www.elsevier.com/locate/dsw

Control limit policies in a replacement model with additive

phase-type distributed damage and linear restoration

David Perry

Department of Statistics, University of Haifa, Mt. Carmel, 31905 Haifa, Israel

Received 1 September 1998; received in revised form 1 January 2000

Abstract

We consider a replacement model for an additive damage process with linear restoration. The replacement policy is of the control limit type. Between replacements the damage level process is modeled as a compound Poisson process with positive jumps and negative drift, reected at 0. We introduce meaningful cost functionals for this system and determine them explicitly for three special cases when the jumps have a phase-type distribution. c 2000 Published by Elsevier Science B.V. All rights reserved.

Keywords:Replacement model; Additive damage; Self restoration; Martingale stopping theorem; Phase-type distribution

1. Introduction

We consider a system working in a random environment that receives shocks at random points of time. Each shock causes a random amount of damage which accumulates over time. The damage process is controlled by means of a maintenance policy which causes the damage to decrease according to a piece-wise linear state-dependent restoration rate function r(x) = 1 for x ¿0 and r(0) = 0. Thus, a breakdown can occur only upon the occurrence of a shock. Upon failure the system is replaced by a new identical one with a given cost. When the system is replaced before failure, a smaller cost is incurred, so that there is an incentive to attempt to replace the system before failure.

It was shown in [13] that for a model the optimal replacement policy is a so-called control limit level policy (CLL). That is, since record values occur only at times of shock arrivals there exists a certain critical level

such that the system is replaced once the damage process upcrosses it. Posner and Zuckerman [13] have shown that under natural assumptions the CLL policy is optimal for a large family of cost functions. However, they were only able to nd the control limit by binary search. Perry and Posner [11], in a subsequent paper, restricted themselves to the case that the damage process is a regenerative process for which in each cycle

E-mail address:[email protected] (D. Perry).

the shocks are exponentially distributed and arrive in accordance with a compound Poisson process. Under these assumptions they extended the analysis to determine the optimal CLL for a certain cost function.

However, the assumptions made by Perry and Posner [11] are too restrictive. Firstly, their cost function includes only xed, but not proportional maintenance costs. Secondly, they introduce explicit expressions for the cost functionals only for the case of exponential jumps.

This paper is an extension of Perry and Posner [11] in the sense that these two restrictive assumptions are re-moved. We add the proportional maintenance costs component to the cost function, and also, we make the rst step towards generalization by assuming that the jump sizes have a phase-type distribution. Strictly speaking, we consider three special cases of phase-type distributions: exponential, Erlang (2; ) and hyperexponential.

For the past three decades many researchers and practitioners have shown interest in the study of mainte-nance models for systems with stochastic failures using CLL policies (see Aven and Gaarder 1987, [20,23], the survey papers of Valdes-Flores and Feldman [21], Pierskalla and Voelker [12] and the references therein). One major reason for this is that maintenance models can be applied to a variety of stochastic models such as queues, inventories and insurance risk. For example, replacement can be interpreted as “disaster” or work removal by negative customers [4,7,8] in queueing models. It can be interpreted as an action of clearing in inventory models [14,18]. Under certain circumstances, it can be interpreted as a bankruptcy in insurance risk models [1, Chapter III]. Indeed, the damage level process, as dened in this study, is a regenerative process that can stay in zero for some time (this period of time is called an idle period). The risk process, in the insurance risk model is “killed” at the time of bankruptcy. The circumstances mentioned above represent the fact that the time to bankruptcy in the risk process can be interpreted as an arbitrary cycle whose idle period is deleted. According to the CLL policy, the system is replaced once a certain level is upcrossed by the additive damage process. From a modeling point of view, our problem belongs to the family of rst exit-time problems [2,3,5,6,15 –17,24]. A key study in the area of additive damage is the paper by Taylor [19] in which he assumed that the damage process is a compound Poisson process. Aven and Gaarder (1987) extended his paper in a dierent direction. They also assumed that the cumulative damage is generated only by shock sizes; however, the system cannot restore the damage as time progresses.

In Section 2, we introduce the dynamics of the damage process and the cost functionals. Explicit expressions for the cost functionals are obtained in Section 3 for the exponential jump case, in Section 4 for the Erlang (2; ) jump case and in Section 5 for the hyperexponential jump case. In Section 6, we introduce some numerical results and nally, in Section 7 we lay the ground for further research.

