1 THE INFLUENCE OF ISLAMIC VALUE TOWARDS SOCIAL

REPORTING (A CASE STUDY: BSM AND BMI)

Submitted By: Sholatia Dalimunthe Student ID: 604082000015

INTERNATIONAL PROGRAM ACCOUNTING DEPARTMENT

FACULTY OF ECONOMICS AND SOCIAL SCIENCES UNIVERSITAS ISLAM NEGERI SYARIF HIDAYATULLAH

2 THE INFLUENCE OF ISLAMIC VALUE TOWARDS SOCIAL

REPORTING (A CASE STUDY: BSM AND BMI)

Thesis

Submitted to Faculty of Economics and Social Sciences

As Partial Requirement for Acquiring the Bachelor Degree of Economics

Submitted by:

Sholatia Dalimunthe Student ID: 604082000015

Under Guidance of

Thesis Advisor I Thesis Advisor II

Prof. Dr. Abdul Hamid, MS Ade Wirman Syafei, SE., MSc NIP. 131 474 891

INTERNATIONAL CLASS PROGRAM ACCOUNTING DEPARTMENT

FACULTY OF ECONOMICS AND SOCIAL SCIENCES STATE ISLAMIC UNIVERSITY SYARIF HIDAYATULLAH

3 THE INFLUENCE OF ISLAMIC VALUE TOWARDS SOCIAL

REPORTING (A CASE STUDY: BSM AND BMI)

Thesis

Submitted to Faculty of Economics and Social Sciences

As Partial Requirement for Acquiring the Bachelor Degree of Economics

Submitted by:

Sholatia Dalimunthe Student ID: 604082000015

Under Guidance of

Thesis Advisor I Thesis Advisor I

Prof. Dr. Abdul Hamid, MS Ade Wirman Syafei, SE., MSc NIP. 131 474 891

Professional Examiner

Drs. Abdul Hamid Cebba, Ak., MBA NIP. 132 055 044

INTERNATIONAL CLASS PROGRAM MANAGEMENT DEPARTMENT

FACULTY OF ECONOMY AND SOCIAL SCIENCES STATE ISLAMIC UNIVERSITY SYARIF HIDAYATULLAH

4 Today, we administered a comprehensive examination to Sholatia Dalimunthe ID 604082000015. The title of her thesis is: “The Influence of Islamic Value towards Social Reporting” (A Case Study: BSM and BMI). After proper examination of the work student, we have decided that she has met all of the requirements for the title of Bachelor of Economics on the field of Accounting, State Islamic University (Universitas Islam Negri) Syarif Hidayatullah Jakarta.

Jakarta, August 1st 2008

Comprehensive Examination Team

5 AUTO BIOGRAPHY

I. IDENTITY

Name : Sholatia Dalimunthe

Place/ Date of Birth : Medan, 26 April 1987

Religion : Islam

Address : Jln Kenanga No 257 Yogyakarta

Post Code: 55282.

Phone No : 0274-485384/ 081574897998

E-mail :[email protected]

II. EDUCATIONAL BACKGROUND

1. SDN Maguwoharjo 1 Yogyakarta (1992-1998)

2. SLTP N 4 Depok Yogyakarta (1998-2001)

3. SMU N 11 Yogyakarta (2001-2004)

4. UIN Syarif Hidayatullah Jakarta (2004-2009)

III. ORGANIZATIONAL EXPERIENCE

English Club – LIA Pramuka

IV. FAMILY BACKGROUND

1. Father : Danas Dalimunthe

2. Place/ Date of Birth : Sihepeng, 21 August 1945

3. Address : Jln Kenanga No 257 Yogyakarta

4. Phone No. : 0274 - 485384

6 6. Place/ Date of Birth : Sihepeng, 08 August 1954

7. Address : Jln Kenanga No 257 Yogyakarta

8. Phone No. : 0274 - 485384

7 ABSTRAK

Bank Islam merupakan bank yang berdasarkan prinsip-prinsip syariah dimana diharapkan bank Islam dapat memberikan kesejahteraan kepada masyarakat sesuai dengan prinsip syariah. Oleh karena itu, bank Islam diharapkan dapat memberikan informasi yg berkaitan dengan kegiatan sosial.

Tujuan penelitian ini untuk mengidentifikasi pengungkapan sosial dan pengaruh nilai-nilai Islam terhadap pengungkapan sosial dalam laporan tahunan Bank Syariah Mandiri dan Bank Muamalat Indonesia dari tahun 2003 sampai 2007. Penelitian ini menggunakan instrumen dari Haniffa dan Maali dkk.

Dari hasil penelitian, menyatakan bahwa pengungkapan sosial Bank Syariah Mandiri dan Bank Muamalat Indonesia lebih tranparan dan dipengaruhi nilai-nilai Islam yang sesuai dengan prinsip syariah.

8 ABSTRACT

Islamic Bank is a bank based on shari’ah principles whereas Islamic bank is expected can produce prosperity to community based on shari’ah principle. Therefore, Islamic Banks are expected to provide information related with social activity.

The objective of this research is to identify the social disclosure and the influence of Islamic value towards social reporting in annual report of Bank Syariah Mandiri and Bank Muamalat Indonesia from 2003 until 2007. This research uses instrument from Haniffa and Maali et al.

Result of the research indicates that social reporting in Bank Syariah Mandiri and Bank Muamalat Indonesia is more transparent and influenced by Islamic value which is according to shari’ah principle.

9 PREFACE

Alhamdulillahirabbil’alamin, In the name of Allah, the beneficent, the

most merciful. All praises be to him, the lord of the World, as benefits His glory

and the greatness of His Power. I am grateful to Him for the blessings bestowed

upon me, and for honoring me with His aid in finishing this thesis in order to fulfill one of the requirement programs in order to graduate as a bachelor of

economy, on the topic I have chooses on “The Influence of Islamic Value towards

Social Reporting (A Case Study: BSM and BMI)”, where the thesis has been

well-made and can be easily understandable as what I have been expected.

This thesis finishes with support and help from many people. Therefore, in

this opportunity I want to say thanks to;

1. My great family, my lovely parents and all my sister, kak butet, kak eni,

kak epi, kak dewi, and kak ito, who always give a support, love, advice etc

during my thesis process.

2. Mr. Prof. Dr. Abdul Hamid, MS as my first supervisor who gives

knowledge and advice in finishing the thesis, therefore this thesis can

finish as the expectation.

3. Mr. Ade Wirman Syafei, SE, Msc as my second supervisor who always

be patient in guiding me and giving me an advice in every step in this

thesis.

4. Mr. Moh. Faisal Badroen, SE, MBA as the Dean Faculty of Economics

10 5. Mr. Junino Jahja as the Head of International Program.

