Relative GDP per capita is an important determinant of the real exchange rate not only at the aggregate level, but also at the level of individual goods. Based on these two characteristics of the data, we develop a theoretical model of determining the real exchange rate. In addition, in the model, real exchange rates are linked to the movement of internal relative prices.

Similarly, if a country's average real exchange rate is well above (below) PPP relative to the EU average, almost all individual real exchange rates are above (below).

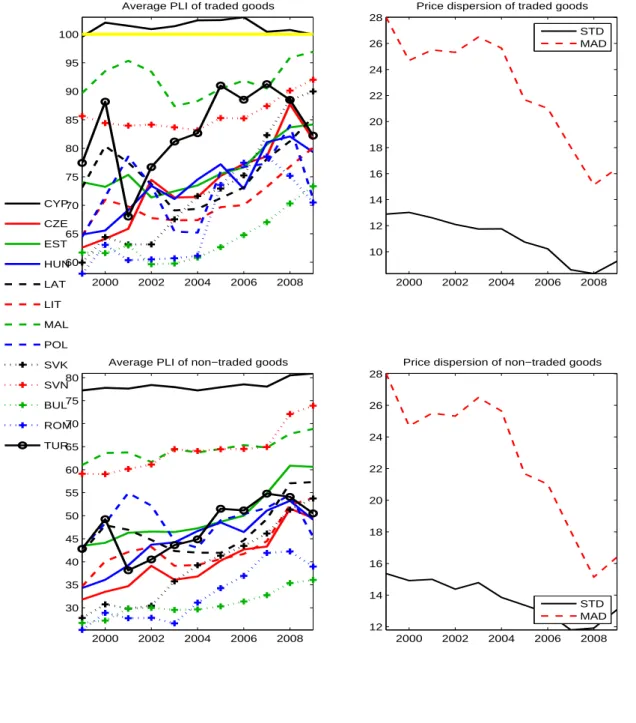

Decomposition into Traded and Non-Traded

Thus, the proportional difference in real exchange rate adjustment between euro area members and floaters at the disaggregated level is much less than at the aggregate level.9. The average deviation from PPP is much higher for the non-traded category, although again there are significant deviations from PPP for the traded category, and the time series characteristics of real exchange rates are essentially identical for both traded and non-traded categories. Thus, countries with higher real exchange rates have on average higher relative prices of non-traded goods.

It shows the relationship between the average rate of real exchange rate appreciation and the average rate of growth in prices of non-market goods relative to traded goods in the sample where each observation represents.