2. The model

LetW={W(t):t¿0} be the additive damage level process. We assume thatW is a Markov jump process in which the shocks arrive according to a Poisson process with rate . Due to maintenance operation, we assume (without loss of generality) that the damage level process decreases at rate r(W(t)) = 1 whenever

W(t)¿0 and r(0) = 0. A failure occurs once the damage level upcrosses a certain level #0. Upon failure the system is replaced by a new identical one and the replacement cycles are repeated indenitely. Each replacement costsC dollars and each failure adds an additional cost of K dollars. Thus, there is an incentive to attempt to replace the system before failure. We allow the controller to replace the system at any stopping timeT6 where is the failure time of the system. In addition, we assume proportional maintenance costs. It has been shown by Posner and Zuckerman [13] that the optimal replacement policy is that of the CLL. That is, there exists an optimal level 0¡ ¡ #0 such that whenever W upcrosses , the system is replaced and a new cycle starts, so that W is a regenerative process, and each cycle starts with damage level 0. We dene the cycle length by T and note that failure may occur at the end of a cycle with a positive probability

p. Formally, let {N(t):t¿0} be a Poisson process with rate and dene

where the Vi’s are i.i.d. random variables having Laplace transform (LT)(). Dene cycle is a probabilistic replication of the stopped reected process{Z(t): 06t6T}, so that the stopping time

T can be dened also with respect toW. Each cycle of W starts from 0, T is a point of discontinuity and 0 =W(T+)6W(T−)¡ W(T).

An upcrossing of level can also be an upcrossing of level #0(¿ ). As mentioned, this event occurs with probability p. That it, p is the probability that the end of the cycle is the failure and q= 1−p is the probability for replacement before failure. Obviously, p is a function of the decision variable . Since is composed of a geometric number of cycles, it is clear that E() =E(T)=p. In order to dene the expected discounted costs over an innite horizon, letT1=T andTn+1= inf{t ¿ Tn:W(t)¿}. That is, Tn is the end

of the nth cycle. Dene the cost function

R=E

where is the discount factor and hdW(t) is the proportional maintenance cost per time unit if the damage level is W(t) at the time interval dt.

Since W is a regenerative process, R can be trivially expressed in terms of three cycle cost functionals.

This is done in the following lemma.

Lemma 1. Let

To derive the cost functionals of Lemma 1 we will use a martingale {M(t): t¿0} that was introduced by Kella and Whitt [9] in another context (see also [10] for a Brownian inventory application). As will be seen, the martingale used by Perry and Posner [11] can be obtained as a special case of M(t).

Lemma 2 is restricted to the case that Z(t) is a reected compound Poisson process, and we use the martingale for a simple rst passage stopping time T. Thus, EM(T) =EM(0) by the optional sampling theorem and since {Z(t):t6T} represents an arbitrary cycle of W we obtain

Then, Eq. (2.4) can be written as

’(; )E

By substituting the roots of (3.2) in the fundamental equation (2.7), the left-hand side of (2.7) vanishes and we obtain two equations with two unknowns:

1 = e−1()

Note that (3.5) is the cost functional A1() of Lemma 1. Clearly, by the memoryless property,

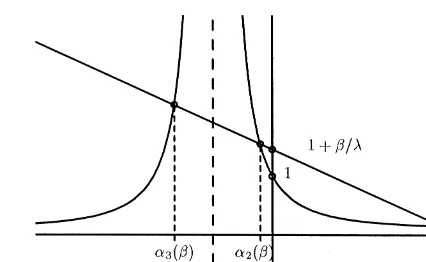

Fig. 1. Roots of’(; ) in theErl(2; ) case.

so that

A2() = e−(#0−)A1(): (3.7)

To obtain A3() divide both sides of (2.7) by ’(; ), take the derivative with respect to and set = 0. We nd that

A3() =(1−(=))A1() +((1=) +−())

2 : (3.8)

The functionals A1() andA2() (but notA3()) have already been obtained in [11].

4. Erlang jumps

Assume now that the shock sizesVi∼Erl(2; ) so that () = (=(+))2. Substituting in (2.5) we have

’(; ) =− 1−

+

2!

−: (4.1)

Lemma 3. For ¿0 the function ’(; ) has three real roots

1()¿0¿ 2()¿− ¿ 3():

Proof. The three real roots of ’(; ) are the three match points of the function (=(+))2 and the linear function (of ), 1 + (=)−(=), as seen in Fig. 1.

