THE INFLUENCE OF REFORM ADMINISTRATION TAX AND EMOTIONAL

INTELLIGENCE TOWARD AWARENESS OF INDIVIDUAL TAXPAYERS

(AT SUB- SUB DISTRIC WEST PAMULANG)

THESIS

Submitted to Faculty of Economics and Business as Partial Requirement for Acquiring the

Bachelor Degree of Economics

By:

Wike Vidya Paramita

107082103606

DEPARTEMENT OF ACCOUNTING

INTERNATIONAL CLASS PROGRAM

FACULTY OF ECONOMICS AND BUSINESS

SYARIF HIDAYATULLAH STATE ISLAMIC UNIVERSITY

JAKARTA

CERTIFICATION OF TIIESIS EXAM SHEET

Today is Monday, June 20, zo11 has been conducted on student

thesis examination :

1.

Name2. Student Number

3.

Department4.

Thesis TitleDistrict West pamulang)

After careful observation and attention to appearance and

process,

it

was decidedthat the

above student passedrequirements

to

obtaina

Bachelorof

Economicsin

the Hidayatullah State lslam ic Unive rs ity Ja ka rta.Jakarta, June 20, 20L1

Prof. Dr. Abdul Hamid, MS

tD.19570617 198503 1 002

Rahmawati Dahyar, SE, MM

rD. 197708142A0604 2 003

Prof. Dr. Azzam Jasin, MBA

Prof. Dr. Ahmad Rodoni rD. 1 9690203 2001 12 1 003

Wike Vidya Paramita 107082103606 Accounting

The lnfluence of Reform Administration Tax and Emotional

lntelligence toward Awareness

of

lndividual Taxpayer (at sub- subcapabilities relevant for thesis examination and

the

thesis was accepted as one of Facultyof

Economics and Business SyarifSecretarv /

lJ

.M,

Examiner ExpertChoirulAnwar, MBA, MAFiS, CpA

SHEET STATEMENT

AUTH ENTICITY SCIENTI FIC WORKS

Signatures below: Name

Students Number

Faculty Department

Wike Vidya Paramita 107082103606

Economics and Businesss Accounting

Hereby declare that in the writing of this thesis, l;

1.

Not use other people's ideas without being able to develop and accountable2.

Do not do plagiarism of other people,s work manuscrlpt3.

Do not use other people's work without mentioning the original source or without theowner'$ permission

4,

Do not manipulate and falsify the data5.

Own work and able to work responsible for this worklf in the future there is a demand from the other side of my work, and have been accountably proved, was indeed found evidence that I have violated the above statement, then i am ready to be sanctioned according to rules applicable in the Faculty of Economics and Business Syarif Hidayatullah State lslamic University Jakarta.

CURRICULUM VITAE

PERSONAL DATA

Name : Wike Vidya Paramit a

Gender : Female

Place/ Dat e of Birt h : Tangerang/ Nov, 25,1989

Nat ionalit y : Indonesian

M arit al St at us : Single

Religion : M oeslem

Address : Komp. Pamulang Permai 1 Blok B 11 no.9 West Pamulang- Sout h

Tangerang

i

ABSTRACT

This research to find out significant the reform administration tax and

emotional intelligence influenced awareness of individual taxpayers also to

reveal the level of awareness of taxpayers in the Sub- Sub district West

Pamulang. This research use Regression Multiple Linier. Sampling technique

is taken by the proportional random sampling area. Based on the result

regresion multiple linier that Reform Administration Tax has a positif and

significant on Awareness. Emotional Intelligence has a negative and

significant influence on Awareness. Significant Awareness various is 65, 0%

can be explained by all of independent. However the others 35, 0% are

explained by the other factors that are not calculated in this research.

ii

PREFACE

Bismillaahirrahmaanirrahiim

Assalamualaikum Wr.Wb

Praise be to God Almighty who always gives His grace and guidance and

blessings infinite, so I can finish this paper with the title "The Influence of Reform

Administration Tax and Emotional Intelligence toward the Awareness of Individual

TaxPayers (At Sub-Sub-District West Pamulang)" as one a prerequisite for

completing educational programs Strata Bachelor Level One (S-1) merger

Accounting Program at the Faculty of Economics and Business Syarif Hidayatullah

State Islamic University Jakarta. With the weaknesses that exist, the author will not

be fully realized apart from the mistakes and shortcomings. Therefore, the authors

deliver to apologize as much as possible when writing there are many shortcomings.

To complete this thesis, the author gets of many highly valuable assistance in

the form of moral and material from various parties with a single-minded. On this

occasion, with all humility there is no better word to convey the author, except Praise

and thanks are very sincere to:

1. Beloved family, mother, father and my sisters (Anne Destiany, SE, Wenny

Listyawati, SE) dear beloved who have provided moral and material assistance,

so I can finish this thesis.

2. Mr. Prof. Dr. Abdul Hamid, MS as the Dean of the Faculty of Economics,Syarif

Hidayatullah State Islamic University Jakarta.

3. Mr. Prof. Dr. Ahmad Rodoni as Vice Dean I of the Faculty of Economics,Syarif

Hidayatullah State Islamic University Jakarta and as Supervisor I who has

provided much direction and guidance and motivation to the author so I can finish

iii

4. Mr. Indo Yama Nasarudin, MAB as Vice Dean II of the Faculty of

Economics,Syarif Hidayatullah State Islamic University Jakarta.

5. Mrs. Rahmawati, SE, MM as Chairman of the Accounting Studies Program

Faculty of Economics Syarif Hidayatullah State Islamic University Jakarta.

6. Mr. Arief Mufraini, Lc,M.Si as Chairman Head of International Program Faculty

of Economics Syariff Hidayatullah State Islamic University Jakarta.

7. Mr. Choirul Anwar MBA, MAFiS, CPA as Supervisor II who has provided much

direction, guidance and motivate to the author. However I can finish this paper as

appropriate.

8. Mr. and Mrs. lecturer UIN International, which has provided guidance to the

author, and all staff employees of the Faculty of Economics Syariff Hidayatullah

State Islamic University Jakarta, which has provided assistance to the author.

9. Kak Sugih Waluyo, friends batch 4 and the International Accounting, Management

International UIN and colleagues that can not be mentioned one by one, which has

a lot of help in completing this thesis.

Finally, the author realizes that this thesis is far from perfect because the

author just ordinary people who did not escape from all sin. Therefore, suggestions

and constructive criticism is the author expected. Hopefully this paper can increase

knowledge for the benefit of all parties who read it.

Wassalamualaikum Wr.Wb.

