to longitudinally test the propositions of the Electronic Market Hypothesis (EMH) within the context of the US home mortgage industry.

Design/methodology/approach– The paper uses a deductive, positivist case study, through a systematic examination of “texts” in the trade press over three time periods: 1995-1999, 2000-2002, and 2003-2007.

Findings– EMH propositions, while generally not found to be valid in the early years, were more consistent with evidence in the home mortgage industry in the later period.

Research limitations/implications – Throws fresh light on the debate between the appropriateness and the inappropriateness of the EMH as a core theory explaining the influence of Information Technology on market and industry structures.

Practical implications– Designing of corporate strategies to foster efficient market mechanisms.

Originality/value– Using a relatively uncommon (analysis of primary data from trade press articles) qualitative research methodology which could serve as a guideline for future research. This approach offers opportunities to use various trade press sources to perform studies on the effects of IT on people, such as analyzing how IT departments are adapting their governance practices as workers increasingly use personal computing devices to access organizational assets (e.g., networks, applications, and data).

Keywords Electronic market hypothesis, Home mortgage industry, Qualitative, Deductive, Mortgage companies, United States of America

Paper type Research paper

The current issue and full text archive of this journal is available at www.emeraldinsight.com/0959-3845.htm

Received 30 November 2012 Accepted 4 December 2012

Information Technology & People Vol. 26 No. 1, 2013

pp. 4-27

rEmerald Group Publishing Limited 0959-3845

DOI 10.1108/09593841311307114

The authors are grateful to The Institute for the Study of Business Markets (ISBM), Pennsylvania State University, who helped partially fund this research. The authors also thank the Associate Editor, Professor Neil Doherty, and the three anonymous reviewers, for their excellent feedback and guidance during the review process, which resulted in a much stronger paper.

4

Introduction

While scholars agree that information technology (IT) has had a major impact on business transactions over the last few decades, the precise nature of the effects of IT on market and industry structures also has been the subject of much debate (Chircu and Kauffman, 2000; Sarkaret al., 1995; Wigand, 1997). One very influential work shaping research on how IT-mediation is changing business models and industry structures was published by Maloneet al.(1987) in the form of the “electronic market hypothesis” (EMH). The EMH posits that as a result of IT-mediation, market-based forms of governance (in the form of “electronic markets” or EM) will gradually take over from hierarchical forms of governance (in the form of “electronic hierarchies”), owing primarily to reduced costs of coordination (Maloneet al., 1987; Granadoset al., 2006). In addition to predicting a move toward EM (Bakos, 1997), a fair amount of academic discussion surrounding the EMH has focussed on if and how IT actually enables such a shift.

While the EMH has been instrumental in guiding much research in this area for the past decade, the basic assertions of the EMH have not found unequivocal support among scholars. Indeed, a review of the past literature shows that while being heavily referenced by researchers across several disciplines, EMH assertions have both been supported and heavily criticized and we are still no nearer to the truth regarding the validity of the EMH than we were a decade ago. Moreover, industry structures have continued to evolve as a result of IT mediation. Consequently, there is a need to investigate the EMH and its basic assertions anew, an objective that we pursue in the current study. In this research, we conduct an industry-level case study using “texts” in trade publications of the primary market of the home mortgage industry (HMI). We use hypothetico-deductive (H-D) logic in order to test the EMH’s propositions. The purpose of our empirical re-examination of the EMH is either to support or to cast doubt on the EMH, and hence the e-commerce research and corporate strategies that are based on the EMH.

A focus on the EMH also brings us closer to understanding human decision making in business. This is because the EMH is based on transaction cost economics (TCE), which, in turn, builds upon fundamental assumptions about human nature and behavior (Rindfleisch and Heide, 1997). In particular, three behavioral assumptions about human nature underpin TCE: bounded rationality, opportunism, and risk neutrality. Bounded rationality “is the assumption that decision makers have constraints on their cognitive capabilities and limits on their rationality” (Rindfleisch and Heide, 1997, p. 31). Opportunism “is the assumption that, given the opportunity, decision makers may unscrupulously seek to serve their self-interests, and that it is difficult to know a priori who is trustworthy and who is not” (Rindfleisch and Heide, 1997, p. 31). Finally risk neutrality can be understood in terms of the (risk neutral) party being “indifferent between a prospect of uncertain profits and a certain profit, provided that the expected average of the prospective fluctuating profits is equal to the certain profit” (Aoki, 1984, p. 15; cf. Chiles and McMackin, 1996, p. 81). TCE, therefore, builds upon key assumptions about human nature, and it is therefore not surprising that it has often been viewed as a theory guiding managerial choice and decision making (Chiles and McMackin, 1996). As Rindfleisch and Heide (1997) also showcase, TCE has seen heavy application in the realm of managerial/corporate decision making. It is therefore evident, that EMH – which closely builds upon the TCE (and its underlying assumptions) – is itself closely related to managerial decision making in a technology-enabled business landscape,

5

especially related to choosing governance structures such as markets or hierarchies (Chiles and McMackin, 1996).

As a direct outcome of our study, there would either be recognition of a greater need for developing alternate theories (or more refined versions of the EMH) or there would be a strong rationale for renewed faith on the EMH propositions, and their implications for future research and practice, including those for understanding human behavior in EM.

Overview of the EMH

The EMH, as articulated by Malone et al.(1987), holds that “by reducing the costs of coordination, information technology will lead to an overall shift toward proportionately more use of markets – rather than hierarchies – to coordinate economic activity” (p. 484). Furthermore, the EMH predicts that the move from electronic hierarchies to EM would not occur instantaneously, but over a period of time (Granadoset al., 2006).

A possible (electronic) hierarchy scenario exists when a buyer has a sole source relationship with a single vendor (using IT to communicate and coordinate), and inherent biases, rather than market forces, determine key characteristics of the procurement transaction, such as price, design, and quantities. Markets, on the other hand, “coordinate the flow through supply and demand forces and external transactions between different individuals and firms” (Malone et al., 1987, p. 485). A possible (electronic) market scenario is one where a single buyer (i.e. either a firm or an individual consumer), chooses from among several possible suppliers (in an IT-mediated platform), with market forces determining the price and other key transaction characteristics.

The EMH argues that, other factors being equal, the primary economic activity coordination mechanism (EACM) (i.e. the structure that facilitates transactions) in any given industry will eventually evolve into an EM. The general underlying reason for this proposition is that, in addition to the benefits of increased price competition that are inherent in markets, the utilization of IT will reduce certain transaction costs (primarily coordination costs (CC)) that would otherwise result from conducting business in a marketplace with multiple suppliers.

CC include the costs of gathering and processing information, negotiating contracts, and taking steps to minimize the risks of “dealing with ‘opportunistic’ trading partners” (Malone et al., 1987, p. 486). Additional CC attributable to marketplace coordination include any added time and expense associated with dealing with multiple vendors instead of conducting business as a hierarchical relationship with a sole vendor (or with a vertically integrated, related party). For example, a market purchase would require additional time and effort to search through all the available alternatives (i.e. costs, design features, supplier reputations, etc.) to select a vendor, to determine a delivery schedule, to make payments, and to accurately record accounting information (e.g. to set up a new vendor in the system). In the presence of advances in IT support, however, the additional CC can be dramatically decreased, thereby making the market structure a viable alternative to a hierarchical relationship in an electronic environment. If the costs of coordination can be reduced sufficiently by electronic means, a buyer can also obtain the lower prices available in a market while retaining some of the benefits similar to a close hierarchical relationship (e.g. a tightly coupled payment and accounting system like electronic data interchange (EDI)). Therefore, according to the EMH, as the costs of coordination continue to

6

decrease because of increasing IT support, industries will tend to evolve toward an EM structure as the predominant EACM.