6. Mr. Arisman M.Si as the Secretary of International Program.

7. Mr. Dr Abdul Hamid Cebba, Ak, MBA as the Head of Accounting

Department.

8. Mr. Amilin, Ak. as the Secretary of Accounting Department.

9. My friend demo, lala, sinta, novita, tantra, who always give me a support

and fun moment when I give up.

10.My lovely friends fitry the lambreta girl that always company me, ica who

always scream in my ears an advice and support, iyah who has same

problem with me, nada who always bring me to a great event, and kiki

who always give an advice to me.

11. My college friend especially accounting class: virul, sofyan, mamat,

faqih, and nada. I hope we can make that company together as we expect and all my classmates who always give me a fun moment.

12.Last but no Least a Special thanks to all Management Divisions of

International Class Program Bu Hayati, Mbak Muty, K’Sholatia, K’Yazid,

K’Fitri and K’Ilham who sacrifices their full time in Secretariat of Int’l

Class and giving us support, patient managing Int’l Class students.

Jakarta, 24 December 2008

Sholatia Dalimunthe

11 TABLE OF CONTENTS

Page of Thesis Approval ... i

Page of Thesis Examination Approval ... ii

Page of Comprehension Test... iii

Auto Biography…... iv

Abstrak.…………... vi

Abstract…………... vii

Preface……… ... viii

Table of Contents... x

List of Tables………... xii

List of Appendix…………... xiii

CHAPTER I INTRODUCTION A. Background ... 1

B. Problem Identification ... 4

C. Purpose of Study and the Use of Study... 4

CHAPTER II THEORETICAL FRAMEWORK A. Islamic Bank ... 5

B. Islamic Value ... 7

1. Tawhid... 8

2. Khilafah... 10

3. Al Adl... 11

4. Halal and Haram, Ummah, and Maslahah ... 15

C. Social Reporting in Islamic Perspective... 16

1. Corporate Social Responsibility……… ... 16

2. Social Reporting………... 18

3. Scope of Disclosure……… ... 21

D. Benchmark for Social Disclosures by Islamic Bank………... 24

CHAPTER III METHODOLOGY A. Scope of The Research ... 36

B. Sampling Method ... 36

C. Data Collection Method... 36

D. Data Analysis Method ... 37

1. Coefficient Determination……….... 39

2. T test………... 39

12 CHAPTER IV RESULT AND FINDING

A. Company Profile ... 43

1. Bank Muamalat Indonesia ... 43

2. Bank Syariah Mandiri... 44

B. Result and Findings ... 46

1. Coefficient Determination ... 46

2. T test ... 47

CHAPTER V CONCLUSION AND IMPLICATION A. Conclusion ... 50

B. Implications ... 51

13 List of Tables

Number Explanation Page 2.1 Objectives and Ethical Statement of Islamic Social Reports 20

3.1 Instrument of Independent Variable ... 41

3.2 Instrument of Dependent Variable... 42

4.1 Coefficient Determination …. ... 46

14 List of Appendix

15 CHAPTER I

INTRODUCTION A. Background of Study

Islamic banking is a worldwide phenomenon involving a variety of

institutions instruments rather than one “project” or institution (Timberg,

2000: 2). In Indonesia, the development of Islamic bank is a phenomenon and

has a significant role in the economy. According to Alfi wijaya, the head of

research and management project division in Karim Business Consultant,

Islamic Bank shows quick development from year to year although it is new in the banking business and year of 2008 is predicted as a successful Islamic

bank development year in Indonesia.

The fast development of islamic bank in indonesia has begun since the

legalize UU no 10 1998. This recognizes the practice explains the law and

kind of business that can be operated and implemented by islamic bank.

Beside that, this UU gives a direction for conventional banks to provide

shari’ah bankin services by establishing an independent islamic branch.

This opportunity has been responsed with high antusiasm by the banking

community in Indonesia. It can be seen from the establishment of shari’ah

bank that is a convertion from conventional bank such as Bank Syariah

Mandiri (convertion from Bank Susila Bakti), and the establishment of conventinal bank that has Shari’ah Business Unit such as Bank Bukopin, Bank

16 development of Shari’ah Bank is supported by the addition of office

channeling of Shari’ah Bank and Shari’ah Business Unit (Antonio, 2005:25). Islamic Bank is a business unit that is focus in finance to mobilize society

fund and give services to other banks based on islamic principle (shari’ah)

from Al-Qur’an and Al-Hadist. Shari’ah is concerned with promoting justice and welfare in society (Al-adl and Al-ihsan) and seeking God’s blessings (Barakah), with the ultimate aim of achieving success in this world and

hereafter (Al-falah) (Haniffa and Hudaib, 2007:99). This statement is

supported by Alwosabi who says that the purpose of Shari’ah is to promote and protect the interest of individuals and societies by bringing benefits and

preventing harm in relation to their necessities, needs and wants.

The differential principle and operation between Islamic bank and conventional bank gives a difference implication in the accounting principles on both disclosure and reporting. While conventional financial institution follows the accounting standards of the International Accounting Standards,

American Financial accounting Standards, and British Accounting Practices,

the AAOIFI was created in 1990 to design and disseminate accounting and

auditing standards that can be applied internationally by all Islamic

institutions.

According to AAOIFI (2004: 65) the financial statement should disclose

all material information that is necessary to make those financial statements

17

objective of corporate reporting is to allow Islamic enterprises to show their compliance with Shari’ah (Baydoun and Willett, 1997: 6).

According to Farook and Lanis (2005: 356) the social role of Islamic

Banks that entails social justice and accountability, requiring the banks to

disclose corporate social responsibility (CSR) information. It is appropriate with shari’ah principle that business transactions can never be separated from

the moral objectives of society. According to Farook and Lanis (2005: 356) a

number of scholars have developed a normative standard for reporting and

indeed social reporting for Islamic businesses based on Islamic principles

(Haniffa 2001; Maali et al, 2003). Governments in Muslim populated

countries such as Malaysia and AAOIFI have also voiced their support for the

development and adoption of such CSR reporting standards encouraged and

propagated by Islam (Sharani and Yunus, 2004).

The objective of this study is to measure the annual report social

disclosure levels of Islamic banks based on a benchmark derived from Islamic

principles. Second objective is to know whether there is an influence of

Islamic value to social reporting in Islamic bank. This study will discuss the

role of Islamic bank and the Islamic value that imply in Islamic bank. Besides

that, this study will explain the disclosure from the Islamic perspective. The

scope of this study is Bank Muamalat and Bank Syariah Mandiri. These two

18 B. Problem identification

In this research, the writer identify main problem that are:

1. How the social disclosure and reporting in Islamic Bank is?

2. Does Islamic value influence social reporting of Islamic Bank?

C. Study objective and Benefit

Based on the problem identification, it is expected:

1. Study objective

a. To analyze the social disclosure and reporting in Islamic Bank.

b. To analyze the influence of Islamic value to social reporting.

