In this regard, an interesting question is whether financial inclusion affects Islamic banking in Saudi Arabia. Using a questionnaire-based methodology, the results show that the impact of financial inclusion on Islamic banking in Saudi Arabia is limited.

Introduction

However, there is a remarkable impact of the quality dimension of financial inclusion on the three aspects of Islamic banking. This result indicates that the improvement of the quality of products and services results in more confidence, more innovative capacity and a stronger competitive position of Islamic banks.

Research question

Islamic banking industry

- Set of prohibitions

- Set of permissibles

- Financial intermediation of Islamic banks

- Recent trends in Saudi Arabia: overview and challenges

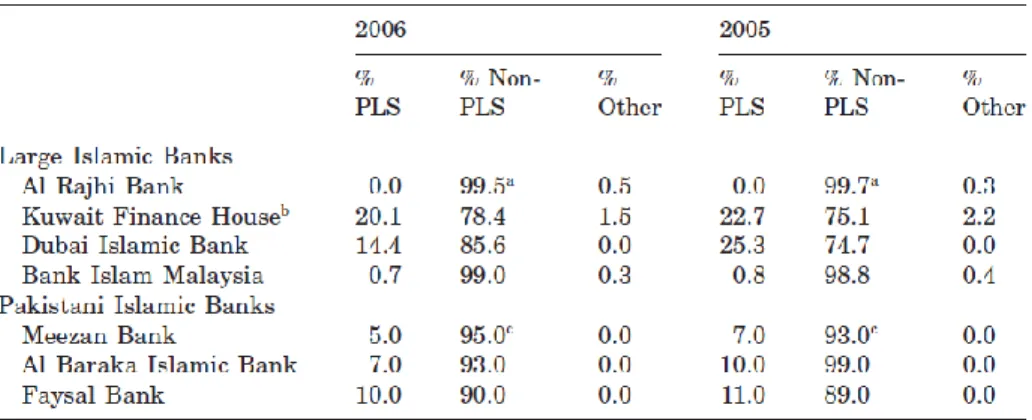

This means that the de facto behavior of Islamic banks does not seem to be consistent with the de jure behavior. Islamic banks' financial intermediation has various common and unusual aspects with conventional banks. The coexistence of inequalities and inequities means that the financial intermediation of Islamic banks must be based on a set of permitted, do not apply any of the set of prohibitions and be oriented towards an ethical role.

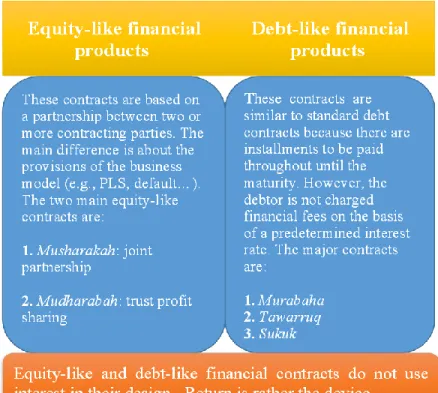

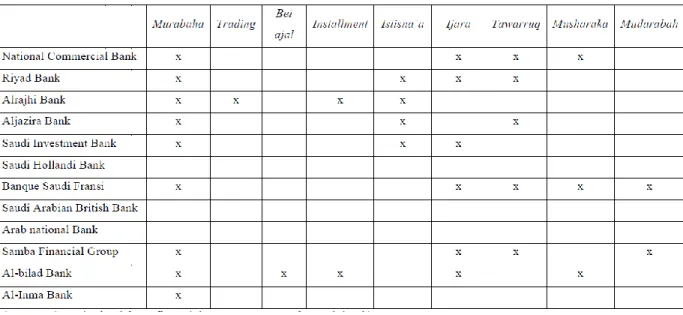

Financial products and Islamic banking can be classified into two main categories, namely debt-like and equity-like products, as can be seen in Figure 4.

Financial inclusion

Dimensions of financial inclusion

Standardization and Regulation: This challenge aims to unify how professionals in the Islamic banking industry can uniformly interpret Sharia-compliant products. All three indicators converge to the idea of facilitating access to external resources at an acceptable price and with a high-quality service. On the part of customers, access to financial resources becomes cheaper, funds can be allocated to low-income customers, the loan process runs smoothly, and the quality of information is improved.

On the banks' side, customer confidence improves, the quality of products and services improves, and the competitive position becomes more favorable.

