This paper proposes a simple non-parametric procedure to evaluate the speed of adaptation in the presence of nonlinearity using the maximum Lyapun exponent of the time series. The purpose of this paper is to propose a simple measure of the persistence of PKM deviations based on the largest Lyapun exponent of the nonlinear real exchange rate adjustment process. Second, it is similar to the half-life measurement in the sense that it can be interpreted as the half-lives of locally linearized nonlinear processes.

This function can be seen graphically by the shape of the impulse response function in Figure 1. In addition to q0, the shape of the impulse response also depends on the magnitude and sign of current and future shocks. Below we consider an alternative measure of persistence based on the largest Lyapunov exponent in the time series.5.

The largest Lyapunov exponent is a measure of the stability of a dynamic system in terms of sensitive dependence on initial conditions. Since the denominator of the linear half-life τ is the convergence rate ln|ρ|, we can construct an analogous persistence measure for a stable nonlinear system by replacing ln|ρ| with λ or τ∗ ≡ ln(1/2)/λ. In general, the nonlinear AR (5) model can be estimated using a nonparametric regression technique without specifying the functional form as in the TAR or STAR models.

However, it is a half-life-like measure in the sense that it can be interpreted as the half-life of the locally linearized non-linear processes.

Simulation

In the empirical section we also report the conÞdence interval for the nonparametric measureτb∗ based on the asymptotic distribution of the local quadratic estimator of the Lyapunov exponent derived in Shintani and Linton (2001).7 In Murray and Papell's (2002) study they used a median unbiased estimator of ρ and reported that conÞdence intervals of b. For a unit root process, the linear measureτb is consistent in the sense that half-life estimates diverge to infinity as the sample size increases. In Shintani and Linton (2001) it is shown that the Lyapunov exponent based on the local quadratic regression converges to zero when the true process is a random walk, or m(qt−1) = qt−1 and an iid error in (5).

This implies that τb∗ is also consistent in the sense that it diverges to infinity for a unit root case. First, when c = 0, (4) reduces to a simple linear model with AR parameter 0.5 and the true half-life is one year. As expected, since there is no misspecification with linear measure in this case, the bias of the linear measure is smaller than that of the nonparametric measure.

When the true half-life is as high as 5.70, unit roots are obtained for several cases, resulting in infinite half-life estimates (the median is 8.62). On the other hand, the nonparametric measurement τb∗ does not suffer from the upward bias observed in the linear measurement. Although the nonparametric estimates depend to some extent on the selection of the smoothing parameter, the small sample bias, as well as the variability in the estimates, appears to be significantly smaller than that of linear measurements.

When c = 0, both non-parametric and linear measurements come closer to the true half-life compared to the case at T = 100. As c increases, the upward bias of linear measurements is greater than that for T = 100 cases, while relatively accurate estimates are obtained with non-parametric measurements with a smaller smoothing parameter. However, the upward bias of the linear measurement is larger compared to that of the nonparametric measurement.

In summary, the simulation result supports Taylor's (2001) discussion that inappropriate linear specification can lead to large half-life estimates if there is nonlinearity in the fitting process.

Data

Cointegrating Rank Test

Estimation of Two Convergence Measures

This point becomes clearer if we plot the nonparametric estimates of the rate of adjustment at each data point. It suggests that the data are favorable to our conjecture about the presence of trade costs as a source of non-linearity. At the same time, the wide conÞdence intervals for linear measures show the uncertainty in the point estimates.

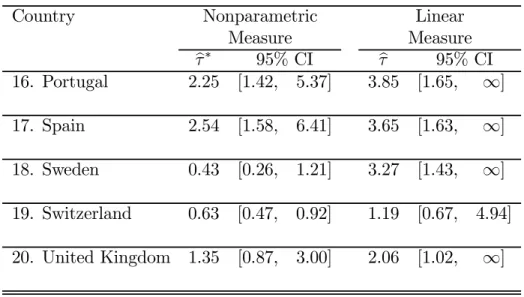

These observations are consistent with the previous things in the literature as well as with the result of the linear cointegrating rank test in this paper. When the non-parametric measure is used, half-lives are again shorter than those based on long-term data. Most notably, however, the nonparametric method provides smaller half-life estimates than the corresponding linear estimates for all countries except Canada.

The median of the nonparametric half-life measure is 1.44 years, and the median difference between the nonparametric and linear measures is 0.99 years (the mean half-life and difference are 1.53 and 1.08 years, respectively, when Canada is excluded). Regarding the precision of the point estimates, the confidence intervals of the nonparametric half-lives are significantly shorter than those of the linear half-lives. In some cases, the 95% upper bounds for the nonparametric half-lives are actually lower than the corresponding point estimates based on the linear measure.

The simulation result on the Þnite sample properties of the non-parametric measure is found to be encouraging. When the true process has TAR or STAR structure, half-lives based on the linear measure suffer from upward bias due to misspecification. In contrast, the non-parametric measure provides relatively accurate estimates for both linear and non-linear adjustment process.

When annual historical data are used, the non-parametric method yields a reduction of over two years in the half-life of British/American organisms. In the first case, infinite half-lives are excluded from the intervals in almost all cases. Real exchange rate behavior: the recent exchange rate from the perspective of the past two centuries.

Sampling and specification biases in mean-reversion tests of the law of one price. Nonlinear mean reversion in real exchange rates: Towards a solution to purchasing power parity conundrums.

Linear Impulse Response and Half- L ife

Nonlinear Impulse Response and Half- L ife