2. Benefit

a. For Shari’ah bank, this study can be a reference whether

Shari’ah bank is compliance with Shari’ah and the Islamic

value has been applied in social reporting.

b. For community, this study gives the information that is related

to Islamic value in bank and its impact.

c. For Islamic Economic development, this study is expected to

19 CHAPTER II

THEORETICAL FRAMEWORK A. Islamic Bank

Islamic Banking act (2008):

“Islamic banking business means banking business whose aims and operations

do not involve any element which is not approved by the Religion of Islam.”

While Ariff (2007:3) defines Islamic bank as an institution that deals in money and its substitutes and provides other financial services. Banks accept

deposits, make loans, derive a profit from the difference in the profits-shares,

and fee incomes that are consistent with the Shari’ah common law principles

governing such a bank. According to Haniffa and Hudaib (2007: 99) Islamic banking refers to a system of banking which is consistent with the principles of Islamic law. Shari’ah bank is one of national banking which operates according to shari’ah principle. Shari’ah prohibits transaction involving

interest (riba), uncertainty (gharar), and unlawful (haram) and it requires muslim to pay zakah. Riba refers to the addition in the amount of the principal of a loan. The prohibition of interest means that Islamic banks cannot incur or

earn interest in any of their financial transactions. Beside that, riba is

prohibiting in Islam because it’s established injustice and exploitation in

economic system. Sulaiman (2003: 6) argue that the moral motive behind the

prohibition of interest is based on the principle of not exploiting the poor and

the needy through charging interest on loans extended to them. According to

20 welfare in society (Al-adl and Al-ihsan) and seeking God’s blessings (Barakah), with the ultimate aim of achieving success in this world and hereafter (Al-falah). It describes that the purpose of Shari’ah is to promote and protect the interest of individuals and societies by bringing benefits and

preventing harm in relation to their necessities needs and wants.

Consequently, the various financial instruments develop by Islamic bank

base on two principles: the profit-and-loss sharing principle and the mark-up

principle (Aggarwal and Yousef, 2000: 95). According to Haniffa and Hudaib

(2007: 100) Financing instruments based on the former principle include

mudharabah (venture capital) and musharakah (partnership arrangement); While instruments based on the latter include murabahah (resale with stated profit), bay’al-salam (forward sale contract), ijarah and ijarah wa iqtina (operating and financial lease) ;

1. Mudharabah is a form of partnership where one party provides the

funds and the other provides the expertise and management.

Mudharabah is based on profit sharing.

2. Musharakah is involving places capital with another person and both

sharing the risk and reward. Musharakah is based on profit and loss

sharing.

3. Murabaha is a contract of sale between a buyer and a seller in which a

seller purchases the goods needed by a buyer and sells the goods to the

buyer on a cost-plus basis. Both the profit and the time of repayment

21 4. Salam is a sale of goods where the price is paid in advance and the

goods are delivered in the future.

5. Istisna’ is a contract for manufacturing (or construction) whereby the

manufacturer (seller) agrees to provide the buyer with goods identified

by description after they have been manufactured or constructed in

conformity with that description within a pre-determined time-frame

and price.

6. Ijara (operating lease) is a form of leasing. It involves a contract where

the bank buys and then leases an item. The duration of the lease, as

well as the basis for rental, are set and agreed in advance

7. Ijarawa- igtina (lease with optional ownership) is another form of Ijara,

except that included in the contract is a promise from the customer to

buy the equipment at the end of the lease period, at a pre-agreed price. B. Islamic Value

According to Chapra (1992: 200) Islamic worldview is based on three

fundamental principles: Tawhid (unity), khilafah (vicegerency, free will & responsibility), and Adalah (justice, equilibrium). Haniffa and Hudaib (2004: 7) argue that there is some important concepts in understanding Islamic

22 1. Tawhid (Unity)

According to Naqvi (1992: 15) unity is a concept where the political, economic, social and religious aspects of an individual's life

are integrated into a homogeneous whole, consistent from within the

individual himself as well as integrated with the vast Universe. The

doctrine of Unity preserves the absolute monotheism of Islam where

God's sovereignty is recognized. This dominates Islamic belief and

practices and consequently affects how Muslims view religion. The

concept of Unity is Tawhid.

Tawhid is the highest principle of Islam. Tawhid is the basis on which the Islamic worldview and strategy are founded. Sulaiman

(2005:3) defines Tawhid as the Unity of God and the belief that the universe is consciously designed and created by God and do not come into existence by chance or accident. Tawhid is the highest principle of Islam. The belief in Tawhid or the oneness of god constitutes the most important principle of an Islamic society. In simple terms, it expresses

the conviction that there is only one source of power that is worthy of

worship and reverence. It also constitutes the basis of all other

principles of the faith. Tawhid is held to arm the faithful against the worship of false gods, such as other men, nations, money or ideas

(Nomani and Rahnema, 1994: 34).

23 of resource mobilization, production and their financing in ways that

bring about complementary linkages between the Shari’ah determined possibilities. The external meaning of Tawhid is now explained in terms of an increasingly relational, participatory and complementary

developmental order wherein possibilities unify among themselves

(Choudhury and Hussain, 2005: 204). According to Nomani and

Rahnema (1994: 35) the traditional and formalistic Islamic man,

concerned only with private Islamic junctions, has to experience three

different forms of liberation before he can transform into an

unalienated social being armed with an Islamic mission that gives

meaning and directions to his life.

First, man has to emancipate himself from all his inner instinctual

sources of temptation. Self-purification or tazkiyah cleanses the individual from attachment to the pleasures of wealth, power, fame and

the sense. This individual and psychological aspect of Tawhid compels the new Islamic want to liberate his oppressed inner self, attaining a

mystical spirit of total freedom and emancipation.

Second, at social level, Tawhid requires the new Islamic man to reject all submission and subservience to other men. In the economic

realm, Tawhid is interpreted as a call to abolish the exploitation of the weak by the strong, for the eradication of feudalism, capitalism, or

24 Third, at the cultural level, Tawhid engages the new Islamic man in a constant struggle against cultural imperialism and blind allegiance to all the fads, fashions and forms of artistic and individual expression

that originate in the west.

2. Khilafah (vicegerency, free will & responsibility)

The concept of Khilafah (vicegerency) defines a person's status and role, specifying the individual's responsibilities to himself and his

responsibility to the ummah. Chapra (1992: 203) suggests four

implications emanating from the concept of khilafah:

The first is universal brotherhood where mutual sacrifice and

cooperation are the social order. Such a social order allows the

development of the entire human potential. Accordingly, from the

perspective of business enterprises, competition is encouraged if it is healthy, raises efficiency, and helps promote the well-being of

society. Competition that results in jealousy, ruthlessness and

destruction must be avoided.

