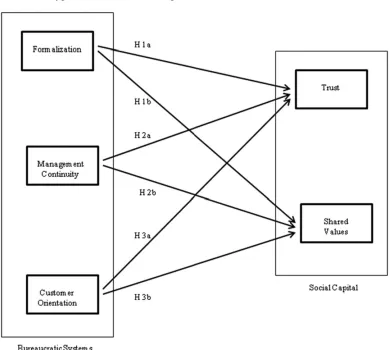

Bureaucratic Systems’

Facilitating and

Hindering Influence

on Social Capital

Patrick A. Saparito

Joseph E. Coombs

This study demonstrates how banks’ bureaucratic systems (i.e., formalization, management continuity, customer orientation) are associated with social capital’s relational and cognitive dimensions. We collected survey data from a matched sample of 884 small- and medium-sized enterprises (SME) executives and 217 bank managers across 22 banks to test hypoth-esized relationships. Our results showed that formalization is negatively associated with both dimensions of social capital, while management continuity and customer orientation are positively associated with them. These results are a first step in answering calls in the literature to study bureaucratic systems’ influence on social capital. Theoretical and future research implications are discussed.

Introduction

Social capital plays an important role in investor–small- and medium-sized enterprise (SME) relationships (Le & Nguyen, 2009; Sapienza & Korsgaard, 1996; Shane & Cable, 2002; Uzzi & Lancaster, 2003; Yli-Renko, Autio, & Sapienza, 2001). Social capital helps increase investors’ information and understanding of SMEs (Yli-Renko et al.) resulting in greater access to both equity and debt funding alike (Le & Nguyen; Shane & Cable; Uzzi & Lancaster). While this important research examines social capital as an antecedent to resource acquisition (i.e., knowledge, financial capital), little attention has been paid to the antecedents of social capital within SME–investor relationships. Indeed, Payne, Moore, Griffis, and Autry (2011) point out that over 90% of social capital research treats social capital as an independent variable.

In practice, many banks struggle with configuring their bureaucratic systems in attempts to enhance their client relationships with SMEs (Berger & Udell, 1998). Researchers acknowledge the importance of bureaucratic systems’ influence on social relationships (e.g., Adler & Kwon, 2002; Nahapiet & Ghoshal, 1998; Payne et al., 2011), and indeed suggest this influence is “inevitable under conditions of repeated action”

Please send correspondence to: Patrick A. Saparito, tel.: 610-660-1157; e-mail: [email protected], and to Joseph E. Coombs at [email protected].

P

T

E

&

1042-2587

(Adler & Kwon, p. 19). Adler and Borys (1996) argue that whether the influence is negative or positive is based upon whether or not bureaucratic systems depersonalize interaction and attenuate employees’ abilities to develop unique understandings about the task at hand. However, despite repeated calls for research that studies bureaucratic systems’ influence on social relationships (e.g., Adler & Borys; Adler & Kwon; Nahapiet & Ghoshal), little work has focused upon this relationship.

We respond directly to these calls and attempt to make a focused contribution to the literature. In particular, our purpose is to examine how bank-level bureaucratic systems influence social capital within bank–SME relationships. By doing so, our study takes the rare steps of a multilevel approach and an examination of social capital as a dependent variable (Payne et al., 2011). We test our hypotheses on a matched sample of 884 SME executives and 217 managers across 22 banks. Data from bank managers measure the bank-level bureaucratic systems (i.e., formalization, management continuity, and cus-tomer orientation), while data collected from SME executives measure social capital’s relational (i.e., trust) and cognitive (i.e., shared values) dimensions. We conclude by discussing our results and implications for future research.

Social Capital Dimensions

Adler and Kwon (2002, p. 23) define social capital as “the goodwill available to individuals or groups.” The general intuition behind the concept of social capital is that trust, expectations of reciprocity, and shared values and norms facilitate resource flows and promote group action (Adler & Kwon; Nahapiet & Ghoshal, 1998). Social capital can provide differential access to various resources and thereby be used for an individual’s benefit and competitive advantage (Burt, 1992; Portes, 1998). For SMEs, social capital can provide access to critical resources necessary for firm survival and growth (Morse, Fowler, & Lawrence, 2007; Packalen, 2007).

