No paragraph of this publication may be reproduced, copied or transmitted except with written permission or in accordance with the provisions of the Copyright, Designs and Patents Act 1988, or under the terms of any license permitting limited copying issued by the Copyright Licensing Agency, 90 Tottenham Court Road, London W1T 4LP.

Acknowledgments

Several versions of different parts of this book have appeared on the website of my company – Evolutionary Finance™ Ltd. Kevin Upson from JellyBean Web in Cambridge did a fantastic job designing my company's website, while Tony Donnelly from UBS helped immensely with valuable tips on setting up Evolutionary Finance™ Ltd's absolute return strategy vehicles , which are specifically designed to take advantage of the Evolutionary Finance™ Ltd. Financial principles espoused in this book.

Preface

Finally, in Chapter 8 we will tell the reader what we believe to be the overarching nature of our philosophy. In this book we focus exclusively on the financial consequences of the 'by-product' of human actions that generate information.

Introduction

Our goal is to correct this error primarily through a better understanding of the process of information construction itself and, more importantly, how it interacts with asset prices. By doing so, we are thus better able to predict the evolution of the shape of the time-dependent distribution of asset prices in response to this biologically-like molecular formation of information.

The “Old” View of Finance

- The efficient markets hypothesis: The traditional (albeit incomplete) standard-bearer for information assessment

- A little more on the link between the theory and the applied

- Cost, ability and speed: Important information determinants

- Do empirical studies of the EMH shed any light on the actual speed of information transferal?

- Is “Strong EMH” all there is to the “Traditional”

Consequently, the implications for "optimal" investment decision-making (and for financial engineering . "best practice") are very different in the "real world" to the theoretical purity of strong EMH/traditionalist utopia. It is the set of information that is assumed to be fully reflected in the security price at the appropriate time.

In rebuttal, we argue that while the benefits of the Gaussian shape (σ) may come in terms of mathematical utility (see later for more details), it comes at a considerable cost in terms of the adequacy of the assumptions of "traditional finance" in interpreting the prevailing orthodoxy of the "real world" of analytical and information behavior. In conclusion, we would argue that the mathematical utility of the Gaussian shape appears to have been placed before the relevance of traditional financial assumptions about the market (and information behavior in particular) to what we observe in the real world.

The “New” View of Finance

So where does Evolutionary Finance fit-in to the

In conclusion, then, rather than limiting ourselves to saying that our own field of evolutionary finance depends on any "new" interpretation of the view, we prefer to argue that what will be presented in the following chapters represents the fruit of an eclectic mix of components within each of challenges 1, 2 and 3 of the "new" view. We would only add that in the past too much time and effort was devoted to market structure and investor behavior, but not enough to the actual structure of the information itself. Herein lies our greatest contribution – simply by our modeling of the creation and shaping of information into a structured set of bytes, memes, themes and even general market sentiment as a result of a biological molecular evolutionary process.

The Mechanics of Modeling Information as an Evolutionary

Evolutionary information basics: Memetics and the contribution of Richard Dawkins

In his book The Selfish Gene (1976), Professor Dawkins devotes an entire chapter to the analogous connections between biological evolution and cultural evolution.3 In particular, Professor Dawkins coined the concept of 'memes' as the analogous metaphysical cousin of the ubiquitous gene.4 A coincidental insight that we will make extensive use of on the following pages. Professor Dawkins continually worked to disabuse readers of the idea that cultural evolution and genetic evolution are somehow irreconcilably intertwined. To his credit, Professor Dawkins has also given us some groundbreaking insights here on which we can build in our efforts.

Moving past the elementary: Taking the evolutionary information concept further into the field of finance

That is, there is a degree of latency within each byte of information that will only be unlocked when more information arrives. Indeed, in accordance with the following third point of our attack on IID, it will be established that the sequence of information has the potential to change the distributional consequences of a given byte of information on the net sum of existing information simply because of the presence of the Complex non-linear relationships between each information byte within a given information set. But to take our analogy further, we need to formalize our “information genome” framework in much more detail—this is the charter for the following section.

The building blocks of our evolutionary approach toward information in finance

Evolutionary biology Evolutionary finance Genetic information of an organism.. consisting of the entire gene sequence, which represents the entire base sequence. . resources). A mem is a subset of the information genome (. ϕa) and represents a specific final sequence of information bytes. This concludes our discussion of the building blocks of an evolutionary approach to information in finance.

Some consequences of our evolutionary approach toward modeling information

However, Darwinists would prefer a smooth continuous form for a mathematical representation of the process of evolution. For example, Shannon and Weaver (1963) demonstrated that the more new information enters a system, the faster the rate of decay (entropy) of the existing information set. This is only the tip of the proverbial iceberg when it comes to reaping some of the benefits of our evolutionary approach to information in the financial sphere.

How investors interpret Evolutionary Information

Further, we hope that we have provided some insight into the implications of the assumptions we have made in our formalization of this informative microstructure in Section 4.3. 45 The categorization of information into separate bundles is handled by separate areas of the brain. Behavioral Finance in particular has shown little understanding of the micro-fundamental building blocks of what we as investors come to perceive as "information" in the first place.

