International Journal of Economics Development Research, Volume 5(1), 2024

pp. 312-336

Socioeconomic Development Sustainability Analysis: A Review of Corporate CSR and ESG in Indonesia

Ahmad Thoriq Alfan1, Nurlaila Harahap2, Muhammad ikhsan Harahap3

Abstract:

This research elaborates the influence of ESG and CSR on socio-economic development in Indonesia. With a sample of 11 companies and crosschecking statements according to GRI g4.

This research aims to provide awareness to each company about the impacts it will face in a sustainable and advanced social economy. The analytical method used is multiple regression analysis using the CEM (Common Effect Models) model. The results of the research show that the calculated F value is 454.2893 > F table which is 3.327654 and the sig value is 0.00000

< 0.05, so this means that H0 is rejected and Ha is accepted, so this means that the CSR variable and ESG have a very significant effect on socio-economic development, so ESG and CSR disclosures have a significant effect on Socio-Economic Development in Indonesia.

Keywords: CSR, ESG, Economic

Submitted : 25 December 2023, Accepted : 10 January 2024, Published : 17 January 2024

1. Introduction

Disclosure of Environmental, Social, and Governance (ESG) information is a component of corporate CSR disclosure that focuses on organizational performance in the environmental, social, and governance fields (Triyani et al., 2020; Rajesh et al., 2022). Business operations carried out by the company will have an impact on the company's environment (Triyani & Setyahuni, 2020). Disclosure of environmental, social, and governance (ESG) information is one of the various parts that are used as indicators in disclosing the social responsibility (CSR) provided by the company, which focuses on the performance of a company in the social, environmental and governance fields. In social environmental responsibility or also the way the company manages (ESG) is an important component that has an impact on the financial success of a company (Husada & Handayani, 2021).

Based on the analysis, the presence of corporations can actually cause social costs as well as social benefits. Social benefits refer to the beneficial impacts or advantages

1 Faculty of Economics, Universitas Muhammadiyah Cirebon, Indonesia.

2 Faculty of Economics, Universitas Muhammadiyah Cirebon, Indonesia.

3 Faculty of Economics, Universitas Muhammadiyah Cirebon, Indonesia.

Ahmad Thoriq Alfan, Nurlaila Harahap, Muhammad ikhsan Harahap

313

that the presence of a corporation has on society. Corporate social benefits can be achieved through several tangible and intangible actions. Social benefits are realized as a form of corporate social responsibility (CSR) towards the environment or recognized by stakeholders. This makes it clear that the company is responsible to a wider constitution than just to the surrounding community in addition to the company's own shareholders (Nurlaila, 2021).

The realization of a company's social responsibility towards the environment can be done in various ways, such as investing in environmentally friendly industries, waste treatment, and increasing social costs with the aim of maintaining a balance between the existence of human resources, companies and the social environment in which the company operates (Salote et al., 2022). The industry that stands will never be far from where the community lives, because it is the needs of the community that continue to be met by building new industries in an area. Economically, companies are oriented to make a profit, while from a social aspect the company must contribute directly to the community, namely improving the quality of life of the community and its environment. This clearly shows that more and more business actors are aware of the importance of the company's role in preserving social and environmental elements, in order to continue to gain the trust of the community (Husada & Handayani, 2021).

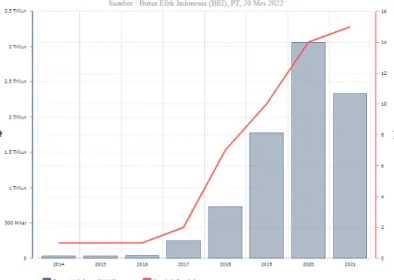

Figure 1. Fund Value and Number of ESG Mutual Funds in Indonesia Source: Nearadata.co.id (2023)

Investments that embrace Environmental, Social, and Governance (ESG) principles are becoming increasingly popular in Indonesia. This trend is expected to continue to grow. When the Indonesia Stock Exchange (IDX) first introduced the concept of environmental, social, and governance (ESG) mutual funds in 2014, there was only one ESG mutual fund product available, and the value of assets under management (AUM) was 38 billion Indonesian Dirhams. Subsequently, as shown in the graph, both the quantity of products and the value of assets under management experienced periods of significant growth in the following years. This indicates that the level of

Ahmad Thoriq Alfan, Nurlaila Harahap, Muhammad ikhsan Harahap

314

investment given the impact of ESG is significant. This means that investors' awareness of the importance of ESG in implementing a sustainable economy is enthusiastic, as ESG disclosures provide a comprehensive picture of a company's efforts in mitigating adverse environmental impacts, managing its interactions with the environment, and implementing effective governance principles to promote a sustainable economy (Elili, 2022).

Based on research conducted (Darwanti et al, 2021), Indonesia's economic growth from 2014 to 2019 was relatively low due to inefficient investment management. This is due to the low quality of human resources. Based on news from Indopremier.com, the Incremental Capital Output Ratio (ICOR) level in Indonesia continued to increase between 2016 and 2018. The ICOR value is a reliable indication of investment efficiency. The optimal ICOR value is in the range of 3-4 as stated by Imelda in 2017.

In Indonesia, the ICOR (Incremental Capital Output Ratio) value was at 6.3 throughout the 2016-2018 period. From 2018 to 2020, it ranged from 6.3% to 15.09%.

In the 2020-2022 period, the ICOR value ranged from 6.88% to 6.2%.

The larger the ICOR number, the more inefficient the investment is. This is because ICOR is already taken into account. The quality of a business's financial statements can provide a picture of the company's success, which can be evaluated by printing the company's earnings and the company's stock performance. Reducing the problem of information asymmetry can be done through the use of high-quality financial reporting (CNBC, 2023). In addition, paying attention to the quality of the financial statements produced will strengthen the ability of shareholders to supervise management, thus having an impact on reducing problems arising from information asymmetry. Disclosures on social, environmental and corporate governance or ESG, included in non-financial reports issued by companies, also play an important role in relation to investment efficiency.

Another part of the problem with CSR in Indonesia is that in its implementation, there are still many companies that tend to be reluctant to run CSR programs. This is because many companies consider CSR as an extra expense that is not profitable in the short term. CSR also requires companies to allocate their resources in the implementation and management of CSR programs. On the other hand, there are also companies that do not understand CSR programs and therefore do not implement them. This attitude tends to occur in traditional companies that have not been able to adjust to environmental and community accountability.

To maximize economic profits, businesses only prioritize the interests of the corporation itself, without regard to the environment in which they operate. When compared to Thai corporations, recent studies show that Indonesian businesses have a lower quality of corporate social responsibility (CSR). This information is provided by the ASEAN CSR Network. Research conducted by the Centre for Governance, Institutions and Organizations at the Business School of the National University of Singapore (NUS) reveals that the poor quality of implementation of this agenda may be due to limited corporate awareness of corporate social responsibility (CSR) activities. One hundred businesses from four different countries - Indonesia, Malaysia,

Ahmad Thoriq Alfan, Nurlaila Harahap, Muhammad ikhsan Harahap

315

Singapore and Thailand - were the subject of the research study. According to Lawrance Loh, Director of Corporate Governance and Information Officer at the National University of Singapore Business School, the four countries selected show a fairly high level of corporate social responsibility reporting. It should be noted, however, that this does not necessarily indicate a high standard of quality in their actual activities. Many companies in Indonesia, Malaysia, Singapore and Thailand prioritize the importance of CSR reporting (ASEAN CSR Network, 2023).

