These actions in which one shareholder sues in the name and on behalf of the company. Second, our takeover-oriented class actions share many of the same characteristics found in securities and derivatives fraud cases as indicators of agency costs of litigation.

SHAREHOLDER LITIGATION IN DELAWARE

Overview of the Data: Delaware Court of

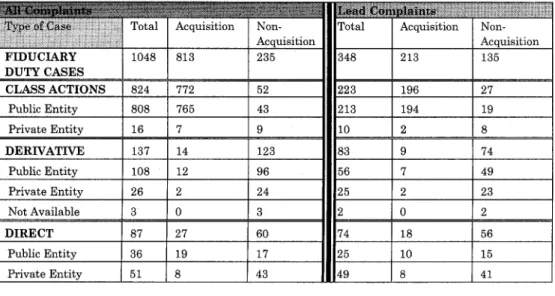

75 percent of the civil cases filed in the New Castle County Chancery Court are classified as corporate cases (1280 of 1716), 148 a number that will not surprise anyone familiar with this court. The remaining 25 percent of the civil cases reflect that court's less well-known jurisdiction over other equity cases such as trusts and estates or complaints seeking injunctions in a variety of non-corporate cases for alleged damages.149. Looking more closely at the corporate docket, we find in Table 1B that nearly 80 percent of the complaints filed (1003 of 1280) raised fiduciary duty issues, which are the subject of this article, while the remaining cases deal with a number of more discrete corporate issues (we will discuss these cases in more detail in Section C below).

Thus, fiduciary disputes accounted for approximately 60 percent of the New Castle County Chancery Court's total caseload.150. We found no complaints filed with the Sussex County Division of the Court of Chancery that fell within the scope of our search for fiduciary duty cases. For this project, we read each of the 1,325 complaints classified as corporate filings in the Chancery Court filing system for New Castle County.

See generally COURT OF CHANCERY OF STATE OF DELAWARE for essays on special features of this court.

The Fiduciary Duty Claims

Almost all (94 percent: 772 of 824) class actions arise in a takeover situation, whereas almost all (90 percent: 123 of 137) of the derivative lawsuits arise in a non-acquisition situation. Although there is more to say about derivative claims, our focus in this paper is on class actions, which are by far the largest segment of the data set.152 Put another way, class actions constitute almost all of the cases brought against public corporations, and the class actions are almost always brought against public companies. Class actions virtually all arise in an acquisition context and constitute an even higher percentage of cases arising from acquisitions.

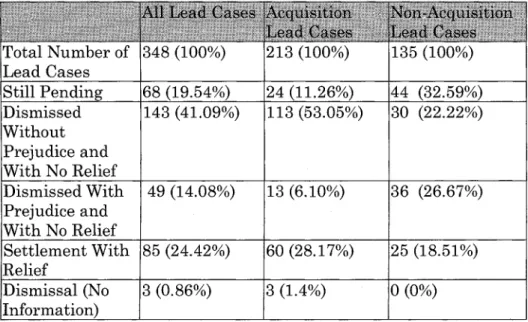

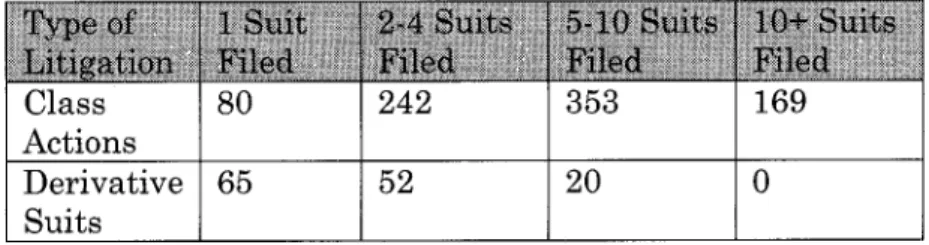

Before we go any further, we should note that in proxy litigation it is not unusual to see multiple complaints filed in relation to the same transaction as law firms fight for a piece of the proceedings. The main result of handling potential customer complaints is to mitigate some of the trends just discussed. During the two-year period we studied, 348 main appeals were filed in the Chancery Court, of which approximately 61 percent (213) were class actions against public companies aimed at takeovers.

A brief overview of the remaining business cases Before we move on to discussing the fiduciary duty cases in more detail.

A Brief Overview of the Remaining Corporate

2004] THE NEW EVENT OF SHAREHOLDER LITIGATION 169 number of lead complaints filed in federal securities fraud actions, we find that in 1999 a total of 219 such actions were brought, while in 2000 there were 202 federal securities fraud complaints. Appraisal proceedings make up a very small portion of the Chancery Court docket (about 1 percent or 22 cases out of the two-year total of 1,716 cases filed), which is consistent with earlier research finding that appraisal is an underused remedy in Delaware. 159 Indemnification litigation pursuant to section 145 of the Delaware Corporate Code constitutes an even smaller percentage of the cases in the sample, only 12 cases in total. Finally, actions involving the various code provisions relating to the liquidation of the corporation's business (including dissolution, appointment of a receiver and appointment of a custodian) comprise a larger proportion of the statutory caseload, with 45 cases (or approx. 2.5 percent of the total). file of the court).