Motivation for the study

We have alluded to the fact that the EMH has both been applauded and criticized in the literature. The purpose of this motivation section is to briefly recapitulate the contradictory evidence and viewpoints found in the past literature on the EMH, thereby establishing the need for further investigation.

First, past research studies have compiled much evidence that is inconsistent with the EMH (e.g. Hess and Kemerer, 1994; Daniel and Klimis, 1999; Krautet al., 1999; Wigand et al., 2005). Second, apart from evidence inconsistent with it, the EMH has also been theoretically criticized (e.g. Bakos and Nault, 1997, citing Gurbaxani and Whang, 1991; Clemonset al., 1993; Grover and Ramanlal, 1999; Kauffman and Mohtadi, 2004).

On the other side of the fence, significant evidence consistent with the EMH has also been presented (e.g. Chircu and Kauffman, 2000; Fine and Whitney, 1996). And significantly, Hess and Kemerer (1994), whose study on the EMH showed limited support for the theory, have also wondered if “the full results predicted by the EMH require a longer gestation period” (p. 251).

Recently, a number of scholars have provided evidence for the general emergence of EM (which is what the EMH posited) by pointing out that the rise of electronic intermediaries has helped mitigate the imperfections associated with EM (e.g. Bakos

et al., 2005; Spulber, 1999). Since intermediaries are seen as institutional mechanisms enabling EM (Son et al., 2006; Pavlou et al., 2007), the emergence of intermediaries would strongly indicate that EM are becoming more efficient and prevalent, in effect supporting the EMH claims of increasing market-based governance.

In summary, past research related to the EMH has presented evidence that is somewhat contradictory in nature. On one hand, we have studies that have theoretically criticized the EMH and presented data inconsistent with the perspective; on the other hand, we have studies that have argued that EM are indeed becoming more prevalent and dominant. The current study may thus be seen as one effort to resolve the anomalies in the literature surrounding the EMH, and to assess the empirical validity of the theory in a specific setting. We believe that such an undertaking is useful, given that EMH has served (and continues to serve) as a theoretical basis for much research in this area (Granadoset al., 2006).

Additionally, there is current evidence presented by some scholars that many industries have become “more market-like” (Granados et al., 2006, p. 152) in recent years. In fact, recent adoption of standards in the HMI (the context of our study) have significantly reduced CC (Wigandet al., 2005), thus satisfying the original conditions of the EMH. Given that this is a relatively new phenomenon, we feel that a re-investigation of the EMH adds value. Simply put, if the conditions purported by the EMH are becoming true only in recent times, we argue that the opportunity is ripe to test whether the EMH really holds. It is also notable that Hess and Kemerer (1994), when they tested the EMH, concluded that the EMH needs a greater “gestation period,” which, we argue has now passed – reinforcing the appropriateness of testing the EMH. We should also note that, in a broader sense, our research (which examines this phenomenon over three time periods between 1995 and 2007 in the HMI) also responds to Choudhuryet al.(1998) call for studies of “Electronic Markets [y] to

7

build the cumulative body of evidence necessary to understand fully the dynamics of the uses and consequences of Electronic Markets” (p. 501, emphasis added).

We should also justify here the focus of our study (e.g. the US HMI). There are two main reasons for this. First, it has been a cynosure of past research related to EM (e.g. Hess and Kemerer, 1994; Steinfield et al., 2005; Wigand et al., 2005). Second, “the U.S. Home Mortgage Industry is characterized by high fragmentation, with several thousands of mortgage bankers and brokers, and a high degree of vertical disintegration, with numerous players such as bankers, brokers, credit agencies, appraisal, title, escrow companies, and so on” (Wigand et al., 2005, p. 175). In other words, the US HMI is a particularly good candidate for testing the EMH because it resembles a market-like structure, perhaps due to the reduced CC resulting from the adoption of industry standards (Wigandet al., 2005).

The following sections of the paper will provide an overview of the EMH, discuss the development of the EMH model (drawing upon Maloneet al., 1987), discuss our case background, and present our research methodology. Following that, we subject the EMH to deductive empirical testing in the HMI, after which we discuss the overall results and their future implications, both in terms of research and practice.

Operationalizing Malone, Yates, and Benjamin’s EMH model

We now turn our attention to the first step of empirically evaluating the EMH – operationalizing the EMH model. A major challenge we face in empirically testing the EMH is that the variables are not clearly identified or defined. Our strategy has been to explicitly define the variables that we discern through the study of the foundational work on the EMH (Maloneet al., 1987), and to develop a working model with relationships between/among the variables.

Variables

The EMH can be operationalized in different ways. For our test, we use the following variables that we understood from reading and analyzing Malone et al.’s paper, together with our understanding of the relevant literature.

Independent (or antecedent) variable. The independent variable in the EMH is what we name “advances in IT.” In our conceptualization, advances in IT can be understood to be the IT innovations that provide the infrastructure and functionality necessary to facilitate economic transactions (Bakos and Brynjolfsson, 1993; Maloneet al., 1987). Specifically, the variable attempts to capture enhancements in hardware, software, data management techniques, and networks in deliberate configurations, which permeate an industry and accelerate the electronic communication and coordination capabilities of industry participants.

Mediating variable. The EMH concentrates on an important mediating variable: CC. In our context, CC include the time and effort required by a buyer to evaluate alternative suppliers and to coordinate the transaction’s requirements, such as scheduling deliveries and making payments, thus referring to the costs incurred in an economic exchange (Alchian and Demsetz, 1972).

The dependent variable. The dependent variable, “EACM,” indicates the predominant nature of economic structures responsible for facilitating the exchange of key goods or services within an industry (Malone et al., 1987). Specifically, EACM seeks to capture the degree to which economic transactions are processed through an EM-mediated mechanism as compared to an electronic hierarchical mechanism. It should be noted that we do not conceptualize that there will be either

8

hierarchical mechanisms or market mechanisms in an exclusive manner. Both can coexist, but the EACM variable captures the relative pre-dominance of one mechanism over another. Thus we conceptualize the EACM moving along a continuum with purely hierarchical mechanisms and market mechanisms on the extremes.

A predominantly hierarchical mechanism would signify that (in our context) consumers would select loan procurement from a select few, established providers. On the other hand, a predominantly market mechanism would signify that the consumers use the internet marketplace extensively to identify and select among multiple providers (often based on loan terms and conditions), or use loan intermediaries (like LendingTree) – who themselves are an interface to multiple loan providers– in order to procure a loan. As shown in our empirical study, in many cases, such a relative predominance is not easily recognizable – leading us to conclude that there is approximately equal preponderance of either mechanism.

Relationships among the variables. We draw from Malone et al.’s (1987) original theory to present the relationships between the variables. The following diagram (Figure 1) represents the EMH variables and relationships as articulated by Maloneet al.(1987). The justification for these propositions is presented in Table I. The business to consumer (B2C) sector of the HMI

Maloneet al.(1987) use “the termsbuyers, procurers, andconsumersinterchangeably” (p. 490, emphasis in original), indicating that EMH is applicable in B2B as well as B2C contexts. While the EMH has often been studied in B2B settings, in our study, we focus

Advances in

1. There is a direct positive influence of IT on EACM (i.e. without regard to the intervening mediating variables); specifically, more advances in IT lead to greater proportion of transactions being mediated through a market mechanism

(Arrow 1 in Figure 1)

“[y] the overall effect of this technology will be

to increase the proportion of economic activity coordinated by markets” (p. 489)

2. There is an inverse influence of IT on CC (Arrow 2 in Figure 1)

“[y] since the essence of coordination involves

communicating and processing information, the use of information technology seems likely to decrease these costs” (p. 486)

3. There is an inverse influence of CC on EACM

(Arrow 3 in Figure 1)

“[y] by reducing the costs of coordination,

on the B2C context. This setting is appropriate for testing EMH propositions, which are based on TCE. Indeed, proponents of the TCE suggest that the theory can be applied as much to B2C scenarios as to B2B scenarios. There have been studies that have explicitly used TCE in order to understand online consumer shopping behavior, a typical B2C scenario (e.g. Teo and Yu, 2005; Liang and Huang, 1998). Furthermore, all the fundamental assumptions on which TCE is based are about universal human attributes – opportunism, bounded rationality, and risk neutrality (Rindfleisch and Heide, 1997). Since universal human attributes should apply to consumers at least as much they do for firms, we may argue that the fundamental assumptions of TCE are consistent with the B2C unit of analysis. Since the EMH has TCE as its underlying theoretical rationale, it logically follows that the EMH can also be investigated in the B2C context.