Based on the study's findings, Thailand had the best level of corporate social responsibility (CSR) implementation, scoring 56.8 out of a possible 100, while Singapore scored 48.8. It should be noted that Indonesia and Malaysia scored 48.4 and 47.7 respectively. Many indicators from the Global Reporting Initiative (GRI) framework were used to determine the quality evaluation criteria. These indicators are considered. Corporate governance, economics, environment, and social issues are some of the aspects that come into play. The findings of this study lead Loh to conclude that the government and other industry stakeholders have their own roles to play in ensuring CSR reporting is implemented. This, he continues, is often considered the most important factor in corporate governance. At the Conference on Corporate Governance and Responsibility: Theory Meets Practice coordinated by the National University of Singapore (NUS) and the ASEAN CSR Network (ACN), the research findings were presented and published. The aim of the conference was to examine the many stakeholders involved in sustainable development (ASEAN CSR Network, 2023).

As a result of a number of previous studies, the authors developed an interest in investigating the impact of Environmental, Social, and Governance (ESG) and Corporate Social Responsibility (CSR) disclosures made by businesses. In general, most of the studies that have been conducted in the past have only analyzed the impact of financial reporting quality on investment efficiency. Meanwhile, the impact of ESG and CSR disclosures on the effectiveness of Social Economic Development (SED) is still rare. This study aims to examine the effect of disclosing CSR and ESG on socio- economic sustainability, to see whether companies prioritize ESG and CSR disclosure to improve the sustainability of socio-economic development or just for the all-too- common annual reporting.

2. Theoretical Background Corporate Social Responsibility

Corporate social responsibility or often referred to as Corporate Social Responsibility (CSR) is increasingly popular among business people in the world, including in Indonesia. Companies in Indonesia that implement the concept of CSR mean that they have contributed to the surrounding environment, both to society and nature around the company's environment in various forms of activities and businesses that are disclosed in a systematic report, namely the CSR index (Haniffa, 2022).

Ahmad Thoriq Alfan, Nurlaila Harahap, Muhammad ikhsan Harahap

316

Corporate Social Responsibility (CSR) is a concept according to Totok Mardikanto, where businesses voluntarily incorporate social and environmental issues into their operations and relationships with stakeholders. This ultimately results in the achievement of sustainable commercial success. According to Euis Rosidah, the definition of Corporate Social Responsibility (CSR) is based on the idea that organizations, especially companies, have various responsibilities towards all their stakeholders. These stakeholders include customers, workers, shareholders, communities, and the environment. all areas of the company's activities, including those related to the environment, economy, and society (Kusumawati et al, 2022).

However, the concept of reporting with this common CSR index still has shortcomings and limitations. Corporate social responsibility is like a social concept to balance the 3Ps (profit, planet, people). These three components are currently often used as the basis for planning, implementing and evaluating corporate social responsibility programs (Haniffa, 2022).

According to (Zumarah & Wahyuni, 2019) Social Responsibility (CSR) is a company's commitment to contribute to sustainable economic development and community welfare, taking into account corporate social responsibility and emphasizing the balance between economic and social aspects. According to Bukhari Alma and Doni June Priansa in his book "Management of Islamic Banks", CSR, or corporate social responsibility, refers to the promise made by the business world to consistently behave ethically, operate legally, and contribute to economic improvement. In addition, CSR aims to improve the quality of life of workers and their families, improve the quality of local communication and the wider community (Zumarah & Wahyuni, 2019).

In a broad sense, Corporate Social Responsibility (CSR) is a type of corporate social obligation towards all parties, both direct and indirect, that are affected by business operations. This is achieved by giving greater attention to these parties. CSR Responsibility program is an investment made in the long term and has the potential to provide benefits to reduce various risks, one of which is social risk. Not only that, this program also aims to improve the organization's reputation in the eyes of the wider community. Empowering or improving society is one method of realizing the idea of corporate social responsibility. As a result, corporate social responsibility is no longer seen as a tool to pursue and generate profits; on the other hand, this investment can also be utilized by the business world as an investment in order to encourage sustainable growth and development (Rohmawan et al., 2021).

Companies have a responsibility to the social environment in which they operate. This is the basic concept of corporate social responsibility (CSR). The implementation is in accordance with the company's capabilities. CSR will be very beneficial and have a positive impact on society. However, this will depend on the orientation and capacity of other institutions and organizations. The triple bottom line is the elementary dimension of CSR (people, profit, planet), in other words, CSR activities will always be related to and within one or more of these dimensions. In doing CSR, companies have various motives (Haniffa, 2022), In CSR disclosure, the formula below can be used:

Ahmad Thoriq Alfan, Nurlaila Harahap, Muhammad ikhsan Harahap

317

CSRj=

Description:

CSRj = Corporate Social Responsibility of company j.

Σ Xij = Number of items disclosed by company j.

N = Total number of items.

Environment, Social, Governance (ESG)

Environmental, social and governance are the three components that make up ESG, and they can be stated in general terms. The governance element relates to the way business is conducted, the environmental aspect includes the company's relationship with the environment directly, social factors relate to the company's social influence on society, and there are also environmental factors. ESG is a concept that emphasizes investment and business development for economic sustainability (Kim & Li, 2021).

First, Environment is in the context of corporate responsibility for the environment, the term environment refers to the evaluation of actions taken by the company in order to preserve and improve environmental sustainability. The company's performance in terms of building a favorable environment is referred to as the environment. The company's concern for the world can be realized in several forms, one of which is good environmental performance. In the assessment carried out in measuring environmental performance in Indonesia is the Ministry of Environment which developed the Company Performance Rating Assessment Program in Environmental Management (PROPER). Regulation of the Minister of Environment Number 6 of 2013 defines PROPER as an assessment program for those responsible for businesses or activities in controlling pollution or environmental damage, as well as hazardous and toxic waste treatment. In relation to a company's environmental performance, there are levels ranging from the best to the worst, and evaluations made using color symbols are easier to understand (Lydenberg, 2013).

Companies cannot provide information to management and investors regarding reputation, quality, brand capital, safety, corporate culture, strategy, and how to identify assets through the use of financial statements. Environmental, social and governance (ESG) measures cover all additional aspects of a company's performance that are not reflected in financial reporting. This is due to the fact that it is impossible for companies to include information regarding these features in their financial statements. According to Kim and Li (2021), there are other things that have greater significance in the knowledge-based global economy. In order for ESG indicators to assess a company's management capabilities while limiting risks, they need to collect more non-financial data in the sections that talk about social, environmental and how the company operates (Galbreath, 2013).