Jakarta, May 2011

iv

BRIEF TABLE

NO

Explanation

Page

2.1 The differences in domestic taxpayers and foreign taxpayers…... ..23

2.2 SPT 1770...34

2.3 SPT 1770 S ... 34

3.1

Reliability Instrument Scale …...49

3.2

Research Operational Variable………...58

4.1

Respondents Characteristics……….. ...61

4.2

Validity Test: Reform Administration Tax ………...63

4.3

Validity Test: Emotional Intelligence ...………...64

4.4

Validity Test: Awareness …...65

4.5

Validity Statistics... 65

4.6 Reliability Statistic………...66

4.7

Autocorrelation Statistics ...69

4.8 Multicollinearity Statistics...71

4.9 Coefficient Determination ...72

4.10 F test ...73

v

BRIEF FIGURE

NO

Explanation

Page

2.1

Research Design ………...39

3.1

Theoretical Framework...59

4.1

Normality Test Result………...67

4.2

Histogram………...68

vi

BRIEF ATTACHMENT

ATTACHMENT

A

QUITIONAIRES

ATTACHMENT

B

DATA RESULT

ATTACHMENT

C

VALIDITY AND REABILITY TEST

ATTACHMENT

D

CLASSIC ASSUMPTION

vii

BRIEF CONTENTS

SUPERVISOR SHEET

ENDORSEMENT SHEET (COMPREHENSIVES EXAMS)

CERTIFICATION OF THESIS EXAM SHEET

SHEET STATEMENT (AUTHENTICITY SCIENTIFIC WORKS)

CURICULUM VITAE

ABSTRACT ………...i

PREFACE ………..ii

BRIEF TABLE ………..iv

BRIEF FIGURE ……….v

BRIEF ATTACHMENT ...………vi

BRIEF CONTENT ………...vii

CHAPTER I INTRODUCTION

A.

Background...1

B.

Research problem ………..7

C.

Research objectives ………...7

CHAPTER II THEORITICAL FRAMEWORK

A.

Literature Review...9

1. Definition of Tax ………...9

2. Tax Administration Reform... 13

3. Emotional Intelligence...16

4. Taxpayers Awareness...18

5. Income Tax...20

B. Previous research...36

C. Effect of the Reform Administration Tax toward

Awareness of Individual Taxpayer ...38

viii

E.

Hypothesis ………..40

CHAPTER III RESEARCH METHODOLOGY

A

.

Research Scope...41

B. Sampling Method...41

C. Data Collection Techniques ………....42

D. Analysis Method ...46

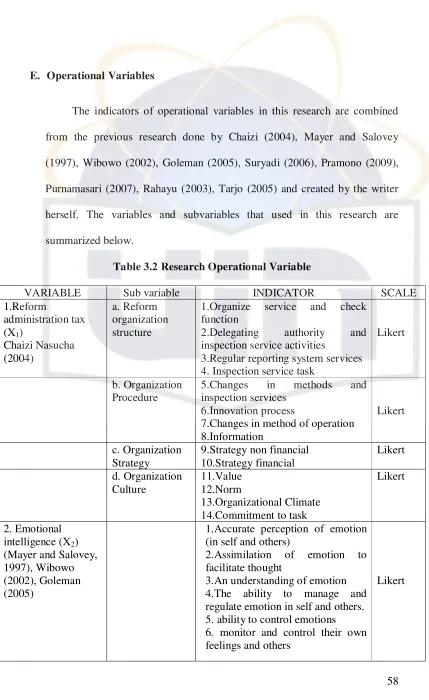

E. Operation Variables...58

F.

Theoretical Framework ...59

CHAPTER IV ANALYSIS

A.

General Description of Research Object ...60

B.

Analysis and Discussion ………...62

1.

Validity Test ...62

2.

Reliability Test...66

3.

Classic assumption ...67

4.

Hypothesis Test ………...72

C.

Interpretation ...75

CHAPTER V CONCLUSION

A.

Conclusion ………...79

B.

Implication ………...80

C.

Recommendation ………81

1 CHAPTER I

INTRODUCTION

A. Background

In an effort to finance the construction of the government is

absorbing the tax sector, though no less important income from various

sectors of other income. In the atmosphere of the country still covered by

remnants of the economic slump, the government carried the burden

which is currently very heavy. To finance the government's national

development can not only rely on external debt with interest rates that are

not minor or from natural resources are increasingly depleted oil and gas.

Hope the one that can be counted on to finance national development is

taxation revenue.

The Government has reformed tax. Actually it aims to support the

tax sector for better future. There are two significant leaps in tax reform.

First is the open of the large taxpayer’s office, followed by testing for

medium and small taxpayers with a modern tax system. At these large

taxpayers office, established an account representative which aims to

know all behavior, business scope, and all things related to view the

rights and obligations of taxpayers who monitored (knowing your

Taxpayer) and services to the taxpayer can be done completely on a

single table. Leap second is a proposal to change or amendment of tax

2 Act (Income Tax), and the Law on Value Added Tax (VAT). The point is

to change the tariff, subject, and subject to tax in order to competitive.

Anggito Abimanyu (2009)

With reform is launched in taxation that is marked with law (UU)

Number 16 year 2009 about number 5 year 2008 change four on law (UU)

number 6 year 1983 about general roles and tax roles; UU. Number 36

year 2008, about change three on law (UU) No.7 year 1983 about income

tax. Although perfect a reform tax policy, so that the result did not satisfy

if was not followed by reform administration tax. Nasucha (2004: 8).

Sophar Lumbantoruan (2005: 19) in Suryana (2010: 6) Administrative tax

is manner or procedure collection tax.

Indonesia's tax reform aimed at improving the efficiency of tax

collection in order to support the national revenue; improve services, legal

certainty and justice for the society to enhance competitiveness in the field

of investment to continue to support the development of small and

medium enterprises; adjust the demands of socio-economic development

of society and development in the field of information technology;

improve the balance between rights and obligations; simplify tax

administration procedures; improve the application of the principle of

self-assessment in an accountable and consistent and supportive business

climate towards a more conducive and competitive. Siti Resmi (2009: 20)

Chaizi Nasucha (2004) the government of Indonesia has done

3 procedures, namely change organization to tax inspection office be tax

service office. That change occurred because there was reform tax in

1983, namely change in system to official assessment be self assessment.

The change caused a major access for the taxpayer. One of them is

the decrease taxpayer compliance and awareness of his duty because

basically bad service. Besides that there is no transparan and simple

about procedure. Awareness to be abiding taxpayers is one of adherence

to the law. Compliance with tax payments, including rules against tax

law where the law mentioned indiscriminate taxation and a not exception

either escapes from anywhere or anyone all the same under the

provisions of the applicable tax law to avoid administrative sanctions that

would harm its own taxpayers.

