With humble honor and respect, I submit my internship report on "The Effects of Default Loan on Bank Profitability in Bangladesh". As per partial completion of the requirements for the BBA degree, this internship was carried out under your supervision. This report is an integral part of our academic courses in completing the BBA program which gave me the opportunity to get an insight into the core part of the subject.

I hope this report reflects the contemporary financial issues facing organizations in our country. While completing the report, I have tried my best to combine all my knowledge and provide all available details and also tried to avoid making the report unnecessarily long. I certify that this project report titled “Effects of Non-performing Loan on Bank Profitability in Bangladesh” is the bona fide work of Abdur Rakib Chowdhury who conducted the study under my supervision.

At the outset I want to express my deep gratitude to the Almighty, the Most Merciful for his kindness in giving me the opportunity to complete this report successfully. Shahbub Alam, Lecturer, Department of Business Administration, Sonargaon University (SU) for his guidance, suggestions and encouragement for the preparation of this report. In conclusion, I am grateful to all the respected teachers of Bachelor of Business Administration for the inspiration, continuous help during these years.

To become a developed country, the banking sector needs special reforms to control defaults (non-performing loans).

Chapter: 01 Introduction

BACKGROUND OF THE STUDY

The banking sector of Bangladesh has been going through tough times for the past few years. There is no other option than to reduce the outstanding loan in case of stability in banking. Lack of proper supervision and absence of good governance has resulted in an appalling culture of non-performing loans in Bangladeshi banking.

According to the BB report, “the non-performing loan ratio stood at 8.1% in December 2020, compared to a ratio of 8.9% in the previous quarter, despite close monitoring by the central bank. Nevertheless, some adverse contributing factors still have not disappeared from the banking operations and are adversely affecting the overall credit performance of the commercial banking sector of Bangladesh. Due to the satisfactory level of good governance practices, the economy of Bangladesh has played a very promising role in the past few years compared to other neighboring countries in the South Asian region.

It should be noted here that the present growth of financial intermediation is a reflection of the positive and healthy trend of the commercial banking sector of Bangladesh. Private commercial banks in Bangladesh have emerged as the most potential business sector in the last few decades.