The second implication of khilafah is that the individual is regarded as the trustee for God's resources. This leads to a totally

different meaning to private ownership as understood in the secular

world. Although private ownership is recognized in Islam, ownership

is not absolute. The property owner recognizes his responsibility of

using his resources in a manner that will provide benefits not only to

25 The third implication of khilafah is the emphasis on a humble lifestyle. A lifestyle of extravagance may result in unnecessary pressure on resources which, in turn, may lead to the

inability to satisfy the basic needs of society.

Finally, khilafah also implies the concept of human freedom in Islam. An individual's freedom to act is not curtailed by any other

individual but is constrained by the bonds of social responsibility.

Hence there is a qualification as to what individual freedom entails in

Islam. Unlimited freedom goes hand in hand with unlimited

responsibilities. Consequently, it is inconceivable that anyone would

want unlimited freedom.

3. Al Adl (justice, equilibrium)

Al Adl or justice is a combination of moral and social values denoting fairness, balance, temperance and straightforwardness. There

are three basic criteria for the attainment of social justice:

absolute freedom of conscience, complete equality of all men and

the permanent mutual responsibility of society and individuals. It

follows that if the social behavior pattern and the economy of

Islamic societies are strictly in accordance with Islamic teachings,

there cannot exist extreme inequalities of income and wealth. In

Economics term Al Adl means the profit not only for individual that

can harm people but to society (Karim, 2007: 50). However, Islam

26 efforts, as well as risk. Injustice and Islam are at variance with each

other and cannot coexist without either of the two being uprooted or weakened. Chapra (1992: 210) gives an important framework that

must be discussed:

a. Need Fulfillment

The logical fulfillment of brotherhood and the trust nature of

resources is that these resources must be utilized to satisfy the

basic needs of all individuals and to assure everyone a standard of

living that is compassionate and respectable, and in harmony with the dignity of man inherent in his being the khalifah of God. Since

resources are relatively limited, this goal cannot be actualized

unless claims on the available resources are made only within the

limited of humanity and general well-being. Need fulfillment must

be within the framework of simple-living and, while it should

include comforts, it cannot take the dimension of waste and

snobbery which have been prohibited by Islam but which have

nevertheless become uncontrolled in Muslim countries.

This stress on need fulfillment in Islam received an important

place in the fiqh and other Islamic literature throughout Muslim

history. The jurists have unanimously held the view that it is the

collective duty (fard kifayah) of Muslim society to take care the

27 b. Respectable source of earning

The dignity attached to the status of khalifah implies that need

fulfillment must be through the individual’s own effort;

accordingly, the jurists have emphasized the personal obligation of

every Muslim to earn a living to support himself and his family. Since a Muslim may not be able to fulfill the duty of earning an

honest living unless opportunities are available for

self-employment or unself-employment, it may be inferred that it is the

collective obligation of a Muslim society to ensure for everyone an

equal opportunity to earn an honest living in keeping with his

ability and effort.

Only when these are unable to fulfill their collective

obligation, should the state enter into the picture. This will impose

a smaller economic burden on the Islamic state. The ultimate

objective of all help should be to enable those so helped to stand

their own feet through an increase in their ability to earn more. But

until this becomes a reality, the help must also include income

supplements. Islam has a built-in institutional arrangement to get

the necessary wherewithal for this purpose through the obligatory

28 c. Equitable Distribution of income and wealth

In spite of need fulfillment, there can be extreme inequalities

of income and wealth. Inequalities can be admitted in a Muslim

society primarily insofar as they are more or less in proportion to

skill, initiatives, effort and risk. These are bound to be normally distributed in a society where Islamic teachings are sincerely

followed. Hence Islam not only requires the fulfillment of

everyone’s needs, primarily through a respectable source of

earning, but also emphasizes an equitable distribution of income

and wealth.

The Islamic stress on equitable distribution has been so intense

that there is some Muslims who have held the opinion that equality

of wealth is essential in a Muslim society. It is the general opinion

of Muslim scholars that if the social behavior pattern and the

economy are restructured in accordance with Islamic teachings,

there cannot be extreme inequalities of income and wealth in a

Muslim society.

d. Growth and sustainability

It may not be possible for the Muslim ummah to realize the objectives of need fulfillment and a high level of self-employment

29 rate of economic of growth. Even the goal of equitable distribution

of income and wealth will be realized faster and with smaller sacrifice on the part of the well-to-do if a higher rate of growth is

attained and the poor are enabled to obtain a proportionately larger

share of the fruits of that growth. A better performance in terms of

economic stability will also help reduce the suffering and

inequities that recession, inflation and unpredictable movements in

prices exchange rates necessarily bring about.

4. Halal and haram, ummah, and maslahah

Shariah aspects of Islamic banking and finance revolve around

Shariah requirements. The purpose of the Shari’ah requirements is to ensure that the products are permissible (halal) and to ensure that the trading in them becomes permissible and valid (halal and sahih). According to Deraman Islamic banking products are based on and

developed from permissible (halal) contracts which do not involve gharar, maisir, and riba.

The concept of ummah (community) in Islam implies unity and harmony in social, economic and political affairs. In many Islamic

activists, the notion of ummah is an important and integral part of the

modern Muslim consciousness. While the concept is part of the

Qur’anic revelations, its meaning and usage has evolved with the

30 (2002: 4) Ummah can be viewed at least from two analytical

perspectives.

From the first perspective, the Ummah can be viewed as a

community. In sociology, community types of social organizations are

characterized by social homogeneity, and they are largely based on

primordial and organic ties and have a moral cohesion, often founded

on common religious sentiments. These types of social organizations

are transformed and dissolved by the growing social differentiation

caused by the increasingly complex division of labor, individualism

and modern capitalistic competitiveness, which gives rise to a society

based on associational types of relationships.

From the second perspective, the Ummah can be viewed as a

collective identity. Collective identity is grounded in the socialization process in human societies Individuals develop it by first identifying

with the values, goals and purposes of their society and by

internalizing them. This process, besides constructing the individual

identity, also constructs the collective identity.

As such, Islam gives preference to the needs of the ummah over those of the individuals. Whenever conflict of interest arises, the

needs of the ummah must be met first (maslahah). Therefore,

economic goals must be pursued for the betterment of the ummah.

Haniffa argues (2004: 9) by adhering to Shari’ah Islami’iah, mankind

31 al-haraj), prevention of the forbidden (Daf al-darar) and striving for the

truth (Haqiqiyah) before pursuing self-interest. Such promotion of equality and virtues in society would guarantee the achievement of A l-adl (justice) and Al-falah.

