It was not until 1998 that regulators in Shanghai and Shenzhen realized the importance of effective monitoring and therefore introduced delisting regulations.1 The delisting rules state that if a listed company reports accounting losses for two consecutive years (ie . negative profit), its stock will be given 'Special Treatment' (ST) status. In our sample, the earnings-based delisting rule triggered 83% of involuntary withdrawals in China, so we focus on this paper. As suggested by Shleifer and Vishny (1992) and Asquith et al. 1994), the liquidation value of the company's assets will be less than the market value of the company's equity capital.

The sample is then grouped into healthy firms and firms at risk of delisting due to the earnings-based delisting rule. An ST firm that receives special treatment due to profit-based rules is given the value 1 for the ST dummy variable, and 0 otherwise. Another official from Shandong province noted "The main point is that the firm must comply with government policies designed for tax-based subsidies."

To assess the impact of a subsidy, the timing of the outcome variables in the test is crucial. An ST company is defined as a company that is at high risk of delisting because it receives special treatment due to the revenue-based rules. It is given the value 1 for the dummy variable ST, and 0 otherwise. In this study, the backgrounds of the largest shareholder and the background of the ultimate controller are manually collected and examined.

To measure the strength of political connection, this study calculates the percentage of the council who work or have previous work experience in the government or the military (PoliticalConn(%)).6 The two variables of political connection are collected manually.

Methodology

ST covers whether and to what extent the risk of delisting affects the government's decision to subsidize. PoliticalConn captures who the company is associated with, and Country captures the nature of the company's ownership. Since firms at risk of withdrawal may also participate in other restructuring programs such as mergers and acquisitions, this study also includes restructuring to control for the impact of the restructuring program on the firm's subsidy receipt.

This study also includes industry dummies as important variables to capture the government's decision on a subsidy. Li and Yamada (2015) and Tian and Estrin (2008) find that the government retains a stake in certain industries for national security and development purposes, thus it is likely that. Equation (2) is estimated using only a sample of ST firms. Z)*[]^_ represent Tobin's q and ROA, respectively.

It measures the impact of a government subsidy on an ST firm during the delisting risk period versus the non-delisting risk period. PoliticalConn (%) is used in equation (2) to examine the role of political connection in a firm's performance. 17 the percentage measure is used instead of a dummy variable that is more appropriate for a probit model in Equation 1.

The variable Ln(K/S) is used to measure the extent of the agency problem because tangible assets are easier to monitor and can be used as good collateral. The higher the cash flow of a firm in this sample, the better it is for the firm's performance. This study also includes industry dummy variables to control for industry fixed effects in all equations.

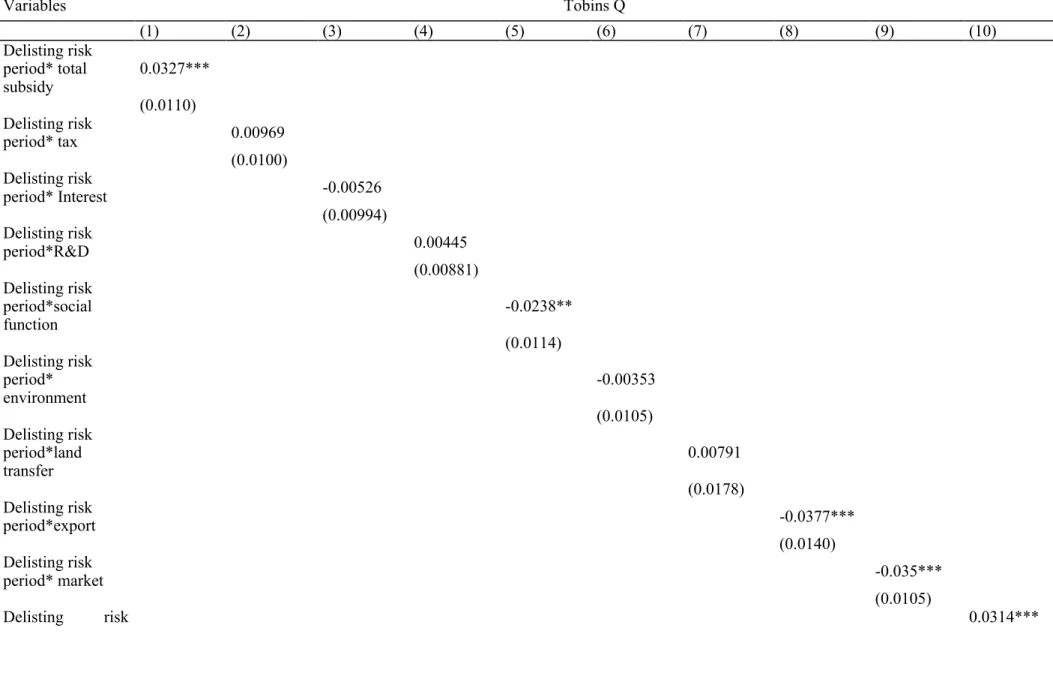

To enrich the understanding of subsidy, it is assessed how each specific type of subsidy affects firm performance. The estimation model is an extension of equation (2) formulated as follows: .. 3) Equation (3) is estimated using only a sample of ST firms. The coefficient c/ captures the effect of the size of each different type of subsidy on the performance of an ST firm.

Results

This suggests that when an ST firm faces a delisting risk, it is less likely to receive a government subsidy. The interaction term for ST firms*State is positive and significant, but the interaction term for ST firms*PoliticalConn is not significant. This result shows that having government ownership can help ST firms (non-healthy firms) to receive a government subsidy, but not by establishing political connections.

