Background of the study

Background of the organization

- Brief profile of the firm

- Partners and their area of specialization

- Vision and mission

Objective of the study

Scope of the study

Limitations of the study

Sources and methods of collecting information

Report Preview

Introduction

The possibility that the auditor may issue an incorrect auditor's report because of significant errors identified in the financial statements. The primary purpose of conducting audits is to appropriately mitigate the possibility of inaccuracies and fraudulent activity in the organization's financial records.

Significance of audit and audit risk

The audit risk assessment helps auditors provide an accurate assessment of the company's financial statements. The auditors are not able to examine all of the company's transactions, and the audit risk assessment therefore increases attention to high-risk areas.

Types of audits and audit risks

- Different types of audits

- Different types of audit risks

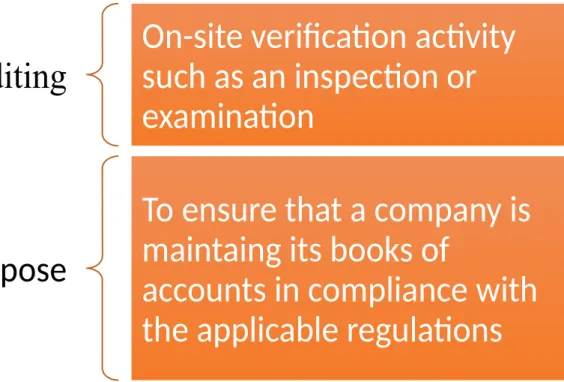

External audits are conducted by third-party organizations and entities that offer an unbiased perspective that internal auditors may not have. External audits are conducted to detect material inaccuracies or errors in a company's financial statements. External audits play a key role in providing various stakeholders with the assurance needed to make informed decisions about the audited company.

The IRS conducts audits, also known as tax audits or government audits, on businesses to verify that their financial information has been reported according to tax regulations. During office audits, the IRS holds extensive face-to-face meetings to examine your tax filings and examine all pertinent details to validate the accuracy of your financial documentation. Conducting on-site audits at your place of business is comparable to conducting audits in an office environment, but the IRS representatives will also evaluate your facility and the activities that take place there.

History of auditing

Control risk: Control risk is a type of risk that there is a chance to manipulate or misjudge the figures in the financial statements. So there is a control risk involved here due to management inefficiency. The intern has audited another company named "Khaja Plywood Industries Ltd." The company has shown their inventory balance of 2431874 Taka in their statement of financial position.

He also noticed that the cash balance in the cash register is shown as 2483831 Taka in the notes to the financial statements. In the notes to the financial statements, the company showed a cash balance of 1613066 Taka. One element of audit risk is inherent risk, as mentioned in the introduction to this work.

Introduction

In this chapter, the author basically discussed the methodology of research of his research report. He discussed regarding the philosophy of research, approach of research, strategy of research, the data collection process, the data analysis process and authenticity &.

Research philosophy

- Positivist, Interpretivist, Pragmatic and Realistic

- Justification of choosing Interpretivist Philosophy

The actuality is determined by current circumstances and is not influenced by an unreal or split mind. Realist research philosophy: The realist approach to research philosophy draws from both positivist and interpretivist principles. The foundation of the realist research philosophy rests on certain assumptions that recognize the subjective nature of human perception.

Since it is not a report where survey was used or it is not a scientific research report, therefore positivist philosophy cannot be used. The author has studied various articles available on the internet and discussed with his senior supervisors to understand the audit risk assessments.

Research approaches

- Qualitative, quantitative and mixed approaches

- Justification of choosing mixed approach

Conducting quantitative research on these brands can lead to significant savings in time, effort and resources. Quantitative research is mainly applied in disciplines such as natural and social sciences, education and management. The research approach should generally allow the manipulation of only one variable at a time to avoid complexity in the statistical analysis.

Mixed Approach: Mixed method research involves integrating quantitative and qualitative methodologies to incorporate data from both types into a unified study. By using mixed method research, researchers can exploit the synergy and effectiveness inherent in the combination of quantitative and qualitative research methods. The author used some case studies related to the assigned topic and he used some quantitative data in the analysis section.

Research strategy

Data collection method

Data analysis method

Reliability and validity

If the management control system is not strong enough, there is a possibility of this type of risk occurring. Chartered Accountants is one of the registered CA firms of ICAB (Institute of Chartered Accountants of Bangladesh). The author believes that the numerical evaluation is useful, especially given the satisfactory accuracy of the risk assessment.