Putting it Altogether – An Evolutionary Model of

Stage I: Developing an intertemporal optimization model of information production/consumption and solving for

Since we are only dealing with the information aspect of the investor's long-term optimization problem, we can effectively solve the instantaneous utility maximization condition presented in Equation (5.2) by setting a budget constraint of total revenue at each specific time. equivalent to However, it is important that this is only one side of the coin – the demand side – of our model for the intertemporal equilibrium conditions in the supply of information within financial markets. Since, as stated earlier, we are only dealing with the information aspect of the representative investor.

Stage II: Linking analyst research output to asset price dynamics

This predominantly cyclical behavior on behalf of analysts in the format of their asset price recommendations arises thanks to the presence of the negative feedback expressed in Equation (5.31). What rationale is there for such obviously pro-cyclical behavior on behalf of the analyst community. Finally, let us conclude our analysis of this particular attachment to our model by confirming that since we have not changed any of the fundamental equations in the information production/consumption framework presented in Section 5.1 – remember, we are talking about the just part of.

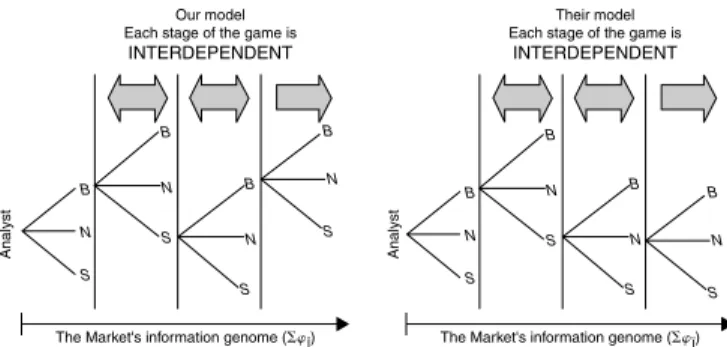

Stage III: Highlighting our preferred evolutionary model of the market – constructing the informational

Conversely, both θ and γ control the degree of "price conservation" behavior on behalf of analysts where the feedback from price activity influences the "buy/sell" recommendation decision made by analysts - in a positive way to reinforce price sweeps, on a negative way for the settlement of price preservation. Finally, by changing the value of ω, we can extend our model of representative asset prices to any asset price across an entire portfolio spectrum simply by the degree of hypothesized association between the representative asset(i) and price of the portfolio asset(a). Furthermore, since we code only research output with our system of comparisons, we have in no way altered the general equilibrium conditions advocated in Section 5.1 in our model of intertemporal information production/consumption – a convenient outcome in the general we feel.

Increasing analyst uncertainty

Furthermore, this perpetual research output flows into a system of equations that influence broader asset prices via its genome-like sequencing effect, as the series of recommendations correlates (via a memetic scalar) with the price of a representative asset. It is this all-encompassing byte to meme, meme to theme, theme to overall market sentiment explanatory power that makes this particular appendage to our model far superior to those listed in Section 5.2. To give the reader an insight into the capabilities of the model, we have given a brief representation of a number of calibrations of equations.

Equilibrium price convergence

In doing so, it is important to note that we have allowed for a greater degree of reverse lookup crowding behavior on behalf of analysts (in other words ς1 > ς0), so there is an increasing tendency for volatility within the system. Rather, it is price action—and in particular, the compensating force of analysts' price-gathering behavior—that forces the system toward an equilibrium price as shown in Figure 5.6.

Jump diffusion

Overwhelming sellers

Associative asset prices

As can be seen, different memetic sequences clearly have different impacts on the performance of the overall market index. We will model the microfoundations that drive such behavior on behalf of the analyst community in more detail in Chapter 6. So we can plot the evolution of key memetic sequences along the information genome of the market (and the efficiency of our investment process). in time).

The Implications of Our Evolutionary Perspective for Distributional Form

Foundations for an evolutionary approach toward distributional form

Thereby, it is via this process that the format of the market's information genome (. ϕÏ) will be determined. Well, it basically provides the generalized solution to the format of the stream of information bytes produced by a diverse ecology of pure strategy following analysts. This is where one of the serendipitous beauties of the game-theoretic analysis we have presented in the previous subsections, the Ewens distribution, manifests itself.

Analyst/investor strategies and the ecology of the market

Quite simply, if the market has assigned a "dominant player" title to a particular analyst, it implies that a particularly powerful emerging theme is already in effect.19 As this theme grows in strength – in fact, as the information spreads within the wider analyst community – there will (by definition) be more converts to the specific pure strategy grouping. Yet, to the extent that the market will mimic these analyst's moves, there will still be a dominance of analysts in a single pure strategy grouping. Following Equation (6.15) and assuming a direct relationship between the presence of externality potential (x), the strategy transition factor (Œ) and subsequently Œ, we can therefore identify direct causality between the actual production of the seminal information grab which extremely high externality potential (and in turn anointing our "dominant player" within the market), and the simultaneous re-defeat by the analyst community in a specific pure strategy after grouping.