This thematic paper demonstrated how to value the share price of S.KHONKAEN Foods Public Company (SORKON) which applied the concept of the discounted cash flow valuation model. I used the discounted cash flow valuation method to express the valuation of the company's share price.

LIST OF ABBREVIATIONS

VALUATION

Highlights

- The Market Leader of Thai Foods Industry

- Product Diversifications with Sustainable Growth

- Strong and Large Distribution Channels

Business Description

- Visions

- Missions

- Business Strategies

- Nature of Business Products

The company has the ambition to penetrate the AEC market initially by appointing an authorized dealer in each country to distribute the company's products. The frozen food factory served as the central kitchen for QSR, "Zapp Express" and "Yunnan".

Macro-economic Analysis

- Impact from Asian Economy Community (AEC) markets

- Evaluation of Raw Material and Supplies

Ensuring that there will be enough supply to serve in production in the future is a concern of this type of industry. This question is related to fluctuations in price because it will be the key determinant of costs.

Industry Analysis

- Traditional Thai Foods

- Processed Seafood (Fish Balls)

- Frozen Foods

The company is prepared for a dramatic competition in the modern trade which is considered to be the direct issue of the sales numbers, despite the fact that the company has the huge advantage in terms of cost by owning as the market leader of Traditional Foods in the country and becomes decisive of prices in this industry. The company owns approximately 80 percent of this stock market in modern trade, while the other 20 percent is divided among various major players. One factor in the current situation is that lifestyles have shifted towards more ready-to-eat meals and instant noodles.

Current customer behavior has shifted more towards convenience food products and is reflected in a gradual rise in demand over the past year. As we can see that consumer behavior has changed, people tend to go more for convenient stores, departments and supermarkets. Most of the SORKON Company's products are distributed via modern trade and convenient store channels.

If this channel rejects his products, it will have a major negative impact on sales. However, the company has established good relationships with distributors and has also expanded its channel through the QSR line to generate more revenue and have direct customer contact.

Competition Positioning

- Competition Analysis

- Major Competitors

Within the food industry in Thailand, there are many players in the market and under our scrutiny; we selected TU, Thai Union Group Public Company Limited and SSF, Surapon Foods Public Company Limited and CPF, Charoen Pokphand Foods PCL as our competitors. We chose to compare S.Konkaen with Surapon Foods PCL (SSF) as a direct competitor because both of their main revenues come from similar type of distribution channels, product types and target customers. We chose to compare S.Konkae with SSF food, Surapon, because both of their main revenues come from similar type of distribution channels, product types and target customers.

Currently, the company produces and distributes various frozen foods, including ready-to-cook and ready-to-eat products. The company offers products such as Dimsum, buns, appetizers, raw materials, pastry, etc. In Thailand, the company can be recognized through all CP products, CP fresh marts, BKP, JerHigh, Chesters Grill, 5 star chickens, Meji, and etc.

The company has had many acquisitions and partnerships with international companies that help TU to advance in international markets in the frozen seafood business. It is known in Thailand and many other countries around the world as the top player in the canned tuna industry.

Investment Summary

- Efficiency Improvement

- Capacity Expansion of MFP

- QSR Branch Expansions

- Launching new Products

- Traditional Trade Penetration

- Targeting Chinese Tourists

- Invention of OEM policy for RTE and RTH

- Qualify as an exporter for EU and Middle East markets

In April, 2014, the company launched a new product called "Moochi" in which the target for young generation segment. Entrée” on shelves in 7-eleven in which the company was able to gain more sales across the country. About 80% of revenue comes from modern trade channel; however, the company still believes that there is more room to grow in traditional market such as wet market.

Traditional Thai dishes and meat snack staples are quite popular among Chinese tourists; the well-known products often come from meat snacks such as Entrée pork and chicken. Because Chinese tourists make a great contribution and the number of Chinese tourists visiting Thailand every year is very high and continues to rise. To counter the risk of raw material price fluctuations, which can affect lower profit margin, the new OEM policy has emerged.

By doing so, the company has moved its production for Ready to Eat and Ready to Heat to Quick Service Restaurant instead called "Zaap Express" where it has a higher profit margin. One of the strategic plans is to penetrate new markets which are the Middle East and European countries and the United States by complying with the standard of Halal as prescribed by The Central Islamic Committee of Thailand, which is in accordance with the standard of being qualified exporters.