In 2010, the number of registered taxpayers reached 15,911,576

people both personally and corporately, but only 14,101,933 are required

to submit tax return that the SPT is 8,202,309 taxpayers or by 58.16

percent compliance rate. It's still up significantly compared to the year

2008 which is only 33.08 percent and 54.15 percent in 2009. A total of

5,899,624 taxpayers reported individuals and entities do not meet their

obligations to obey a notification letter announcing the annual Income

Tax in 2010. Erlangga Djumena, kompas.com (May 20: 2011)

When compared with the percentage of taxes last year mandatory

compliance has decreased which in 2010 amounted to 61.91% while for

4 taxpayers who report an increase, which for 2010 individual taxpayer

who reports by 320,488 while the year 2011 amounting to 443,159

individual taxpayer. humaspajak.co.cc (May 20: 2011)

Indonesia tax revenue from Income Tax (Income Tax) of the

Personal in 2008 only amount 22.89%. While revenue from corporate

income tax to the realization of non-oil tax revenue reached 77.11%. In

2009 Indonesia tax revenue from Income Tax (Income Tax) of the

Personal is 61.28%. While revenue from corporate income tax to the

realization of non-oil tax revenue reached 38.72%. State revenue from

income taxes (Income Tax) private persons (OP) to the new 1-2010

semesters reached Rp 1.94 trillion or 45.22% of the target in APBNP

2010 amounted to Rp 4.29 trillion. Realization of revenue from corporate

income tax until the semester 1-2010 reached Rp 72.62 trillion or 57.34%

of target. Corporate income tax revenue in 2011 reached 70% of the total

tax revenue while only 30% of an individual. (Investor Daily Indonesia)

Still quite a lot of people are not aware of the obligations. They do

not realize to meet income tax obligations, even though income taxes

have been prepared in accordance with the law. This means a collective

agreement that must be obeyed.

Reduced awareness on taxpayers can be caused due to poor control

of their emotion. In a good emotion, the taxpayers can control his

emotions in the act for paying as aware and the taxpayer does not feel

5 intteligence. Goleman (2005) emotional intelligence is the ability to

motivate yourself and the ability to manage emotions well in ourselves

and in relationship to others. Meanwhile, according to Yunita (2005) in

Sukma Adiatma (2010) Emotional intelligence or Emotional Quotation

(EQ) includes the ability to express feelings, awareness and

understanding of the emotions and the ability to regulate and control it.

Mayer and Salovey (1995: 197) in

Elizabeth et al (2010)

defineEI as the capacity to process emotional information accurately and

efficiently, including that information relevant to the recognition,

construction, and regulation of emotion in oneself and others. According

to Morehouse (2007) in James Thomas Kunnanatt

(2008)

EI can alsoraise the level of individual and team performance. Perhaps due to an

enhanced ability to recognize and manage emotions and brace against

distracting emotions, EI skills connect both to individual cognitive-based

performance and team task performance skills.

So taxpayer’s emotional intelligence must be implemented well in

order to raise awareness of the taxpayer. Because the more control EI, the

better relationship between officer tax payer and taxpayers.

Consciousness to become taxpayers and meet all obligations that

need to be fostered in every heart that lived socializes taxpayers. Thus,

the wheels of government will run smoothly for the benefit of the

taxpayer's own and smooth the wheels of government will also launch

6 just and prosperous country within the scope of value - the value of

Pancasila and the 1945 Constitution. Each of the people and residents

should be aware that the obligation to individual income tax is not to

another party, but to streamline the way the wheels of government which

deals with all the interests of the people themselves. So a conscious is

needed a sacrifice and it is for its own interests from generation to

generation.

Therefore, the role of consciousness and forces the taxpayer is

required to participate in paying individual income tax, thereby

increasing state revenues. Therefore, with the change in taxation (reform

administration tax) and emotional intelligence are expected to taxpayers

awareness of self can arise from the taxpayer. So that taxpayers are aware

of obligations in terms of paying taxes, especially individual income tax.

So the writer was intrigued when a study was written under the title

"THE INFLUENCE OF REFORM ADMINISTRATION TAX AND

EMOTIONAL INTELLIGENCE TOWARD AWARENESS OF

INDIVIDUAL TAXPAYER (AT SUB- SUB DISTRICT WEST

7 B. Research problem

Based on the description above, the authors formulate the

problem as follows:

1. Do reform administration tax and emotional intelligence or partial

effect to awareness of individual taxpayers?

2. How is significant of awareness of individual taxpayers at the sub

sub-district west Pamulang?

C. Research objectives and Usefulness of research

1. Objective:

a. To find out significant the reform administration tax and emotional

intelligence influenced awareness of individual taxpayers.

b. To reveal the level of awareness of taxpayers in the Sub- Sub

district West Pamulang.

2. Usefulness of research

The uses of this research are:

a. As a regulation to achieve undergraduate in international

program, accounting, faculty economic and business, state Islamic

University Syarif Hidayatullah Jakarta.

b. As an application and applying knowledge that already get from

accounting merger and give the writer understanding about tax.

c. Theoretically, this research can have a function in knowledge

development especially in taxation subject. Beside that can be use

8 d. Taxpayers can obtain knowledge about efforts to increase taxes,

especially individual income tax.

e. As the input material which can be considered by the agency in

9 CHAPTER II

THEORITICAL FRAMEWORK

A. Literature Review

1. Definition of taxes

According to Rochmat Soemitro in Siti Resmi (2009: 1):

“Tax is cash contributions to the people of the State based on the law (Can be forced) to not get behind the timbale services (contra) Which is shown by direct cans and it is Used to paying the common expenses”.

According to N.J.Feldman in Siti Resmi (2009: 2):

“Taxes are imposed unilaterally by the achievements and outstanding to authorize (based on the stipulation of norms in general) without the there is a contraprestasi and is solely Used to cover general expenses”.

Under Article 1 of Law No.28 of 2007 is as follows:

“Tax is a compulsory contribution to the State which are payable by the individual or entity that is enforceable under the law by not getting benefits directly and used for the purposes of the State for maximum benefit and prosperity of the people”.

For Standard Chartered Bank can be taken fourth definitions that

conclusion:

a. Tax levied based on the power of the law and the role of exercise.

b. On paying the tax can not be showed there is an individual contra by

government.

c. Taxes levied by the State for both central and local government.

d. Taxes destined for government expenditure, which if there is still a

10 Tax has budgetary function meaning that tax is one source of

government revenue to finance both routine and development

expenditures. Taxes have regulatory functions, meaning that tax as a

means to regulate or doing government policy in the field of social and

economic as well as achieving certain objectives outside the financial

sector. Siti Resmi (2009: 3)

There are third kinds of taxes. It is classified Based on Class, its

collector Characteristics and Institutions. Based on class, tax is classified

Became two, namely Direct taxes have to be paid or borne solely by

taxpayers and cannot charge or delegated to others or other parties, tax

burden taxpayers should be concerned (Income Tax). Indirect tax, the tax

would ultimately be charged or transferred to another person or a third

party. Indirect tax occurs if there is an activity, event, or act which causes

the tax becomes due. Siti Resmi (2009: 7)

Based on Characteristics, tax classification became can be two,

there are Subjective tax; the tax imposition is notice of personal

circumstances or the taxation of taxpayers who watched a state subject

(Income Tax). Objective tax, the tax imposition is noticed either in the

form of objects, things, actions, or events that result in liability to pay tax,

regardless of personal circumstances subject to tax (tax payers) or place of

residence. Siti Resmi (2009: 8)

Based on Institutional collectors, tax is classified became two,

11 used to finance the State households in general. Local tax, the tax levied

by local governments both local provincial (provincial tax) and local level

II (tax district and city) and used to finance local households each.