The social capital literature has two primary research streams. The first locates social capital’s source in the structure of a network’s social ties (Le & Nguyen, 2009; Zhang, Souitaris, Soh, & Wong, 2008). For example, Coleman (1990) suggests that dense ties within a collectivity foster self-enforcing norms facilitating the attainment of group goals. The second research stream focuses on the content of specific ties (Adler & Kwon, 2002). For instance, Uzzi (1999) found that trust-filled ties with banks facilitated an SME’s access to credit, while Yli-Renko et al. (2001) reported that firm-trusting ties with venture capitalists were associated with greater knowledge transfer. Consistent with research examining investor–SME relationships (e.g., Uzzi; Uzzi & Lancaster, 2003; Yli-Renko et al.), we focus on the content of specific ties.

Social capital is increasingly viewed as a multidimensional construct (Nahapiet & Ghoshal, 1998; Tsai & Ghoshal, 1998). Nahapiet and Ghoshal identify three dimensions of social capital: structural, relational, and cognitive. The structural dimension refers to the pattern of network relationships. Network structure includes the existence or absence of connections between a focal party and other actors (bridging approach) and the overall pattern of relationships within a group (bonding approach). Thus, the structural dimension reflects “the impersonal configuration of linkages between people and units” (Nahapiet & Ghoshal, p. 244).

1985; Nahapiet & Ghoshal). Trust appears as the key attribute of the relational dimension (Nahapiet & Ghoshal). In discussing the relational dimension, Nahapiet and Ghoshal’s conceptualization of trust is based upon the notions of reciprocity and expected goodwill that build strong interpersonal bonds. Trust enables sequential business interaction where one party must act first with the expectation that the other party will fully respond and uphold their commitments at a later time. Thus, trust acts as a social mechanism allowing parties to take actions with confidence that future obligations will be fulfilled and vulner-abilities will not be exploited (Ouchi, 1980; Uzzi, 1999).

Finally, the cognitive dimension of social capital refers to shared values, interpreta-tions, and systems of meaning among parties that provide a basis for making sense of knowledge and classifying it into perceptual categories (Nahapiet & Ghoshal, 1998; Tsai & Ghoshal, 1998). Shared values, interpretations, and systems of meaning facilitate learning and knowledge transfer allowing individuals to share each other’s thinking processes. These common understandings help individuals make sense of and interpret the world around them (Nonaka, 1994). Consistent with research examining investor–SME relationships, our focus is on the content of specific ties between parties. Consequently, we focus on social capital’s relational and cognitive dimensions. In doing so, we answer Payne et al.’s (2011) call for research that considers antecedents of social capital. Addi-tionally, we also investigate Adler and Kwon’s (2002) call for additional research explor-ing bureaucratic systems’ influence on social relationships.

Bureaucratic Systems’ Influence on Social Capital

Bureaucratic systems include various attributes of organizational structure and orien-tations that guide organizational action and can have a profound effect on the nature of social relationships (Adler & Borys, 1996; Ouchi, 1980). Key features of bureaucratic systems that influence social relationships include organizational formalization, conti-nuity of employees in particular roles fostering greater specialization, and cooperative orientations that encourage purposeful action and communication (e.g., Adler & Borys; Barnard, 1938; Ouchi).

Formalization’s Effects on Trust and Shared Values

Formalization refers to an organization’s reliance on official rules to control behaviors and decisions (Burns & Stalker, 1961). Formal procedures replacead hocways of doing business, allowing organizational members to form stable expectations regarding firm activities, as well as create a basis for controlling organizational processes and monitor-ing employee actions (Adler & Borys, 1996; Burns & Stalker; Ouchi, 1980). For instance, banks may have formal procedures for approving loans, altering product delivery platforms, and offering packages or fee structures for SME customers in an attempt to standardize various outputs.

is genuinely interested in a client’s success beyond the bank’s own self-interest (Doz, 1996; Rousseau, Sitkin, Burt, & Camerer, 1998).