4 Real Exchange Rate Determinants

Real Exchange Rates and Relative GDP per capita

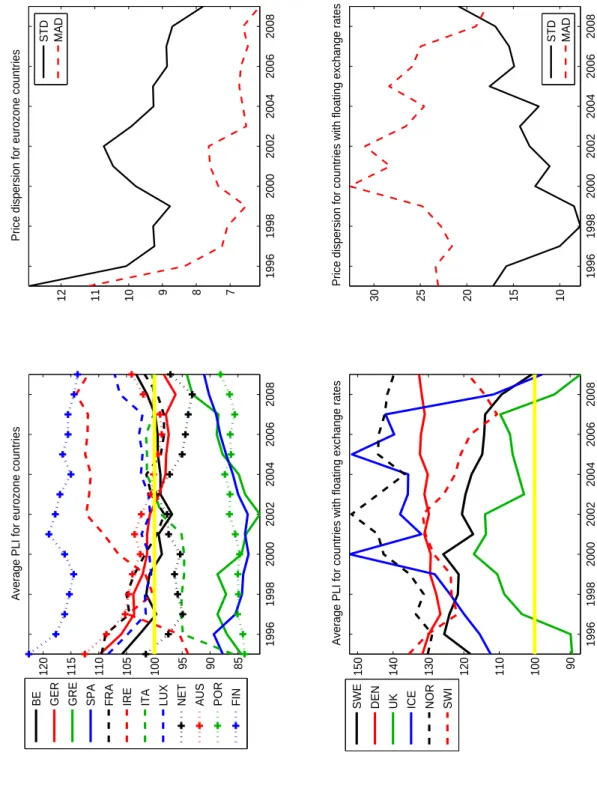

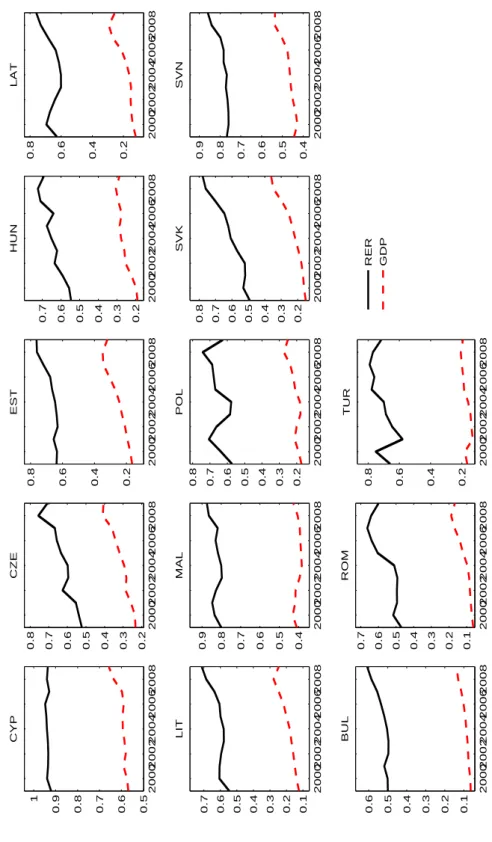

Switzerland, Norway and the Netherlands; real GDP per per capita is proportionally more above the EU average, which is their real exchange rates. Figure 9 suggests that the ratio between GDP per per capita and real exchange rates hold both cross-sectionally and over time. But also within countries, movements in the relative GDP per Inhabitants tend to be associated with movements in real exchange rates in the same direction.

The figure presents a scatter plot of real exchange rates and GDP per capita across all countries and time periods in the sample.

Real Exchange Rates at Monthly Frequency

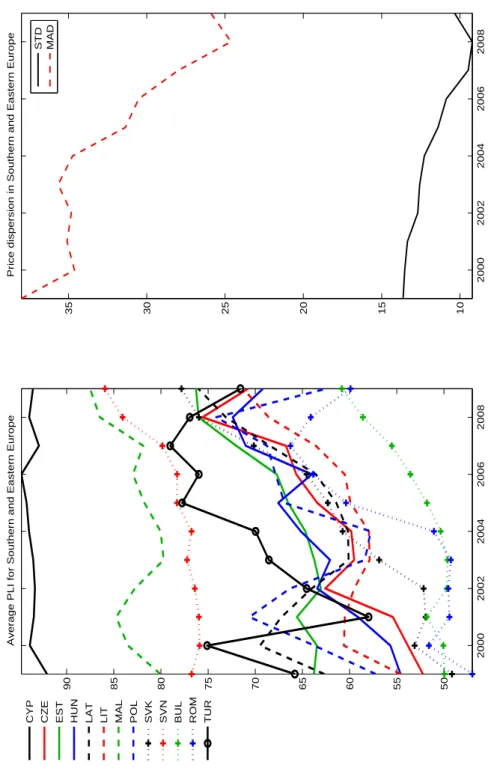

Likewise, real GDP per per capita for the Eastern and Southern European countries is far below the EU average, as is the real exchange rate for these countries, and again the deviation of the relative price from the EU average is significantly smaller than for GDP per capita. inhabitant. Furthermore, both across countries and over time, there is a less than proportional response of the real exchange rate to movements in relative GDP. We see a close correlation, apart from outliers due to Luxembourg, which from figure 10 has a relative GDP per per capita that is significantly out of proportion to its real exchange rate13.

The figure also confirms the above finding that the real exchange rate unconditionally increases by less than proportional to relative GDP.

5 Structural Determinants of Real Exchange Rates

A one percent increase in relative GDP per capita is associated with a 0.35 percent rise in the real exchange rate. In the aggregate, therefore, the relationship between real exchange rates and real GDP per capita is very close. But real exchange rates in the aggregate mask considerable heterogeneity among different consumer goods categories.

More than ever, the key message of mean regressions prevails; the relationship between relative GDP and the real exchange rate is essentially the same in the time-series and cross-sectional dimensions.