Includes provincial taxes and motor vehicle tax on water; vehicle

registrations of motor vehicles and vehicles on water, motor vehicle fuel

tax, and tax collection and utilization of underground water and surface sea

water. Tax district include hotel tax, restaurant tax, entertainment tax,

advertisement tax, street lighting tax, tax collection minerals group C, and

parking tax. Siti Resmi (2009: 9)

Siti Resmi (2009: 9) states that Procedures for tax collection consists

of stelsel tax, the principle of tax collection, and tax collection system.

Stelsel tax; tax collections can be done in three stelsel, namely Stelsel real

(Real); stelsel hereby declare that the imposition of taxes based on the

object that actually happened (hence the object is to tax income).

Therefore, the new tax collection can be done at the end of the fiscal year,

i.e. after all the real income in a tax year is known. Stelsel assumed

(fictitious). Stelsel hereby declare that the imposition of taxes based on the

assumption regulated by law. With this stelsel means the amount of tax

payable in the current year can already determined or known at the

beginning of the year. Stelsel mix; stelsel stated that taxation is based on a

combination of real and stelsel assumption.

There are three principles of tax collections, namely Domicile

12 to tax all income tax payers who are resident in its territory (domestic or

foreign). Principle source, this principle states that the country of right to

tax income sourced in territory without notice residential taxpayers. The

principle of nationality is stating that the imposition of taxes associated

with the nationality of a State. Siti Resmi (2009: 10)

Tax collection system has three systems namely Official

Assessment System is tax collection system that gives the tax apparatus

authority to determine their tax returns each year in accordance with

legislation applicable taxation. Self Assessment system is system of tax

collection which empowers taxpayers in determining their own amount

payable each year in accordance with laws, and regulations that apply, and

therefore taxpayers entrusted to: calculate your own tax returns, calculate

their own tax returns pay, reporting, and account for their tax returns. With

a holding system is tax collection system that gives authority to a third

party designated to determine the amount of tax payable by taxpayers in

accordance with taxation legislation requirements. Siti Resmi (2009: 11)

According to Adam Smith in his book The Wealth of Nations that

in order to attempt the collection of tax fairness objective. That is, the

underlying principle of the collection is general and equitable. The

principle of taxation is known as The Four Maxims or Smith's Cannon,

namely:

a.Equality, equality in tax burden, according to the ability of the

13 b.Certainty, run a firm, clear and definite.

c.Convenience, not pressing the taxpayer, pays taxes willingly.

d.Economy, tax collection costs are not greater than the total tax

revenue.

2. Tax Administration Reform

Tax Reform includes two areas namely the first is regulation Reform

consist of tax amendment and the second is administrative tax. Strategies step

is done by Service Office. Sugihartini Rahayu (2008). According to Sri

Mulyani Indrawati, finance minister "was designed tax reform

comprehensively categorized in four ways:

a. Improve legislation, ranging from income tax laws (Income Tax), Law of

value added tax (VAT). Improvement Act with the spirit and

responsiveness between the rights and obligations between taxpayers and

officials.

b. Improvement of organizational structure, standard operates procedures so

that there is certainty to the process of service and good governance,

increased efficiency and productivity.

c. Fix the data base and information technology systems to support tax

potential. This is to prevent the interaction between officials and taxpayers

are not required.

d. Sector reform and improvement of quality, competence and integrity of tax

14 reform process is a tough task that must be followed Tjiptardjo", Heri

Susanto, Nur Farida Ahniar VIVAnews (July29:2009)

From the above definition can be concluded that under existing tax

reform in Indonesia aims to Revising the regulations on taxation,

Preventing the things that will damage the corporate-tax value of existing,

As well as to make it easier for taxpayers to pay taxes, Tax return

reporting the tax offices so as to create service processes and governance

that is much better than before.

According to Hendi Haryadi (2009: 2) Administration covers all

activities, from setting up the maintenance of a group of people who have

a differentiation of work to achieve a common goal as well as more widely

used for matters relating to state.

According to encyclopedia taxation which is written by Sophar

Lumbantoruan (2005: 19) in Suryana (2010: 6)

“Administrative tax is manner or procedure collection tax”.

Although perfect a reform tax policy, so that the result did not satisfy if was not followed by reform administration tax. Nasucha (2004: 8)

Bird and Jantscher (1992: 1) in Chaizi Nasucha (2004: 8) suggested that

“Policy change without administrative change is nothing and that it is critical to ensure that change in tax policy are compatible with administrative capacity. In a very real sense tax and administration is tax policy”.

Based on developed countries experience, there are three main

context that is needed to tax administration reform be success, namely

15 Reform strategy which is proper to special condition each country must be

developed; and There is a political commitment which is strong toward

increase tax administrative. According to Chaizi Nasucha (2004)

dimensions of reform administration tax, namely:

a. Organization structure

Organization Structure is formal plan to create divide work

which is efficiency and effective coordinate of activities organization

member. Organization structure content about how work task will be

divided, classified, and coordinated as formal. Robbins (2001: 217).

Quoting Adiwisatra (1998) is explained by Nasucha (2004: 69) that

organization structure is element that related to role had fixed and

relationship among role and activity allocation to separate sub-units,

authority’s distribution in between administrative position and

formal network communicate.

b. Organization Procedure

Every society organization facilities in process socialization

as formal in other hand in form education and training activity.

Organization Procedure related to communicate process, decision

making, reward choosing, socialization and carrier. Schein

(1997:210-232) in Nasucha (2004: 9) stressed that organization

socialization is process to teach something, process about something

which is indoctrinated, and process which is learned about what is

16 c. Organization Strategy

Organization Strategy is viewed as strategy, behavior

viewing and act that aimed take benefit every conditions, factors,

opportunities and sources that exists so that organization goal can be

achieved as successful and safety. Koontz (1984: 18) in Chaizi

(2004: 9) mentioned that strategy related to wise. Strategy is general

program of acting and commitment on stressed and sources to

achieve goal. Robbins (1990: 138) in Nasucha (2004: 9), states that

dimension of strategy which show implication toward organization

structure is innovation, differentiation, breadth, cost control.

d. Organization Culture

Culture contains as trust, value and behavior together which

is received by several people. Schemerhorn (2001: 101). Quoted by

Edgar Schein, Schemerhorn (2001: 273) stressed that organization

culture is mentioned as a system trust spread and values which is

develop and about behaviors organization member.