Valuation

- Discounted Cash Flow Model

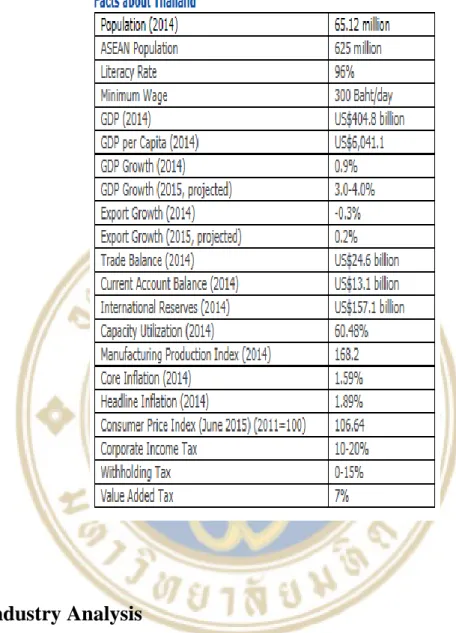

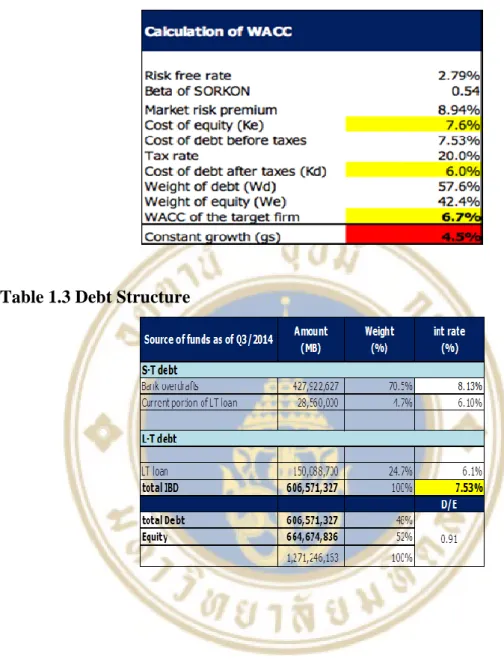

Thailand's GDP was projected to grow by 4%, but according to the World Bank's announcement, Thailand's GDP decreased to 2.5%. However, we account for COGS price fluctuation by averaging the cost over the last few years, which already includes the time of high hog prices. The cost of debt, we calculated from the financing in 2014, in which SORKON relied more on short-term debt than long-term debt with an approximate share of 75%.

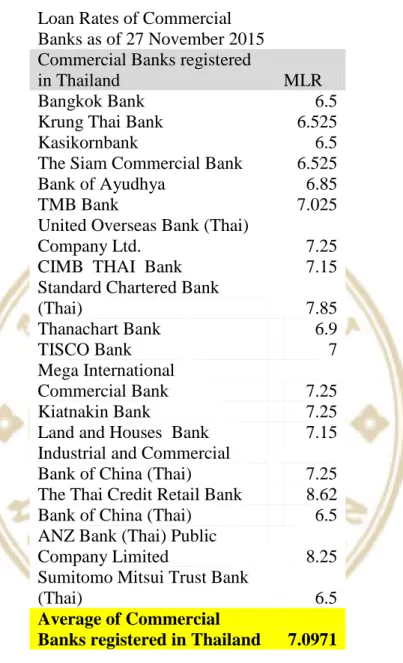

The interest rate on overdrafts was exposed on the annual report with the exchange rate on, so as a conservative point of view we choose the highest interest rate as an assumption. For long-term loans, interest costs were recorded in the annual report as MLR – 1, so we base our assumption on the average commercial bank registered in Thailand MLR to result in a long-term interest rate of 6.1%. Therefore, we calculated using proportional of short/long term debt to get interest bearing debt equal to 7.53% which is the cost of debt before tax.

Ultimately, we calculate the capital structure weight as 48% of debt, with the remaining financing coming from equity. Under the DCF method with our assumption, we value SORKON's share price at 267.45 baht per share.

Financial Statement Analysis

- Summary figures from financial statements (Size analysis)