Business standards in investment practices that incorporate and implement corporate policies in a way that is compatible with environmental, social and governance principles. Environmental standards relating to energy consumption, waste, pollution, conservation of natural resources, and treatment of the company's flora and fauna are topics covered in this section. The social criteria explore the relationship between the business and external parties such as communities, suppliers, community

Ahmad Thoriq Alfan, Nurlaila Harahap, Muhammad ikhsan Harahap

318

organizations, buyers, and other legal entities that have a relationship with the company. This includes communities, suppliers, and community organizations.

Meanwhile, governance criteria are used to assess the superior and sustainable management flow in the organization (Bassen & Kovacs, 2008).

Second, Social This term which says that humans are social creatures also applies to a company. This opinion arises because there is a direct relationship in a prosperous life for society so that there is balance, harmony and harmony, especially in the environment. Businesses driven by a sense of mission are components of society and the wider environment, and they have an impact on each other (Imsar et al, 2023). For this reason, it is necessary to have a social contract based on an agreement that protects each other's interests (Ardianto & Machfudz, 2011). ECG emphasizes social justice in its reporting in addition to environmental reporting, minority interests and reflects broader social expectations with respect to the role of society in the economy or business activities of the company. Corporate social responsibility disclosure is expressed in the Corporate Social Responsibility Disclosure Index (CSRDI) (Aryonanto & Dewayanto, 2022).

The third concept is governance, which is often interpreted as regulation. Corporate governance is the term used to refer to governance in the context of GCG. Corporate governance is defined as planned procedures and systematics that can be used in building a good and advanced business by looking at what responsibilities they have done to the communities affected by the industry. This definition comes from the Finance Committee on Corporate Governance (GCCG) which is part of the Corporate Governance Institute in Malaysia. A number of different parties in management have provided their own interpretations of management, coaching, management, administration, leadership and other related concepts (Usman et al, 2020). Both factors that originate from within the company (and are always necessary within the company) and aspects that exist outside the organization are included in the elements of corporate governance, specifically Corporate Governance. Together, these elements form the elements of corporate governance (and are always necessary outside the company), which are able to guarantee the functioning of Good Corporate Governance (Na et al, 2023).

The concept of governance takes from the term government. Government is a term used for organizations or institutions that exercise government power in a country. In addition, the term governance comes from the word govern which means taking a greater role. Governance includes all the procedures, rules and institutions that enable the management and control of the collective problems faced by a society. In this sense, governance includes all institutions and components of society, both those related to the government and those not related to the government (Usman et al, 2020).

The fact that governance is a highly dynamic form of governance is indicated by some of the perspectives presented above. In other words, governance creates opportunities for the involvement or participation of different sectors of government in activities. In terms of governance, the government is not the only or most influential player. In addition, this view argues that there has been a decline in the power that governments have with respect to matters of public concern (Nurlaila, 2021).

Ahmad Thoriq Alfan, Nurlaila Harahap, Muhammad ikhsan Harahap

319

In recent years, ESG disclosure has emerged as a very important component in looking at corporate social responsibility and economic sustainability. A number of global organizations, such as the Global Reporting Initiative and the United Nations Global Compact, emerged due to the growing need for more systematic environmental, social and governance (ESG) practices. The following year, in 2006, these two groups came together to form a program they called the Principles for Responsible Investment (PRI). The aim of these guidelines was to provide investors with a clear answer as to where environmental, social and governance (ESG) issues could be incorporated into investment research and where advice on a set of standard practices could be provided.

The new metric strategy of voluntarily disclosing corporate responsibility, which often includes CSR reporting in stand-alone annual reports, sustainability reporting, and then continues with integrated reporting, is known as social environmental and governance (ESG) disclosure (Lydenberg, 2013). According to Whitelock in (Aryonanto & Dewayanto, 2022) the actions of a business related to the ecology of the surrounding area, the company's internal control system and in direct contact with the social environment are referred to as ESG. This aims to make the company advanced and sustainable and have a good impact on stakeholders such as the community of workers and the company itself and even the country's economy. To determine the ESG index, a formula is used:

ESG:

Socio-Economic Development

In the context of socio-economic development, we can refer to the fourth principle, which states that Social Justice is justice that applies in society in the field of life, both material and spiritual, and that all Indonesians refer to everyone who is an Indonesian citizen, whether residing in the territory of the Unitary State of the Republic of Indonesia or abroad. Therefore, the phrase 'social justice for all Indonesians' means that every Indonesian has the right to be treated fairly in all aspects of life, whether in the legal, political, social, economic and cultural fields (Sulistyo & Irawan, 2022). If the socio-economic system is responsible for increasing poverty and unemployment, as well as the identification and realization of social inequalities, then attention must be paid to filling these gaps (Rosyadi, 2021).

In the context of human groups, the term socioeconomic life refers to the position or status that a person holds within the community. The answer to this question depends on a number of elements, such as the type of economic activity, income, education level, age, type of residence, and classification in various organizations. Therefore, we can conclude that socio-economic status is a reliable predictor of the socio- economic situation in a community. Parents' educational background, age, type of work, income level, environmental conditions, location of residence, ownership of property, and activities carried out in the community are important indicators that are utilized (Siregar and Nasution, 2020). According to Dalyono, the socioeconomic situation is a reflection of the status of society and groups in relation to average education, product ownership, and participation in activities organized by community organizations. On the other hand, the socio-economic situation relates to various

Ahmad Thoriq Alfan, Nurlaila Harahap, Muhammad ikhsan Harahap

320

elements related to social status. The science of economics studies the various ways that individuals or organizations live their daily lives (Huzaimah, 2020).

The term "socioeconomics" refers to various characteristics that relate to the needs of society as a whole. These factors include occupation, education, income, the number of dependents parents have, ownership, and the number of dependents parents care for. Socio-economic conditions, which include socio-economic indicators, indicate the capacity of a society to meet the needs of its members (De Taryu et al., 2022).

Yayuk Yuliati defines socioeconomics as a person's status or position in a community group, which is determined by the type of economic activity, level of education, and amount of income earned. Education, occupation, income, housing conditions, and position are some of the elements that can be used to determine the socio-economic situation. Additional factors include position. There are many areas of life related to socio-economic indicators, things that include the state of population, health, housing, criminal activity, education, socio-cultural norms, and even well-being in the household (De Taryu et al, 2022).

The concept of Social Economy is presented in Sindung Haryanto's book "Economic Sociology", Burns and DeVille provide evidence of its attachment and influence on the economic performance of a country through their findings. He argues that the concept of capitalism can be understood in different ways in different countries and regions. These changes are due to the contextualization of economic processes or social entanglements in economic activities. Economic transactions and pricing processes embedded in the social, political and cultural laws of local communities are, according to Polanyi, the most general economic rules that have existed throughout history (Khoirunnisa, 2020). Economics is the demands of every human being, the needs of every human being, human resources to meet the needs of life, and the reasons for having human resources, all of which are aspects of economics. The application of economics that examines the creation and use of human resources in relation to economic development is known as application-based economics. Some of the socio-economic factors that affect a society include education levels, income levels, wealth ownership, and the nature of work (Khoirunnisa, 2020).