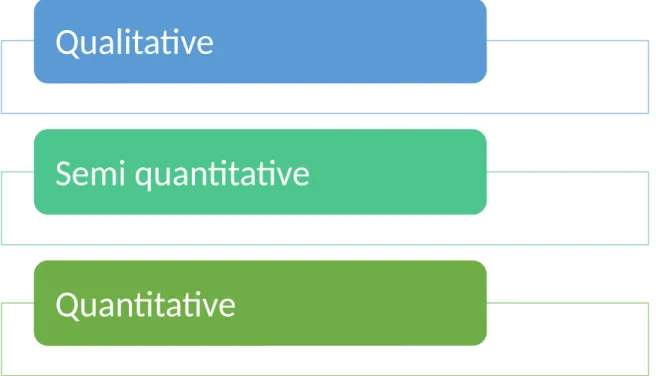

After selecting the sample size, the items will be removed for the auditor to consider. Due to the interdependence of the three components of audit risk, there are still many different opinions about the appropriate valuation methodology. The audit risk score can be quantified in terms of percentage or quality (low, moderate and high).

Working experience

During the first few days of his internship, he has come up with the idea that accountants basically categorize their required documents into three segments: Current File, Permanent File, and Working File. Current file contains the documents that are relevant for the current year, permanent file contains the documents that are necessary for the company in the long term, and working files contain documents that are immediately necessary for an accountant to perform a specific task. He has visited a company as a "customer visitor", where he has gained the experience of a company environment.

Theoretical framework

To prevent this type of risk, an auditor must have an in-depth knowledge of his/her client's business and the nature of the company. One of the important reasons for giving a qualified opinion is the failure to prepare financial statements in accordance with the PPPK. To summarize, it can be said that when auditors cannot have sufficient access to company information, they may issue an adverse opinion.

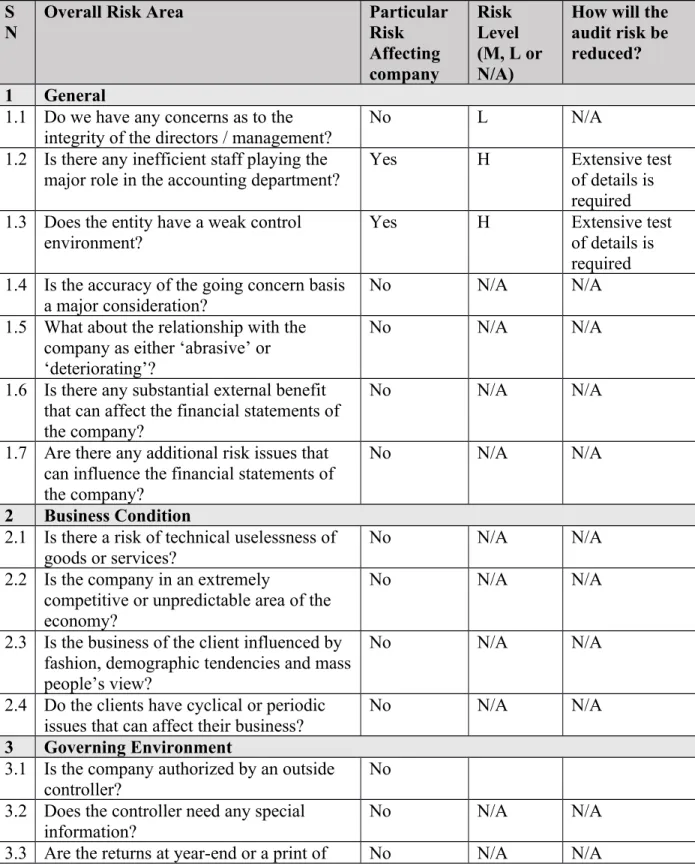

This is the percentage of the population that the auditor is willing to accept, while also using the estimated control risk and the estimated amount of operational financial errors decided during planning. Yes H An extensive test of details is required 1.3 Does the entity have weak control. 1.4 Is punctuality the basis of a functioning company. If we focus on the practical side of the issue, we can see that most current applications follow the same model of international standards.

Introduction

Because of circumstances like these, this action is often the most difficult in the risk management process. Mathematical tools generally estimate the risk that can provide a time precision and certainty unfounded; events that are prospects for one person or entity (cost savings) may be a danger to others (lowering earnings). The benefits of the risk assessment segment can be seen in: the ability to compare current risk levels with past statistics or risk levels in the field; the ability to aggregate risk across multiple activities to calculate total risk; the level of knowledge of ambiguity relevant with outcomes tracked; and whether decisions must be made after there is a risk.

When the annual accounts contain significant misinformation, there is an audit risk that the auditor declares an incorrect audit opinion. Control risk is the risk that the entity's internal controls will not prevent, detect, and correct a misstatement that may occur in a claim about a class of transaction, account balance, or disclosure, and that may be material, either individually or aggregated with other misstatements. Detection risk is the possibility that an existing and potentially material misstatement will not be detected by the techniques the auditor uses to reduce audit risk to an acceptable level, either alone or in combination with other misstatements.