C. Social Reporting: In Islamic Perspective

1. Corporate Social Responsibility

According to Kotler and Lee (2005: 15) Corporate Social Reporting is a commitment to improve community well being through business practices and contributions of corporate resources. Ararat and

Göceno lu (2006: 2) define CSR as institutionalized corporate practices and behavior drives by the acceptance of moral obligation

and accountability for the consequences of corporate activity for all of

the stakeholders and society at large. In the other side, Emily (2008: 3) defines CSR is a voluntary form of regulation over the potentially negative impacts of business activities on society and the natural

environment. According to Al Khater and Naser (2003: 539)

Corporate Social Responsibility is a responsibility of actions which do not have purely financial implications and which are demanded of an

organization under some (implicit and explicit) identifiable contract. In

general term, Corporate Social Responsibility is a voluntary commitment undertaken by a company (or a public institution) to

contribute to the improvement of the environment and society. Thus,

32 aligned with the priorities of sustainable development. It stated in the

UU no 40 2007 about CSR and environment is a company commitment in the economic development (Anshori, 2008: 30).

2. Social Reporting

Social Accountability is the responsibility to account for actions for which one has under an established contract. In the former context,

responsibility must be clearly defined to satisfactorily discharge

accountability arising from that responsibility (Sulaiman and Willet,

2002: 23).

Gray et al (1987: 9) define corporate social disclosure as the process of communicating the social and environmental effects of

organization’s economic actions to particular interest groups within

society and to society at large. At such, it involves extending the accountability of organizations (particularly companies), beyond the

traditional role of providing a financial account to the owners of

capital, in particular, shareholders. Such an extension is predicated

upon the assumption that companies do have wider responsibilities

than simply to take money for their shareholders.

In Islamic perspective, Haniffa and Hudaib (2004: 18) define

disclosure as disclosing information that would aid economic as well as religious decision-making. It means disclosing any information

deemed relevant and should be rightfully given to members of the

33 According to the definition above, it can be concluded that social disclosure is disclosing information concerning the impact of an entity and its activities on society.

Voluntary social reporting is highly valuable exercises for a variety of reasons, not the least of which is its usefulness for experimentation purposes (Gray, 2001: 13). Al-khater and Naser (2003: 540) argue that Corporate Social Responsibility reporting is important to various users of corporate information such as employees,

consumers, local community, and government and its agencies, and

pressure groups and society at large. According to Haniffa and Hudaib

(2004: 17) the purpose of social information is to determine and

communicate to relevant user groups the social impact of business

activities. Besides that, it has a function to determine the effects corporate actions have on the quality of life of society and hence the

emphasis on accountability. As it is generally understood in

non-Islamic accounting, the primary objective of social responsibility

accounting may be similar to Islamic accounting but it should have a

wider focus. Haniffa (2002:141) argues the objectives of social

responsibility and accountability are addressed in both instances but

the underlying principle is different. The concept of accountability in

islam is different as it extends beyond human superiors to God, as

34 Table 2.1

Objectives and ethical statements of Islamic social reports

Objectives:

1. To demonstrate accountability to God and community 2. To increase transparency of business activities by providing

relevant information in conformance to the spiritual needs of Muslims decision makers

Ethical statements: To demonstrate accountability

1. To Strive to provide excellent lawful products/ service as trustee of God

2. To fulfill obligations to God and society

3. To create reasonable profits in conformance with Islamic principles

4. To attain the objectives of the business venture

5. To be just with employees and communities

6. To ensure that business activities are ecologically sustainable 7. To recognize work as form of

workship To demonstrate

transparency

1. To provide information regarding all lawful and lawful activities undertaken

2. To provide relevant information regarding financing and

investment policy

3. To provide relevant information regarding employees policy 4. To provide relevant information

regarding relationships with communities

5. To provide relevant information regarding the use of resources and protection of the

environment

35 3. Scope of disclosure

Haniffa (2007: 101) gives a benchmark of ideal ethical identity based on the Islamic precepts follows that is focus on developmental

and social goals:

Islamic Bank is expected to be more socially responsible than their

conventional counterparts, as Islam emphasizes social justice. One of

the indicators is their contribution to and management of Zakah (religious levy), Saddaqa (charity) and Qard Hassan (benevolent loans) funds. Zakah is one of the five pillars of the Islamic faith and the spending of the proceeds and the beneficiaries are specified in the

Qur’an. However, there have been mixed opinions as to which party is

liable for Zakah: banks or individuals (i.e. shareholders and

depositors). Regardless of who is liable, what is more important is for the Islamic Bank to communicate the following details:

a. A statement showing the sources and the uses of the Zakah fund.

b. The balance of the Zakah fund not yet distributed, and the reasons

for the delay in distribution, if the amount is material.

c. An attestation by the Shari’ah Supervisory Board (either in the

report of the Board or separately) that the amount of Zakah has

been properly computed and these funds have been distributed

36 Unlike Zakah, which is obligatory, Saddaqa (charity) is voluntary in nature and can be used for purposes allowed by Shari’ah for the benefit of society. Hence, Islamic Bank should communicate:

a. The amount and the sources and uses of charity funds, separate

from the Zakah funds.

Public duties in Islam are seen as a part of the general meritorious and

ethical tendency of the faith. The concepts of Ummah, Amanah and Adl stress on the importance of sharing a common goal and removal of hardship in society and this could be achieved via Saddaqa ( charities), Waqf ( trusts) and Qard Hassan ( lending with no profit). As such, Islamic Bank should ideally communicate the following in their annual

reports:

a. The amount and the sources and uses of such funds;

b. The banks’ policies in providing such funds and how

non-repayment of such funds will be dealt with.

Matters on employees should also be given due attention as they are

related to the ethical concept of Amanah and Adl. Employees are the greatest asset of the business and their welfare should be given due

attention. It is the responsibility of employers to ensure that employees

are paid fair wages, not overworked and have the opportunity to fulfill

their spiritual obligations. Equal opportunity is also stressed in Islam.

Hence, the following should be communicated in the annual report:

37 b. Training and development (especially on Shari’ah awareness),

amount spent on training, provision of special training or recruitment schemes.

c. Equal opportunity

d. Reward to employees.

Debtors receive special attention in Islam. Lenders are asked to be

lenient with their debtors and in certain circumstances, debtors are

entitled to receive Zakah and debts should be written off as charity. As

such, Islamic Bank is expected to demonstrate and communicate such

commitments in their annual reports:

a. Debt policy and type of debt

b. Amount of debts written off.