So it can be interpreted that Socio-Economic Development is development that aims to improve the welfare of the community for a sustainable economy, by looking at aspects of income, education, employment, and the environment needed by the community for mutual benefit. This concept introduces social development as a process of planned social change designed to improve people's lives, where development is complementary to the economic development process.

Sustainable Development Goals (SDGs)

SDGs (Sustainable Development Goals) is an effort to face the challenges of the world situation while realizing the welfare of society and the planet through a sustainable development program that contains 17 goals with 169 targets that are enforced from 2016 to 2030. Sustainability is the key to finding solutions to the problems facing the world. SDGs is a sustainable development framework that relates to environmental, social, and economic dimensions. The SDGs replaced the previous program, the

Ahmad Thoriq Alfan, Nurlaila Harahap, Muhammad ikhsan Harahap

321

MDGs, with a validity period of 2000-2015. The presence of SDGs is more precisely to continue and develop the goals of the previous program to be more complex (Pizzi et al, 2020). One of the differences between the two is that the MDGs contain 8 goals while the SDGs are broader in scope, namely having 17 goals.

In the SDGs concept, there is a need for a new development framework that can handle all developments that have occurred since the Millennium Development Goals (MDGs) were implemented in 2015. So the most important thing is how changes have occurred in global conditions starting from 2000 on the issue of depletion of natural resources or natural resources, increasingly important climate change, environmental damage, social protection, as well as development that is more in favor of the poor (Bappenas), and food and energy security. As an indicator, the idea of Sustainable Development Goals (SDGs) is formed by three main pillars, as follows: First, indicators related to human growth, namely health and education. Second, indicators related to the environment (Social Economic Development), including the availability of the things most needed by the environment and the expansion of the economy.

Third, several indicators related to the environment (Environmental Development), such as the quality of the environment and the availability of natural resources. These three pillars form the basis for breaking down the project into seventeen goals to be achieved.

These three pillars form the basis for breaking down the project into seventeen goals to be achieved. There are various goals related to human growth that are included among the 17 goals. These goals include goal three, goal four, and goal eight. In addition to ensuring that people live healthy lives, the third goal aims to improve the well-being of the population which includes people of all ages, the fourth goal is to ensure that everyone has access to better lifelong learning possibilities and ensure equitable and inclusive quality education. On the other hand, the eighth goal is to achieve sustainable and inclusive economic development, provide productive and full employment opportunities, and ensure that everyone has access to good jobs.

In addition to ensuring people live healthy lives, the third goal is to improve the well- being of the population at all ages. The goal of this third goal is to stop the deaths of children, mothers and people under the age of 70 caused by various diseases. One indicator of the Sustainable Development Goals (SDGs) is the expected live birth rate.

If connected to one of the indicators that make up the Human Development Index (HDI). If one of the Sustainable Development Goals (SDGs) indicators, namely the newborn mortality rate, is reduced to achieve the goal, then life expectancy at birth will increase indirectly. The fourth goal is to ensure that everyone has access to improved lifelong learning possibilities and to ensure equitable and inclusive quality education. Ensure that all girls and boys have equitable access to early childhood development, care and education to prepare them for primary education. This is the fourth goal they have set for themselves. Achieving this goal is expected to increase the percentage of students who graduate from primary, junior secondary and senior secondary school.

Ahmad Thoriq Alfan, Nurlaila Harahap, Muhammad ikhsan Harahap

322

On the other hand, goal eight is to achieve inclusive and sustainable economic development, provide opportunities for full and productive employment, and ensure that everyone has access to good jobs. Target 8 is part of the eighth goal, which is to increase economic growth per capita in line with national conditions and achieve gross domestic product (GDP) growth rates of at least 7 percent per year in developing countries. An increase in Gross National Product (GNP) per capita is one sign that progress is being made in achieving this goal. Increased gross national income per capita will indirectly lead to increased spending per capita. The Sustainable Development Goals (SDGs) bring continuous improvement to human development goals and targets. It can be concluded that human progress can be achieved by achieving the goals set out in the Sustainable Progress Goals (Siburian, 2021). The goal of sustainable development is to improve the welfare of society and fulfill individual needs and ambitions. As stated by Omer and Nouguchi (2020), the main goal of sustainable development is to achieve equal development between the generations living now and the generations that will live in the future.

ESG and CSR Disclosures On Socioeconomic Development Sustainability Socio-economics is an individual placed in a certain position in society based on his socio-economic status, which is a socially controlled position. This status is accompanied by a series of privileges and duties that must be fulfilled by the person who has it to maintain their position. According to M. Sastropradja, socio-economics refers to the state or position of a person in the society that surrounds him.

Furthermore, it is a position that is socially controlled and places a person in a certain position in the social community, as stated by Manaso Malo. In other words, a position that places a person in a certain position in social society (Yatimah et al, 2020).

Granoveter asserts in his book that the economy is closely linked to the social framework in which it exists. The concept of economic embeddedness is not limited to a network of interpersonal ties; rather, it can also be found in a sphere of supra- individual and interpersonal social relations. Given the fact that one's economic activity cannot be separated from the social context (Yuslem et al., 2021). Burns and DeVille provide evidence of embeddedness and its influence on a country's economic performance through their findings. They argue that the concept of capitalism can be understood in different ways in different countries and regions. These changes are due to the contextualization of economic processes or social embeddedness in economic activities. Economic transactions and pricing processes embedded in the social, political and cultural laws of local communities are, according to Polanyi, the most general economic rules that have existed throughout history (Angela, 2022).

The socio-economic state of a society is determined by several factors, including the level of education, income level, wealth ownership, and the nature of labor. The demands of every human being, human resources to fulfill the needs of life, and the reasons for having human resources are all aspects of economics. The application of economics that examines the creation and use of human resources in relation to economic development is known as application-based economics. When economic life changes, economic change is a natural consequence. The way a person carries out economic activities will vary from one person to another. Some of these changes

Ahmad Thoriq Alfan, Nurlaila Harahap, Muhammad ikhsan Harahap

323

include the variety of types of labor and income offered, which in turn leads to disparities in the economic changes that occur. In the context of the economy, for example, having a better career and earning more money will ultimately lead to a better life. Therefore, changes in society caused by aspects of the economy undergoing transformation are called socio-economic development (Yusniah, et al, 2022).

CSR is the concept of doing business that is honest and reliable will form stronger relationships among its customers and society as a whole, because they have built strong anticipation of their brand (Sarfraz et al, 2022). Companies will provide social responsibility is beneficial in providing solutions to the community for the industry they build around the industry (He & Haris, 2020). Social development initiatives implemented by the current government are expected to be able to overcome various social problems, including but not limited to poverty, neglect, disability, immorality, remoteness, and several other problems. However, in reality, the development carried out still faces challenges in the form of limited budget funds owned by the state, as well as ineffective implementation of social security assistance and services. As a result, the government is said to be unable to reach all levels of society, especially those living in remote areas. For this reason, the role of companies as a supporting role or what is often referred to as Corporate Social Responsibility (CSR) is needed in order to realize an empowered society (Octaviani et al, 2022).