3. Emotional Intelligence

According to Wibowo (2002) in Arsinawati (2010)

“Emotional intelligence is emotional intelligence for use in accordance with the desire, ability to control emotions so as to provide a positive impact”.

Salovey and Mayer in Goleman (2005) define

17 Mustofa and Agus (2007) define that

“Emotional intelligence include abilities are different, but complementary to academic intelligence, the purely cognitive abilities measured by intelligence”.

Goleman (2005) defines that

“Emotional intelligence is the ability to motivate yourself and the ability to manage emotions well in ourselves and in relationship to others.”

Emotional intelligence is the ability to listen and communicate

orally, adaptation, creativity, mental resilience to failures, self-confidence,

motivation, teamwork and desire to contribute to the company. Goleman (1999: 14) in Ary Ginanjar Agustian (2001: 56) and use self-awareness.

Covey (1990: 109) in Ary Ginanjar Agustian (2001: 57)

Mayer and Salovey (1995: 197) in Elizabeth J. Rozell and Wesley

A. Scroggins (2010) defineEI as

“The capacity to process emotional information accurately and efficiently, including that information relevant to the recognition, construction, and regulation of emotion in oneself and others”

The ability models focus on traditional forms of Intelligence

combined with emotion and is the composite of four separate dimensions.

Mayer and Salovey (1997) in Elizabeth J. Rozell et al (2010: 3):

(1) Accurate perception of emotion (in self and others);

(2) Assimilation of emotion to facilitate thought;

(3) An understanding of emotion; and

18 From definition above can be conclude that emotional intelligence

related to our ability to control and manage our emotion in order to keep

emotion stable and well, to motivate ouselves in order to get positive

impact. However it can be increased awareness of taxpayers.

4. Taxpayers Awareness

According to Tarjo, et al (2005)

"Awareness of taxation is an attitude toward the meaning and function of the tax, a component of a constellation of cognitive, affective, and co native that interact in understanding, feeling and behaving to the meaning and function of tax”.

Widjaja (1984: 14) in Fanie (2009: 24)

“Awareness is defined as an attitude or behavior to know or understand, obey and comply to the rules of existing legislation, is also an attitude or behaviour know and understand, obey and comply with the customs and traditions and habits of living in society”.

Siti Resmi (2009: 21)

“Taxpayers are individuals or entities include taxpayers, tax collectors and tax cutters who have rights and tax obligations in accordance with the provisions of tax legislation”.

According to Tarjo and Sawarjuwono (2005: 21) in order to increase

awareness of taxpayers within related to taxation that government

through connect to Mayor Directorate Tax always increase intensities

socialization tax which focused in awareness taxpayers to tax.

Individual taxpayer’s awareness will grow either if they had known

or understood besides that there have to punish which is tiding. If only

know and understand, but there is no punishing so that there is no scared.

19 perception by taxpayer can open knowledge them that it is implemented

as fairness to all of taxpayers. However it can grow awareness taxpayers

to report theirs tax as punctual.

Someone will be aware if understand. Its mean that theirs have

to know first related to tax. After knowing it then understanding so that

appear to be aware even though either can obey or fulfill their tax duty.

Rahayu (2003: 19). According to Mangkoesoebroto (1999: 52) in

Purnamasari (2007: 20) taxpayer’s awareness always is related to

compliance through hold tax’s right and obligation as role especially for

The higher society knowledge’s, the easier taxpayer understands

especially related to relationship between cost and benefit of every

government activities, The Knowledge levels, Fair of tax system and

administrative system are either easy or simply.

According to Reza Mardian (2009), awareness of taxpayers so

often associated with compliance and compliance in implementing the

rights and obligations taxation accordance with existing regulations,

especially in terms of the following are Knowledge society, the higher

the public's knowledge of tax neighbors then the easier the government to

explain to the public (taxpayer) related to regulatory and tax benefits

from the public and government. Education level, this is necessary in

understanding the tax and the tax filing in odd moments seems

20 question is a fair tax system for all parties and system is administration

simple and easy.

Pramono (2003: 16) in Reza Mardian (2009) stressed that indicator

of the consciousness of taxpayers are Knowledge of Taxation,

Knowledge about tax regulations, Patterns of behavior toward the

taxpayer tax payments. Suryadi (2006) mentions that indicators of

awareness have four type, namely Taxpayers Perception, Knowledge of

Taxation, Taxpayers Characteristic, and Socializations Taxation.

Based on expert opinions, we can conclude that consciousness is

an activity or behavior of someone who is influenced by education,

knowledge, habit patterns of behavior and socializations. Awareness is a

conscious act of doing certain activities. Growing awareness on the

individual taxpayer is required to be carried taxation. Taxpayers must

have an awareness of paying taxes so the tax system in Indonesia can be

run well and the source of government revenue can be increased in

developing countries.

5. Income Taxes

The word "Income Tax" has two meanings together with the other.

The First is understanding of the meaning of "tax" itself and second is

sense of the meaning of "income". Understanding tax is free to do as a

state obligation in the form of devotion and the active role citizens and

21 implementation of national development which is set in legislation and

regulations for the purpose of welfare of the nation and the State.

In other words, understanding the tax can be considered as fringe

benefits provided by society to the government for the facilities that we

can enjoy being able to live well in a State. Despite of income is the

amount of money received for work done by individuals, agencies and

other business forms that can be used for economic activities such as

eating and or hoarding and increasing wealth.

According to article 4 paragraphs 1 of the Income Tax Act No. 36

of 2008,

“which meant the income which is any additional economic capability received or accrued by a taxpayer, whether originating from Indonesia and outside Indonesia, which can be used for consumption or to increase the wealth of taxpayers concerned, with the name and in any form”.

So understanding the income tax is a levy directed to the public

official whose income or on income received and earned in the fiscal year

for the interests of the State and society in the life of nation and state as an

obligation that must be implemented. It should be emphasized here, is the

object of income tax, in accordance with article 4 above, is income that is

economical and additional capabilities that can be used for consumption or

to increase the wealth of the taxpayer. In other words if the income

received is not an economical or not additional ability to increase property

22 The legal basis for income tax in Indonesia is a plus Act

regulations that support under it include the following are Government

Regulation (PP), Regulation of the President (Presidential), Regulation of

the Minister Finance (PMK), DGT Regulation (Per.DJP). Laws governing

the income taxes in Indonesia at this time began with the law No. 7 of

1983. Later the law was amended several times, changed into law No.7 of

1991, then changed again into law No.10 of 1994 and last amended to Act

No.17 of 2000. The last Act, i.e. Act No. 36 of 2008 becomes effective

from 1 January 2009. Paryan (2009: 2). Here there are the income tax

explanations, we first need to learn about the subject of taxes and income

tax object.