Public duties in Islam are seen as a part of the general meritorious and ethical tendency of the faith. The circumstantial needs of the

community within which the Islamic Bank operate should first be

catered to. Hence, Islamic Bank should ideally communicate the

following to indicate their commitments to society:

a. Creating job opportunities;

b. Supporting organizations that benefit society and participating in

government social activities;

38 D. Benchmark for Social Disclosures by Islamic Banks

Maali et al (2006: 272) assert that Fundamental to an Islamic perspective on social reporting is an understanding of the concepts of accountability, social justice and ownership that are central to social relations.

1. Accountability

Al-Khater and Naser (2003: 540) define accountability as the relationship between two parties, the accounter and the accountee, when the latter is accountable to the former for his/her activities and the consequences.

Gray (2001: 11) defines accountability as identifying what one is responsible for and then providing information about that responsibility to those who have rights to that information.

Al-Khater and Naser (2003: 540) refer to three basic elements of the accountability concepts.

a. The accountee has an obligation to provide the accounter detailed information.

b. The responsibilities of those who are held accountable for their action and the consequences must be spelled out clearly.

c. Stating accounts of action and related consequences will be used by the accounter as a yardstick to assess the accountee. This is expected to have implications for his/her decisions.

Yet accountability also has broader economic and social purposes,

39 politics, religious and social affairs, especially accounting, fall under

the jurisdiction of the divine law of Islam, the Shari’ah (Lewis, 2006:2)

The Islamic view of accountability creates different objectives for

accounting and reporting. Napier (2007: 10) divides the Islamic view

of accountability based on two main themes. The first of these is the

concept of Tawhid. Baydoun and Willett (1997: 6) argue that the concept of the unity of God gives rise to a different and broader concept of accountability than that implied by Western models

In the Islamic framework, all people are accountable to God on the

Day of Judgment for their actions during their lives. The second main

theme is the concept of ownership in Islam. God has appointed man

his vice-regent (Khalifa) on earth and entrusted him with stewardship of God’s possessions. This does not imply that Islam does not

recognize private ownership. Everyone has the right to own property,

but the ownership is not absolute. (Napier, 2007: 10).

In a business enterprise, both management and the providers of

capital are accountable for their actions both within and outside their

firm. Accountability in this context means accountability to the

community (Ummah) or society at large (Lewis, 2006:2).

2. Social Responsibility and Justice

Individuals are expected to feel socially responsible for others in

40 to allow people to earn their living in a fair and profitable way without

exploitation of others, so that the whole society may benefit. Islam also emphasizes the welfare of the community over individual rights

(Lewis, 2006:4).

Responsibility sets limits to what man is free to do by making him

responsible for what he does and as such. In Islam, there should be no

contradiction between individual freedom and collective freedom. The

difference between the two is bridged by the sense of social

consciousness and Responsibility (Sulaiman, 2005: 7).

Islam stresses the concept of social responsibility. The term ‘brotherhood’ (Akhowa) is widely used in Islamic societies. In this context, justice refers to being fair with everyone (Maali et al, 2006: 272). Justice in Islam also includes the equitable distribution of wealth. The prohibition of Riba (Usury), Infaq, the requirement to pay Zakah

and the provision of Qard Hassan (interest-free loans) are clear examples of the Islamic emphasis on social justice (Maali et al, 2006: 272). Infaq emphasizes benevolence by voluntarily spending one’s wealth on the poor and the needy, while the various institutions are

considered as formal obligations for all Muslims. The most

important institution for the equitable distribution of wealth is the alms

tax (Zakah). It is one of the pillars of Islam that requires each Muslim to pay a fixed minimum percentage over his or her wealth, property as

41

requirement to deal justly encompasses all dealings with employees, customers and all members of the society in which these businesses operate (Maali et al, 2006: 272).

3. Ownership and Trust

Islam perceives ownership as a trust (Amanah). There is no an absolute ownership for human beings, rather it is relative. A part of

one’s assets is a right of other people (Triyuwono, 2004: 4).

In Muslim trade, the concept of Amanah (trust) is significant. Amanah comes very close to the concept of fiduciary responsibility and stewardship function (Malik et al, 1999: 4). This trustee-ownership principle implies that ownership should be exercised for the benefit of society as well as for the benefit of the owner (Maali et al, 2006: 272).

God’s commandments and the benefits of society should be given priority when dealing with properties. The owner is responsible for using the available resources according to the will of God and to the benefit of society.

According to Maali et al (2006: 16) there are three broad objectives that can be set as the bases for identifying the social disclosures of

Islamic business enterprises:

1. To show compliance with Islamic principles, in particular dealing

justly with different parties.

2. To show how the operations of the business have affected the

42 3. To help Muslims to perform their religious duties.

Such objectives will now be used as the basis for proposing a benchmark for social reporting by Islamic banks.

Maali et al (2006: 16) set out the number of items that should be disclosed in islamic banks’ annual reports.

1. Disclosure of Shari’ah Supervisory Board opinion

One distinct feature of the modern Islamic banking movement

is the role of the Shari’ah board, which forms an integral part of an

Islamic bank. A Shari’ah board monitors the workings of the

Islamic bank and every new transaction that is doubtful from a

Shari’ah standpoint has to be cleared by it. Therefore, the first

measure that an institution is in compliant with Shari’ah is to

appoint a Shari'ah Supervisory Board (SSB) or Shari'ah Supervisory Committee (SSC).These boards include some of the

most respected contemporary scholars of Shari’ah and the opinions

of these boards are expressed in the form of fatwas. The users of

Islamic banks’ annual reports will interest in the report of the

Shari’ah Supervisory Board because it shows whether the bank has

complied with Islamic principles or not and whether it has dealt

justly with different parties.

2. Unlawful transactions

Islamic banks should not enter into any transaction that

43 uncertainty in contracts example entering into a transaction whose

consequence is out of usual trade norms. Hence, any contract base on a future uncertain event such as hedging, dealing in derivatives,

etc, within Islamic banking, is not generally allowable. Where a

bank is entered into transactions that are inconsistent with Shari’ah

principles, and hence regarded as unlawful (Haram) by Islam, the

duty of accountability to God and society implies that information

about these transactions should be disclosed to the community. It

considers that the bank should disclose the following:

a. The nature of these transactions

b. The reasons for undertaking such transactions

c. The opinion of the Shari’ah Supervisory Board regarding the

necessity of undertaking such activities

d. The amount of revenue (expenses) earned (paid) in such

transactions

e. How the bank disposed, or intends to dispose, of such revenues

f. Disclosing such items would help the Islamic community in

assessing whether the bank has violated Islamic principles and

the reasons for such violation. In addition, disclosure will help

in assessing the materiality of such prohibited transactions, and

hence the magnitude of the impact on the well-being of the

44 3. Zakah

Zakah is a tax that every Muslim, whose wealth exceeds a certain nisab (minimum amount), has to pay. The Shari'ah specifies

that only individuals are liable for zakah. It is the individual

owners who are responsible for determining the amount that should

be paid out as zakah (Gambling and Karim, 1991:103).