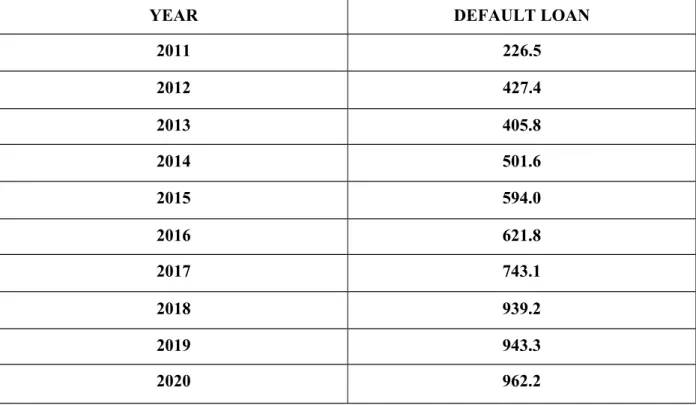

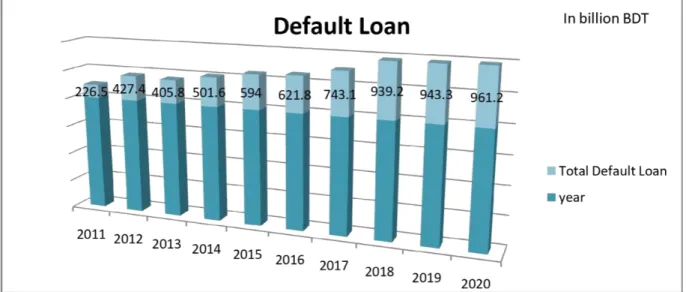

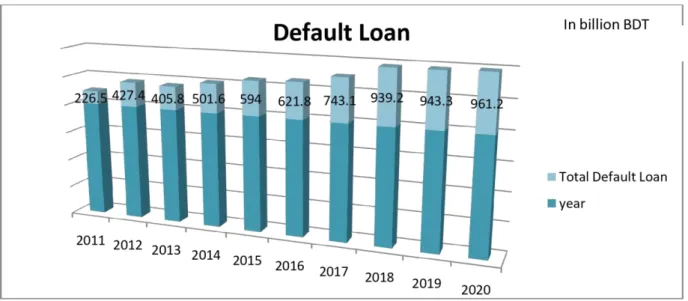

THE REAL PICTURE OF DEFAULT LOAN

Bank

DEFAULT LOAN

NON PERFORMING LOAN

BANK PROFITABILITY

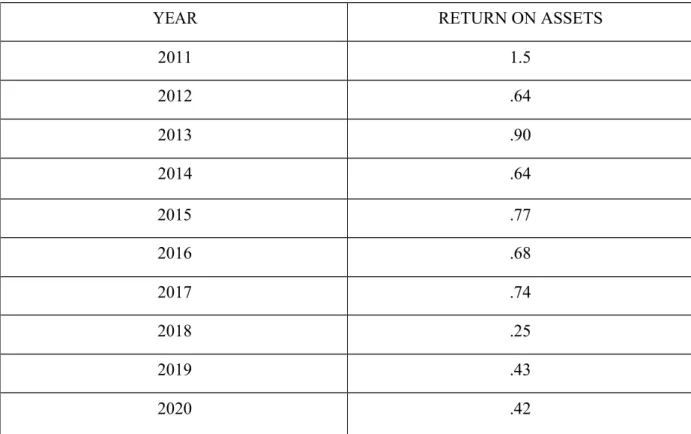

Return on Assets Equation

Bad loans arise when the borrower no longer makes payments in accordance with the terms of the loan. At the end of June 2021, the total outstanding loans of the banking sector was Tk 112,425 crore, which is 11.69 percent of the total outstanding loans, according to WB data. In the World Bank's latest 'Global Economic Prospects' report, Bangladesh's non-performing loan ratio was estimated at 11.4 percent for 2019.

Recently, the Government of India has approved the law namely "The Economic Offenders Bill 2018 to prevent non-performing loans". The choice of sampling period was based on the availability of time series data on new volumes of default loans from banks as well as the availability of ROA. Secondary data on banks' non-performing loan volumes, default loans and bank return on assets were obtained from administrative records and documentation, while data on default loans were obtained from Bangladesh Bank for a period of ten years between 2011 and 2020.

Using this method, the researcher was able to obtain information about the banks' perceptions of the effects of a defaulted loan on the bank's profitability. The unknown variable that is estimated against the objective sought by the research questions is the amount of outstanding loan. The coefficient of determination was also used to determine the prevalence or strength of associations between two variables X and Y.

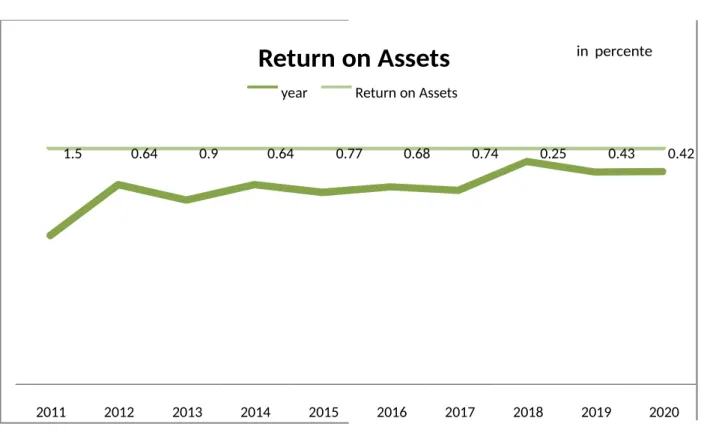

The variations of the Y values in a data set around the fitted regression line and their own mean. Relationship between loan default and Bangladesh banks' return on assets (ROA) from the year 2011 to 2020. The annual return on assets for the period is regressed against the bank's loan default.

The study further indicates that loan defaults have a strong effect on the bank's profitability, as loan defaults increase; Strong effect is exerted on Banks' profitability. The amount of non-performing loans in the country's banking system increased by Tk 14,990 crore in 2021, despite regulatory forbearance. According to Bangladesh Bank data released on Wednesday, the amount of non-performing loans in the country's banks increased to Tk 1,03,274 crore at the end of December 2021 from Tk 88,284 crore a year ago. as regulatory failure categorized a large volume of uncollected loans as unclassified.

The amount of non-performing loans in private commercial banks represents 49.89 percent of total non-performing loans, while the ratio was 45.21 percent a year ago. The central bank should prevent banks from issuing dividends or force them to issue lower dividends to improve banks' financial strength, he said. He also sees the existing return on capital and bank assets as very negligible, preventing the strengthening of the banks' financial base. The government after the outbreak of the coronavirus announced a one-year moratorium facility for the borrower in 2020. Before the economic consequences caused by the coronavirus, The NPL ratio in the country's banking sector stood at 11.99 percent or Tk 1,16,288 crore of outstanding loans at the end of September 2019, when banks implemented a special rescheduling policy, allowing defaulters to fix their loans. defaulters by paying a paltry 2 percent of their outstanding loans. Subsequently, the non-performing loans in the country's banking sector gradually declined. Adding the written-off loans amounting to Tk 43,270 and the loans amounting to Tk 80,000, the recovery of which remained in abeyance. in court proceedings, the total of defaulted loans stands at Tk 2,26,544 crore at the end of December 2021.

A proper NPL workout should be determined for each bank based on international factors.