The principle relating to the subject of Tax is the principle of

domicile which is a principle of taxation based on domicile or residence

subject to tax. The principle of source, namely the principle of taxation

based on source of income derived subject to tax. The principle of

nationality is the principle of taxation based on citizenship subject to tax.

The tax liability of an individual or agency or heritage begins and

ends at when an individual who resides in Indonesia, an individual

residing in Indonesia for more than 183 (one hundred and eighty-three)

days within any 12 (twelve) months, or an individual who in a tax year are

in Indonesia and has the intention to reside in Indonesia. Board was

23 longer domiciled in Indonesia. The emergence of inheritance and ending at

the time of the inheritance is distributed.

At the start and end of subjective tax liabilities in the income tax is

very important because income tax is a subjective kind of tax that the tax

liability attached to the subject of taxes is concerned, meaning that tax

liabilities are not intended to be delegated to other tax subjects. Because

state taxes are attached to the subject in question, it is important to know

for sure about when to start and when to end one's subjective tax liability.

The tax liability of an individual as written above begins when the

individual is born, it means simply to say that individuals can obtain tax

ID when she was born with a birth certificate showing proof of or letter of

his birth, especially in this modern age is not income monopoly only

adults only, but anyone regardless of age can earn revenue from various

types of work and activities. For example: a toddler, even a baby can earn

not less than the ads that is role.

In accordance with the principles above, the subject of individual

tax and or general body may be subject to tax in domestic or foreign tax

subject. Here are the differences in domestic taxpayers and foreign

[image:37.612.148.526.62.438.2]taxpayers, among others are:

Table 2.1

The differences in domestic taxpayers and foreign taxpayers

Taxpayer Taxpayers overseas

Subject to income tax on both Received outside Indonesia Just or obtained from Indonesia.

Imposed tax on income from income derived from sources in Indonesia.

24

Subject to tax based on net income.

The tax rate used is the general tariff (rate of Income Tax Law Article 17).

Obligation to submit tax returns SPT.

Tax rate used is the rate worth (tariff Income Tax Law Article 26).

Not required to submit tax returns SPT.

Based on the explanation above regarding the subject of domestic

taxes and foreign tax subject, that it is clear that, for payers in the country,

subject to income tax whether received or obtained from Indonesia and

outside Indonesia, in accordance with the principle of nationality, while

WP's foreign taxable only on income derived from sources of income in

Indonesia, according to the principle source. For an individual who is the

subject of taxes in the country and abroad is an individual who resides in

Indonesia counted since its presence in Indonesia for 183 (one hundred

and eighty-three) days within a period of 12 (twelve) months may be taxed

as a subject of domestic taxes in accordance with the principle of domicile.

For more details, this included in the Personal category as the

subject of taxes is as follows:

a. Employees in general, namely an individual who did the work under an

employment agreement or agreements either written or unwritten,

including those that do the work in the office of the country or state

owned enterprises and state owned areas;

b. Permanent employees, i.e. an individual who works at the employers

who receive salary or earn a certain amount on a regular basis,

25 supervisory board who regularly participate directly manage the

company's activities;

c. Employees separated, i.e. an individual who works at the employers

who only receive benefits if the individual in question worked;

d. Employees with WP status abroad that is an individual who does not

reside in Indonesia or are in Indonesia for not more than 183 days

within a period of 12 months who receive or earn a salary, honorarium

and other benefits related to employment, services, and activities;

e. Pension recipients, the individuals or their heirs who receive or obtain

compensation for work performed in the past, including private

persons or their heirs who receive Old Age Savings or Retirement

Allowances;

f. Honorarium Recipient, the individuals who receive or obtain

compensation in connection with, positions or activities that do;

g. The recipient of wages, i.e. individuals who receive daily wages, weekly

wages, piece rate, or wage unit;

From what has been described above, it can be concluded that the

subject of taxes is the all-income persons or entities in Indonesia, both as

an Indonesian citizen who earn income abroad either individually or in the

form of the body.

While that does not include tax subjects that first is the

representatives of foreign countries. Second is The official representatives

26 and those who assisted to those who work in and live with them, provided

that; No citizen of Indonesia and in Indonesia does not receive or obtain

other income outside his office in Indonesia and The States concerned to

provide reciprocal treatment. Third is International organizations referred

to in the decision of the Minister of Finance Number 574/KMK.04/2000

dated 26 December 2000 as last amended by Decree of the Minister of

Finance Number 243/KMK.03/2003 dated 4 June 2003, provided that

Indonesia is a member organization and not conducting business or other

activities to earn income from Indonesia other than lending to the

government whose funds come from contributions of members.

Last is The official representatives of international organizations as

referred to in the Decree of the Minister of Finance Number

574/KMK.04/2000 dated 26 December 2000 as last amended by Decree of

the Minister of Finance Number 243/KMK.03/2003 dated 4 June 2003,

provided that No citizen Indonesia, Not conducting business or doing any

activity or other work to earn income in Indonesia.

According to Article 4 paragraph (1) states that the object the income

tax is earn. Income is any additional economic capability received or

accrued by taxpayers, whether they come from Indonesia and outside

Indonesia, which can be used for consumption or increase the wealth of

Taxpayer, with the name and in any form.

What is included in the definition of income is:

27 Received or accrued, including salaries, wages, honoraria,

commissions, bonuses, gratuities, pensions, or compensation in other

forms, unless otherwise provided in this Act;

b. Gifts from the lottery or work or activities, and awards;

c. Operating income;

d. Gains from the sale or transfer of property including;

1) Gain due to transfer of property to the company, partnership and

other agencies in lieu of shares or equity participation.

2) Gains derived by the company, partnerships and other entities for

the Transfer of property to shareholders, partners, or members.

3) Gain in liquidation, merger, consolidation, expansion, split, or Take

over attempt.

4) Gain in the transfer of property in the form of grants, aid or

donation, except given to blood relatives in a straight line one

degree, and religious bodies or agencies of education or social

agencies or small businesses, including cooperatives established by

the Minister of Finance, as long as there is no correlation with

business, occupation, possession, or control between the parties

concerned.

e. Refunds of tax payments that have been charged as an expense;

f. Interest, including premiums, discounts and other benefits for loan

28 g. Dividends, by whatever name and form, including dividends from

insurance companies to policyholders, and the distribution of

cooperative effort;

h. Royalty;

i. Rental and other income in connection with the use of property;

j. Acceptance or obtaining periodic payments;

k. Benefits Due to debt relief, except to a certain amount determined by

government regulation;

l. Foreign exchange gains from foreign currency;

m. Difference from revaluation of assets;

n. Insurance premiums;

o. Contributions received or obtained from part association consisting of

the taxpayer are engaged in business or professional services;

p. Wealth net additional income derived from that has not been taxed.