Islamic banks may be required by law to pay zakah or the

shareholders and/or the depositors may require a bank to pay zakah

on their behalf. For those banks that are required by law or their

shareholders to pay zakah, Islamic Bank should ideally

communicate the following in their annual reports:

a. A statement showing the sources and the uses of the zakah

fund. This statement will show from which sources the funds were collected (shareholders, depositors, others) and to which

uses they have been applied. It is important to provide detailed

disclosures of such uses to assure readers of annual reports that

these funds is used according to God’s will.

b. The balance of the zakah fund not yet distributed, and the

reasons for the delay in distribution, if the amount is material.

c. An attestation by the Shari’ah Supervisory Board (either in the

report of the Board or separately) that the amount of zakah is

properly computed and these funds are distributed according to

45 4. Qard Hassan

Qard Hassan is a non-profit bearing financing intended to allow the borrower to use the loaned funds for a period of time with the understanding that the same amount of the loaned funds will be repaid at the end of the Qard period (Haniffa and Hudaib, 2004: 25). Qard Hassan is a sort of loan which does not require borrowers to pay interest or even someparts of profits earned from

their businesses, except repaying the principal loan to the banks

(Triyuwono, 2004: 9).

Providing Qard Hassan (benevolent or interest-free loans)

for socially beneficial causes is an important social contribution

that Islamic Bank may make, especially to the local community in

which they operate. As such, Islamic bank should ideally communicate the following in their annual reports:

a. The sources from which such loans are financed: these sources

may include the bank own funds and depositors’ funds. Users

need to know whether the bank finances such activity from its

own resources or from the depositors’ resources, and whether

or not the bank operates a formal scheme whereby depositors

may designate funds to be used for Qard Hassan.

b. The amount advanced to beneficiaries during the year, and the

purposes for which these loans were given.

46 d. Its policy for dealing with those who are unable to repay their

loans.

5. Charity and other social activities

In addition to Qard Hassan, Islamic banks should engage in

other social activities, such as making charitable donations

(charity) is voluntary in nature and can be used for purposes

allowed by Shari’ah for the benefit of society (Haniffa and Hudaib, 2004: 25). It is not obligatory but strongly recommended Islamic banks, which usually control large funds, are expected to

participate in providing such charitable donations. Islamic society

and the stakeholders of the bank should know about the bank’s

contribution to the well-being of society and whether the bank

fulfils society’s expectations regarding this issue. Rather, such activities should be genuine, and not undertaken for publicity

purposes. We therefore recommend that Islamic Bank should

disclose:

a. The nature of charitable and social activities financed by the

bank

b. The amount spends on these charitable and social activities.

c. The sources of funds use for charity: the sources may include

the bank’s own funds and revenues from sources prohibited by

Shari’ah

47 Other revealing indicators of an organization’s ethical stand

from an Islamic perspective are the ways it treats its employees and debtors as well as its commitments to society. Employees are the

greatest asset of the business and their welfare should be given due

attention.

The Islamic community needs to know if the bank deals

justly with its employees: exploitation and discrimination are not

acceptable, as these are strictly prohibited by the Qur’an and

Sunah. In addition, education and training are important as Islam

encourages the search for knowledge. So, the bank must disclose:

a. Payments of wages and bonuses.

b. Education and training for employees.

c. Equal opportunities. d. The working environment.

7. Late repayments and insolvent clients

Islamic banks, when utilizing mark-up financing

arrangements such as Murabaha and Ijara, may face situations in

which clients are unable to pay amounts when they fall due.

It will expect users to be interested in how the bank deals

with insolvent clients, and whether the bank deals with them in an

ethical way, consistent with Islamic principles. Therefore, it

considers that the Islamic bank should disclose:

48 b. The amounts charged as late penalties, if any.

c. The opinion of the Shari’ah Supervisory Board regarding whether charging penalties is permissible.

d. How the bank deals with such penalties (allocation to charity or

revenue).

8. The environment

Destruction or damage of the physical environment, if it is

considered harmful to an individual or community, is prohibited in

Islam. As Haniffa (2001:18) observes that there are about 500

verses in the Qur’an giving guidance on matters related to the

environment and how to deal with it, which indicates the

importance of taking care of the environment.

Banking is unlikely to cause direct harm to the environment in the way that the oil and nuclear industries might, but Islamic

Bank is not expected to finance activities that lead to harming the

environment, because such projects will harm the Islamic society.

In addition Islamic Bank is able to provide donations to help

preserve the environment. Users will require assurance that the

activities of Islamic Bank affect positively the wellbeing of the

Islamic society. Therefore it is expected that Islamic Bank report

on the following issues:

a. The amount and nature of any donations or activities

49 b. Disclosures indicating whether the bank has financed any

projects that may lead to harming the environment. 9. Other community involvement aspects

In addition to their zakah and charitable activities, Islamic

Bank is expected to undertake other activities which enhance the

well-being of the Islamic community in which the Islamic Bank is

allowed to operate and make profits. Thus, Islamic Bank should

respect the requirements of their community. Because of this,

Islamic Bank should give priority in their investments to those areas

that help in solving the problems of the society, even if this will

lead the Islamic Bank to sacrifice some of their profits. Thus, it is

expected that Islamic Bank will disclose its role in:

a. Enhancing economic development in the communities in which it operates.

b. Solving the social problems (such as housing and literacy) of the

50 CHAPTER III

RESEARCH METODOLOGY A. Scope of Research

Scope of this research is on social reporting in annual report of

Islamic bank. Using Haniffa and Maali et all benchmark, this research will

evaluate annual report of Islamic bank to determine the item that is

disclosed by Islamic bank.

B. Sampling Method

Sample that will be collected in this study is annual report of bank period of year 2003-2007 (Syariah Mandiri Bank and Muamalat Bank).

The reason of using that period is based on the effective of accounting

standard in Indonesia (PSAK no 59) which is on January 1, 2003. After

the effective of PSAK in year 2003, Shari’ah Bank in Indonesia has its own accounting standard in disclose their operation.

C. Data Collection Method

Process data collection will be done by collecting the annual report of

bank period of year 2003-2007. Data collection is obtained from the

website of both banks. In order to gain information that will support this

research, hence technique data distribution is library research. This

research is used in order to collect data from present literature, past

research and other information that related to the topic of this research.

The type of data that will be collected and used in this research is

51 related or relevant to the variable of the research (books, journals, articles,

internet and other media information). D. Data Analysis Method

This research uses analysis variance (ANOVA). According to

Faraway (2002: 169) ANOVA is a hypothesis-testing procedure that is used to evaluate mean differences between two or more treatments (or

populations). ANOVA is used because its original thinking is trying to

partition the overall variance in the response to that due to each of the

factors and the error. In ANOVA independent variable is called a factor. In

this research the independent variable is one, therefore this research uses

one-way ANOVA.

