Every fishery visited targets southern lobster (Jasus edwardsii) and the delegation noted that common to all these management systems is the use of Total Allowable Commercial Catch (TACC) to limit the industry's annual catch. For example, there are currently different maximum size limits in the northern and southern fishing regions. As a result, in 2003 the Western Australian Government committed to a review of the management arrangements for the rock lobster fishery on the West Coast.

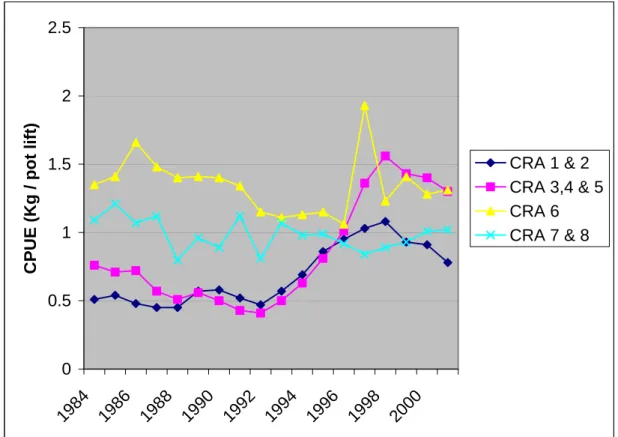

Rather, the amount contributed each year by the industry is a fixed percentage of the deemed value of all lobster quotas. However, since the introduction of the QMS, there has been a significant increase in the value of the quota entitlement and the price for leasing quota. Under the QMS, some of the fisheries (CRA and 5) experienced significant improvements in CPU, while the remaining fisheries essentially maintained pre-QMS CPU (CRA 6, 7 and 8), with these values already being significantly high .

However, the fact that the New Zealand SMC was in force and that there are no closed seasons within this management system enabled the industry to take full advantage of the high prices offered during the autumn-winter. The division of New Zealand's fisheries into 10 separate management areas limits the ability of operators to be highly mobile and roam over large areas.

Tasmania

Reduce the catch to a sustainable level by rebuilding the biomass of the rock lobster resource over time; and. These goals came about because the government and the majority of the industry agreed that there is an overcapacity problem in the fishery which leads to the overexploitation of the resource and limits the economic viability of the industry as a whole. In Tasmania, the management system relies mainly on advice from the Tasmanian Aquaculture and Fisheries Institute (TAFI) about the health or sustainability of the resource.