Analysis on audit risk assessment

Following regions corresponding to each type of account, as well as additional aspects of the audit such as balances and accounts, interim financial statements and year-end records, all carry specific inherent risks. These components will be based on numerical or non-numerical approximations to be representative of the total population they represent. Tolerable error approved by the auditor should also be considered at this point.

As mentioned earlier, audit risk is typically estimated at 5% and is combined with inherent risk and control risk to estimate the probability of detection. Its objective is to establish a low level of risk while establishing a balance between audit risk and cost. The approach is based on the false assumption that the three elements of audit risk are independent of each other.

Analysis on audit risk assessment for a particular company

0 management during the preparation of the income statement rather than being calculated by others as part of the general accounting procedure. Is there a pattern whereby accounting judgments and estimates made when finalizing the accounts are all skewed in the direction management wants. Were there any completed contracts or transactions, particularly where this was close to the year-end, where.

Conclusion

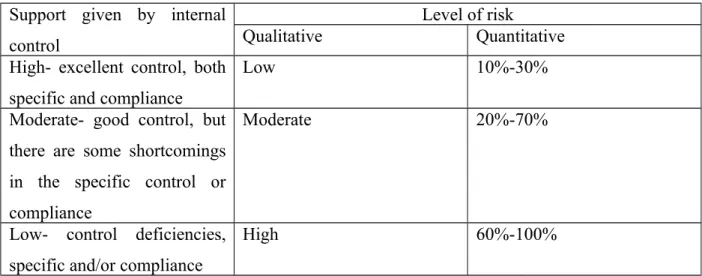

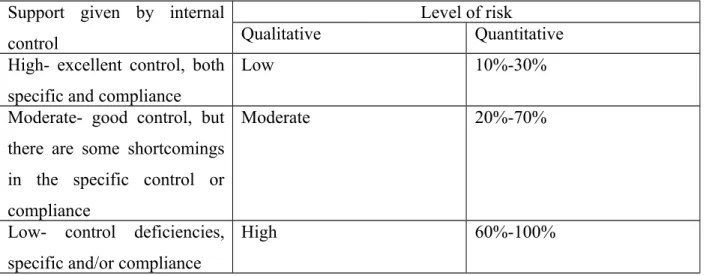

If the management is excellent, it can be seen that the risk level is lower and the percentage range is 10%-30%. If management is deficient, the risk level is higher and the percentage range is 60%-100%. The author has prepared the entire report with the topic "Perspective on audit risk assessment for Bokhteyar Humayun & Co.

In order for the audit process to be effective and accurate, it is necessary to conduct an effective audit risk assessment. He has also suggested how effectively his firm can conduct an audit risk assessment. The future researchers can investigate the importance of audit risk assessment in detail how it can have a positive impact on an audit procedure.

Findings

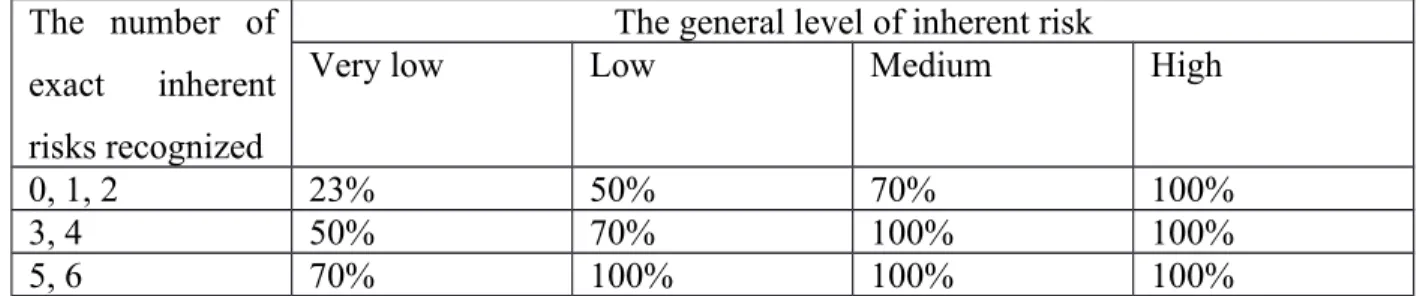

The level of risk was found to increase as the number of identified specific inherent risks increased. If the management system is moderate, the risk level is also moderate and the percentage interval is 20%-70%. The author also assessed the detection risk in table 5-4. It was found that if the certainty level is high, then the risk level is low; if the certainty level is moderate, then the risk level is also moderate and if the certainty level is zero, then the risk level is high.

It has indicated for different degrees of risk what sample size and range should be used to check transactions. If the control risk estimate is low, then the sample size should be lower, and if the control risk estimate is high, then the sample size should be higher. If the acceptable margin of error is small, then the sample size should be higher, and if the margin of error is high, then the sample size should be lower.

Recommendations