There is another issue that needs to be clarified with respect to the B2C scenario: the notion of hierarchy. Since the EMH provides an explanation for domination of EM over electronic hierarchies, it is critical to explain what these terms mean in the context of a B2C relationship. While the first (i.e. EM) is easy to comprehend, the notion of hierarchy in a B2C relationship requires further explanation. Granados et al.(2006), who apply Maloneet al.’s (1987) work to both B2C and B2B transactions in the airline and financial securities industries, suggest that hierarchies could well exist in the case of B2C transactions. We are aware that the purest form of hierarchy is the firm itself (Coase, 1937; Granados et al., 2006). What does this mean in a B2C scenario? A hierarchical B2C scenario would imply that a consumer is biased toward one or a few firms so that the consumer does not readily engage in market-based mechanisms. Due to the existence of brand loyalty in a B2C e-commerce context (Srinivasanet al., 2002) it can be argued that we, as consumers, often have our preferences and biases about procuring from a specific firm or a set of firms.

We now come to our specific case, the HMI in the USA, and explicate our rationale for choosing this case. Steinfieldet al. (2005) note that there are two main segments in the HMI in the USA: a primary B2C market where the consumer obtains a loan from a mortgage lender (sometimes facilitated by brokers), and a secondary B2B market where the loans are sold by the lender to free up capital. Jacobides (2001) describes the impact of IT in the mortgage banking industry and clearly distinguishes between B2B and B2C electronic transactions. He discusses both B2B in the origination process (between mortgage banks and mortgage brokers) and the “development of the B2C origination markets” (p. 124) for consumers to purchase loans through the development of web channels by existing industry brokers and a “new breed of cyberbrokers” such as LendingTree. In our study, we focus only on the primary market, which includes the B2C component of this complex industry. This will effectively limit our scope only to economic activity between consumers seeking loans and brokers and lenders. One of the major reasons for selecting the HMI for testing the EMH is that Hess and Kemerer (1994) conducted their study in this industry, and while they did not find support for the EMH at that point, they made a conjecture that EM would become more dominant with the passage of time (as suggested by EMH).

Given the current state of the internet in the USA, we believe that the IT infrastructure for lending activities has, over time, experienced advancement as predicted by the EMH. Hence, if the EMH is valid, the primary EACM for the HMI should have evolved to a point where EM are dominant. Accordingly, we concluded that this industry made a good candidate for empirically testing the EMH’s propositions longitudinally.

10

Methodology

To empirically test the propositions of the EMH, we use H-D logic, the validity of which has long been recognized in information systems and related disciplines (Ackroyd and Hughes, 1992; Lee, 1989; Sarker and Lee, 2002; Lee and Hubona, 2009). In contrast to an inductive approach used in case studies that are directed toward building theory, a theory-testing case study guided by H-D logic involves applying an already formulated theory (specifically, the propositions of the theory) to the facts of a case or situation in order to deduce predictions of what one would expect to observe if the theory was valid. Popper (1985) notes that: “So long a theory withstands detailed and severe tests [y], we may say that it is ‘corroborated’” through the tests, though it must be kept in mind that subsequent tests can always invalidate the theory. On the other hand, if the evidence is not what was expected (i.e. not consistent with the theory’s predictions), the theory is disconfirmed and should possibly be discarded (Darkeet al., 1998).

In our study, we test the EMH propositions with observations of past events (within the context of the HMI). Because we make “predictions” about events occurring in the past, a more suitable term would be “post-dictions.” As far as H-D logic is concerned, a post-diction has the same logical form as a prediction. TheOxford English Dictionary

defines post-diction as “(The making of) an assertion or deduction of something in the past.” Whether dealing with a prediction or a post-diction, H-D logic performs testing in the same way.

We also used specific tactics to support the scientific reasoning process, so as to develop some degree of “evidential meaningfulness” (e.g. Glymour, 1980), as discussed in Chatterjee et al. (2009). This includes systematically selecting relevant “texts,” coding them, and ensuring satisfactory validity and reliability.

In order to draw reasonable conclusions about whether or not the observations in a case (e.g. observations of naturally occurring industry-related artifacts, such as documents and trade press) match the stated post-dictions, a researcher must use an analytical strategy to create observation statements from the data they have gathered. Accordingly, we analyze “texts,” which primarily consisted of papers from publicly available documents, specifically trade and popular press papers related to the HMI in the USA. The use of popular or trade press papers as forms of natural artifacts constituting “first-order” observations is established in many social science disciplines, including historiography (e.g. Shulman, 1999), historical sociology (Neuman, 2004), organizational behavior (Galunic and Eisenhardt, 1996), business strategy (Yin, 1993), and sociology and anthropology (Glaser and Straus, 1967). These primary sources are natural artifacts created by members of a specific social community (in our case, the HMI) and, thus, are a valid source of data (Neuman, 2004).

In line with recommendations from Markus (1989), who suggests that cases selected should “be representative of a presumably large class of cases [y]” we developed a list of publications (in consultation with an industry expert: the Director of a University’s Real Estate Institute) that would feature evidence related to the validity of the EMH in the home mortgage context. Apart from ensuring that the “typical case” criterion was satisfied, we “purposefully” included sources that were likely to publish texts that would be inconsistent with the predictions of EMH. Such a purposive sampling strategy would ensure that we subjected EMH to “severe” tests, and if the EMH survived the attempts at its empirical refutation, it would have proven “its mettle” (Popper, 1985). The final list of sources utilized in this study included: American Banker,Bank Technology News, Mortgage Banking, Mortgage Originator Magazine,

11

National Mortgage News, Newsweek, andUS Banker. This list was approved by our industry expert (aware of our research objectives), who certified that it was an acceptable list of publications (for our research objective) because it included the ones “most heavily read in the banking/mortgage origination business.”

Since we concentrate on published “texts” as sources of evidence, our methodological approach closely incorporates Morris’ (1994) schema for content analysis. Our overall approach is as follows. The authors recruited two assistants (graduate students) for 50 hours work, funded through a research grant the authors obtained for this purpose from the Institute for the Study of Business Markets, Penn State University. These two assistants were randomly assigned disjoint subsets of the publications from the list. The coders were asked to identify relevant papers from the list of sources assigned to them. The timeframe for which papers were identified was 1995-2007. Using pre-specified search keywords (such as “mortgage and technology,” “mortgage and automation,” “Internet mortgage,” “electronic commerce and mortgage”), they identified a total of 64 papers (list available upon request). This formed the core of the case study database (Yin, 1994).

Empirical analysis

Variable definitions and levels

This sub-section shows how the earlier-defined EMH constructs formed the basis for coding data. The constructs, coding levels, their meanings, and the corresponding representative evidences (from the texts) are presented in Table II.