ESG generally means a broad set of environmental and social and corporate governance considerations that may impact a company's ability to execute its business strategy and create value over the long term. While ESG factors are sometimes called non-financial, the way a company manages them must have measurable financial consequences. According to nasdaq (2019), indicators included in ESG performance range from the climate affected, the company's management, and the social actions provided to affected communities. ESG investments exist within a broader spectrum of investments based on financial and social returns. On one end of the spectrum, purely financial investments seek to maximize shareholder and debt holder value through financial returns based on absolute or risk-adjusted measures of financial value.

At the very least it assumes the efficiency of capital markets will effectively allocate resources to parts of the economy that maximize benefits, and contribute more broadly to economic development. Pure social investment, such as philanthropy, seeks only social returns, as investors expect profits from confirming evidence of benefits to segments or whole societies, particularly with regard to environmental or social benefits, including those relating to human and labor rights, gender equality. Social impact investing seeks a mix of social and financial returns but prioritizing social or financial returns depends on the extent to which investors are willing to compromise one for the other in line with their overall objectives (Bofo & Patalano, 2020). The term Corporate Social Responsibility (CSR) is defined by Irham Fahmi as a management obligation to make decisions and take actions that contribute to the realization of community welfare. Apart from being a form of obligation to the government in the form of timely and honest tax payments, this obligation is also a

Ahmad Thoriq Alfan, Nurlaila Harahap, Muhammad ikhsan Harahap

324

form of attention from the business world to the surrounding community (Zumarah &

Wahyuni, 2019).

Society's demand for higher ethical standards in economic growth through finance and business These practices have also contributed to the growing demand for ESG tools that can help measure and benchmark these practices. A key set of standards for ESG, and in particular the Social pillar, is the UN Global Compact, which highlights ten principles related to ethical standards related to human rights, labor, anti- corruption and the environment. In the OECD test responsible business can help businesses contribute to economic, environmental and social progress, particularly by minimizing adverse environmental impacts on operations, supply chains and other business relationships. This includes human rights, labor and industrial relations, the environment, combating bribery, and consumer interests (Bofo & Patalano, 2020).

3. Methodology

This study uses qualitative methods, the data analysis technique used is time series by taking multiple linear regression analysis methods, the data taken comes from several indexes. Refinitiv is an index that can be used to measure the ESG performance of a company. This index if detailed, environmental performance is divided into resource use, emissions, innovation, social responsibility performance consists of labor, human rights, community, and product responsibility, and for corporate governance is divided into management, shareholders, and responsibility (CSR) strategy. The Global Reporting Initiative (GRI) disclosure in this study uses the Global Reporting Initiative (GRI) G4 index. This study uses the Eviews 12 analysis tool to help process data and the results that will be obtained in the analysis.

The data used is data taken from the Annual Report of 11 companies in Indonesia with criteria that have an Annual Report, carry out CSR and ESG and are published in the Annual Report, the annual report is issued by the company every year and varies, by processing the data into a number with the Cross Check method by giving a value of 0 if the company does not do and 1 if the company does by looking at the GRI G4 index disclosure. Researchers use data from 2020-2022 by taking a sample of several companies in Indonesia after which the data will be processed using the Eviews 12 tool. The annual report taken from 11 companies, namely PT Erajaya Swasembada Tbk (ERAA), PT Bumi Serpong Damai Tbk (BSDE), PT Surya Citra Media Tbk (SCMA), PT Elang Mahkota Teknologi Tbk (EMTK), PT Media Nusantara Citra Tbk (MNCN), PT Chandra Asri Petrochemical Tbk (TPIA), PT Unilever Indonesia Tbk (UNVR), PT Global Mediacom Tbk (BMTR), PT Bank Rakyat Indonesia (Persero) Tbk (BBRI), PT Ace Hardware Indonesia Tbk (ACES), PT Bumi Resources Tbk (BUMI).

In this study using multiple linear regression equations, namely:

Y = a + b1 X1 + b2 X2 + e

In this study, several methods were used to determine the model to be taken from the three tests to be carried out, in the chow test getting a probability result of 0.0300 this

Ahmad Thoriq Alfan, Nurlaila Harahap, Muhammad ikhsan Harahap

325

determines that P < 0.05, according to the determination if the P value> 0.05 then the one used is the CEM model and if P < 0.05 then the one used is the FEM model, then it is decided that the model is FEM, in the second test a hausman test is carried out to compare the FEM and REM models, then getting a probability result of 0.3847 this determines that the model is FEM, then the model is decided. 0.05 then what is used is the FEM Model, then it is decided that the Model is FEM, in the second test a hausman test was carried out to compare the FEM and REM Models, then getting a probability result of 0.3847 this determines that P> 0.05 then it was decided to use the REM model, third I did the Laggrange Multiplier test to compare the CEM and REM models to get a probability result of 0.5061 this states that the P value> 0.05 then the CEM model (Common Effect Models) will be used.

4. Empirical Findings/Result

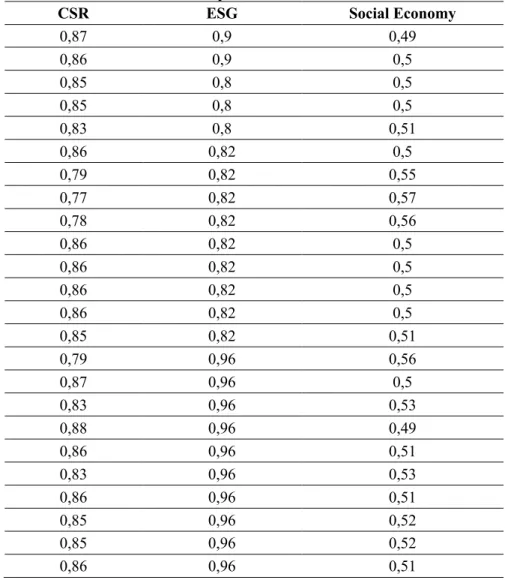

Table 1. Management Data of ESG and CSR Disclosure on Socio-Economic Development 2020-2022

CSR ESG Social Economy

0,87 0,9 0,49

0,86 0,9 0,5

0,85 0,8 0,5

0,85 0,8 0,5

0,83 0,8 0,51

0,86 0,82 0,5

0,79 0,82 0,55

0,77 0,82 0,57

0,78 0,82 0,56

0,86 0,82 0,5

0,86 0,82 0,5

0,86 0,82 0,5

0,86 0,82 0,5

0,85 0,82 0,51

0,79 0,96 0,56

0,87 0,96 0,5

0,83 0,96 0,53

0,88 0,96 0,49

0,86 0,96 0,51

0,83 0,96 0,53

0,86 0,96 0,51

0,85 0,96 0,52

0,85 0,96 0,52

0,86 0,96 0,51

Ahmad Thoriq Alfan, Nurlaila Harahap, Muhammad ikhsan Harahap

326

CSR ESG Social Economy

0,86 0,96 0,51

0,88 0,96 0,49

0,86 0,96 0,52

0,85 0,96 0,52

0,88 0,96 0,49

0,83 0,96 0,53

0,86 0,96 0,51

0,88 0,96 0,49

0,83 0,96 0,53

2. Classical Assumption Test

Based on the Chow Test, Hausman Test and Lagrange Multiplier Test, this study determines that the model that researchers will use is the CEM model (Common Effect Models), therefore the classic assumption tests carried out are multicollinearity and heteroscedasticity (Napitupulu et al, 2021).