The result of one-way ANOVA test gets F test result. F-test is any statistical test in which the test statistic has an F-distribution if the null hypothesis is true. The F distribution has two degrees of freedom, d1 for

the numerator, d2 for the denominator. For each combination of these

degrees of freedom there is a different F distribution. Test of ANOVA will

indicate the influence of independent variable toward dependent variable if

the computed value is larger than the critical value.

The variables in this research are measured using dummy variables since most of the variables are qualitative in nature. According to Amran

and Devi (2004: 21) dummy variables can be incorporated in the

52 that a regression model may contain variables that are all exclusively

dummy, or qualitative in nature.

To know the influence of Islamic value towards social reporting,

this research uses linear regression model. Lind et al (2005: 440)

Regression equation is an equation that expresses the linear relationship

between two variables.

General form of linear regression equation is

Y= a + bX + et

Where:

Y = Predicted value of the Y variable for a selected X value (social reporting)

a = Estimated value of where the regression line crosses the

Y- axis when X is zero.

b = Slope of the line, or average change in Y for each change of one unit in the dependent variable X.

X = Any value of the independent variable that is selected (Islamic value).

et = Error term

In this research, Islamic value is a dummy variable. In order to use

this variable using linear regression, it needs to know the quantifiable

variable to make researchable. This research use 1 for any Islamic value

had by Islamic bank and 0 for none.

53 H0: Islamic value not influence social reporting

HA: Islamic value influence social reporting

In order to calculate linear regression for this research uses

quantitative analysis. Quantitative analysis gives the information and

explanations on the coefficient determination and T-test to answer the

formulation of the problems;

1. Coefficient determination

Coefficient determination is the proportion of the total variation in the dependent variable Y that is explained, or accounted for by the

variation in the independent variable X. The coefficient determination

measures the strength of independent variable influence the dependent

variable. The value of coefficient determination is 0 and 1. The small

value of R2 means the limited ability of independent variable to explain dependent variable. Value of R2 that approaches to 1 means

independent variable almost gives all the information to predict

dependent variable.

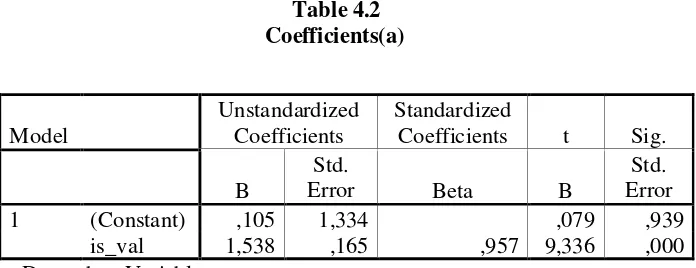

2. T-test

T test is aimed to understand how big the influence each independent variables individually/ partially towards dependent

variable. According to Bhuono (2005:54) the result of this t-test is

from the output of SPSS by looking at the table of coefficients. The

score from t-test can be seen from p-value (in the sig column) in each

54 significant that has been determined, or t-test (in t column) larger than

t-table (counting from two tailed α = 5% df = n – k, k is a total

independent variable.

E. Operational Variable

In understanding the research, therefore it must be an understanding in

the variable of the research:

1. Independent Variable

The independent variable is Islamic value which follows the

benchmark of Haniffa (2002: 101). Haniffa benchmark considers in developmental goals that relate with Islamic value. The independent

variable is variable that will influence the other variable.

2. Dependent variable

Dependent Variable is variable that changes because of the

independent variable. The dependent variable is social reporting which

55 Table 3.1

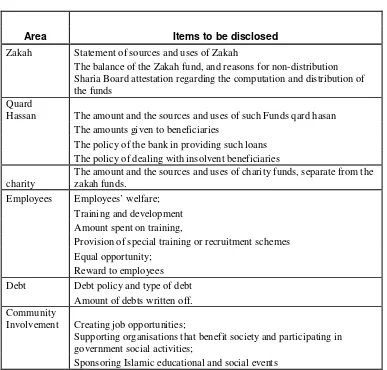

Instrument of Independent Variable

Area Items to be disclosed

Zakah Statement of sources and uses of Zakah

The balance of the Zakah fund, and reasons for non-distribution

Sharia Board attestation regarding the computation and distribution of the funds

Quard

Hassan The amount and the sources and uses of such Funds qard hasan

The amounts given to beneficiaries

The policy of the bank in providing such loans

The policy of dealing with insolvent beneficiaries

charity

The amount and the sources and uses of charity funds, separate from the zakah funds.

Employees Employees’ welfare;

Training and development

Amount spent on training,

Provision of special training or recruitment schemes

Equal opportunity;

Reward to employees

Debt Debt policy and type of debt

Amount of debts written off.

Community

Involvement Creating job opportunities;

Supporting organisations that benefit society and participating in government social activities;

Sponsoring Islamic educational and social events

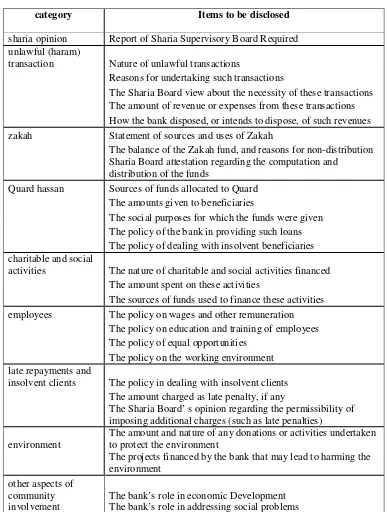

56 Table 4

Instrument of Dependent Variable

category Items to be disclosed

sharia opinion Report of Sharia Supervisory Board Required

unlawful (haram)

transaction Nature of unlawful transactions

Reasons for undertaking such transactions

The Sharia Board view about the necessity of these transactions

The amount of revenue or expenses from these transactions

How the bank disposed, or intends to dispose, of such revenues

zakah Statement of sources and uses of Zakah

The balance of the Zakah fund, and reasons for non-distribution

Sharia Board attestation regarding the computation and distribution of the funds

Quard hassan Sources of funds allocated to Quard

The amounts given to beneficiaries

The social purposes for which the funds were given

The policy of the bank in providing such loans

The policy of dealing with insolvent beneficiaries

charitable and social

activities The nature of charitable and social activities financed

The amount spent on these activities

The sources of funds used to finance these activities

employees The policy on wages and other remuneration

The policy on education and training of employees

The policy of equal opportunities

The policy on the working environment

late repayments and

insolvent clients The policy in dealing with insolvent clients

The amount charged as late penalty, if any

The Sharia B