Inter-rater reliability

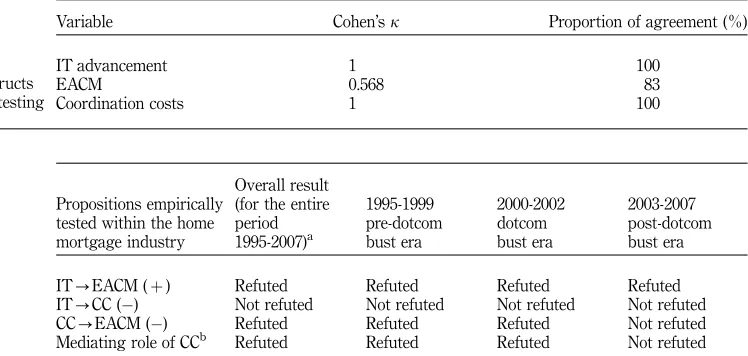

The first empirical result that we report is that of the inter-rater reliability for each construct that was coded by our two assistants (see Table III). The two measures of inter-rater reliability used were Cohen’sk(Cohen, 1960; Landis and Koch, 1977), and the “proportion of agreement” showing “the relative proportion of units of analysis allocated to the same category by two different coders” (Titscheret al., 2000, p. 60).

Proposition testing

Table IV presents the results of our proposition testing. We note that according to H-D logic (e.g. Lee, 1989), a single instance of disconfirming evidence (i.e. a coded paper presenting evidence inconsistent with the EMH in the HMI for a relevant time period) is logically sufficient to render the proposition empirically refuted (for that time period). For example, if we find any instance (i.e. a text) where the CC is coded as 0 (i.e. lowered) while EACM is also coded as 0 (i.e. a hierarchy rather than a market), it would empirically refute the proposition that lowering of CC implies a greater move toward EM. It can be seen from Table IV that we have presented both the overall results and the results for three specific time periods.

We segmented our time range (1995-2007) into the three time periods to reflect the following differences. The first time period reflects the pre-dotcom bust era (1995-1999). The second reflects the dotcom bust era (2000-2002). The third reflects the post-dotcom bust era before the start of the current economic meltdown (2003-2007). Testing the EMH for each of these time periods between 1995 (the year after Hess and Kemerer published their study) and 2007 provides for a more granular and meaningful examination of this phenomenon, especially given the recognition among scholars that many industries, including the HMI, have evolved over this period of time. In addition to the results for the three periods mentioned above, we provide overall results for each

12

Construct and definition

Coding

level Coding meaning Representative evidence

Advances in IT: enhancements in hardware, software, data management, and networks in deliberate configurations that permeate an industry and accelerate the electronic communication and coordination capabilities of industry participants in order to provide the infrastructure and functionality in order to transact and exchange information electronically

0 IT has decreased None

1 IT has advanced In the past few years there has been an exponential growth of technology designed to automate this hopelessly outdated process, and in the next five years there will be as much progress again as there was in the last five years. (“The Paperless Mortgage,” National Mortgage News, 1997)

Coordination costs: time and effort required by a buyer to evaluate alternative suppliers and to coordinate the transaction’s requirements, such as scheduling deliveries and making payments, e.g. costs to: search through all the available alternatives (i.e. costs, design features, supplier reputations, etc.), determine a delivery schedule, make payments, record acct information, etc

0 Low(er) The internet, however, takes response time and customer service to a new level. Web-enabling technologies improve service by offering the customer self-service opportunities. Internet customer service solutions provide customers with imaged documents, access to real-time account postings, enhanced level of research while they are online; The internet has helped create a more sophisticated borrower who has unlimited access to financial information. (Tim Anderson, “Integrating the E-Business Model,”Mortgage Banking, 2000)

1 High(er) None

T

ab

le

II.

Construct and definition

Coding

level Coding meaning Representative evidence

1 Higher proportion of transactions are mediated through a hierarchical mechanism as compared to a market mechanism

The internet is fine for checking rates and getting information, Mr Sumner concurred. But people are still “very reluctant to go on-line” to apply for a home loan. “They still need a phone call to consummate the sale,” he said. (Lew Sichelman, “Mozilo: Net Firms in Trouble?”National Mortgage News, 1999)

Note:We can infer from this quote that consumers are not actually procuring loans over the internet and are procuring loans from their preferred providers, i.e. engaging in a hierarchical transaction 2 Approximately

equal proportions of transactions are mediated through hierarchical and market mechanisms

The field may be divided into at least three groups: lenders and their allies, including bank-run consolidator sites like HomeByNet and Monument Mortgage’s iQualify service; consumer technology companies such as Intuit Inc and Microsoft Corp and their Quickenmortgage.com and HomeAdvisor sites; and broker-based sites such as E-Loan and HomeShark Inc; “The mortgage business has disintermediated itself over the past five years, with many lenders offering loans retail, wholesale, correspondence, and through brokers,” (Drew Clark, “Lenders Dragged and Dropped onto the Internet,”American Banker, 1998)

Note:Here the paper discusses that there is a preponderance of both hierarchy and market mechanisms. The first two represent a hierarchy, while the third represents a market. Since we find evidence that both are quite dominant, we conclude that this evidence shows that proportions of market-based transactions and hierarchical transactions are comparable.

(continued)

T

ab

le

II.

Construct and definition

Coding

level Coding meaning Representative evidence

3a Higher proportion of transactions are mediated through a market mechanism as compared to a hierarchical mechanism

“The Internet is putting powerful tools, like automated

underwriting, in the hands of smaller originators,” he said, adding that brokers, in particular, are a powerful force in this market (John Hackett, “Despite Shortfalls, Expert Sees “Glimmer of Hope” for Internet Lending,”National Mortgage News, 2001)

Note:This quote shows that brokers (i.e. loan intermediaries) are a powerful force, implying that market based mechanism are more prevalent. This is because existence of powerful intermediaries implies a greater market like structure

4 Almost all

transactions are fully mediated through a market mechanism

As more education about the value proposition behind going electronic is discovered, the movement toward paperless processes and eventually electronic mortgages is accelerating [y]. The study

conducted by imaging and collaborative workflow vendor Advectis here surveyed over 60 organizations including 10 of the top 20 lenders and five of the top 10 lenders. When asked how fast their organization will adopt e-mortgage capabilities, nearly two-thirds (63%) said they are either early adopters or part of the early majority. (Anthony Garritano, “Study finds lenders embracing E-Mortgages,”National Mortgage News, 2006)

Note:We can infer that the adaptation of E-mortgage technologies across the board gives rise to more opportunities for online loan intermediaries (brokers) like LendingTree, Certainly, if loan providers adopt E-mortgage technologies, the efficacy of such loan intermediaries is increased. In other words, since intermediaries become powerful, we can indirectly infer that market-based mechanisms are greatly dominant

Notes:aIt should be noted that EACM codes 3 and 4 support the move toward the market. Thus any paper that is coded as a 3 or a 4 (as opposed to 0, 1, or 2) with respect to the EACM variable is evidence that we are moving toward a more market-based mechanism. However, whether it rejects or corroborates the EMH will depend on the corresponding code for the causal (IT or CC variable). For example, if in an paper the CC code is 1 (higher) while the corresponding EACM code is either 3 or 4 (relative dominance of market based transactions) then it refutes the EMH’s assertions that lower CC

will necessarily lead to more market-based transactions

15

The

electr

onic

mar

ket

h

yp

proposition, where the proposition is seen as empirically refuted if any contradictory evidence (i.e. any single observed association in the opposite direction, as explained earlier) is found in papers within the entire data set; i.e. in papers in any of the time periods. If such contradictory evidence cannot be discerned in any of the three eras, we conclude that the proposition cannot be rejected across all the time periods.

Discussion of results

When we looked at the results for different eras (1995-1999, 2000-2002, and 2003-2007), interesting patterns emerged for these periods. Before we discuss the results, we would like to reiterate that the H-D logic of empirical refutation only allows us to invalidate a proposition; a proposition that survives an attempt at its empirical refutation may be considered valid only provisionally. We note that Popper, one of the foremost contributors to the philosophy behind the logic of falsifiability, himself chose to use the word “corroborate,” so as to avoid making positive assertions.

