We examine the impact of the US government's response to the COVID-19 pandemic, including strict social measures and financial support packages, on corporate investment. We find it imperative to examine how the COVID-19 pandemic and the government are responding to the crisis. First, we document, on average, a positive response from corporate investment to the government's response to COVID-19.

We study business investment during the COVID-19 crisis to address the economic impact of the devastating pandemic and the consequences of the government's response to the pandemic. Based on this conjecture, we expect a positive impact of the government response to the COVID-19 crisis on business investment. Our study is positioned in the rapidly developing literature on the economic impact of COVID-19 as one of the first studies to examine how government response to the pandemic would impact business activity.

GSTRINGENCY is used to examine the impact of the pandemic social distancing and containment measures on corporate investments of US firms. The new variable (GESI) is to evaluate the impact of government economic support on corporate investment of US firms. However, we doubt that CAPEX and NCAINV are valid measures to examine the impact of the government's response to the COVID-19 crisis on corporate investment.

These two variables are used to examine how corporate investment during the COVID-19 crisis responds to government policies.

Model specifications

Applying this procedure, we obtain two alternative measures of business investment after extracting the impact of COVID-19, namely Res_CAPEX and Res_NCAINV.

Data and sample

13 uncertainty shocks such as the US-China trade war, the Global Financial Crisis and US election years on corporate investment. To ensure the comparability of corporate investment between firms in our sample, we exclude all financial firms from the sample. All financial data items are winsorized at the upper and lower percentiles to alleviate the impact of outliers on the outcomes of our analysis.

The Stringency Index and the Economic Support Index (Hale et al., 2020) are taken from the Oxford COVID-19 Government response Tracker (Ox-CGRT) database. We use official COVID-19 data from the US Centers for Disease Control and Prevention (US CDC), including the daily data on the number of infected COVID-19 cases and deaths due to COVID-19 in the US. Since there were no confirmed cases of COVID-19 in the United States prior to January 21, 2020, we assign all data points for COVID-19 CASES and COVID-19 DEATHS prior to this date with the values zero.

This treatment applies to both COVID-19 data and government response data (GSTRINGENCY and GESI).

Empirical results and discussion

Descriptive statistics

Furthermore, fixed characteristics such as SIZE, LEVERAGE, ROA, SALESGR and DIVIDEND are positively correlated with CAPEX.

The impact of COVID-19 on corporate investment

- The net effect of government’s responses

- Additional analysis

We observe a significant positive coefficient (0.0023) of the GESI (t-statistic) which means a positive impact of the economic support stimulus on corporate investment. The results also suggest that the government's response to the pandemic crisis is not only affecting long-term investment, but also shows a significant impact on US firms' short-term investment.This is an important finding that suggests business activities are picking up with the support of the government's response as lockdown and social distancing restrictions are eased.

In contrast, profitability (ROA) and sales growth (SALESGR) show a significant positive impact on corporate investment regardless of the investment proxy. Overall, the results in Table 4 show that the government's response to the COVID-19 crisis, in terms of controlling the spread of the disease and extending economic support, has proven to be a reassuring factor for US businesses. The findings support our hypothesis 1 and are consistent with current literature showing a positive impact of government response on investors and business confidence, leading to improved stock market performance (Ashraf, 2020;.

Next, we use sub-sample analyzes to account for various market-level, seasonal, and estimation factors that may influence the causal relationship between government response and corporate investment. Panel A, Table 5, shows that the response of the US government to control the spread of COVID-19 has a significant positive impact on corporate investment, regardless of the choice of investment measure. These observations suggest that our baseline model captures the actual impact of government response on corporate investment in the wake of the COVID-19 crisis.

Overall, the results of the subsample analyzes are consistent with our baseline estimates, suggesting that market-wide or seasonal effects do not drive our findings about the impact of government response on corporate investment. Rather, our results confirm that there is a positive effect of the government's response to COVID-19 on corporate investment. To provide a better understanding of the positive impact of the government's response to COVID-19 on corporate investment, we consider two firm-specific factors, namely the degree of.

We divide companies into those with higher and lower political risk9 to determine the impact of political risk on the relationship between government responses and business investment. Panels A and B, Table 6 show that the government response in the form of stringent measures and economic support have a more pronounced effect on business investment in companies with a lower level of political risk compared to companies with a higher level of political risk risk. . A comparison of coefficients indicates that the impact of the government response on business investment for firms with lower political risk is almost double compared to firms with higher political risk (0.0026 and 0.0023 compared to 0.0013 and 0. 0014).