6 A Simple General Equilibrium Model

The model

We can then compare the simulated path for the real exchange rate with that of the historical sample path, for each country. Our results above indicate an empirical elasticity of the real exchange rate to relative GDP per capita of 0.35 to 0.4, both across countries and over time. The key aspect of the model calibration is to determine the relationship between growth in real GDP per capita and movements in the real exchange rate.

On the other hand, if b = 1 then the real exchange rate is constant (not necessarily equal to unity, unless a = 1 too), since YN and YX then move in relation to each other as relative GDP per capita (Y) moves. The estimates above suggest that the elasticity of the real exchange rate to relative GDP in the cross-section and time dimension is between 0.35 and 0.4. The figure illustrates the path of the home country's relative GDP and the real exchange rate.

The second panel of the figure illustrates the analogue of the empirical elasticity of the real exchange rate to relative GDP. The evaluation of the model depends on the closeness of the sampling path and the simulated real exchange rates. The model-generated real exchange rate for Switzerland is very close to that in the data.

In particular, Norway's model-generated real exchange rate is very close to the historical sample. On the other hand, the model-generated real exchange rate for some European countries (e.g. France and Germany) is somewhat smaller than the historical sample.

7 Conclusions

It follows that the real exchange rates implied by the model can be adjusted by the difference between the effective VAT rate of each country and the European average. The adjustment affects only the levels, but not the rate of change, of the simulated real exchange rates. The main difference is that the real exchange rates of the Scandinavian countries no longer look so unusual compared to the model-generated real rates.

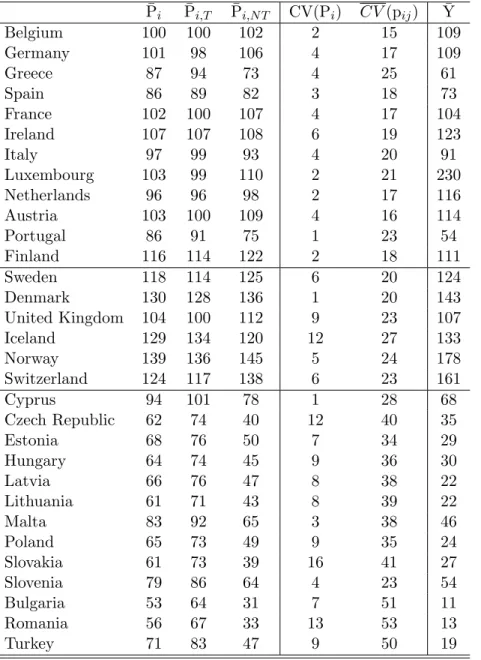

Among the floating exchange rate countries, Switzerland's real exchange rate now looks somewhat abnormal, as Switzerland has a relatively low VAT rate. Overall, we can conclude that the incorporation of differential VAT rates in the model does not significantly change the good performance of the model in relation to the pattern of real exchange rates in Europe. The main advantage of the dataset is that it allows for an explicit comparison of price levels across countries, allowing us to explore the cross-sectional and time-series characteristics of real exchange rates.

While real exchange rates continue to deviate from PPP, we find that, both cross-sectionally and in time series, relative GDP per capita can explain a substantial part of the variation in European real exchange rates, for both eurozone countries as floating exchange rates. exchange rate countries and the emerging countries of Eastern Europe. In addition, real exchange rate movements are strongly positive as the relative price of non-traded goods rises. We used a simple general equilibrium model of the real exchange rate, in which real exchange rates were driven by different growth rates in traded and non-traded sectors.

When we simulate the model to fit the past sample path of relative GDP for each country in our sample, we find that for most countries the implied path of the real exchange rate is remarkably close to the sample real exchange rate, both in terms of level and rate of change over time. Although the mechanism driving real exchange rates in our model is parsimonious, the success of the model in accounting for real exchange rate levels and trends suggests that there is good potential for further research aimed at uncovering the peculiarities of the real exchange rate. determination in European countries.