While discussing the patterns showcased in our results, we often find that EMH propositions are empirically refuted, partly or wholly during the overall time period 1995-2007. In those cases we provide alternate explanations, which are summarized in Table V. These explanations also are elaborated upon below, wherever appropriate. Our first proposition was that IT advancement would lead to a greater proportion of market transactions, as opposed to hierarchical transactions, within the HMI. This proposition was overall empirically refuted. Results indicated that during the period of 1995-2007, there was a continuing dominance of hierarchical transactions. This is consistent with Granadoset al.’s (2006) view, indicating that the move to EM may not

Propositions empirically tested within the home mortgage industry

Overall result (for the entire period 1995-2007)a

1995-1999 pre-dotcom bust era

2000-2002 dotcom bust era

2003-2007 post-dotcom bust era IT-EACM (þ) Refuted Refuted Refuted Refuted IT-CC () Not refuted Not refuted Not refuted Not refuted CC-EACM () Refuted Refuted Refuted Not refuted Mediating role of CCb Refuted Refuted Refuted Not refuted

Notes:aUnder this column, we indicate a proposition as empirically refuted or “falsified,” if the

proposition in the corresponding row has been found inconsistent with even one instance of the data, that is, texts in chosen papers published in any of the three eras. If we fail to find such evidence, then we conclude that the proposition has not been falsified.bThe mediating role of CC was falsified if any one or both of the relationships IT-CC () and CC-EACM () was falsified. We thus see that the only period where the mediating role of CC was not falsified was in the 2003-2007 time period where both the above relationships were not falsified

Table IV.

Deductive testing results

Variable Cohen’sk Proportion of agreement (%)

IT advancement 1 100

EACM 0.568 83

Coordination costs 1 100

Table III.

Reliability for constructs used in proposition testing

16

have materialized for the HMI (as opposed to other industries such as air travel). Unlike other industries such as air travel, the HMI has a lower transparency, a key variable in determining market structures (Granadoset al., 2006). While the advancement of IT can lead to greater market transparency, and help move toward a free market structure, ultimately, this move depends on the large market participants, some of whom may choose not to disclose certain types of information, thereby negatively affecting the move toward EM. Traditionally, the HMI has been dominated by a set of key players, and thus this study’s results may be reflective of the effect of the key players’ ability to control the disclosure of information in order to maintain their market clout.

A more in-depth analysis of the data revealed that this proposition was empirically refuted for the 1995-1999 and 2000-2002 time periods only. Interestingly, the proposition was not empirically refuted for the last time period (2003-2007). This is consistent Granados et al.’s (2006) argument that “the industry is more market-like” (p. 152) in recent years.

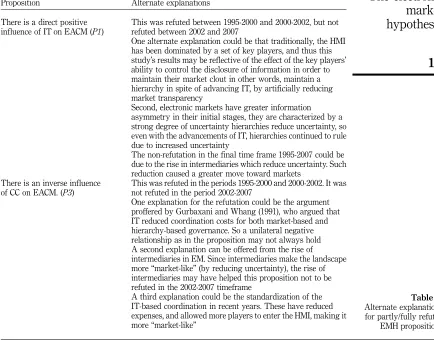

Proposition Alternate explanations There is a direct positive

influence of IT on EACM (P1)

This was refuted between 1995-2000 and 2000-2002, but not refuted between 2002 and 2007

One alternate explanation could be that traditionally, the HMI has been dominated by a set of key players, and thus this study’s results may be reflective of the effect of the key players’ ability to control the disclosure of information in order to maintain their market clout in other words, maintain a hierarchy in spite of advancing IT, by artificially reducing market transparency

Second, electronic markets have greater information asymmetry in their initial stages, they are characterized by a strong degree of uncertainty hierarchies reduce uncertainty, so even with the advancements of IT, hierarchies continued to rule due to increased uncertainty

The non-refutation in the final time frame 1995-2007 could be due to the rise in intermediaries which reduce uncertainty. Such reduction caused a greater move toward markets

There is an inverse influence of CC on EACM. (P3)

This was refuted in the periods 1995-2000 and 2000-2002. It was not refuted in the period 2002-2007

One explanation for the refutation could be the argument proffered by Gurbaxani and Whang (1991), who argued that IT reduced coordination costs for both market-based and hierarchy-based governance. So a unilateral negative relationship as in the proposition may not always hold A second explanation can be offered from the rise of

intermediaries in EM. Since intermediaries make the landscape more “market-like” (by reducing uncertainty), the rise of intermediaries may have helped this proposition not to be refuted in the 2002-2007 timeframe

A third explanation could be the standardization of the IT-based coordination in recent years. These have reduced expenses, and allowed more players to enter the HMI, making it more “market-like”

Table V.

Alternate explanations for partly/fully refuted EMH propositions

17

The finding that hierarchical structures were initially dominant during the period of 1995-2007 may also be explained by the fact that hierarchies are often chosen to reduce uncertainty (Kauffman and Mohtadi, 2004; Granadoset al., 2007). Owing to the fact that EM are not “spot markets,” and have greater information asymmetry in their initial stages, they are characterized by a strong degree of uncertainty (Datta and Chatterjee, 2008). Uncertainty refers to the inability of consumers to make predictions due to the availability of imperfect information (Bauer, 1960; Pavlouet al., 2007; Knight, 1985). Furthermore, Williamson (1985) argues that market inefficiencies are prime reasons for increasing uncertainty. It has also been argued that certain inefficiencies of physical markets are more acute in EM (e.g. sellers have greater anonymity since their identity is masked by a web site, products are difficult to represent in an online environment, and the transparency of the transaction process is also low at times) (Williamson, 1985; Hodgson, 1997; Tan and Thoen, 2001). Given this uncertainty that pervades EM (Clemonset al., 2002), and the belief that hierarchical coordination reduces uncertainty, hierarchical transactions may have continued to dominate the HMI over a greater part of the past decade or so.

Our results (related to 2003-2007), on the other hand, are consistent with the notion that in recent years, the HMI has been more market-like. We believe that this may be due to the increasingly important role being played by the intermediaries. By offering unbiased institutional mechanisms that can provide better information or avenues for recourse if vendors act against the interests of consumers, intermediaries have been argued to reduce consumer uncertainty related to EM transactions (Hart and Saunders, 1997; Pavlouet al., 2007). There is a need for trust in the face of uncertainty (Akerlof, 1970; Datta and Chatterjee, 2008), and intermediaries serve as institutional mechanisms providing such trust (Datta and Chatterjee, 2008).

P2andP3argued the role of CC in mediating the relationship between IT and the economic structure (i.e. whether EM or electronic hierarchies). As discussed earlier, our results are consistent with the proposition that IT has an effect on CC during the entire period (i.e. 1995-2007), as well as separately within each of the three sub-periods. This corresponds with prior research that has argued that IT reduces CC (e.g. Brynjolfssonet al., 1994; Bakos and Brynjolfsson, 1993; Benjamin and Wigand, 1995; Chircu and Kauffman, 2000; Bakos, 1997; Granadoset al., 2006). Advancements in IT make it easy to substitute manual human tasks with automation (Bresnahan et al., 2002), resulting in a decrease of the CC.

Specifically, within the HMI, our evidence was found to be consistent with the assertion that IT reduces the coordination efforts related to researching about (and eventually obtaining) a mortgage. Using communications and coordination technologies described earlier, a borrower can go online to seek information about the application process, and then can apply to multiple lenders by just completing one application. Indeed, the time and other resources necessary to initiate and complete the home mortgage transaction have been dramatically reduced during the time periods covered by our study, as exemplified in the following quote (Garritano, 2006):

At the broker and the small banker level there is a lot of emphasis on imaging and back-office automation, he [A.W. Pickel III, president of Lenexa, Kansas.-based Leader One Financial Corp.] pointed out. We take it further here. We take the application online, use PaperClip Software as our storage facility and we underwrite from that paperless file.