Conclusion

19 The results show that corporate investments of firms with higher investment irreversibility react less positively to government policies during COVID-19, compared to their counterparts. More importantly, our results show that the gap in the difference in investment between higher and lower investment irreversibility industries is widening when capital expenditure is used as a proxy for investment. This observation suggests that firms in higher investment irreversibility industries are less inclined to make long-term investments due to prevailing uncertainties under the pandemic.

Our results confirm the findings of Demers (1991), Dixit (1995), Gulen and Ion (2016) and Kim and Kung (2017) that firms with higher investment irreversibility tend to be more cautious in making investment decisions during market turmoil. Furthermore, with regard to investment irreversibility, empirical results show that corporate investments of firms with higher investment irreversibility react less positively to government policies during COVID-19, compared to their counterparts, and that those firms are less inclined to make long-term investments due to the prevailing uncertainties in the context of the pandemic. Finally, our findings suggest that austerity measures and stimulus packages of economic support, at the same time, by a government to counter the economic and social effects of COVID-19 can increase the confidence of businesses to invest and accelerate the pace of economic recovery.

This provides practical implications for policy makers and governments who may face dilemmas during the decision-making process to control the next spikes of COVID-19 or a similar pandemic in the future.

Muthukrishnan, 2020, Corporate Recruitment under COVID-19: Labor Market Concentration, Downskilling and Income Inequality, Working Paper 27208 (the National Bureau of Economic Research). Weber, 2020, Labor Markets During the COVID-19 Crisis: A Preliminary View, Working Paper 27017 (the National Bureau of Economic Research). Xie, 2020, Corporate Immunity to the COVID-19 Pandemic, Working Paper 27055 (The National Bureau of Economic Research).

Genovese, 2020, Impacts of the COVID-19 Pandemic on Global Agricultural Markets, Environmental and Resource Economics. Jabeur, 2020, The Bubble Contagion Effect of the COVID-19 Outbreak: Evidence from the Crude Oil and Gold Markets, Finance Research Letters, 101703. Kira, 2020, Oxford Covid-19 Government Response Trackers, Working Paper 25 (Blavatnik School of Government, University of Oxford) .

Gómez, 2020, Estimating the COVID-19 cash crunch: Global evidence and policy, Journal of Accounting and Public Policy 39, 106741. CASES OF COVID-19 The natural logarithm of one plus the total accumulated number of cases of COVID-19 in the United States. The natural logarithm of one plus the total number of total deaths due to COVID-19 in the United States.

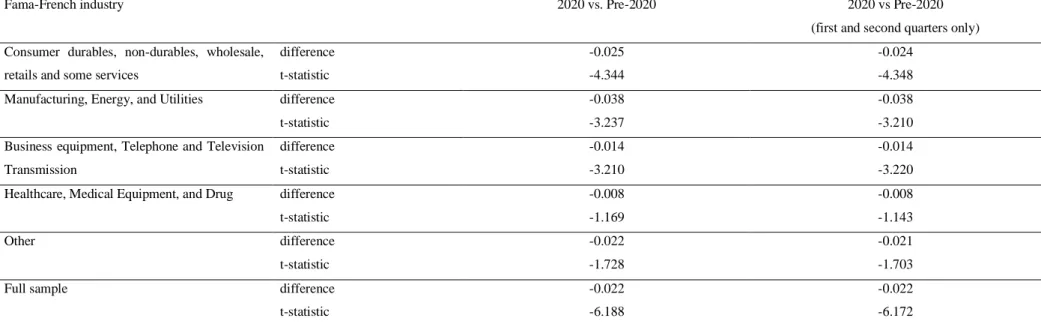

GSTRINGENCY The natural logarithm of the Stringency Index that records the stringency of the country's containment policies in response to the COVID-19 pandemic from the Ox-CGRT database. Confirmed COVID-19 cases, deaths, and government responses to COVID-19 in the United States from January 2020 to June 2020. Tests of mean difference of corporate investment between COVID-19 period and other periods by Fama-French operation. First and second quarter only) Consumer durables, non-durables, wholesale,.

Tests of the average difference in business investment between the COVID-19 period and other periods, by SIZE quintile. first and second quarter only). Tests of the average difference in business investment between the COVID-19 period and other periods by CAPEX quintile. first and second quarter only). Tests of the average difference in business investment between the COVID-19 period and other periods by LEVERAGE quintile. first and second quarter only).

32 This table shows the regression results of model (2) using alternative measures of corporate investment and government responses to the COVID-19 pandemic. The Net Effect of Government Responses to COVID-19 on Firm Investment Given Irreversibility and Firm-Level Political Risk Panel A.