Because SMEs are generally more dependent upon particular banks than large firms with more financing options (Berger & Udell, 1998), bank responsiveness and interest in the SME’s success is particularly salient. An SME’s attributions of a bank’s goodwill can increase the social-psychological bonds between interfacing parties creating an important foundation for trust (Doz, 1996). Additionally, close and flexible interactions between parties create a basis for socialization (Mayo, 1945; Ouchi, 1980) which allows parties to understand preferred ways of doing things, accept those ways as their own, and foster shared values (Ring & Van de Ven, 1994). Therefore, bank bureaucratic structures that allow for flexibility can create an atmosphere of trust and promote shared values with their SME customers (Adler & Kwon, 2002). Alternatively, formalization by its nature depersonalizes interaction (Burns & Stalker, 1961), which can reduce socialization that supports shared values development and can alienate those interacting with highly formalized organizations (Adler & Borys, 1996; Ouchi). Accordingly, we propose:

Hypothesis 1a: The degree of a bank’s formalization is negatively associated with an SME’s trust in the bank.

Hypothesis 1b: The degree of a bank’s formalization is negatively associated with an SME’s shared values with the bank.

Management Continuity’s Effects on Trust and Shared Values

Management continuity refers to the continuance of particular individuals within specific organizational roles (Doz, 1996), which leads to greater employee specializa-tion (March & Simon, 1958; Simon, 1945). That is, the longer an employee remains in a particular organizational role, the deeper his or her knowledge and understanding becomes regarding the nuances and context of organizational role responsibilities (Barnard, 1938). Additionally, employee specialization is a key factor in bureaucratic systems that affect the social nature of the organization (Adler & Borys, 1996; Ouchi, 1980). Within the realm of bank–SME relationships, management continuity refers to the degree that there is a continuance of management on the part of the bank. More specifi-cally, management continuity herein refers to the degree that the bank employee(s) who interacts with a particular SME is consistent over time.

Doz (1996) argues that management continuity develops commitment to the relation-ship itself. Ring and Van de Ven (1994) also suggest that if interacting parties remain constant through repeated cycles of exchange, interactions become more deeply socially embedded and each party may come to believe that the other party understands their goals, shares their values, and will act in accordance with concern for the relationship itself. Affective bonds, shared goals, and concern for the relationship itself are each identified as important underpinnings of trust (Ring & Van de Ven; Rousseau et al., 1998). Addi-tionally, Mayo (1945) suggests that employment stability fosters socialization. Socializa-tion toward common values requires consistent interacSocializa-tion over time where parties come to recognize the values and goals of interacting parties and to accept these values and goals as their own (Mayo). Therefore, if a bank maintains consistency in personnel, this should foster the development of shared values between interfacing parties at the SME and the bank. Thus we suggest:

Hypothesis 2b: The degree of a bank’s management continuity is positively associ-ated with an SME’s shared values with the bank.

Customer Orientation’s Effects on Trust and Shared Values

Finally, bureaucratic systems can embody cooperative orientations (Barnard, 1938; Ouchi, 1980; Simon, 1945). Such organizational cooperative orientations can induce organizational members to continue their participation in the organization and promote behaviors that facilitate attainment of joint goals. (Barnard; Ouchi). While this work has focused on how internal orientations can induce organizational members to act toward collective goals, organizational orientations can also foster cooperative action and loyalty from important external partners (Das & Teng, 1998; Ring & Van de Ven, 1994). Indeed, Saparito, Chen, and Sapienza (2004) found that bank customer orientation increased customer firm loyalty. In particular, this systematic set of bank behaviors is designed to build long-term relationships with SMEs (Haines, Riding, & Thomas, 1991; Saparito et al.). Since we are focused on the interorganizational relationships between banks and SMEs, we adopt Saparito et al.’s term of “customer orientation.”

Bank customer orientation is aimed at developing long-term customer relationships through advice giving, attention, and responsiveness. Such activities develop expectations of reciprocity and fair dealing that create social-psychological bonds (Granovetter, 1985; Ring & Van de Ven, 1994) which are important to trust development (Rousseau et al., 1998). Additionally, bank customer orientation enhances trust by encouraging communi-cation and information sharing with SMEs through which the SME comes to better understand the bank’s capabilities and dependability. This allows an SME to reflect on the bank’s track record for role-related duties, which is an important element in assessing a party’s trustworthiness (Granovetter).