Table 2. Lagrange Multiplier Test

The table above is LM or Lagrange Multiplier testing which compares what model is better used in choosing the Commen Effect Model (CEM) or Random Effect Models (REM). Then the table above shows a P value of 0.5061> 0.05, so the Commen Effect Model (CEM) was chosen. The following is the meaning of the variables to be tested:

X1 : CSR X2 : ESG

Y : Socioeconomic Development

Lagrange Multiplier Tests for Random Effects Null hypotheses: No effects

Alternative hypotheses: Two-sided (Breusch-Pagan) and one-sided (all others) alternatives

Test Hypothesis

Cross-section Time Both

Breusch-Pagan 0.442021 0.508143 0.950163 (0.5061) (0.4759) (0.3297)

Honda 0.664846 -0.712841 -0.033937

(0.2531) (0.7620) (0.5135)

King-Wu 0.664846 -0.712841 -0.379310

(0.2531) (0.7620) (0.6478) Standardized Honda 1.141618 -0.409438 -2.930677

(0.1268) (0.6589) (0.9983) Standardized King-Wu 1.141618 -0.409438 -2.716689

(0.1268) (0.6589) (0.9967)

Gourieroux, et al. -- -- 0.442021

(0.4535)

Ahmad Thoriq Alfan, Nurlaila Harahap, Muhammad ikhsan Harahap

327

Autocorrelation Test

Table 3. Durbin Watson Autocorrelation Test

In the table above using the durbin watson autocorrelation test which shows a value of 1.823789, then according to the provisions of the durbin watson test if DU < DW

< 4-DU then 1.6044 < 1.823789 < 2.3956, it can be concluded that there are no symptoms of auto correlation or pass the autocorrelation test because the DW Statistic value is between the DU value and the 4-DU value. This means that there is no significant dependence over time.

Multicollinearity Test

Table 4. Multicollinearity Test

So based on the above test, the correlation coefficient of X1 and X2 is 0.295292 <0.85, it can be concluded that X1 and X2 are free from multicollinearity or pass the multicollinearity test (Napitupulu et al, 2021).

Heteroscedasticity Test

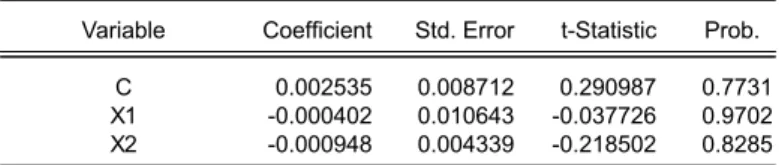

Table 5. Heteroscedasticity Test

In the table above, it can be seen that the probability value on the variables X1 and X2

, P> 0.05, so in accordance with the test decision in the heteroscedasticity test, there is no heteroscedasticity. The heteroscedasticity test aims to test whether in the regression model there is an inequality of variance from the residuals of one observation to another (Ghozali, 2018: 120).

R-squared 0.968037 Mean dependent var 0.513939 Adjusted R-squared 0.965906 S.D. dependent var 0.021351 S.E. of regression 0.003942 Akaike info criterion -8.147546 Sum squared resid 0.000466 Schwarz criterion -8.011500 Log likelihood 137.4345 Hannan-Quinn criter. -8.101770 F-statistic 454.2893 Durbin-Watson stat 1.823789 Prob(F-statistic) 0.000000

X1 X2

X1 1.000000 0.295292 X2 0.295292 1.000000

Total panel (balanced) observations: 33

Variable Coefficient Std. Error t-Statistic Prob.

C 0.002535 0.008712 0.290987 0.7731

X1 -0.000402 0.010643 -0.037726 0.9702

X2 -0.000948 0.004339 -0.218502 0.8285

Ahmad Thoriq Alfan, Nurlaila Harahap, Muhammad ikhsan Harahap

328

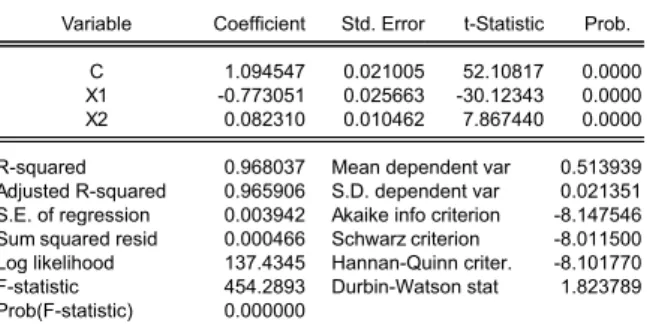

Panel Data Regression Equation

Table 6. Panel Data Regression Equation

In this research test, the results of the panel data representation are as follows:

Y = 1.09454662451 - 0.773051429658X1 + 0.0823098378387X2

The test results above can explain several related things as follows:

1. The coefficient value of Y is 1.094, which defines that without the CSR (X1 ) and ESG (X2 ) variables, the socio-economic development variable (Y) will increase by 1.094%.

2. The value of the beta coefficient of the CSR variable (X1 ) of -0.77 means that if the value of other variables is constant and the variable X1 has decreased by 1%, the Socio-Economic Development Variable will decrease by 0.77%, and vice versa if the value is constant and the CSR variable (X1 ) has increased by 1%, the Socio- Economic Development Variable (Y) will increase by 0.77%.

3. The beta coefficient value of the ESG Variable (X2 ) of 0.082 means that if the value of other variables is constant and the X2 Variable has increased by 1%, the Socio-Economic Development Variable will increase by 0.82%, and vice versa if the value is constant and the ESG variable (X2 ) has decreased by 1%, the Socio- Economic Development Variable (Y) will decrease by 0.82%.

T Test

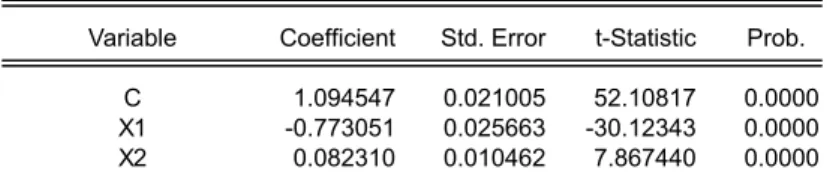

Table 7. Hypothesis Test Results T

In the table above, it can be seen that the hypothesis results of the influence of the independent variable on the dependent variable are as follows:

First Hypothesis CSR (X1)

H01 : CSR variables do not affect the socio-economic development of companies in Indonesia.

Ha1 : CSR variables affect the socio-economic development of companies in Indonesia.

The results of the t test on the CSR variable (X1 ) obtained the t value of -30.12343 <

t table which is 2.039513 and sig value. 0.000 <0.05 then Ha is rejected and H0 is

Dependent Variable: Y Method: Panel Least Squares Date: 09/07/23 Time: 09:10 Sample: 2020 2022 Periods included: 3 Cross-sections included: 11

Total panel (balanced) observations: 33

Variable Coefficient Std. Error t-Statistic Prob.