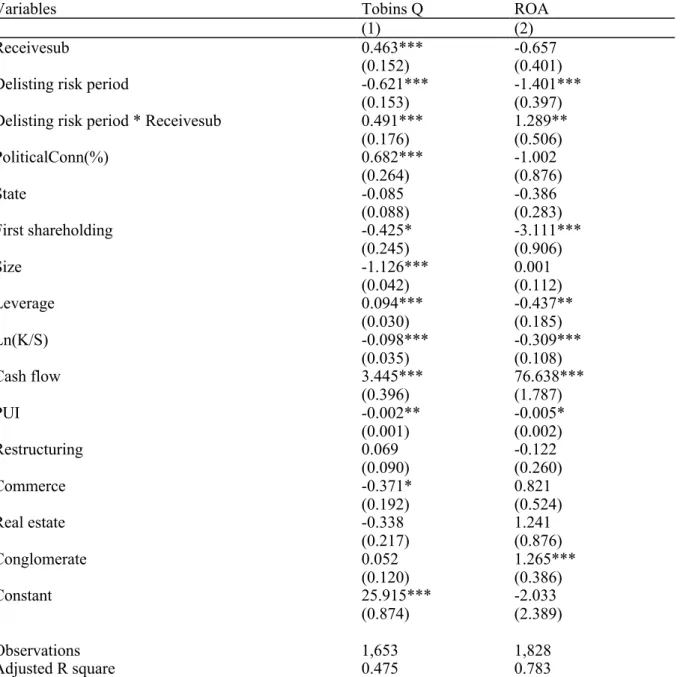

In Table 6, the coefficient of Receivesub in the Tobin's q equation suggests that subsidy recipients have an average Tobin's q that is 0.463 units higher than non-recipients, but there is no effect on ROA. The result for the coefficient for the delisting risk period shows that ST firms in the delisting risk period have an average Tobin's q that is 0.621 lower than in the post ST period. Similarly, ST firms have an average ROA that is -1,401 units lower during the delisting risk period than after the ST period.

For the interaction terms, the coefficient for the period of delisting risk* Receivesub is statistically positive at 0.491 for Tobin's q equation and 1.289 for ROA equation. In this section, the study elaborates on subsidy channels by classifying subsidies into nine groups for ST firms. This is followed by a tax credit or refund with 284 deals averaging RMB 12.5 million (US$1.9 million).

There are 223 environmental subsidy agreements with an average of RMB 3.9 million per agreement (US$0.6 million). The least given type of subsidy is landless transfer, but the size is 12.2 million RMB (1.8 million US dollars). This section assesses the impact of different types of subsidies on the performance of an ST firm.

The results show that, overall, the total subsidy has a positive effect on Tobin's q during the delisting risk period, which is consistent with our results in Table 6 and hypothesis 3. The market probably perceives those subsidies as negative for Tobin's q because an ST company must first bear the costs before a subsidy can be awarded and the amount awarded is really small compared to the costs and risk of failure, not to mention the time needed for the international market to pick up compared to the tight time frame for an ST firm. In terms of Tobin's q equation, in total, the total subsidy has a positive effect on ROA during the delisting risk period.

Conclusions and implications

This shows that a company can receive multiple subsidies and that the total amount is more important than the individual types. A firm is coded as state-owned if the government is the largest shareholder or if a government-controlled nominal agent is, and is coded as non-state otherwise. A company is considered to have political connections if at least one board member works or has previous work experience in government or the military.

A firm is considered politically unaffiliated if none of its board members work for or have previous work experience in government or the military. Tobin's q is the sum of the market value of assets and debt divided by total assets at the end of the year; when there is non-negotiable capital, the accounting value is used (this variable is estimated at 1%). State is a dummy variable equal to 1 if the government or a nominal agent controlled by the government is the largest shareholder, and 0 otherwise.

PoliticalConn(%) is the percentage of the Board that has work or previous work experience in government or the military. First shareholding is the percentage of shareholdings held by the largest shareholder. Cash flow is measured as net income before extraordinary items and depreciation divided by the replacement value of capital stock at the beginning of the year, gained at 1%. EM is the industry average adjusted accruals, gain at 1%; Accruals are defined as the difference between net income and cash flow from operating activities divided by total assets.

Note: Table 4 shows the average of the key variables for the pre-ST, ST and post-ST period for firms at risk of delisting. NUM is the number of all listed companies in a province in a given year where the headquarters of a listed company is located. Z-score is Altman Z-score calculated as Z = 1.2WC_TA + 1.4RE_TA+ 3.3EBIT_TA + 0.6MV_BV + 0.99S_TA, where WC_TA: working capital/total assets, RE_TA: retained earnings/total assets, EBIT_TA: earnings /earnings before interest total assets, MV_BV: market value of equity/book value of total liabilities, S_TA: sales/total assets.

EM is industry average adjusted accruals, allocated at 1%; Accruals are defined as the difference between net income and cash flow from operating activities divided by total assets. Tobin's q is the sum of the market value of assets and liabilities divided by total assets; when there is non-negotiable equity, book value is used (this variable is profitorized at 1%). ROA is measured by net income divided by total assets, then winsorized at 1% level.

PoliticalConn(%) is the percentage of the board that work or have previous work experience in government or the military. Cash flow is measured as net profit before extraordinary items and depreciation divided by the replacement value of the share capital at the beginning of the year, winsorized at 1%.