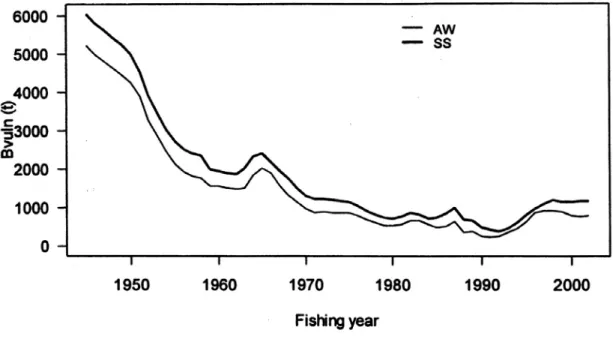

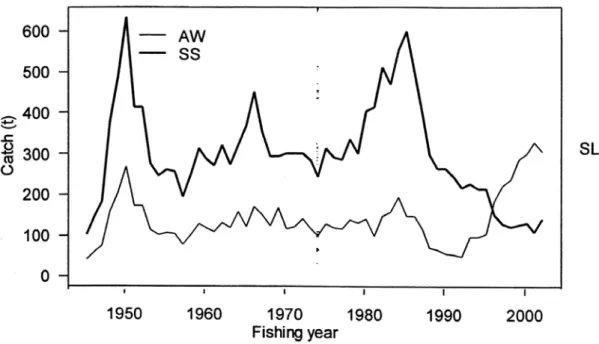

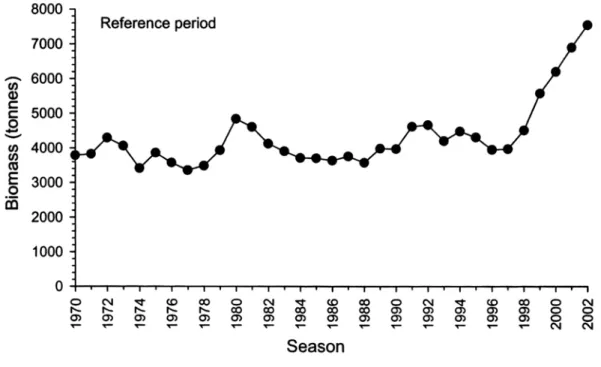

To illustrate the effect on resource sustainability in Tasmania attributed to the QMS, Figure 11 shows the legal biomass size, number of pots lifted (effort) and catch per unit effort (CPUE) for the fishery for the period 1947-2001. It was noted that there are aspects of the assessment that warrant further discussion and research (Gardner 2004). However, the pace at which this restructuring took place, both in terms of license and vessel numbers, increased with the introduction of the QMS.

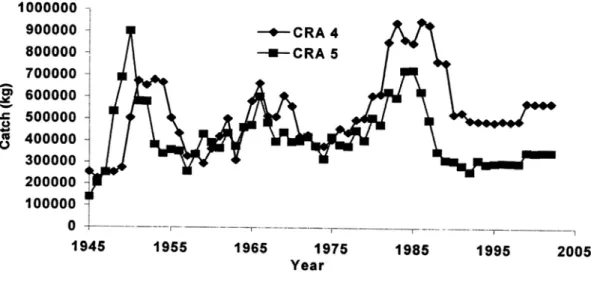

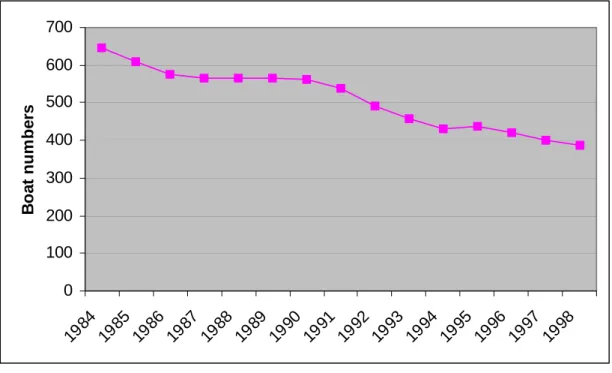

Under the QMS, it has been reported by both industry and fisheries managers that there is increased absentee ownership and therefore less conservation of the resource. It is clear from Figure 12 that the Tasmanian QMS facilitated an accelerated restructuring of the industry - something that was intended. The removal of 70 boats (about 22 percent of the fleet) in a two-year period represents a significant adjustment, but the majority of those in the fishery were always participants before the introduction of the QMS.

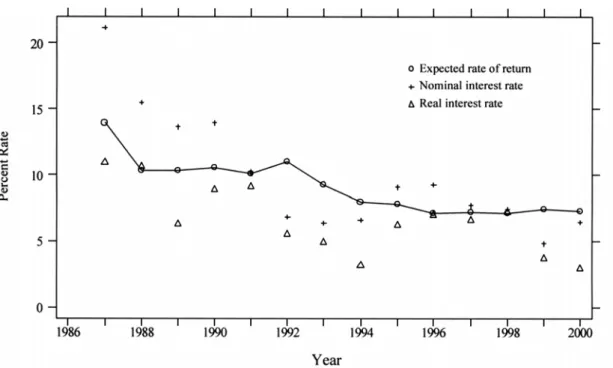

Shortly after the QMS was introduced, a number of factories in some of the more remote locations (eg Strahan) closed. Prior to the introduction of the QMS, there had been relatively modest growth in the value of a Tasmanian rock lobster claim. Since the introduction of the QMS, these trends have continued, although not at the spectacular rate of change observed for fleet restructuring.

Both the fishing and processing sectors of the Tasmanian industry state that under the QMS, decisions about when to fish are increasingly based on price.

South Australia

Restructuring was not an explicit objective in the northern zone, but improving the economic performance of the fisheries was. Figures 19a and 19b illustrate, for some of the performance indicators, the improvement in fishery health in the South Zone since the introduction of the QMS in 1993. At first glance, the success of the QMS in the South Zone is a bit puzzling given that the TACC is not significantly different from the reported catch under the pre-existing input management system.