C 1.094547 0.021005 52.10817 0.0000

X1 -0.773051 0.025663 -30.12343 0.0000

X2 0.082310 0.010462 7.867440 0.0000

R-squared 0.968037 Mean dependent var 0.513939 Adjusted R-squared 0.965906 S.D. dependent var 0.021351 S.E. of regression 0.003942 Akaike info criterion -8.147546 Sum squared resid 0.000466 Schwarz criterion -8.011500 Log likelihood 137.4345 Hannan-Quinn criter. -8.101770 F-statistic 454.2893 Durbin-Watson stat 1.823789 Prob(F-statistic) 0.000000

Dependent Variable: Y Method: Panel Least Squares Date: 09/11/23 Time: 20:32 Sample: 2020 2022 Periods included: 3 Cross-sections included: 11

Total panel (balanced) observations: 33

Variable Coefficient Std. Error t-Statistic Prob.

C 1.094547 0.021005 52.10817 0.0000

X1 -0.773051 0.025663 -30.12343 0.0000

X2 0.082310 0.010462 7.867440 0.0000

Ahmad Thoriq Alfan, Nurlaila Harahap, Muhammad ikhsan Harahap

329

accepted, meaning that the variable CSR (X1 ) does not significantly affect the socio- economic development (Y) of the Company in Indonesia.

Second Hypothesis ESG (X2)

H02 : ESG variables do not affect the socio-economic development of companies in Indonesia.

Ha2 : ESG variables affect the socio-economic development of companies in Indonesia.

In the second hypothesis test, it can be seen that the t test on the ESG variable (X2 ) the t value is 7.86744> than the t table of 2.039513 and the sig value. 0.000 <0.05 then H02 is rejected and Ha2 is accepted, meaning that the ESG variable (X2 ) has a significant effect on the socio-economic development variable (Y) of companies in Indonesia.

F Test

Table 8. F Test

The table above is to prove which one to choose from the hypotheses: Third Hypothesis CSR and ESG

H01 : CSR and ESG variables have no effect on the socio-economic development of companies in Indonesia,

Ha1 : CSR and ESG variables affect the socio-economic development of companies in Indonesia.

In the table above, the calculated F value is 454.2893> F table which is 3.327654 and the sig value is 0.00000 < than 0.05, this means that H0 is rejected and Ha is accepted, this means that CSR and ESG variables simultaneously affect socio-economic development in Indonesia.

Coefficient of Determination Test R2

Table 9. Coefficient Of Determination Test R2

The table above shows that the Adjusted R Square value is 0.965906 or 96.6%, so this value indicates that the independent variables consisting of CSR and ESG are able to explain the Socio-Economic Development variable in Indonesian companies by

R-squared 0.968037

Adjusted R-squared 0.965906 S.E. of regression 0.003942 Sum squared resid 0.000466 Log likelihood 137.4345

F-statistic 454.2893

Prob(F-statistic) 0.000000

R-squared 0.968037

Adjusted R-squared 0.965906 S.E. of regression 0.003942 Sum squared resid 0.000466 Log likelihood 137.4345

F-statistic 454.2893

Prob(F-statistic) 0.000000

Ahmad Thoriq Alfan, Nurlaila Harahap, Muhammad ikhsan Harahap

330

96.6% while the remaining 4.4% is explained by other variables not included in this model.

5. Discussion

The Effect of Corporate Social Responbility (CSR) on Socio-Economic Development in Indonesia

CSR will have a very positive impact in addressing socio-economic development and progress. Other studies have different results with this research, focusing on whether if investment is carried out through CSR reviews, it will have a positive impact on the socio-economy in Indonesia. According to Rohmawan et al. (2021) said that CSR does not have an important role in the company because it is done voluntarily, therefore if investors are not interested in the implementation of good CSR this means that CSR does not provide attractiveness to investors so that it will have an impact on an unsustainable economy. In research (Taufiq & Iqbal, 2021) argues that Community Development (Comdev) is something that must be considered and is needed so that the community is more self-sufficient in economic terms. Community Development is a community development activity that is carried out methodically, planned, and directed with the aim of expanding community access to create better social, economic and quality of life conditions compared to development activities that have been carried out in the past (Iqbal 2021).

So this concludes that the improvement that should be made in CSR investment is to make investors aware of the economic sustainability that they get if they look at CSR and ESG. Corporate Social Responsibility (CSR) can mitigate corporate harm by encouraging socially responsible and environmentally friendly actions (Yadav et al., 2021). CSR plans establish strategies to support socio-economic and environmental sustainability through management and stakeholder engagement (Tiep et al., 2021).

So it is expected that companies can meet the expectations of society by not only implementing CSR programs disclosed in the Company's Annual Report but actually doing so for the sake of progress and socio-economic sustainability in Indonesia.

Corporate social responsibility (CSR) disclosure programs are designed to accelerate the pace of communication between the company and its stakeholders in order to better integrate the company's vision and goals with the organization's activity processes. In addition, corporate social responsibility (CSR) disclosure will help companies become more sustainable by ensuring that companies pay attention to the economic, social, and environmental factors included in CSR disclosure. There is a correlation between the economic component and the ability of businesses to generate, disseminate, and increase economic value, which in turn has an impact on the general economic situation of the society. An example of corporate social responsibility is the social component of CSR that impacts the health and safety of workers and the surrounding community.

In research (Song & Bong, 2022) revealed that CSR authenticity is a multifaceted and multidimensional concept that is researched in various contexts. However, the

Ahmad Thoriq Alfan, Nurlaila Harahap, Muhammad ikhsan Harahap

331

concepts and theories still lack clarity and consistency. Methodologically, qualitative and quantitative methods both contribute to the investigation of CSR authenticity.

However, scale development and validation still need to be improved. As one example, if companies do not implement the GRI G4 statements on emissions, income, welfare and other aspects, it is certain that Indonesia has no hope in economic and socio-economic sustainability. Because Corporate Social Responsibility (CSR) is no longer faced with a task that only relies on one thing, namely the value of the company which is only represented in its financial condition. Because financial conditions cannot guarantee the development of company value in the long term (sustainable), other benefits are not only financial, but also social and environmental.

This is because financial conditions alone cannot guarantee success (Rohmawan et al., 2021).

The Effect of Environtment, Social, Governance (ESG) on Socio-Economic Development in Indonesia

This test shows that Environtment, Social, Governance (ESG) has an effect on Socio- Economics. According to research (Bullay et al 2020; Passas et al., 2022), this shows that shareholders place a higher priority on investing in environmental standards and transparency than on increasing company value. In addition, environmental disclosure is still optional, meaning that it is unclear and still difficult for investors to examine.

This is consistent with the previous test which explains that there is about 4.4%

influence on socioeconomic development. In ESG disclosure, each part must have its advantages, the researcher assumes that this test produces a large R Square value because the test is carried out only for the three components, it can be seen that the independent variables are very influential on the Socio-Economy.