Interestingly, while the proposition that IT has a negative influence on CC was corroborated by the data, the proposed relationship between CC and EACM

18

was empirically refuted – our results indicated that this reduction in CC does not necessarily indicate a move toward markets (as predicted by the EMH). While this result initially appeared surprising, we believe that it has reasonable explanations. For example, Gurbaxani and Whang (1991) argued that IT reduced CC for both market-based and hierarchy-based governance. Furthermore, Grover and Ramanlal (1999) argue that a reduction of CC in a previously monopolistic supply chain made the tightly coupled supply chain (in other words, the hierarchy) easier to sustain. Hence, it cannot be unilaterally predicted that innovations in IT would always lead to market-based forms of governance. In fact, as suggested above, the reduction of CC can influence a move toward both markets and hierarchies, or even curb the move toward markets from existing hierarchies. Given that a market-like structure (as compared to a hierarchical structure) has a greater amount of uncertainty (Kauffman and Mohtadi, 2004; Granadoset al., 2007), it is not surprising that the structure of the HMI resembled an electronic hierarchy (e.g. Wigandet al., 2005), rather than the market.

We see that the posited effect of CC-mediated move toward markets was not empirically refuted only for the 2003-2007 time period. We believe that there are two possible explanations for this result. First, as argued earlier, uncertainty is one of the prime reasons why the industry moved toward a hierarchical structure. Given that intermediaries are able to reduce this uncertainty to a great extent, and prior research suggests that they have been on the rise in recent years (Datta and Chatterjee, 2008), intermediaries could have prompted the move of the HMI toward markets during the third time period (i.e. 2003-2007).

Second, IT coordination, was, until recently, based on EDI (Wigand et al., 2005), which was expensive and complex (Steinfieldet al., 2005). Such costly standards made it difficult for smaller industry players to enter or survive in the HMI, with a result that even in the primary market of the HMI, consumers were left with few choices for loan providers, and these choices generally pertained to the already well-established industry leaders. In effect, such costly standards can be understood to be “structures of domination” (Crowstonet al., 2001, p. 173) controlled by the industry leaders. However, in recent years, the standardization of coordination in the industry has led to better (and less expensive) data exchange and information transparency, which has driven the move toward EM (Granadoset al., 2006).

The above discussion suggests the effect of IT on the HMI has changed since Hess and Kemerer conducted their research in the early 1990s. One of the reasons for this change is the growing dominance and commercialization of the internet, which has paved the way for the development of different efficient market mechanisms (e.g. intermediaries). In summary, our data indicates that, while the propositions of the EMH may not have been empirically valid before or soon after Hess and Kemerer’s study, in recent years, the EMH appears to reflect the state of the HMI. The evidence regarding the relative dominance of market-based mechanisms in this industry appears to be growing. We believe that such an increasing move toward more market-based mechanisms through increased competition – due to a variety of loan originators, including traditional institutions such as Wells Fargo and Citibank and internet specialists such as Quicken Loan and E-Loan (Applegate, 2000; cf. Datta and Chatterjee, 2008) – provides much greater price fairness to the end-consumers (as noted by Brynjolfsson and Smith, 2000). A move toward markets may have reduced some of the power held by the major industry players, especially because of reduced profit margins (Benjamin and Wigand, 1995). However, we feel that the industry as a whole, and especially the consumers, are beginning to benefit more

19

from this recent market-based governance, realizing Benjamin and Wigand’s (1995) prediction of this very phenomenon more than a decade earlier.

Contribution

Our paper contributes to the existing literature on the EMH and the HMI in multiple ways. First, it is one of the few empirical attempts at validating the EMH within the HMI since Hess and Kemerer (1994). Given the number of years that have elapsed since Hess and Kemerer’s work was published in 1994, and the occurrence of other significant technology-related events that have happened around the world since then (e.g. the “dotcom burst,” Y2K), we felt that it was important to re-evaluate the validity of the EMH. By analyzing data over a significant period of time (i.e. from 1995 to 2007), this study provides a more in-depth longitudinal examination of the EMH within the HMI, thereby going beyond existing studies in the literature. While the EMH found limited support in the periods 1995-1999 and 2000-2002, the finding that recent patterns in the HMI are more consistent with EMH propositions should be encouraging news for researchers who have intellectually supported, and/or based their work on, the EMH. The results hold special implications for managerial and consumer decision making in EM. This is because EMH builds upon TCE, which is a theory of managerial choice and decision-making incorporating core behavioral assumptions about human nature – bounded rationality, opportunism, and risk neutrality (as noted in “Introduction”). Of all these behavioral assumptions, our results are perhaps most indicative of the salience of opportunism. Opportunism arises in an uncertain market environment (Datta and Chatterjee, 2008). Datta and Chatterjee (2008) also argue that, due to this possibility of opportunism, intermediaries are required when the consumer faces uncertainty in decision making. Therefore, the existence of loan brokers/ intermediaries (such as LendingTree) alleviates consumer uncertainty arising from the opportunistic tendencies of loan providers. Indeed one of the reasons for the rise of EM in recent years in the HMI (as showcased in our study) is that consumers now feel safer from seller opportunism due to the existence of intermediaries providing guarantees. Such intermediaries may also be interpreted as “structures of legitimation” (guarding against opportunism) in EM (Crowstonet al., 2001, p. 174).

A second contribution of the study is an explicit operationalization of the EMH model. While the EMH has been viewed as a major theoretical perspective in e-commerce research, there has been a lack of a precise and explicit operationalization of the EMH. Our study addresses this void in the literature.

Third, our study not only tests the EMH within the HMI, but also provides an understanding as to “why” it now holds (or did not hold) within this industry. For example, it suggests that dominance of market-based transactions in recent years (as compared to the years before the turn of the last millennium) is attributable specifically to the rise of intermediaries and the reduction of CC through development of industry-level standards.

A fourth major contribution of this study is the showcasing of how a qualitative case study using H-D logic can be conducted using published “texts.” This is especially significant for two reasons. The first reason is that case studies have often been viewed as subjective and interpretive, and this study shows that they can follow the same line of execution as a quantitative positivist study, with objective theory testing. The second reason is that this study highlights the possibility of using case research (whether interpretive or positivist) to leverage the wealth of such data (publications or “texts”) available to researchers, which can be used to good effect in a qualitative study.

20

Often, qualitative case studies require significant time and effort, for example, to gain researcher entry to an organization, negotiate terms and conditions, observe the phenomenon over a period of time, conduct interviews, and then analyze the large volume of data. As a result, qualitative researchers have acknowledged criticisms of qualitative research being labor-intensive, stressful, and demanding (Miles, 1979). In this context, our study showcases a genre of qualitative research that does not require fieldwork in a traditional sense while at the same time ensuring the rigor of such qualitative studies. In fact, a strategy based on published data (like ours), can be argued to contribute toward increased relevance and generalizability of the study. It is also an approach that can be used by colleagues in geographical areas where there are not too many “case sites” readily available. Moreover, this method offers a streamlined opportunity to study the impact of IT on people (and vice versa) by using sources from the popular press.

Fifth, on a related note, another important contribution of the paper is the provision of guidelines (through our articulation of our empirical strategy) on how to conduct a positivist qualitative study. Qualitative research, in comparison to quantitative research, often has fewer guidelines and formulations for the researcher to follow (Miles, 1979). We hope that the discussion presented here – related to operationalization, data collection, variable coding, empirical analysis, and empirical refutation strategy – provides future researchers with relatively clear-cut guidelines.