A bank’s customer orientation should also foster the development of shared values. Advice giving and helpfulness act as signals of goodwill and intimacy (Das & Teng, 1998) which can enhance an SME’s perception of value congruence and identification with its banking partner (Coleman, 1990; Granovetter, 1985). Further, a bank’s frequent dialogue and interaction with SMEs can facilitate social-emotional relationships fostering positive attributions about the bank’s moral integrity and goodwill, which are also important elements fostering shared values (Coleman; Rousseau et al., 1998). Based upon this, we propose the following two hypotheses:

Hypothesis 3a: The degree of a bank’s customer orientation is positively associated with an SME’s trust in the bank.

Hypothesis 3b: The degree of a bank’s customer orientation is positively associated with an SME’s shared values with the bank.

Methodology

Second, each bank compiled a complete list of SMEs with which the bank had both deposit and lending relationships. Consistent with the U.S. Small Business Administra-tion, SME customers were defined by a credit limit of up to $1 million. We randomly distributed 7,298 surveys to these SMEs. Overall, 884 complete surveys were returned for this research for a 12.1% usable response rate. The response rate is consistent with similar studies with surveys of similar length (Haines et al., 1991; Lange, Warhuus, & Levie, 1999).

Responding firms had a median age of 15 years, six full-time employees, annual sales in the $500 thousand to $1 million range, and had conducted business with the bank a median of 5 years. Since the surveys were anonymous, it was not possible to calculate differences between respondents and nonrespondents. However, late respon-dents are considered similar to nonresponrespon-dents (Churchill, 1991). A two-tailed t-test comparing early versus late respondents found no significant differences for any firm variables.

Third, responding SME executives identified the bank manager primarily responsible for the company’s account. Additionally, bank executives identified the bank manager in charge of small business lending operations. We sent surveys to 263 bank managers, assuring participation confidentiality, and they returned 217 surveys for an 82.5% response rate. The result of this three-step sample design is 884 matched bank–SME dyads. The 884 SMEs are nested within the 22 banks (range—23 to 65 SME respondents/ bank; median—44 SME respondents/bank).

Measures

Trust (Dependent Variable). We used Sapienza and Korsgaard’s (1996) 3-item trust measure, adapted to reflect a banking context, and a 7-point scale (1=very rarely true to

7=very often true). We asked SMEs to rate: (1) The bank is honest in their dealings with

us; (2) We can trust the bank; (3) If the bank made a decision that was different from what we would make, we would believe that the bank had good reasons for making this decision (alpha=.88).

Shared Values (Dependent Variable). We adapted Tsai and Ghoshal’s (1998) 2-item measure for shared values to reflect both an interorganizational and a banking context, and used a 7-point scale (1=very rarely true to 7=very often true). SMEs rated two

statements: (1) We share common business values with the bank; (2) We feel that the bank would act in a fashion consistent with what we would recommend without prior discussion with us (alpha=.85).

Formalization (Independent Variable). We adapted Nohria and Ghoshal’s (1994) 3-item measure to reflect the extent that banks employ formal rules and procedures in their dealings with SMEs and a 7-point scale (1=very infrequently to 7=very frequently). We

Management Continuity (Independent Variable). We used Saparito et al.’s (2004) 3-item measure and a 7-point scale (1=very infrequently to 7=very frequently). We

asked bank managers to rate three statements as they related to the bank’s interaction with SMEs: (1) One employee or a small team of employees handles a given small business client’s accounts across various product and service lines; (2) Employees with direct client interaction are rotated between branches and/or departments on a regular basis (reverse coded); (3) There is low employee turnover among employees with direct small business customer interaction (alpha=.72).