This research shows that Environtment, Social, Governance (ESG) can be a solution to meet socio-economic development in Indonesia, companies should take this picture for the progress of the country, There are many national education problems that we actually face, there are at least nine of them (Irawan & Sulistyo, 2022). The problem of the large number of children who cannot be accommodated in schools, the problem of the large number of students who drop out of school, the problem of horizontal and vertical inequality, the problem of teacher personnel, the problem of outdated curriculum and teaching methods, the problem of funds donated to education, the problem of centralized state examinations, the problem of jamming the inspection and supervision mechanism, and the problem of not meeting the requirements of educational infrastructure and facilities are problems that need to be overcome.

In research (Husada & Handayani, 2021) argues that social practices and disclosure are not the main emphasis for developing proxied business value. Instead, corporations tend to use other instruments such as earnings, liquidity levels, and sales as a reference to increase their company value (Maama, 2020; Coelho et al., 2023).

He also said that good corporate has no influence on the progress of the Company, but can increase socio-economic progress in order to resolve the conditions of economic inequality in Indonesia. This shows that effective corporate governance standards have not been fully applied to the current form. According to Christofi, Christofi, and Sisaye (2012), disclosures made will expose the company's activities and place the

Ahmad Thoriq Alfan, Nurlaila Harahap, Muhammad ikhsan Harahap

332

organization at a higher level of scrutiny. Companies only disclose information that is not related to their finances to demonstrate compliance. This requirement goes against the stakeholder hypothesis, which believes that businesses should share information unrelated to their finances as an ethical business practice.

Therefore, this research is not only seen from the disclosures made in the company's annual report, there should be a review and supervision carried out so that all of that goes well, so that investors can make this as one of the factors they want to invest in companies in Indonesia. The negative effect of this disclosure is that the implementation is increasingly unstable or not done well. Only as a filling that is done to fulfill the annual report that will be exposed and seen as the company's accountability, so that the company can continue continuously.

As stated by Ruan and Liu (2021) in paying attention to ESG disclosed by companies in China, they argue that their research enriches the literature on the impact of ESG activities on firm performance and provides the latest research results on ESG activities in China. In particular, (Grisales et al, 2019) suggest that more attention should be paid to the ESG performance of non-state-owned enterprises and environmentally insensitive enterprises. Based on the theoretical derivation and empirical tests of this article, we predict that as these two types of firms continue to invest in ESG activities, the impact of ESG on firm performance may gradually decrease from negative to positive and may bring a higher investment premium for corporate investors.

The use of ESG in reporting should make a stable and sustainable economy, in research by Pizzi et al. (2020), said that Non-financial reporting is needed for sustainable economic development, so that companies in Indonesia can consider the strategies they will carry out. Filling this gap through the provision of objectives that explicitly relate directly to companies, these objectives require effective corporate contributions from managerial, organizational, and reporting perspectives. However, despite these provisions, the road to full achievement of the SDGs is still a long way off, due to differing levels of knowledge regarding the need to implement more sustainable practices (Pizzi et al, 2020; Tanjung 2021).

6.

ConclusionsBased on the results of the analysis of the level of health at KSP Kopdit Pintu Air in This study concluded that Corporate Social Responsibility (CSR) has a positive effect on socio-economic development in Indonesia. The results show that investment in CSR can have a very positive impact on socio-economic progress in this country.

Environtment, Social, Governance (ESG) also has a significant influence on socio- economic development in Indonesia. Investments in environmental, social, and good governance (ESG) practices are considered more important than simply focusing on maximizing firm value. This indicates that investors tend to see ESG as a factor that influences their decisions. ESG disclosure by companies is still voluntary and difficult to verify by investors. This raises the need to further monitor and supervise the

Ahmad Thoriq Alfan, Nurlaila Harahap, Muhammad ikhsan Harahap

333

implementation of ESG so that it runs well. Therefore, companies need to pay attention to both CSR and ESG to achieve sustainable socio-economic development.

In the Indonesian context, socio-economic development can be a solution to many of the nation's educational and economic problems. There is potential for companies not to fully invest in ESG, which may reduce its positive impact on the company and socio-economic development. The research also cautions that greater attention should be paid to the performance of non-state-owned enterprises and environmentally insensitive companies in the context of ESG. Thus, the main conclusion is that both CSR and ESG have a positive impact on socioeconomic development in Indonesia, and companies need to be more serious in implementing these practices to achieve better ecological and social outcomes in the country.

References:

Angela, E. W. (2022). Pengaruh Usaha Tambang Emas Rakyat Terhadap Kondisi Sosial Ekonomi Penambangan Desa Kenanga Kecamtan Simpang Hulu Kabupaten Ketapang (Doctoral dissertation, IKIP PGRI Pontianak).

Aryonanto, F. A., & Dewayanto, T. (2022). Pengaruh Pengungkapan Environmental, Sosial, and Governance (ESG) dan Kualitas laporan Keuangan pada Efisiensi Investasi. Diponegoro Journal of Accounting, 11(4), Article 4.

https://ejournal3.undip.ac.id/index.php/accounting/article/view/36382.

Coelho, R., Jayantilal, S., & Ferreira, J. J. (2023). The impact of social responsibility on corporate financial performance: A systematic literature review. Corporate Social Responsibility and Environmental Management.

De Taryu, M., Nurhakim, I., & Santi, R. (2022). Analisis Kondisi Sosial Ekonomi Pemulung di Tempat Pembuangan Akhir Desa Sibau Hilir Kecamatan Putussibau Utara Kabupaten Kapuas Hulu. Geo Khatulistiwa: Jurnal Pendidikan Geografi dan Pariwisata, 2(3), 74-82.

Haniffa, R. (2022). Social Responsibility Disclosure: An Islamic Perspective.

Indonesia Management & Reserch, 1(2), 128-146.

Husada, E. V., & Handayani, S. (2021). Pengaruh Pengungkapan ESG Terhadap Kinerja Keuangan (Studi Empiris Pada Perusahaan Sektor Keuangan yang Terdaftar di BEI Periode 2017-2019). Jurnal Bina Akuntansi, 8(2).

https://doi.org/10.52859/jba.v8i2.173

Iqbal, A. (2021). Analisis Peran Corporate Social Responsibility terhadap Aspek Sosial, Ekonomi, dan Lingkungan pada Industri Ritel. JIA (Jurnal Ilmiah Akuntansi), 22-36.

Imsar, I., Nurhayati, N., & Harahap, I. (2023). Analysis Of Digital Economic Interactions, Economic Openness, Islamic Human Development Index (I- HDI) And Investment On Indonesia's GDP Growth. Edukasi Islami: Jurnal Pendidikan Islam, 12(01).

Irawan, A. D., & Sulistyo, A. Q. P. (2022). Pengaruh Pandemi Dalam Menciptakan Ketimpangan Sosial Ekonomi Antara Pejabat Negara Dan Masyarakat. Jurnal Citizenship Virtues, 2(1). https://doi.org/10.37640/jcv.v2i1.1184

Kim, S., & Li, Z. (Frank). (2021). Understanding the Impact of ESG Practices in Corporate Finance. Sustainability, 13(7). https://doi.org/10.3390/su13073746