The other two categories of cases shown on Table 3 are contract cases (33 cases)160 and claims to determine stock ownership. Statutory matters of this type have been written about elsewhere.162 In this paper we focus our attention on fiduciary duty. In recent years, the Court has allowed parties to a contract otherwise unrelated to Delaware to choose the Chancery Court as the forum to decide all disputes arising under the terms of their agreement.

This choice of forum clause is popular because the Chancery Court provides quick, expert decisions to resolve these cases.

Who Gets Sued in Fiduciary Duty Litigation?

While class actions are almost always brought against public companies, derivative suits are more evenly distributed, with about 70 percent against public corporations and 30 percent naming closely held companies. 66 If we look at direct lawsuits, about 65 percent of these complaints list private entities as defendants. There are many reasons to think that lawsuits by small investors in private companies are different from those filed by small investors in public companies.16 7.

The average market capitalization for publicly traded companies subject to derivatives cases is $1.138 billion, with the 25th percentile being $219.5 million and the 75th percentile being $6.15 billion.6 8 This limit is significantly greater than for class actions, where the. This is driven upward by the derivative lawsuits for improper financial data, lack of oversight and misleading statements, which are typically brought against very large companies. Derivative cases differ from class action cases in that derivative cases comprise a substantial portion of cases brought against closely held companies, illustrating that derivative litigation plays a distinctive role in private companies.

The companies sued in derivative suits are less likely to be headquartered in California than the companies in class action lawsuits, with the Golden State companies accounting for only 10 percent of the derivative suits (compared to 16 percent of the class actions).169 Internet and computer companies make up about 19 percent of the derived sample, in the same range as with class actions, but lower than observed for securities fraud cases.170 However, there is little reason to expect the same pattern among the defendants in our cases as in the federal cases, as our class actions challenge the terms of acquisitions, while the federal class actions allege securities fraud, often in the IPO context.

Acquisition Cases: Friendly, Hostile, Arm's

Two other types of friendly deals, management buyout proposals (MBOs) and sales to a friendly third party, each result in about 23 percent of the complaints shown in Table 5. MBO cases trigger conflict-of-interest claims because of the potential to direct a company's board of directors to give its to managers special preferences in control sales. Third-party transactions raise less obvious conflict-of-interest concerns, such as the possibility that managers received better treatment than other shareholders because they received side payments from the bidder.

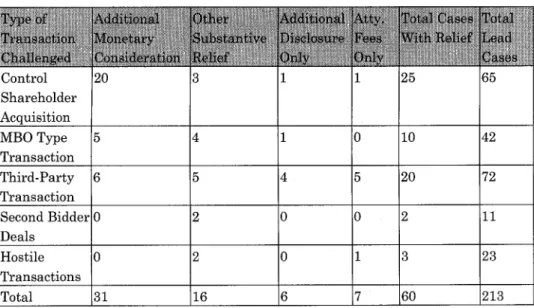

Ten of the 27 leading direct acquisition cases are complaints filed by bidders either in hostile transactions or in second-bidder situations. Hostile bid cases now outnumber other bidders, reflecting the extraordinarily large number of multiple complaints filed in the second bidder. There are 23 lead cases involving hostile takeovers, which also represents about 10 percent of the total number of lead cases.

While one might assume that the high number of appeals filed in second-party cases reflects either a strong legal claim or a high expected payoff to plaintiffs' attorneys, we actually find that this is not the case.

