The authors have received invaluable assistance from a number of individuals while working on this report. In particular, the authors would like to thank Bronwyn Howell, Managing Director of the New Zealand Institute for the Study of Competition and Regulation, and Lew Evans, Professor of Economics at Victoria University in Wellington. All of these people generously gave their time and were willing to give a candid look at New Zealand's gas industry.

The views in this report are those of the authors and do not necessarily represent those of the institutions with which they are affiliated or their constituent members.

Introduction

The authors were also able to speak to other experts in the gas industry in New Zealand. While all these discussions remain confidential, the information and understanding gained from these meetings provided useful background information for the preparation of the report. The second part of the report provides an overview of today's gas industry along with some production and demand forecasts.

The third part of the report provides an analysis of the key policy issues facing the industry and makes a number of policy recommendations.

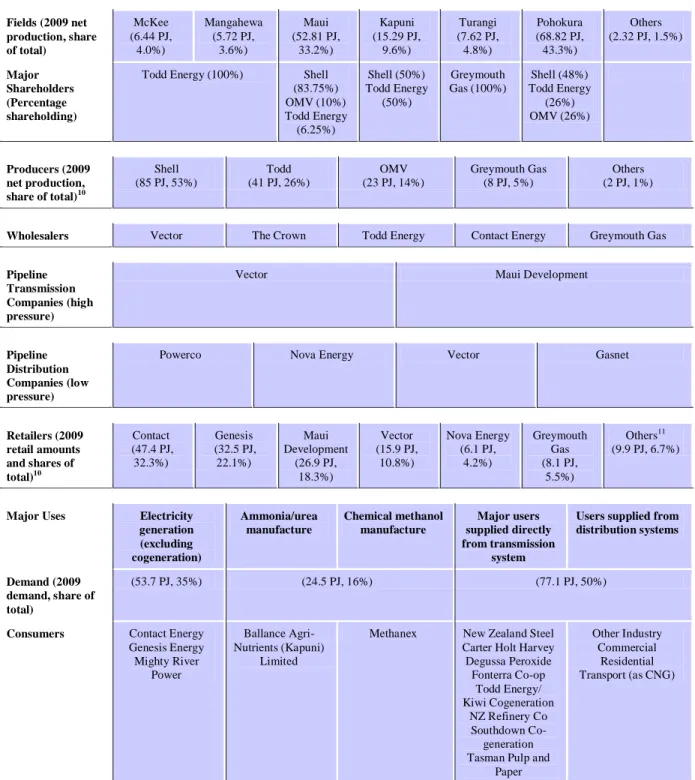

Overview of the Gas Industry in New Zealand

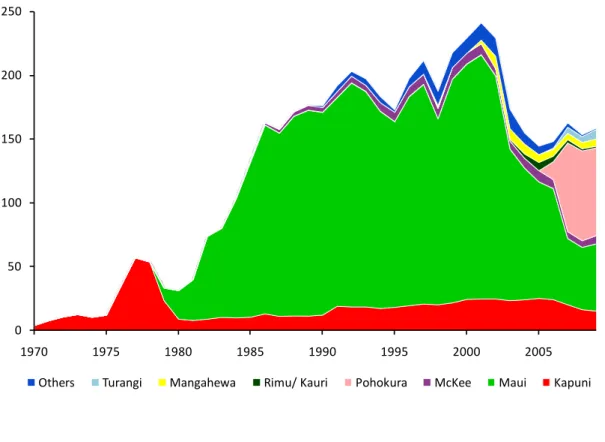

Contact Energy is a major user of gas, with gas-fired power stations in Stratford in the Taranaki region and Otahuhu in Auckland.6 Currently, Contact Energy has no generating assets. Australian energy company Origin Energy owns 51 percent of Contact, and they hold a number of oil exploration licenses in New Zealand, including a 50 percent interest in the Kupe field.7 The Kupe field contains approximately 13 percent of New Zealand's P508 gas reserves. As reserves and production at the Maui field have declined, a number of new fields, notably Pohokura, have been developed in the region, offsetting much of the decline in Maui production.