- Common Size Analysis

- Trend Analysis

- Financial Ratios: Return

- Financial Ratios: Risk

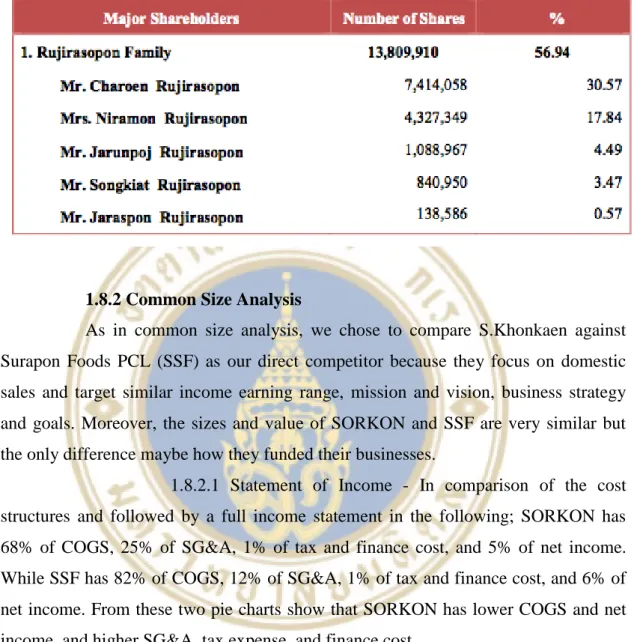

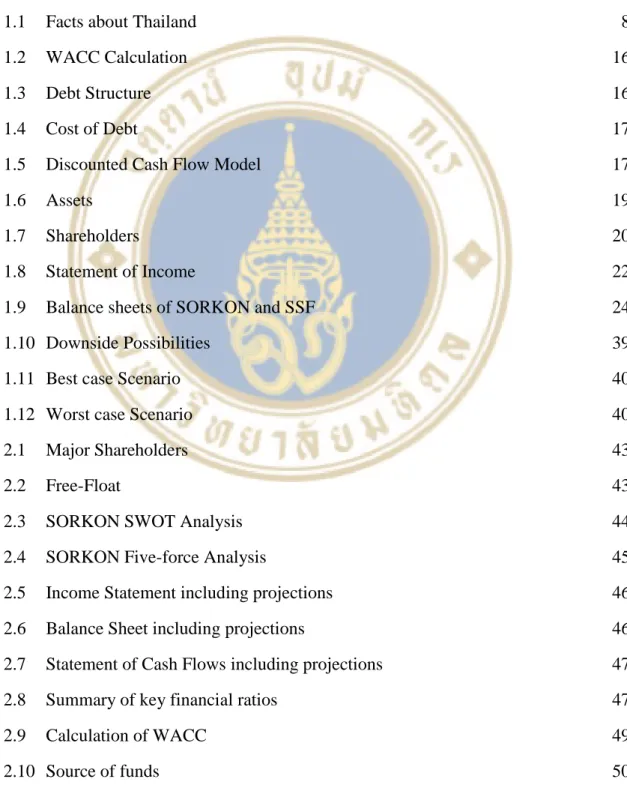

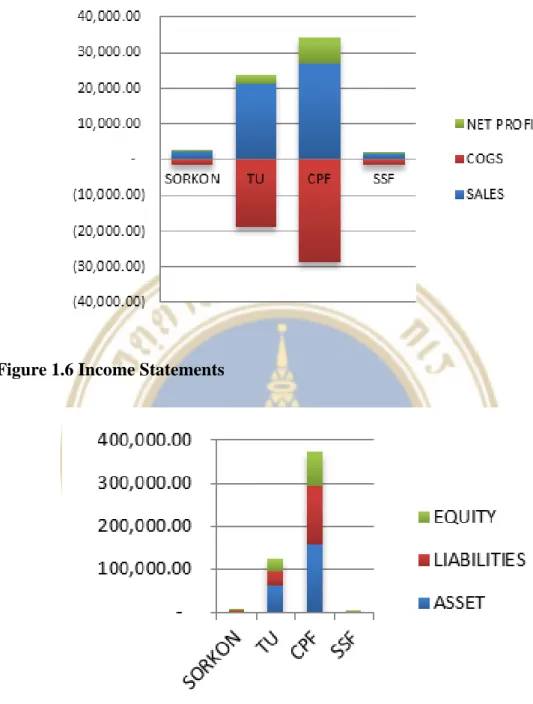

Furthermore, the sizes and value of SORKON and SSF are very similar, but the only difference is perhaps the way they financed their businesses. Of these two pie charts, SORKON has lower COGS and net income, and higher SG&A, tax expense and finance costs. As shown in the income comparison statement, SORKON's net profit in 2014 was 111.42 million baht or 5% of total income; while SSF's net profit was 105.29 million baht or 6% of total revenue.

So we can assume that SORKON's major portion is in PPE, but SSF's major portion is in other non-current assets. Another point is that we noticed that SORKON has significantly higher number in trade receivables compared to SSF from 23% to 7%. We noticed that the magnitudes and values of both SORKON and SSF are quite similar.

SORKON has total current assets of 586 million baht, 1,022 million baht in non-current assets, 735 million baht in total current liabilities, 208 million baht in non-current liabilities and 664 million baht in equity. We can see that SORKON improved in sales and gross margin while it was able to lower its cost of sales and other expenses. One of the main components affecting the longer days for SSF is the day the company changes inventory to cash which is around 48 while SORKON has shorter days at 45.

On the other hand, SSF's profit margins have ups and downs along the line with the maximum number of 12% profit margin in the year 2011.