Recent empirical results

Hypotheses development

Q10 You constantly use your bank's products and services because you think they are sophisticated. Q2 The features of your bank's products and services are most important for increasing its market share. Q4 Long-term use of your bank's products and services can attract new customers.

Financial inclusion seems to affect Islamic banking only in terms of the quality of products and services. The structure of the products and services you use is clear Number Percentage Valid. You constantly use the products and services of your bank because you think they are sophisticated.

The characteristics of your bank's products and services are most important for increasing its market share. 9 Confidence in the bank improves when the quality of the bank's products and services is high. 10 You constantly use your bank's products and services because you think they are advanced.

Empirical methodology and results

Description of questionnaire design

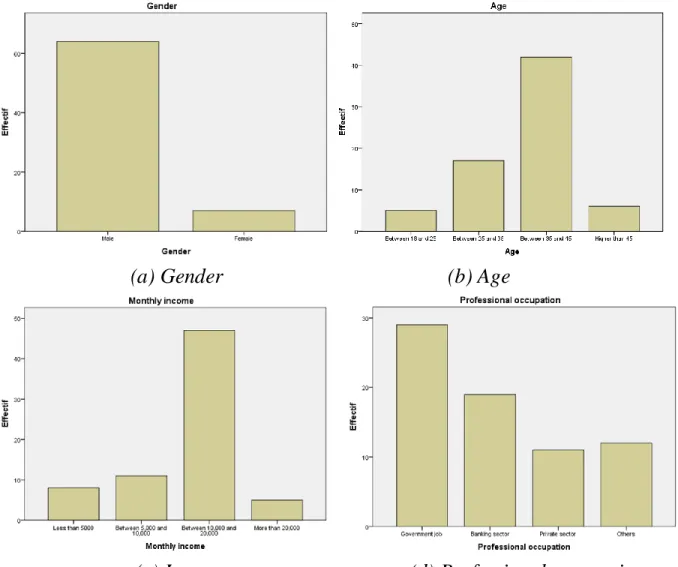

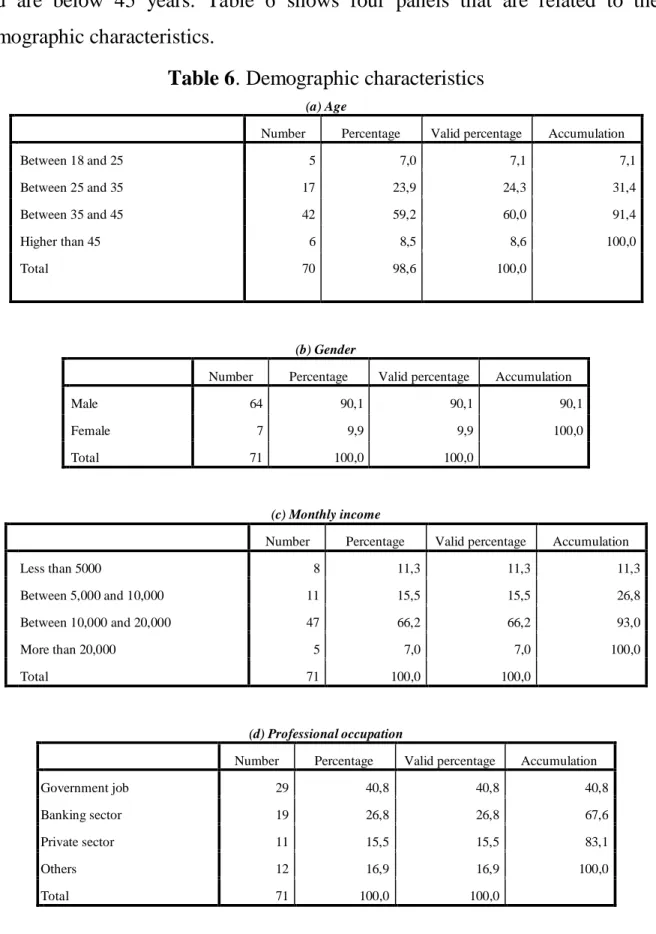

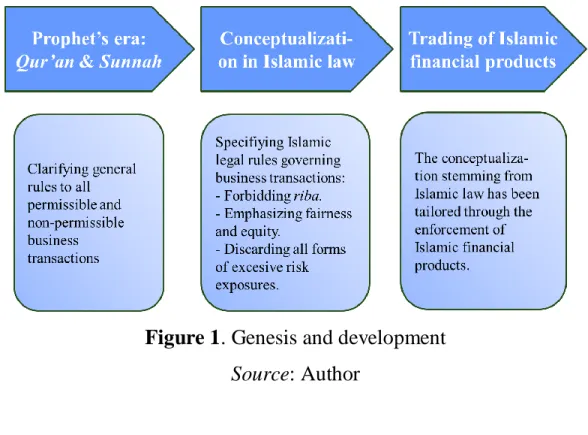

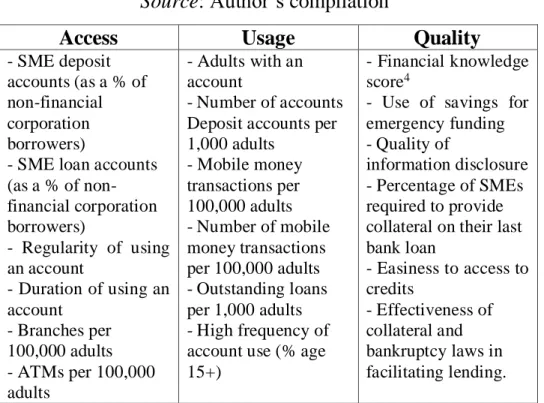

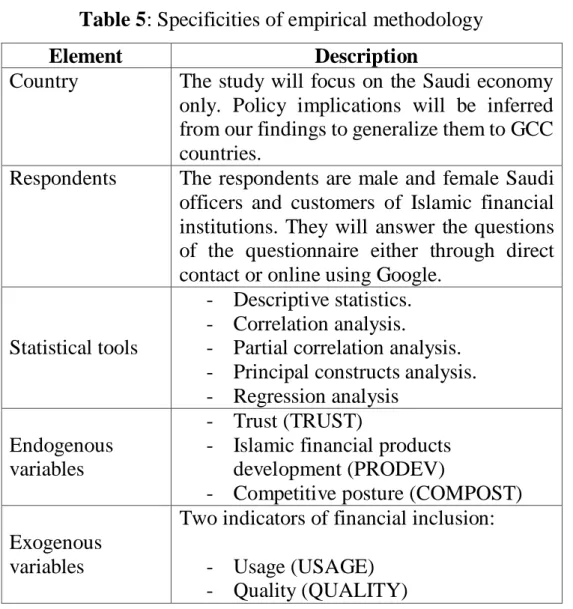

Respondents The respondents are male and female Saudi officers and customers of Islamic financial institutions. They will answer the questions in the questionnaire either through direct contact or online using Google. The questionnaire consists of 4 questions (Part I), 12 questions (Part II), 9 questions (Part III), 9 questions (Part IV) and 6 questions (Part V), which corresponds to 40 questions in total.

Some descriptive statistics

Principal components analysis

Q3You trust that the products and services provided by this bank have an optimal relationship between quality and price. Q8 Your bank makes sufficient efforts to develop new products and services that meet your needs. Q9 You believe that your bank was able to attract new customers because its products and services are sophisticated.

On the one hand, the approach is reflected by questions 4, 5 and 6, because they are highly and positively related to it. On the other hand, it is clear that questions 1, 2 and 3 reflect quality for the same reason. As for product development and competitive positioning, the definition of constructs is done using the same principle.

Quality2, however, is connected to the will and effort in itself to develop new financial products. KMO and Bartlett tests indicate the degree of suitability of the collected data for structure detection. As an illustrative example, note that the Bartlett is statistically significant (p-value, which means that the data is suitable for factor analysis.

Bivariate analysis

This means that Saudi customers believe that product development is closely related to the quality of products and services provided. In other words, Saudi customers believe that Saudi banks develop new products because they will deliver the quality of their product set, and not necessarily for the purpose of increasing their customers' usage in the long run. This result seems to reflect a particular interpretation by Saudi customers in a way that they believe that Saudi banks are willing to continuously improve the quality of their products, which indirectly increase the use of their services.

This means that Saudi customers believe that the quality of products that are supposed to satisfy their needs is positively associated with their trust in the bank. In other words, they believe that when Saudi banks improve the quality of the products and services they offer, their trust increases. This implies that when Saudi banks make efforts to improve the quality of their products and services to meet the needs of their individual and business customers, their competitive attitude tends to increase and strengthen.