Customer Orientation (Independent Variable). We used Saparito et al.’s (2004) 4-item measure and a 7-point scale (1=very infrequently to 7=very frequently). We asked bank

managers to rate three statements as they related to the bank’s interaction with SMEs: (1) The bank encourages bank managers to play a helpful and advisory role with their small business clients; (2) The bank encourages bank managers to act with significant flexibility in meeting small business client borrowing and other financial needs; (3) The bank focuses on improving bank–small business relationships by selling products that fit a specific client’s needs; (4) The bank attempts to understand the business and marketplace of its small business clients (alpha=.74).

Control Variables. Control variables included those known to affect bank–SME relation-ships. Bank market competitiveness influences the level of bank service and number of banking alternatives (Berger & Udell, 1998; Petersen & Rajan, 1994). Therefore, we included the U.S. Federal Reserve Bank’s Herfindahl–Hirschman index (HHI) bank concentration index as a measure of bank market competitiveness (Petersen & Rajan). Additionally, since the HHI is specific to different geographic markets, the index also acts as an identifier of various local markets (Petersen & Rajan).

Since large banks are generally less involved with smaller loans, bank size (the natural log of total assets reported in each bank’s 1999 annual report) was included (Berger & Udell, 1998). Bank profitability influences the organization’s ability to extend loans (Berger & Udell). Therefore, we measured bank profitability by bank return on assets.

Both firm size and firm age have important implications for a firm’s ability to accumulate many important intangible resources such as legitimacy and social connec-tions that are important to social capital development (Adler & Kwon, 2002; Aldrich & Auster, 1986). Consequently, we controlled for both factors. We measured firm size by two factors—number of employees and sales revenues. Firm age was the number of years that the SME had been in operation.

The banking relationship’s age and product breadth have significant influences on the nature of the bank–firm relationship including social-psychological factors such as commitment and trust (Saparito et al., 2004; Uzzi, 1999; Uzzi & Lancaster, 2003). Consequently, we controlled forrelationship ageandnumber of accounts. We measured relationship age by the number of years the SME conducted business with the bank. As a measure of the breadth of the bank–SME relationship, we measured the number of accounts the firm had with the bank. Whether or not a particular bank is a firm’s primary banking institution influences a firm’s dependence on the bank (Uzzi). We measured the

Aggregation of Organizational-Level Variables

We used multiple bank managers as informed observers (Chen, Fahr, & MacMillan, 1993) to construct the bank-level independent variables. While aggregating employee perceptions is a valid means to measure organizational-level variables, interrater reliabili-ties should be established (Chen et al.; Rousseau, 1985). We estimatedrwg(j)statistics for

manager perceptions for bank-level constructs using procedures outlined in James, Demaree, and Wolf (1993). This analysis yielded values indicating acceptable agreement (i.e., above 0.70) for each aggregated bank-level variable (i.e., formalization, management continuity, and customer orientation).

Model Estimation

We used hierarchical linear modeling (HLM) for hypothesis testing. HLM is appro-priate because the data include multiple SME customers per bank. HLM is better than Figure 1

ordinary least squares (OLS) regression in nested group settings, where the observations for each SME cannot be considered independent due to potential autocorrelation (Byrk & Raudenbush, 1992). HLM corrects for potential autocorrelation and heteroscedasticity and also reduces aggregation bias (Bloom & Milkovich, 1998). Although OLS generates biased parameter estimates and standard errors when using multilevel data, it does provide adequate effect size estimates and is therefore used to estimate model R2to convey these

effect sizes (Wallace & Chen, 2006).

Results

Table 1 presents the means, standard deviations, and Pearson correlations for the variables. Responding firms had a mean age of 21.1 years of operation and approximately 20 full-time employees, which is well under the 500 employee criteria for U.S. Small Business Administration classification as a small firm. All variance inflation factors were below 10 indicating there were no multicollinearity issues (Neter, Wasserman, & Kunter, 1990).