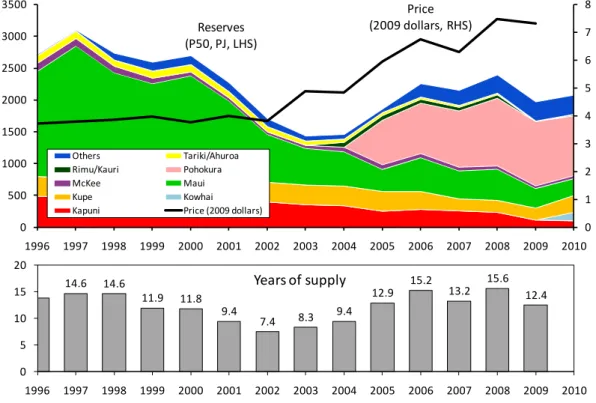

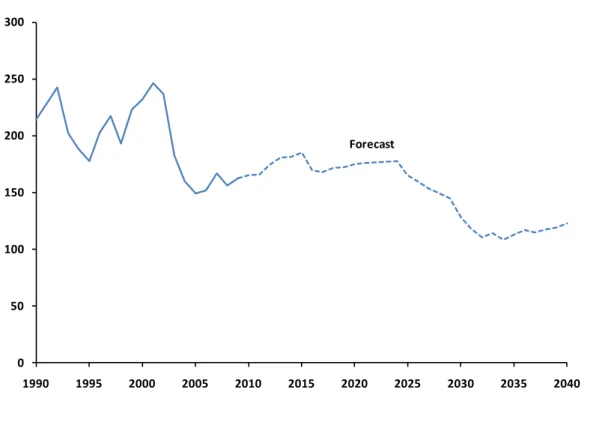

Since the prices on the chart are averages, they may deviate from the marginal price of gas in the period. In the future, the demand for gas will be largely dependent on developments in the electricity sector. The real wholesale gas price is expected to remain constant in the reference scenario until 2030.

Gas produced in the Taranaki region is distributed throughout the North Island through these networks. Most areas in the North Island are served by these networks, with the notable exception of the Wairarapa region. There is currently no gas transmission from the North Island to the South Island and no gas production in the South Island.

A large part of the existing gas pipelines and distribution networks was built in the 1970s by the then state-owned Natural Gas Corporation. The Maui pipeline can adjust to this changing demand by changing the pressure and consequently the amount of gas in the pipeline. The current lack of capacity in the Vector pipeline system means that new gas-fired power stations are likely to be built mainly in the Taranaki region, close to the gas fields.

This trend is also supported by recent increases in investment in the electricity transmission network across New Zealand.

Analysis and Policy Issues for the Gas Industry in New Zealand

Due to the cost of proving reserves, years supply cannot be expected to be greater than this. Currently, MED appears to provide little if any analysis of the data it collects. However, it appears to be the case that participants in the gas industry express reservations about almost every one of the regulatory components that have been introduced.

In any case, the CPI is a questionable measure of inflation for the annual asset value adjustments that are part of the Commission's proposal. Under the proposed CPP, once a new investment is approved, the default value-for-money (CPP) path would change to a CPP with terms more appropriate to a company's specific circumstances. Second, it affects the Commission's credibility because the Commission did not stand by the results of its own analysis.

As a result, the Commission uses different methodologies and determines the middle of the rate of return calculations. There are other concerns about aligning the duration of risk-free assets used in rate-of-return calculations with the economic life of pipeline investments. However, because there are concerns about many components of the regulatory framework for pipeline companies, the Commerce Commission should reconsider its rate of return determinations to ensure that the permitted rate of return is sufficient to allow regulated pipeline companies to attract new capital.

As a result of this example, and perhaps other aspects of the proposed regulation, the Commerce Commission should consider simplifying the proposed standard price-quality path methodology and take steps to reduce the risk inherent in the regulations. Fundamental to the regulation of a company such as a pipeline company is the concept of the regulatory bargain. For this to work, the regulated companies must be confident that the regulator will honor its side of the bargain.