Income can be grouped into four namely Income from

employment in employment and independent work, such as salary,

honorarium, income from the profession of experts. Income comes from a

business or an activity. Income from capital or the use of property, such as

rent, interest, dividends, royalties, gains from the sale of unused property,

and so forth. Other income, i.e. income that can not be classified into one

of three income groups above, such as Gains due to debt relief; Foreign

exchange gains due to foreign currency; Difference from revaluation of

29 For taxpayers is the country which became taxable income is

good income coming from Indonesia and outside Indonesia. Whereas for

foreign taxpayers, who becomes a taxable income only income comes

from Indonesia alone.

While that does not include a taxable income in accordance with

the provisions of Article 4 paragraph (3) of the Income Tax Act are:

a. Aid donations, including alms received by the agency alms charity or

institution established or approved by the government and is entitled to

alms recipients;

b. The property gift received by family incest in a straight line one degree,

and by religious bodies or agencies or educational charities or small

businesses, including cooperatives established by the Minister of

Finance, as long as there are no relationships with business,

employment, ownership, or mastery between the parties concerned;

c. Heritage;

d. Assets including cash deposits received by the agency as an exchange

for shares or capital;

e. Replacement or compensation in connection with work or services

received or acquired in kind and or enjoyment of the taxpayer or the

government;

f. Payment of an insurance company to an individual in connection with

health insurance, accident insurance, life insurance, endowment

30 g. Dividends or share of profits received or accrued by a limited liability

company as a Taxpayer, cooperatives, state enterprises, or enterprises,

from investments in other business entity established and domiciled in

Indonesia with the following requirements are Dividends from retained

earnings reserve. For limited companies, SOEs and enterprises that

receive the lowest dividend of 25% (twenty five percent) of the paid up

capital and must have an active business outside the ownership of

these shares;

h. Contributions received or accrued pension fund which establishment

was approved by the Minister of Finance, be paid by the employer or

employee;

i. Income from capital invested by pension funds as referred to in number

7, in specific areas determined by the Minister of Finance;

j. Equity in net income received or accrued by a member of a limited

partnership whose capital is not divided into shares, partnership,

association, firm, and the joint venture;

k. Interest received or accrued by a member of a limited partnership

whose capital is not divided into shares, partnership, association, firm,

and joint venture;

l. Interest received or accrued bond mutual fund companies during the

first 5 years since the founding of the company or business

31 m. Income received or accrued by venture capital firms for a share of

income from agency business partner, founded and run a business or

activity in Indonesia, provided that such business partner agencies: a

small, medium, or which carries on business in the business sectors

determined by the decision of the Minister of Finance and its shares are

not traded on stock exchanges in Indonesia.

The obligation to submit and report annual tax return (SPT) is a

means for taxpayers to report on matters relating to tax obligations. SPT

must be filled in correctly, completely, and clearly in the Indonesian

language using Latin letters and Arabic numbers, the currency of rupiah and

sign and submit it to the Tax Office (KPP) and any other place determined

by the Directorate General of Taxation.

Function returns for taxpayers income tax is as a means to report and

account for calculating the amount of tax actually owed and to report on:

a. Payment or repayment of tax which has been implemented alone and or

through the withholding or collection of other parties within one (1) tax

year or the tax year;

b. Income subject to income tax and or subject to tax;

c. Property and liability;

d. Payment of the cutter or collector of tax cuts or individuals or other

entities within one (1) the tax period in accordance with the provisions of

32 Individual taxpayers each year must report income received or

obtained during one year. Income reported is any additional economic

capability in the form of taxpayer’s money and the form of goods (in

accordance with article 4 paragraph 1 of Act KUP). If there is a net income

that has not been reported in previous years, it can be reported by organizing

includes in the SPT have been reported. Required to submit annual tax

returns are:

a. Individual taxpayers who receive or earn income from business activities

and or independent;

b. Individual taxpayers who receive or obtain income from capital and

others;

c. Employees who receive or earn income other than in connection with

work, service or activity and or who earn income in relation to

employment, services or activities of more than one employer;

d. Authorization for an undivided inheritance;

e. State officials, civil servants, members of the Armed Forces and

employees of state-owned companies;

f. Indonesian citizen who works in a foreign country representatives and

representatives of international organizations;

g. Foreigners residing in Indonesia for more than 183 days within a period

of 12 months or person in a tax year are in Indonesia and have the

33 h. Each husband and wife is taxed separately in terms of income; Husband

and wife have lived apart. Required in writing by the husband and wife

under the separation agreement and property income (in this case

husband and wife must have tax ID).

Income Tax Act of 2008 requires public and private employees

whose income above PTKP must have a Taxpayer Identification Number

(TIN). As a consequence because they have a TIN to report income in the

Personal Income Tax Return a year. Excluded from the obligation to submit

annual tax returns:

a. Individual taxpayers who are exempt from the obligation to submit the

income tax returns and annual tax section 25 income taxes. (PMK

183/KMK.03/2007); "individual taxpayer in a tax year to receive or

obtain net income does not exceed non taxable income referred to in

Article 7 third law changes the income tax 1984";

b. Individual taxpayers who are exempt from the obligation to submit

income tax returns the article 25 but must submit annual income tax

returns. (PMK 183/KMK.03/2007): "an individual taxpayer who does

not carry on business or not doing the job free.

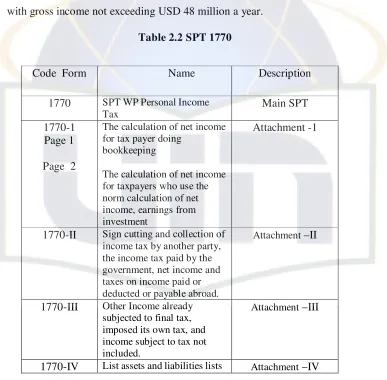

In accordance with PER-81/PJ/2007 and PER-8/PJ./2008

(PER-161/PJ./2007 changes) can be explained that for the Personal Income Tax

Annual tax return since tax year 2007 and subsequent years there were two

types of namely SPT 1770 is intended for individual taxpayers who carry on

34 taxpayers who do not conduct business activities and independent. SPT 1770

SS is intended for individual taxpayers who have income from one employer

[image:48.612.151.538.154.534.2]with gross income not exceeding USD 48 million a year.

Table 2.2 SPT 1770

Code Form Name Description

1770 SPTWPPersonalIncome Tax

Main SPT

1770-1 Page 1

Page 2

The calculation of net income for tax payer doing

bookkeeping

The calculation of net income for taxpayers who use the norm calculation of net income, earnings from investment

Attachment -1

1770-II Sign cutting and collection of income tax by another party, the income tax paid by the government, net income and taxes on income paid or deducted or payable abroad.

Attachment –II

1770-III Other Income already subjected to final tax, imposed its own tax, and income subject to tax not included.