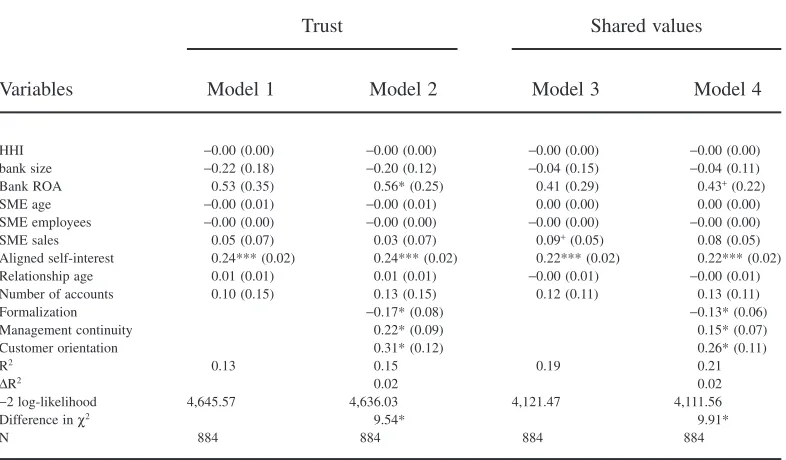

Table 2 presents our regression results. Hypothesis 1a suggests a negative relationship between formalization and trust. Results show formalization is significantly and nega-tively associated with trust supporting hypothesis 1a. Hypothesis 1b proposes a negative relationship between formalization and shared values. As is shown in Table 2 (Model 4), the coefficient for this variable is negative and significant providing support for hypothesis 1b.

According to hypothesis 2a, management continuity is positively associated with trust. Results in Table 2 (Model 2) support hypothesis 2a showing that management continuity is positively and significantly associated with trust. Hypothesis 2b suggests management continuity and shared values are positively associated. As is shown in Table 2 (Model 4), the coefficient for this variable is positive and significant providing support for hypothesis 2b.

Hypothesis 3a predicted a positive relationship between a bank’s customer orientation and trust. As results in Table 2 (Model 2) demonstrate, hypothesis 3a is supported. Lastly, hypothesis 3b predicts a positive relationship between a bank’s customer orientation and shared values. Results in Table 2 (Model 4) support hypothesis 3b. To summarize, all hypotheses are supported.

Discussion

In response to calls for multilevel research and examinations of social capital as a dependent variable (e.g., Adler & Kwon, 2002; Payne et al., 2011), our study makes a focused contribution by extending our understanding of how bureaucratic systems influ-ence social capital’s relational (i.e., trust) and cognitive (i.e., shared values) dimensions. Our findings demonstrate that bank formalization is negatively associated with both dimensions of social capital, while management continuity and customer orientation are positively associated with both dimensions of social capital.

Table 1

Correlations, Means, and Standard Deviations†

1 2 3 4 5 6 7 8 9 10 11 12 13 14

1. HHI§

2. Bank size‡

-0.08*

3. Bank ROA 0.44** 0.08*

4. SME age 0.03 0.01 0.13**

5. SME employees -0.01 0.14** 0.10** 0.24**

6. SME sales -0.05 0.20** 0.14** 0.21** 0.50**

7. Aligned self-interest 0.02 0.04 0.10** -0.01 0.05 0.09** 8. Relationship age -0.06 -0.09** 0.05 0.35** 0.03 -0.03 -0.05

9. Number of accounts 0.05 -0.08* 0.01 -0.06 -0.13** -0.19** -0.03 0.21**

10. Formalization 0.27** 0.27** -0.01 0.05 0.08* 0.17** -0.01 -0.06 -0.14** 11. Management continuity 0.06 0.02 -0.05 0.05 0.02 -0.01 0.10** 0.07* 0.01 0.04

12. Customer orientation -0.22** 0.14** 0.02 -0.04 0.10** 0.14** 0.08* -0.12** -0.09** 0.24** 0.25**

13. Trust 0.01 -0.05 0.09** 0.01 0.00 0.03 0.34** 0.01 0.02 -0.06 0.13** 0.12**

14. Shared values -0.00 0.01 0.10** 0.02 0.03 0.08* 0.41** -0.02 0.02 -0.04 0.13** 0.15** 0.71** Mean 1,572.77 6.05 1.13 21.12 19.95 3.34 20.04 9.64 1.61 11.92 16.19 21.87 17.63 10.64 Standard deviation 655.45 0.97 0.52 21.65 41.44 1.84 4.82 11.06 0.75 1.51 1.24 1.87 3.44 2.65

*p<.05; **p<.01

†n

=884.