This shows that Saudi banks are making an effort to improve the quality of their products and services, which is interpreted as better product development capability. In other words, this penetration indicator, expressed in e.g. the number of bank accounts, is not an incentive for Saudi Islamic banks to develop new products and cannot be considered a causal effect of their strategic attitude and the trust of their customers. This means that improving the quality of products and services to meet the needs of individual and corporate customers increases their confidence and improves the bank's competitiveness in the industry.

Analysis of partial correlations

Furthermore, the bank's focus on this aspect increases their ability to innovate and offer new financial Islamic financial products that are Shariah compliant. There is a purely positive and statistical correlation between trust (Trust_access and Trust_quality) and product development (Prodev_quality1). This indicates that financial inclusion seems to positively intervene in these two aspects in a way that when a Saudi bank pioneers sophisticated financial products and services that meet customer needs, trust in the latter increases.

This result is quite logical because trust cannot improve if the bank does not make supplementary efforts to provide more suitable products and services. We noticed that trust induced by access is positively correlated with product development 1, in addition, trust induced by quality is negatively correlated with product development 1. This fact may have a behavioral explanation because customers increase their trust (access to new services and products) ) as result of sophisticated banking products.

The variable Prodev_access is positively related to Compost_access, which means that the intervention of financial inclusion causes the efforts made to develop new products and services simply to increase the number of accounts (i.e., the first dimension of financial inclusion, access) turns out to negatively affect the competitive attitude. In other words, innovating new products and services for the simple purpose of increasing competitive strength cannot make it right. However, it is clear that such efforts can be fruitful when aiming to improve the second dimension of financial inclusion (ie, use) in terms of expanding clients.

Regression analysis

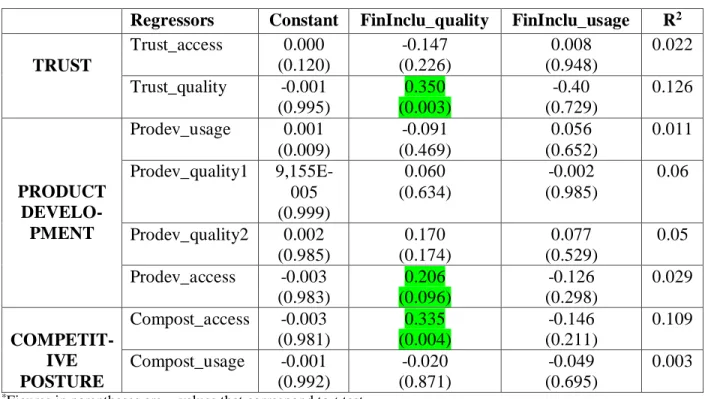

The regression includes the two constructions of financial inclusion as the main regressors (independent variables) and the different constructions of the three aspects of Islamic banking. On the one hand, the use dimension of financial inclusion does not matter for the three aspects of Islamic banking. On the other hand, the quality dimension of financial inclusion matters to some extent for the three aspects of Islamic banking.

This means that Saudi respondents in the sample believe that Saudi banks are taking into account the quality dimension preached by financial inclusion to improve their customers' confidence, to innovate new ones. Moreover, the results do not show that Saudi banks are doing the same by taking into account the use dimension of financial inclusion. The general regression results show that there is a limited impact of financial inclusion on the three aspects of Islamic banking, confirming the bivariate and partial correlation analyses.

Indeed, it is clear from the previous table that at least one item corresponding to each of the three Islamic banking aspects is positive and statistically significant. An additional result is clearly shown through the weak relevance of the usage dimension and the importance of the qualitative dimension of financial inclusion in the Islamic banking industry. These results fully confirm our previous findings, because it is clear that the qualitative dimension of financial inclusion seems to be more informative about how the latter can interact with Islamic banking.

Conclusions and policy implications

Do you think the staff help you to have easy access to the bank's products and services? Do you think you and your bank's customers are better off when you use the products and services offered? You believe that the products and services offered by this bank have an optimal quality-price ratio.

You think your bank has been able to attract new customers because its products and services are advanced. 10 Do you find that the staff helps you to easily access the bank's products and services? 12 Do you think that you and your bank's customers are better off using the products and services offered?

3 You trust that the products and services of this bank have an optimal price-quality ratio. 1 The products and services offered by your bank are advanced Strongly disagree Agree Neutral Agree Strongly agree. 3 There is a suspicion of the use of prohibited interest in one of the products and services offered by your bank.

8 Your bank is making sufficient efforts to develop new products and services that meet your needs. 9 You believe that your bank was able to attract new customers because its products and services are sophisticated.