The rapid recovery was also aided by the southern zone's environmental features that allow for regular recruitment to high-density lobster habitats. Figures 20a and 20b illustrate, for a number of performance indicators, the decline in fishery health in the northern zone under the input management system. For example, in the Southern Zone, maximum holding restrictions and limits on the transferability of rights are intended to limit aggregation and investment from outside the fishery.

It has already been stated that there has been very little change in boat numbers in the southern zone either before or after the introduction of the QMS, compared to the significant drop in vessel numbers in the northern zone since the introduction of a QMS. In addition to the regulatory controls, it has also been suggested that the community structure of the small coastal towns that host the southern zone fishery exerts significant social forces that resist, or at least discourage, investment in the fishery from "outsiders" (Morgan 1999). The strong performance of the southern zone since the introduction of QMS is clearly seen in Figure 23.

Throughout much of the 1990s, the respective values of eligibility in the Northern and Southern Zones were largely the same, despite the Southern Zone moving to a QMS in 1993, while the Northern Zone remained with input controls. This timing coincides closely with the knowledge that the status of the southern fishery was very good and that the status of the northern zone was relatively poor. In South Australia, it is therefore likely that the health of the resource is the largest determinant of entitlement value.

One of the most obvious economic costs of SMC in the southern area is the underutilization of capital. Despite these apparent limitations, current participants in the southern zone fishery are staunch defenders of the existing management system, and it is the sociological benefits currently being realized that are central to this defense. The southern zone season lasts from October 1 to April 30 of the following year, while the northern zone season begins on November 1 and ends on May 31 of the following year.

Findings

The delegation noted that the absence or presence of these measures affects the behavior of the industry, both in relation to investment and fishing strategy decisions. This report groups its analysis of the respective management systems into two categories – fisheries management and industry dynamics and fishing patterns. For each of the fisheries observed, the decision to move to a QMS was based primarily on the need to address sustainability issues.

Following the implementation of a quality management system, each of the fisheries experienced significant improvements in key sustainability indicators. This is true even though the TACC in each fishery has changed very little in percentage terms since it was first introduced. Noting that the QMS has been largely successful in the management of these spiny lobster fisheries, it is important to note that the failure of the previous management systems cannot be solely attributed to the fact that they were input-managed.

The first point of interest is that for three of the four fisheries it was recognized, explicitly or implicitly, that before entering the SMC there was overcapacity and that the new system should facilitate fleet restructuring. The key elements present for each fishery where there has been a significant level of restructuring are: (i) a TACC that limits catch and in doing so creates or exacerbates fleet overcapacity – the greater the imbalance, the more great is the force for restructuring; and (ii) a system that allows a market for units of the right to operate relatively freely. The price for this lifestyle is a relatively limited quota market, and the risk is that the fundamentals underpinning the fishing economy change as regulation hampers the industry's ability to adapt in order to maintain profitability.

It is also clear that the improved health of the fisheries under QMS and the resulting increase in catch rates has improved profitability and added confidence to the market. Across all fisheries, it is clear that the profitability of fishing is less for a fisher who leases a right, as opposed to an owner/operator. The growing presence of charter fishers (quota catchers) in these fisheries has both fishery managers and industry leaders concerned that those employed to catch the lobster do not have a stake in the fishery and are therefore not acting as stewards of the resource.

The development of the Chinese live southern rock lobster market in the 1990s resulted in very high prices being realized during the southern hemisphere winter.

Bibliography

Oct 06

Objective analysis of management scenarios

By establishing appropriate indicators, develop a conceptual model to predict the behavior of the industry under the different management options and therefore the impact of the expected behavior on existing host communities. This study period will take place over a period of 12 months with the aim of releasing papers around May 2005.

Communicate analysis of management scenarios with stakeholders With the various studies complete and published the second phase would commence

RLIAC prepare advice for Government

12 Report of the Rock Lobster Industry Advisory Committee to the Honorable Minister for Fisheries 24 September 1987. 82 The Impact of the New Management Package on Small-scale Operators in the Western Rock Lobster Fishery R. 103 Future Management of the Water Charter Industry in Western Australia Working Group of Fishing Tour Operators (September 1997 ).

123 Future Directions for the Rock Lobster Industry Advisory Committee and the Managed Western Lobster Fishery. A discussion paper prepared by Kevin Donohue on behalf of the Rock Lobster Industry Advisory Committee. 186 West Coast Lobster Fishery Management - Stakeholder Advice on Resource Sustainability Issues.