Attachment –III

1770-IV Listassetsandliabilitieslists Attachment –IV

Table 2.3 SPT 1770 S

Name Description

PersonalIncome TaxAnnualReturn SPT Main SPT

Income related to employment, net income in another country, a list of deductions or tax collection by other parties and the Income Tax borne by the government

Attachment I

35 On SPT 1770 SS consist only of parent annual corporate tax returns

for individuals. While the attachment of Personal Income Tax Annual tax

return is as follows:

a. Balance sheet and income statement (if using bookkeeping);

b. List the calculation of depreciation and or amortization of fiscal;

c. The calculation of compensation for losses in the event of any remaining

losses in previous years can still be compensated;

d. Summary of monthly gross turnover (if using norm calculation of net

income);

e. SSP income tax article 29 of the under payment of tax, unless there is

permission to move or postpone;

f. Special power of attorney if tax return not signed by the taxpayer, or in

the case of a death certificate signed by the heirs;

g. Copy of Form 1721-A1 from the employer (if private sector employees,

including SOEs and enterprises);

h. Copy of Form 1721-A2 from the employer (if civil servants, police, or

State Officials);

i. Calculation of income tax by each party for married taxpayers with

property separation agreement;

j. List of family structure that became taxpayer burden;

k. Proof of payment of alms on income paid by the taxpayer to the Agency

36 The deadline for payment for the types of Personal annual tax

return is the 25th of the third month after the end of the year or the year of

tax and reporting deadlines are no later than 3 months after the end of the tax

or the tax year. Tax payments made by several methods, namely pay tax due,

through withholding and collection by other parties, through tax payments

abroad, and payment of other taxes. Implementation of tax payments to be

School of payment using Tax Payment (SSP) that can be taken by at the Tax

Service Office (KPP) or the nearest KP4, or by other means through tax

payments electronically (e-payment).

Mail tax payments (SSP) is a letter by the taxpayer is used to make a

payment or deposit of tax payable to the state treasury through the Office of

Payment Receipt. Payments Office is a post office or bank and State Owned

or Bank Owned Enterprises Regional or other place of payment designated

by the finance minister as the recipient of payment or tax deposit.

B. Previous research

Results from previous research conducted a few researchers are as follows:

Chaizi Nasucha (2004) entitled the tax administrative reform toward

compliance taxpayers. The Reform tax administration variable with sub

variable: reform organization structure (X1), reform organization procedure

(X2), reform organization strategy (X3), reform organization culture (X4).

There is positive effect of tax administrative reform toward compliance

37 (X3), and reform organization culture (X4) do not affect to compliance but

reform organization procedure (X2) does. For all variabels as simultaneous

affect to compliance. The method used regression Linier analysis and

correlation analysis. All count coefficients is done by SPSS and Likert Scale.

Myleen M. Leary, Michael D. Reilly and F. William Brown (2008) with

title are a study of personality preferences and emotional intelligence. Results

support the relationship between extroversion and the components of EI. A

positive and significant relationship between a preference for the use of

feeling in decision making and an individual’s EI is also found. MBTI, Form

G, and EQI data are collected in a population of over 500 managers and

professional workers in an international manufacturing facility. Both

categorical and continuous analysis of variance is utilized to test ten

hypothesized relationships between personality preferences and EI constructs.

Fenie Oktaliana (2009) entitled headman leadership influence on the

increase of public awareness in paying property tax. Independent variable in

this research is the leadership (X) and dependent variable is the awareness of

society in paying property tax (Y). The method used is a quantitative analysis

method, while for the data analysis technique used is the technique of

correlation between variables to prove the effect of leadership on the public

consciousness in paying property tax. Based on the explanation of the

research showing that there is a very significant impact if the leadership of the

headman upgraded automatically pay more to increase public awareness in

38 Suryadi (2006) The Kausal relationship model among awareness, service,

compliance and its effect toward Tax Receipt Performance at East Java Area.

The result is awareness has positive effect toward Tax Receipt Performance.

With indicator of awareness are Taxpayers Perception, Knowledge of

Taxation, Taxpayers Characteristic, and Socializations Taxation. With used

area random sampling, cluster random sampling, and structural equation

modeling (SEM).

C. Effect of the Reform Administration Tax and Emotional Intelligence

toward Awareness of Individual Taxpayer

The existence of tax administration reform to help taxpayers and

tax authorities in the payment cycle, can simplify the payment. According to

Soebagyo (2005) in Reza Mardian (2009) consciousness to fulfill tax

obligations can arise when people have knowledge of the tax that is why

you should pay taxes, knowing the nature of the tax, knowing the

punishment if they do not pay taxes and therefore knowledge needed to

create communities that are aware of the tax.

A good Emotional intelligence taxpayers can arise their awareness.

According to Goleman (2005) emotional intelligence is the ability to

motivate yourself and the ability to manage emotions well in ourselves and

in relationship to others. Thus, it can be concluded if taxpayers can manage

their emotion as well so it can arise a good relationship, its mean awareness

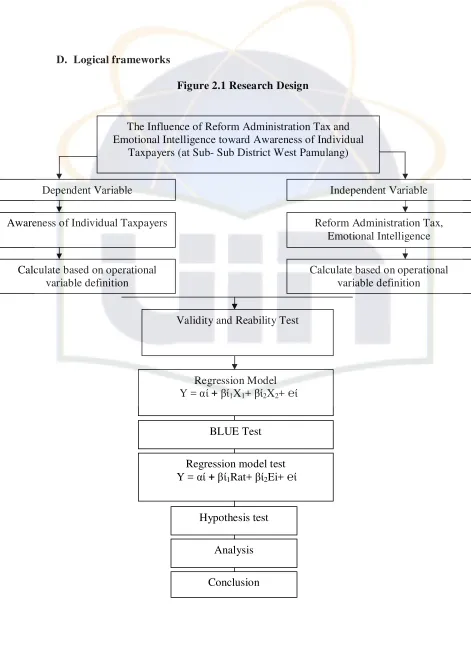

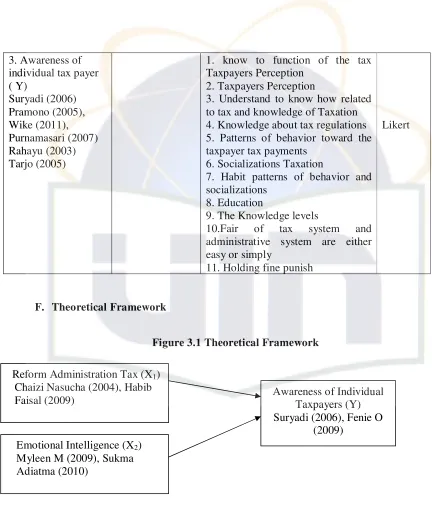

39 D. Logical frameworks

Figure 2.1 Research Design

Dependent Variable Independent Variable

Awareness of Individual Taxpayers Reform Administration Tax,

Emotional Intelligence

Calculate based on operational variable