Future implications

Practical implications

Our research shows that EM mechanisms have increased in dominance in recent years. This finding provides insights regarding how organizations can concentrate on enabling efficient market mechanisms so as to increase consumer confidence and benefits from the online loan procurement process.

One overall focus would be to encourage consumers to engage in EM transactions by reducing concerns which force many of them to refrain from transacting in EM (Datta and Chatterjee, 2008). These concerns are as follows (Datta and Chatterjee, 2008):

. concerns regarding the product (loan product, in our case) purchased;

. concerns regarding the transaction (loan procurement, in our case) process; and

. concerns regarding the vendor (lender, in our case).

Possible organizational strategies stem from the above. For example, in electronic environments, there is limited opportunity to obtain firsthand credible knowledge about any product, especially due to the absence of a human representative (Oorni, 2003). Within the HMI, procurement of a loan has often been described as being very complex. Even the somewhat straightforward fixed-term loan is complicated due to the different available rates and fee combinations. Further, due to the inherently asymmetric nature of the online environment (Granadoset al., 2006), and given that loans are very information-intensive products, complexities faced by the consumers are compounded. However, organizations may develop strategies to alleviate such concerns. For example, one way might be to reduce the number of possible options that are made available to a potential buyer. This can be done by allowing lenders to make preliminary offers to a specific potential borrower based on that borrower’s personal characteristics and preferences. In general, products (i.e. loan

21

offerings in this case) that are less complex are likely to be purchased using market mechanisms (Palvia and Vemuri, 1999). Simple products rarely need customization, and can be purchased from any lender. So, keeping loan offerings simple could be a way lenders increase consumer confidence in online loan transactions.

Another strategy could be to increase efficiency of the loan request and approval process, and here IT can play a critical role. Due to recent advancements in IT, especially in mortgage banking, the principal assets relevant to loan processing are “largely fungible” (Jacobides and Hitt, 2005, p. 1211), and have low asset specificity. For example, loan applications can potentially originate from anywhere (e.g. home, office, etc.), or can be processed by anyone from anywhere (e.g. by an individual residing in India, due to IT enabled communication), and at any time (credit scoring and underwriting can take place without delay since they can be automated). Organizations can leverage this reduced site specificity, human asset specificity, and time specificity in order to streamline and expedite their loan request and approval process, thus significantly reducing consumer concerns related to the loan generation and approval process. E*Trade Financial, for example, allows the potential borrower to apply, choose a loan product, lock an interest rate, and schedule (a time) for an appraisal and document signing, online, thus significantly alleviating consumer concerns regarding the loan procurement process.

Implications for future research

This study has the following implications for future research. First, there is the issue of the performance of the EMH outside of the HMI. The EMH, being a general theory, is about industries in general, not just the HMI. If the EMH is indeed valid, then the propositions (in Table I) should survive in other industries as well, such as health care, retail brokerages, banking, education, and entertainment. Future researchers can thus attempt to collect data from different industries (following our strategy) and thus compare the validity of the EMH across multiple industries.

Second, there is a need to investigate the validity of the EMH as additional evidence emerges in the HMI. Since our study ends in 2007 we believe that there is an opportunity for future researchers to subject EMH to similar deductive falsification testing beyond 2007. Particularly interesting would be to perform a similar analysis for the economic crisis starting in 2008.

Third, future studies could augment the methodological approach by looking at the consumer’s perspective. While the analysis of papers in the trade press is valuable for the reasons mentioned in this study, additional data gathered (either qualitative or quantitative) directly from the end consumers might be used to test the EMH (or other competing theories). Thus, future studies could use the same falsification technique by gathering alternate sources of data from end consumers.

To conclude, the EMH is seen by many scholars as the foundation of much research in the IS discipline, especially in the e-business arena. This study is among the few that systematically articulates the propositions of the EMH and formally subjects them to attempts at empirical refutation. Indeed, through a study of artifacts, much like a historical investigation, the study finds that the patterns in the real world of HMI increasingly match the theory’s prediction, which we see as good news for our discipline. A major premise of the discipline has been that IT, purposely designed and implemented to address the requirements of a given organizational, social, or economic setting, can be beneficial to the people in that setting (Hevneret al., 2004). The EMH, which has survived rigorous testing in this study, can be harnessed not only to design

22

and implement technology for relevant settings, but also to provide an exemplar of the sort of theory that the information systems discipline can and should develop, test, and apply.

References

Ackroyd, S. and Hughes, J.A. (1992),Data Collection in Context, Longman, New York, NY. Akerlof, G. (1970), “The market for ‘lemons’: quality uncertainty and the market mechanism”,

Quarterly Journal of Economics, Vol. 84 No. 3, pp. 629-50.

Alchian, A.A. and Demsetz, H. (1972), “Production, information costs and economic organization”,American Economic Review, Vol. 62 No. 5, pp. 777-95.

Aoki, M. (1984), The Cooperative Game Theory of the Firm, Oxford University Press, New York, NY.

Applegate, L.M. (2000), “Quickeninsurance: the race to click and close”,Harvard Business School Case, 9-800-295.

Bakos, J.K. (1997), “Reducing buyer search costs: implications for electronic marketplaces”,

Management Science, Vol. 43 No. 12, pp. 1676-92.

Bakos, J.Y. and Brynjolfsson, E. (1993), “Information technology, incentives, and the optimal number of suppliers”, Journal of Management Information Systems, Vol. 10 No. 2, pp. 37-53.

Bakos, J.Y. and Nault, B.R (1997), “Ownership and investment in electronic networks”,

Information Systems Research, Vol. 8 No. 4, pp. 321-41.

Bakos, Y., Lucas, Henry C. Jr, Oh, W., Simon, G., Viswanathan, S. and Weber, B.W. (2005), “The impact of E-commerce on competition in the retail brokerage industry”, Information Systems Research, Vol. 16 No. 4, pp. 352-71.

Bauer, R.A. (1960), “Consumer behavior as risk taking”, in Hancock, R.S. (Ed.), Dynamic Marketing for a Changing World, American Marketing Association, Chicago, IL, pp. 389-98.

Benjamin, R. and Wigand, R. (1995), “Electronic markets and virtual value chains on the information superhighway”,Sloan Management Review, Vol. 36 No. 2, pp. 62-72. Bresnahan, T.F., Brynjolfsson, E. and Hitt, L.M. (2002), “Information technology, workplace

organization, and the demand for skilled labor: firm-level evidence”,The Quarterly Journal of Economics, Vol. 117 No. 1, pp. 339-76.

Brynjolfsson, E. and Smith, M.D. (2000), “Frictionless commerce? A comparison of Internet and conventional retailers”,Management Science, Vol. 46 No. 4, pp. 563-85.

Brynjolfsson, E., Malone, T.W., Gurbaxani, V. and Kambil, A. (1994), “Does information technology lead to smaller firms?”,Management Science, Vol. 40 No. 12, pp. 1628-44. Chatterjee, S., Chakraborty, S., Sarker, S., Sarker, S and Lau, F. (2009), “Examining the success

factors for mobile work in healthcare: a deductive study”, Decision Support Systems, Vol. 46 No. 3, pp. 620-33.

Chiles, T.H. and McMackin, J.F. (1996), “Integrating variable risk preferences, trust, and transaction cost economics”,The Academy of Management Review, Vol. 21 No. 1, pp. 73-99. Chircu, A.M. and Kauffman, R.J. (2000), “Reintermediation strategies in business-to-business electronic commerce”,International Journal of Electronic Commerce, Vol. 4 No. 4, pp. 7-42. Choudhury, V., Hartzel, K.S. and Konsynski, B.R. (1998), “Uses and consequences of electronic markets: an empirical investigation in the aircraft parts industry”,MIS Quarterly, Vol. 22 No. 4, pp. 471-507.