This paper has investigated the characteristics of European real exchange rates at both an aggregated and disaggregated level, using a new data set on prices of a large number of consumer goods for a broad sample of European countries over a thirteen-year period. Our results showed that there is a significant deviation from the PPP at both the aggregate and disaggregated levels, both in the euro area countries and the non-euro countries. Moreover, with the exception of the emerging Eastern European countries, there is little in the data to suggest that deviations from PPP decline over time.

Distribution costs and real exchange rate dynamics during exchange rate based stabilisations. Journal of Monetary Economics, September 2003.

Not for publication

Appendix to

What Determines European Real Exchange Rates?”

- Good description

- Examples

- PPP deviations at the good level

- Monthly frequency

- Incorporating VAT differentials

- Model with endogenous capital accumulation

- GDP growth and relative outputs of traded and non-traded goods

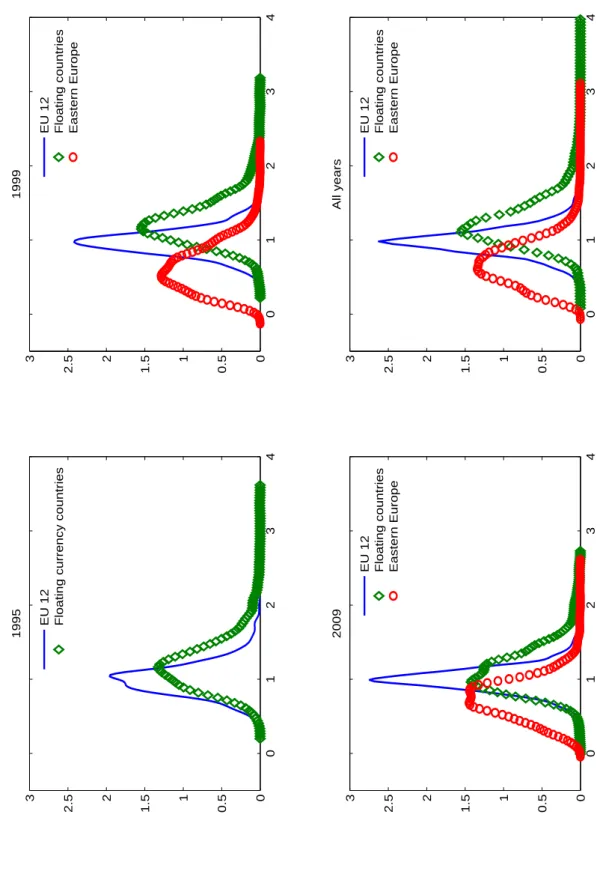

For the group of Central European countries (Belgium, Germany, the Netherlands, France and Austria), there is an even distribution above and below PPP across all goods. For Scandinavian countries, most goods are above PPP, while for Southern European countries, most goods are below PPP. The figures show that the general features of real exchange rates in annual series carry over to monthly data, but these measures of real exchange rates exhibit significantly more volatility.

An interesting feature of the monthly data is the more obvious tendency for the price spread across countries to fall in the period after 2000 for the countries in the euro area. Similarly, the results remain largely unchanged when model results are compared to expenditure-weighted real exchange rates in the data (Figures A9 - A11). Let the production functions for traded and non-traded goods be given by YT t=AT tKT tαL1T t−α , YN t =AN tKN tγ L1N t−γ.

Then the growth rate of PN is t gp = 1g−Tα − 1g−Nγ , and the growth rates of the output of traded and non-traded goods are 1g−Tα and 1g−Nγ, respectively. The real exchange rate will increase over time if the traded goods sector grows faster than the non-traded goods sector. If exogenous productivity grows at the same rate in every sector, then a sufficient condition for the traded goods sector to grow faster than the non-traded sector is that α > γ, i.e.

The theoretical model assumes that GDP growth is associated with faster growth of traded goods compared to non-traded goods. The production of traded goods is the real sectoral production of agriculture, fisheries, industry and construction in national currency (sectors A, B, C, D, E and F). The production of non-market goods is the real production of wholesale and retail trade, repairs, hotels and restaurants, transport, financial intermediation, real estate and other service activities in the national currency (sectors G, H, I, J, K, L, M, N, O and P).

As with our measure of relative GDP, sectoral output of traded to non-traded goods is expressed relative to the EU15 average.