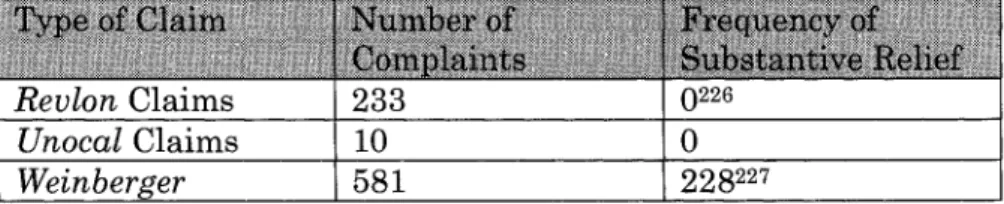

Frequency of Relief

ACQUISITION-ORIENTED CLASS ACTIONS: ARE THEIR

- Litigation Agency Costs Indicators

- Are There Indicators That Litigation

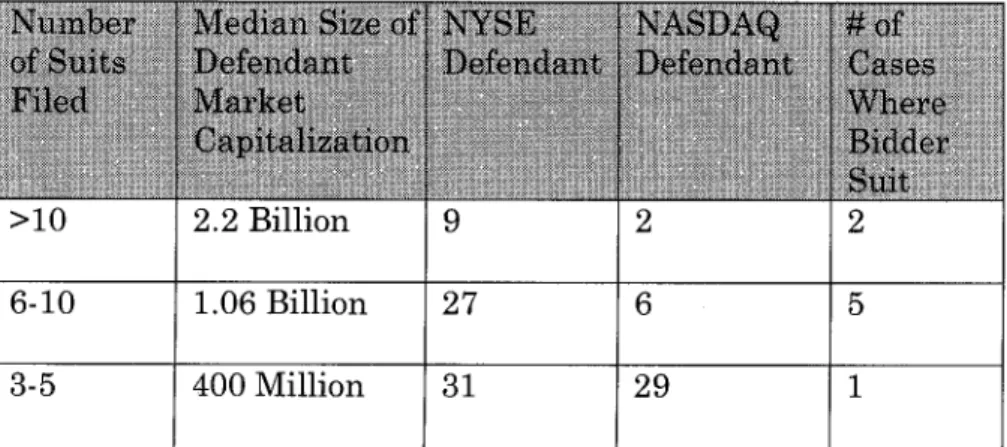

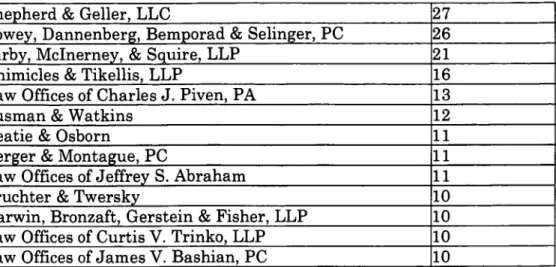

One of the most surprising findings of this study is the extraordinary number of takeover-oriented class actions filed in Delaware state courts. The similar speed in the filing of securities fraud cases, for example, raised concern during the debate over securities fraud class actions prior to the passage of the PSLRA in 1995.188 Another potential "indicator" of litigation agency costs concerns the identity of the law firms filing these cases.

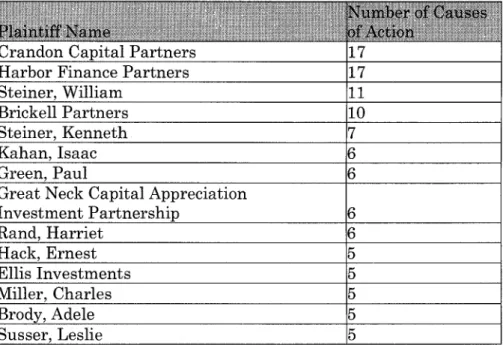

This makes the characteristics of named plaintiffs in class actions another potential indicator of agency costs of litigation. To summarize the discussion to this point, there are several characteristics of acquisition-oriented class actions brought in Delaware that mirror the characteristics of securities fraud class actions prior to the passage of the PSLRA. In short, a class action provides a mechanism to quickly resolve all claims arising from a transaction.

In contrast, average attorneys' fees in federal securities fraud cases from 1991 to 1996 were about 32 percent of.

Affirmative Relief in Acquisition Class Actions

- Control Shareholder Transactions

- Management Buyout Transactions

- Third-Party Friendly Transactions

- Hostile Bidder and Second Bidder

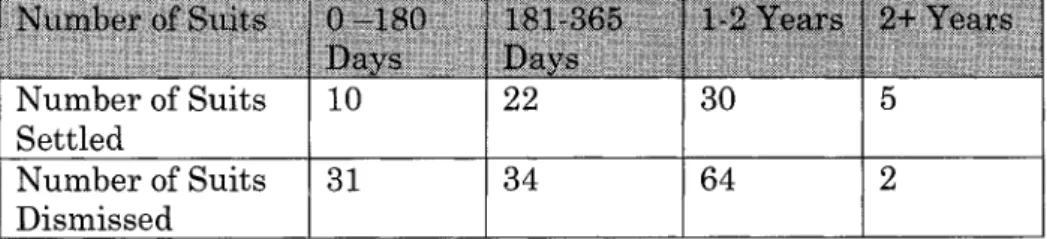

In contrast, in most class actions in our dataset, the target has already agreed to a transaction. We find four different types of settlements in these cases: additional monetary compensation paid to the target company's shareholders (over and above what was originally promised in the transaction announcement); other substantial relief, such as changes to the company's corporate governance structure; There are also other differences in the settlement frequency and form of settlement between countries.

We decided to examine how the total consideration (offer price plus settlement value) paid to shareholders in these settled cases compared to the consideration paid in the remainder of the controlling shareholder transactions resolved without relief. In most of the settlements we discuss in this section, we find that there is both a special committee working on behalf of the target shareholders, and a group of class action lawyers seeking an increase in the price paid in the transaction. search. In all five transactions where a second bidder lawsuit was filed, we find that the second bidder failed to gain control of the target company (four of these companies were bought by another bidder and in one case no transaction completed with any bidder).

With regard to litigation costs, we find that some parts of the traditional representative litigation story are.