Clemons, E.K., Hann, I.-H. and Hitt, L.M. (2002), “Price dispersion and differentiation in online travel: an empirical investigation”,Management Science, Vol. 48 No. 4, pp. 534-49.

23

Clemons, E.K., Reddi, S.P. and Row, M.C. (1993), “The impact of information technology on the organization of economic activity: the ‘move to the middle’ Hypothesis”, Journal of Management Information Systems, Vol. 10 No. 1, pp. 73-95.

Coase, R. (1937), “The nature of the firm”,Economica, Vol. 4 No. 16, pp. 386-405.

Cohen, J. (1960), “A coefficient of agreement for nominal scales”,Educational and Psychological Measurement, Vol. 20, pp. 37-46.

Crowston, K., Sawyer, S. and Wigand, R. (2001), “Investigating the interplay between structure and information and communications technology in the real estate industry”,Information Technology & People, Vol. 14 No. 2, pp. 163-83.

Daniel, E. and Klimis, G.M. (1999), “The impact of electronic commerce on market structure: an evaluation of the electronic market hypothesis”,European Management Journal, Vol. 17 No. 3, pp. 318-25.

Darke, P., Shanks, G. and Broadbent, M. (1998), “Successfully completing case study research: combining rigour, relevance and pragmatism”,Information Systems Journal, Vol. 8 No. 4, pp. 273-89.

Datta, P. and Chatterjee, S. (2008), “The economics and psychology of consumer trust in intermediaries in electronic markets: the EM-trust framework”, European Journal of Information Systems, Vol. 17 No. 1, pp. 12-28.

Fine, C.H. and Whitney, D.E. (1996), “Is the make-buy decision a core competence?”, discussion paper, MIT Center for Technology, Policy, and Industrial Development, Sao Paolo, June 9-12. Galunic, D.C. and Eisenhardt, K.M. (1996), “The evolution of intracorporate domains: divisional charter losses in high-technology, multidivisional corporations”, Organization Science, Vol. 7 No. 3, pp. 255-82.

Garritano, A. (2006), “Study finds lenders embracing E-Mortgages”,National Mortgage News, Vol. 31 No. 13, p. 2.

Glaser, B. and Straus, A. (1967),The Discovery of Grounded Theory: Strategies for Qualitative Research, Aldine, Chicago, IL.

Glymour, C.N. (1980),Theory and Evidence, Princeton University Press, Princeton, NJ. Granados, N., Gupta, A. and Kauffman, R.J. (2006), “The impact of it on market information and

transparency: a unified theoretical framework”,Journal of The Association of Information Systems, Vol. 7 No. 3, pp. 148-78.

Granados, N.F., Gupta, A. and Kauffman, R.J. (2007), “IT-enabled transparent electronic markets: the case of the air travel industry”,Information Systems and eBusiness Management, Vol. 5 No. 1, pp. 65-91.

Grover, V. and Ramanlal, P. (1999), “Six myths of information and markets: information technology networks, electronic commerce, and the battle for consumer surplus”, MIS Quarterly, Vol. 23 No. 4, pp. 465-95.

Gurbaxani, V. and Whang, S. (1991), “The impact of information systems on organizations and markets”, Association for Computing Machinery. Communications of the ACM, Vol. 34 No. 1, pp. 59-73.

Hart, P. and Saunders, C. (1997), “Power and trust: critical factors in the adoption and use of electronic data interchange”,Organization Science, Vol. 8 No. 1, pp. 23-42.

Hess, C.M. and Kemerer, C.F. (1994), “Computerized loan origination systems: an industry case study of electronic markets hypothesis”,MIS Quarterly, Vol. 18 No. 3, pp. 251-76. Hevner, A.R., March, S.T., Park, J. and Ram, S. (2004), “Design science in information systems

research”,MIS Quarterly, Vol. 28 No. 1, pp. 75-105.

Hodgson, G.M. (1997), “The ubiquity of habits and rules”, Cambridge Journal of Economics, Vol. 21 No. 6, pp. 663-84.

24

Jacobides, M.G. (2001), “Technology with a vengeance: the new economics of mortgaging”,

Mortgage Banking, Vol. 62 No. 1, pp. 118-27.

Jacobides, M.G. and Hitt, L.M. (2005), “Losing sight of the forest for the trees? Productive capabilities and gains from trade as drivers of vertical scope”,Strategic Management Journal, Vol. 26 No. 13, pp. 1209-27.

Kauffman, R.J. and Mohtadi, H. (2004), “Proprietary and open systems adoption: a risk-augmented transactions cost perspective”,Journal of Management Information Systems, Vol. 21 No. 1, pp. 137-66.

Knight, F.H. (1985), Risk, Uncertainty, and Profit, University of Chicago Press, Chicago, IL, Reprint edition of 1921 with a foreword by George J. Stigler edition.

Kraut, R., Steinfield, C., Chan, A.P., Butler, B. and Hoag, A. (1999), “Coordination and virtualization: the role of electronic networks and personal relationships”,Organization Science, Vol. 10 No. 6, pp. 722-40.

Landis, J.R. and Koch, G.G. (1977), “The measurement of observer agreement for categorical data”,Biometrics, Vol. 33 No. 1, pp. 159-74.

Lee, A.S. (1989), “A scientific methodology for MIS case studies”,MIS Quarterly, Vol. 13 No. 1, pp. 33-50.

Lee, A.S. and Hubona, G.S. (2009), “A scientific basis for rigor in information systems research”,

MIS Quarterly, Vol. 33 No. 2, pp. 237-62.

Liang, T. and Huang, J. (1998), “An empirical study on consumer acceptance of products in electronic markets: a transaction cost model”,Decision Support Systems, Vol. 24 No. 1, pp. 29-43.

Malone, T.W., Yates, J. and Benjamin, R.I. (1987), “Electronic markets and electronic hierarchies”,

Communications ACM, Vol. 30 No. 6, pp. 484-97.

Markus, M.L. (1989), “Case selection in a disconfirmatory case study”, in Cash, J.I. and Lawrence, P.R. (Eds),The Information Systems Research Challenge: Qualitative Research Methods, Volume 1, Harvard Business School Press, Boston, MA, pp. 20-6.

Miles, M.B. (1979), “Qualitative data as an attractive nuisance: the problem of analysis”,

Administrative Science Quarterly, Vol. 24 No. 4, pp. 590-601.

Morris, R. (1994), “Computerized content analysis in management research: a demonstration of advantages & limitations”,Journal of Management, Vol. 20 No. 4, pp. 903-31.

Neuman, W.L. (2004),Basics of Social Research: Qualitative and Quantitative Approaches, 2nd ed., Pearson Education, Boston, MA.

Oorni, A. (2003), “Consumer search in electronic markets: an experimental analysis of travel services”,European Journal of Information Systems, Vol. 12 No. 1, pp. 30-40.

Palvia, S. and Vemuri, V. (1999), “Distribution channels in electronic markets: a functional analysis of the ‘disintermediation’ hypothesis”, Electronic Markets, Vol. 9 No. 2, pp. 118-25.

Pavlou, P.A., Liang, H. and Xue, Y. (2007), “Understanding and mitigating uncertainty in online exchange relationships: a principal-agent perspective”,MIS Quarterly, Vol. 31 No. 1, pp. 105-36.

Popper, K. (1985),Popper Selections, Princeton Univ. Press, Princeton, NJ.

Rindfleisch, A. and Heide, K.B. (1997), “Transaction cost analysis: past, present, and future applications”,Journal of Marketing, Vol. 61 No. 4, pp. 30-54.

Sarkar, M.B., Butler, B. and Steinfield, C. (1995), “Intermediaries and cybermediaries: a continuing role for mediating players in the electronic marketplace”,Journal of Computer-Mediated Communication, Vol. 1 No. 3.