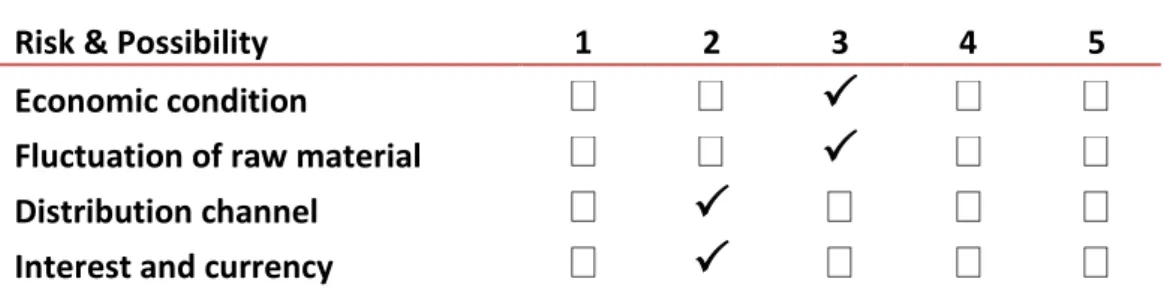

Investment Risks and Downside Possibilities

- Risk from Economic Condition

- Risk from Fluctuation of Raw Material

- Risk from Distribution Channel

- Risk from Interest and Currency

The main channel for the company is through modern trade such as Big C, MAKRO, Lotus, 7-Eleven and etc. where up to 80% of its sales take up. There is possibility that modern trade operators will increase the price such as shelf price and commission on sales. Furthermore, in terms of cash conversion cycle, which normally deals with modern trade, the company must carry long-term cash receivables from the operators.

However, the company is trying to mitigate the risk with greater penetration into other channels such as traditional trade or wet market. However, the short shelf life of the product, where most of the product must be refrigerated, can be one of the obstacles to a wet marketing strategy. Since debt is one of the main means of doing business, interest is one of the concerns that can affect the financial situation.

As for currency risk, since only 10% of sales come from export units, while 90% of products are denominated in Baht currency, the company is only exposed to currency risk to a certain extent. However, to eliminate the currency risk, the company entered into a forward contract to hedge the risk.

DATA

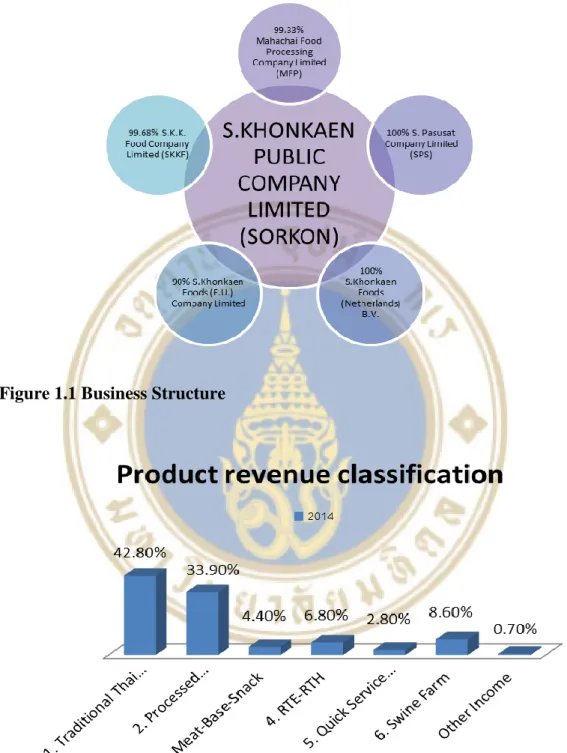

- SORKON Business Structure

- SWOT Analysis

- Five-force Analysis

- Income Statement

- Balance Sheet

- Statement of Cash Flow

- Financial Ratios

- Assumptions

- Revenue Growth Assumptions

- Terminal Growth Rate Assumptions

- Weighted Average Cost of Capital

- Cost of Goods Sold

- WACC

The company also has its own source of raw materials and reliable quality supply, resulting in lower production costs. We believe that SORKON's main products are distinguished from other existing products on the market by the high quality that the company provides. In addition, most of the market shares belong to SORKON, so it is difficult for any other new entrant to enter the market without being noticed and protected by the company.

There are some alternative brands available in the market despite the event of AEC and differentiated products. The Company has its own source of raw materials which makes it easier for the Company to negotiate good deals with other suppliers. Moreover, the required raw materials are common in Thailand and AEC countries, so the company will have high bargaining power from suppliers, besides SORKON is a very big company in Thailand with reliable credit.

From the discussion with management, the company has invested in several projects, including capacity expansion, new product development and branch expansion; therefore we estimated the growth at 10%, where we divide the growth into 2 parts, which is 6% organic growth together with MT expansion and 4% growth from new product launches. There is a possibility of rising commodity prices; fortunately, the company also operates a pig farming business to help minimize such risk.