Remark 1. It is required that all terms of (2.7) are well-dened at the roots i(); i= 1;2;3. Apparently,

3() is obtained outside the domain of convergence of the LT (=( +))2 since 3()¡−. How-ever, the function ’(; ) is analytic on C\ {−}. The integral RT

0 e

−W(s)−sds is easily seen to be an

analytic function of for all ∈ C. Thus, after multiplication by + Eq. (2.7) becomes an iden-tity between analytic functions which holds for ¿− and thus, by analytic continuation, for all ∈

C\ {−}, in particular for =i(); i = 1;2;3. The same problem already occurs in the exponential

case.

It is assumed that the shock sizes Vi∼Erl(2; ), which is the convolution of two exponential () phases.

jump, or W(T)−∼ exp() if is upcrossed by the second phase of the jump. Let E1 (E2) be the event that is upcrossed by the rst (second) phase of the jump. Then

Ee−W(T)−T= e−

+

2

1() + e−

+2(); (4.2)

where

1() =E(e−T1{E1}) (4.3)

and

2() =E(e−T1{E2}): (4.4)

Clearly, by the memoryless property the occurrence of E1 implies that W(t)−∼Erl(2; ) and E2 implies that W(t)−∼ exp().

Substituting =i() on the left-hand side of (2.7) fori= 1;2;3, and then (4.2) – (4.4) on the right-hand

side, we obtain three equations with three unknowns:

1 =ai()1() +bi()2() +i()(); i= 1;2;3; (4.5)

where

ai() = e−i()

+i()

2

and bi() = e−i()

+i()

:

Eq. (4.5) is a simple system of three linear equations whose solution is easily available via MATHEMATICA. However, the explicit formulas are lengthy and not very illuminating.

For the three cost functionals we have

A1() =1() +2(); (4.6)

A2() = e−(#0−)[1()(1 +(#0−)) +2()] (4.7)

and

A3() =[(+ (1=))A1() + (1=)1() +()]−(1−p)(1−A1())

2 : (4.8)

Remark 2. According to (4.6), A1() is composed of the two cost functionals 1() and 2() for some xed discount factor. However,1() and 2() are also improper LTs. Therefore, 1(0) and 2(0) are the probabilities to upcross level by either the rst phase or the second phase ofW(T)−, respectively. Thus, by substituting = 0 in (4.7) we obtain the probability p that a replacement is also a failure.

5. Hyperexponential jumps

It is easy to show (although not obvious at rst glance) that the simplest hyperexponential distribution (namely, the mixture between two exponential distributions) is also of phase-type (see [22, p. 269]). We have

() =

++ (1−)

+: (5.1)

Namely, for some known 0¡¡1 the jump size is a mixture of two exponential random variables; one

with parameter and one with parameter , and assume, without loss of generality, that ¿ . The function

’(; ) for this case is dierent from that of Section 4 but Lemma 3 is still applicable in the sense that

’(; ) has three real roots 1()¿0¿ 2()¿− ¿ 3()¿− for all¿0. These three roots are the three match points between () of (5.1) and the linear function 1 + (=)−(=) as can be seen in Fig. 2.

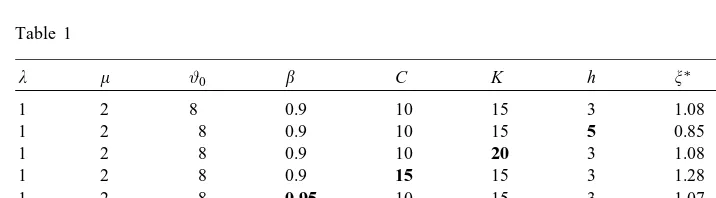

Fig. 2. Roots of’(; ) in the hyperexponential case. Table 1

#0 C K h ∗ R∗

1 2 8 0.9 10 15 3 1.08 5.09

1 2 8 0.9 10 15 5 0.85 7.20

1 2 8 0.9 10 20 3 1.08 5.09

1 2 8 0.9 15 15 3 1.28 5.77

1 2 8 0.95 10 15 3 1.07 4.88

1 2 12 0.9 10 15 3 1.08 5.09

1 4 8 0.9 10 15 3 0.74 1.36

2 2 8 0.9 10 15 3 1.47 8.25

6. Numerical results

The whole analysis is carried out to nd the optimal control level ∗. However, in practice the goal can be achieved only numerically. The expressions of the cost functionals, even in the case of exponential jumps, are too cumbersome for mathematical analysis. In this section we focus on the exponential case and provide some numerical results with respect to the objective function R as given in Lemma 1. Starting with the base

values of the parameters as

= 1; = 2; #0= 8; = 0;9; C= 10; K= 15; h= 3

we note rst that R is a convex function whose minimum is obtained at ∗= 1:08 and R∗= 5:09. In Table

1 below we have varied the parameters one at a time (shown in bold) to see the eect of this variation. For example, increasing the rate of arrival , as well as decreasing the value of , results in an increase of

R. However, R is insensitive with respect to the parameters #0 and K. There is a low sensibility with the parameters andC and high sensibility withh. The changes of the parameters and the objective functionR

are all in directions which agree with intuition.