Because of past and proposed actions, a number of industry participants are not confident that the Commission will uphold its end of the regulatory bargain.

Summary

Major Transmission Pipelines

The Maui High Pressure Transmission Pipeline carries gas as far north as the Huntly Power Station, which can be fired by coal or gas. North of Huntly, the Vector high-pressure transmission pipeline carries gas through Auckland to Whangarei. Major gas users on the Vector transmission pipeline in this area include NZ Steel at Glenbrook, the Otahuhu and Southdown gas-fired power stations, Fonterra at Kauri and Maungaturoto and the Marsden Point refinery.

The Papakura to Henderson transmission pipeline section (shown in green on Map 3) was designed to operate at a lower pressure than other sections of Vector's transmission network. This section is currently limited in capacity, and an upgrade of sufficient capacity to support further industrial production or electricity use would require a bypass pipeline to be constructed along with several sections of the current pipeline. This investment would be large, and although current capacity is limited, it is unlikely that a significant portion of the new capacity resulting from the investment could be absorbed by current demand without a large new user such as energy proposed Otahuhu C or Rodney with gas. the stations.

Northern New Zealand Transmission Pipelines

Major Transmission Pipelines and Large Gas Fired Power Stations

It is costly to transport both gas and electricity, so the location of new gas-fired power plants will be based on a trade-off between production locally to demand or locally to supply of gas, as well as a trade-off of transmission capacity both on the pipeline network and on the electricity transmission network. Vector and Powerco operate the largest distribution networks and, along with Gasnet, are subject to the proposed price-quality regulation by the Commerce Commission. These networks were built as by-pass networks to compete with incumbent distribution companies.

Nova Gas' distribution network is not subject to the Commerce Commission's proposed price quality regulation, nor is it subject to the open access requirement.

Transmission Pipelines and Distribution Networks

While significant privatization of the gas industry took place in the 1990s, a key participant in the gas industry, Genesis, remains state-owned. In the end, both state-owned companies and their privately-owned competitors are uncertain about the arrangements, and this can hamper the functioning of the market. Such privatization can bring benefits, primarily from the investment community's increased control of the company and the need to make its transactions and business relationships more transparent.

With regard to the Commerce Commission's (Commission's) regulation of gas pipeline companies, it is important to point out that the Commission has proposed forms of price regulation, either a weighted average price cap or a revenue cap42, which are superior to e.g. regulation of rate-based returns in terms of the efficiency incentives and flexibility they provide. This is noted by the Commission as an advantage of the weighted average price cap for Vector and distribution companies with large networks considering incremental investments.45 However, the investing company will need to have volumes increased sufficiently to generate sufficient revenue to enable it to recover its investment. Overall, the implementation of the CPP does not appear to be a good regulatory policy, at least in terms of its potential effect on investment.

Another possibility is that a new power plant to be served by the Vector pipeline could be responsible for purchasing enough new pipeline capacity that it would be possible for Vector to build it under the proposed DPP regulation. If the amount of purchased capacity were to increase sufficiently as a result of the new power plant, the quantitative risk that Vector would face from the new pipeline investment would be manageable. In addition to the fact that an electricity generator knows that there would be pipeline capacity available, it also relates to the issue of availability of gas supplies and the different views of producers compared to sellers and customers.

Using a shorter term, which generally yields a lower interest rate, does not sit well with the longer-term life of the assets. Some of these contributing factors are the valuation of the asset base for the regulation, the determination of the rate of return, the mechanics of the proposed DPP, and the determination of the CPP. Businesses are concerned about what the Commission might do at the end of the five-year period and whether any efficiency gains created as a result of the incentives put in place under the default value-for-money regulation will be recouped. .

As a result, the Commerce Commission should consider steps to strengthen the industry's perception that it will honor its side of the regulatory agreement before, during and after the price adjustment period.