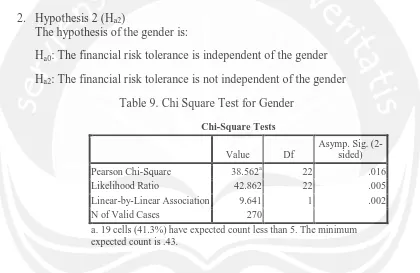

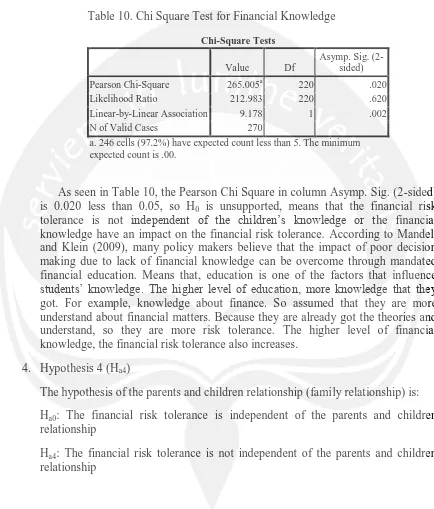

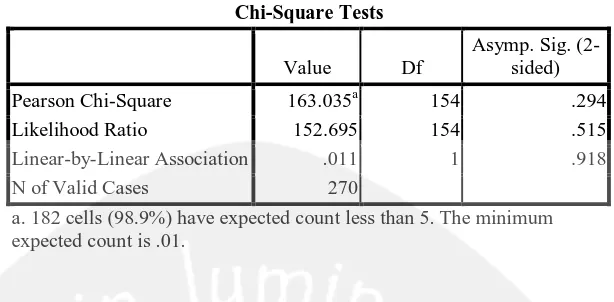

THE IMPACT OF FAMILY RELATIONSHIP, GENDER, AND FINANCIAL KNOWLEDGE ON FINANCIAL RISK TOLERANCE.

Teks penuh

Gambar

Dokumen terkait

The factor that is thought to cause the moderating effect of self-monitoring that does not significantly affect the relationship between financial literacy, herding behavior, and risk

RELATIONSHIP BETWEEN FAMILY KNOWLEDGE ABOUT IRON CHELATION AND ADHERENCE TO GIVING IRON CHELATION IN CHILDREN WITH THALASSEMIA AT RSCM KIARA 1Agung Setiyadi, 2Intan Parulian,

Mediation and Moderated Mediation in the Relationship among Environmental Factors, Health-Related Knowledge, Attitude, Practices, Age and Gender Edwin Balila, Ivonne Panjaitan and Dina

Regarding the above research, whether the CEOs’ financial knowledge and managerial ability have a negative and significant effect on the unsystematic risk of companies listed on the

That's why the study aims to find out whether board gender diversity really matters in the corporate board and can be valuable for predicting financial distress risk in the

Table 4: The relationship between family knowledge and medication adherence in outpatient schizophrenia patients Family knowledge Compliance take medication p High Moderate Low n %

This study will focus on proving the relationship between financial literacy and risk tolerance as a moderating variable on the behavior of using digital financial services, especially

Relationship of profile characteristics of respondents with knowledge level of respondents on climate resilient agricultural technologies Profile characteristics Correlation