7. A concluding remark

Indeed, the three applications presented in Sections 3–5 are the simplest cases of phase-type distributions. However, if we apply our approach to the case that the jump size ∼Erl(n; ), Eq. (2.7) should lead to n+ 1 equations, possibly generated by the roots of the function

’(; ) =−

However, in the case that the jump size ∼ Erl(n; ) we have only two match points between the linear function 1 + (=)−(=) and the LT() = (=(+))n. These two match points are the two real roots at

’(; ). Thus, there must also be n−1 extra complex roots. This problem is now under investigation.

References

[1] S. Asmussen, Applied Probability and Queues, Wiley, New York, 1987.

[2] S. Asmussen, D. Perry, An operational calculus for matrix-exponential distribution with an application to a Brownian (q; Q) inventory problem, Math. Oper. Res. 23 (1998) 166–176.

[3] T. Aven, S. Gaarder, Optimal replacement in a shock model: discrete time, J. Appl. Probab. 24 (1987) 281–287.

[4] R.J. Boucherie, O.J. Boxma, The workload in theM=G=I queue with work removal, Probab. Eng. Inform. Sci. 10 (1996) 261–277. [5] J. De Lucia, H. Vincent Poor, The moment generating function of the stopping time for a linearly stopped Poisson process, Stochastic

Methods 13 (1997) 275–292.

[6] S.F.L. Gallot, Absorption and rst-passage times for a compound Poisson process in a general upper boundary, J. Appl. Probab. 3 (1993) 835–850.

[7] E. Gelenbe, Product form queueing networks with negative and positive customers, J. Appl. Probab. 28 (1991) 656–663. [8] G. Jain, K. Sigman, Generalization of Pollaczek-Khintchine formula to account for arbitrary work removal, Probab. Eng. Inform.

Sci. 10 (1996) 519–531.

[9] O. Kella, W. Whitt, Useful martingales for stochastic storage processes with Levy input, J. Appl. Probab. 29 (1992) 396–403. [10] D. Perry, A double band control policy for a Brownian perishable inventory system, Probab. Eng. Inform. Sci. 11 (1997) 361–373. [11] D. Perry, M.J.M. Posner, Determining the control limit policy in a replacement model with linear restoration, Oper. Res. Lett. 10

(1991) 335–341.

[12] W.P. Pierskalla, J.A. Voelker, A survey of maintenance models: the control and surveillance of deteriorating systems, Nav. Res. Logistics Quart. 23 (1976) 353–388.

[13] M.J.M. Posner, D. Zuckerman, A replacement model for an additive damage model with restoration, Oper. Res. Lett. 3 (1984) 141–148.

[14] R. Serfozo, S. Stidham, Semi-stationary clearing processes, Stochastic Process. Appl. 6 (1978) 165–178. [15] W. Stadje, Optimal stopping in a cumulative damage model, OR Spektrum 13 (1991) 31–35.

[16] W. Stadje, Distribution of rst exit times for empirical counting and Poisson processes with moving boundaries, Stochastic Methods 9 (1996) 91–103.

[17] W. Stadje, D. Zuckerman, Optimal repair policies with general degree of repair in two maintenance models, Oper. Res. Lett. 11 (1992) 77–80.

[18] S. Stidham, Clearing systems and (s; S) inventory systems with non-linear costs and positive leadtimes, Oper. Res. 34 (1986) 276–280.

[19] H.M. Taylor, Optimal replacement under additive damage and other failure models, Nav. Res. Logistics Quart. 22 (1975) 1–18. [20] C. Tilquin, R. Cleroux, Periodic replacement with minimal repair at failure and adjustment costs, Nav. Res. Logistics Quart. 32

(1985) 243–284.

[21] R.C. Valdez-Flores, R.M. Feldman, A survey of preventive maintenance models for stochastically deteriorating single-unit systems, Nav. Res. Logistics Quart. 36 (1989) 419–446.

[22] R.W. Wol, Stochastic Modeling and the Theory of Queues, Prentice-Hall, Englewood Clis, NJ, 1989.