‡Logarithm of total assets.

§Coded as dummy variable with banking institution is primary financial institution

=1, not primary financial institution=0.

HHI, Herfindahl–Hirschman index; ROA, return on assets; SME, small- and medium-sized enterprises.

634

ENTREPRENEURSHIP

THEOR

Y

and

PRA

situations will negatively influence attitudes and social relationships, while bureaucratic systems that leverage employees’ abilities and understandings will enhance attitudes and social relationships. Our findings support these theoretical assertions. In compliance with government oversight and to maintain objectivity, U.S. banks employ significant formalized rules and closely monitor employees and customer transactions for compli-ance. Researchers assert that such reliance on rules and close monitoring will negatively impact social relationships (Adler & Borys; Adler & Kwon). Our findings suggest that bank formalization is negatively associated with social capital. While U.S. banks are embedded in an institutional context that requires significant formalization, they do have considerable freedom and control over their organization’s management continuity and cooperative orientations. As we argued earlier, both of these factors should enable bank employees to leverage their unique understandings of SME clients and respond in ways to enhance the bank–SME relationship. Indeed, our findings show that both of these factors enhance the development of social capital within bank–SME relationships.

We find these results particularly interesting given that neither of our controls of the bank–firm relationship age or the relationship breadth (i.e., number of products) had any statistically significant relationship with either social capital dimension. While both the SME financing and the social capital literatures (e.g., Petersen & Rajan, 1994; Riding, Haines, & Thomas, 1994; Uzzi, 1999; Uzzi & Lancaster, 2003) frequently use these Table 2

Hierarchical Regression Analysis Results for the Predictors of Trust and Shared Values†‡

Variables

Trust Shared values

Model 1 Model 2 Model 3 Model 4

HHI -0.00 (0.00) -0.00 (0.00) -0.00 (0.00) -0.00 (0.00)

Aligned self-interest 0.24*** (0.02) 0.24*** (0.02) 0.22*** (0.02) 0.22*** (0.02) Relationship age 0.01 (0.01) 0.01 (0.01) -0.00 (0.01) -0.00 (0.01) Number of accounts 0.10 (0.15) 0.13 (0.15) 0.12 (0.11) 0.13 (0.11)

Formalization -0.17* (0.08) -0.13* (0.06)

Management continuity 0.22* (0.09) 0.15* (0.07)

Customer orientation 0.31* (0.12) 0.26* (0.11)

R2 0.13 0.15 0.19 0.21

DR2 0.02 0.02

-2 log-likelihood 4,645.57 4,636.03 4,121.47 4,111.56

Difference inc2 9.54* 9.91*

N 884 884 884 884

+p

<.10; *p<.05; **p<.01; ***p<.001

†Betas are unstandardized regression coefficients; standard errors are in parentheses.

‡Two-tailed tests.

structural measures of relationships, we find in this study that it is the set of behaviors (i.e., formalized interaction, continuous contact with particular individuals, cooperative and helpful interaction) that influences social capital development. This finding has potentially important implications for structural measures of social capital if it is replicated in future studies.

Limitations

This study uses cross-sectional survey data. Longitudinal data would add greater confidence to our results and allow for stronger causal inferences regarding the nature of the relationships between bureaucratic systems (i.e., formalization, employee continuity, and customer orientation) and social capital (e.g., trust and shared values). A second limitation is the lack ofmutualdata on trust and shared values. The challenge in doing so is that it requires much greater access to and disclosure by both banks and their SME clients. Finally, while our response rate is consistent with similar studies (e.g., Haines et al., 1991; Lange et al., 1999), increasing the response rate would be beneficial.

Future Research and Conclusions

Although our results provide some evidence regarding antecedents of social capital in SME–bank relationships, further research would provide a deeper understanding of these relationships. For example, future research may investigate how SME–bank social capital influences SME outcomes, such as how easy it is for SMEs to gain access to credit, and what lending terms SMEs receive from their banks. For instance, shared values and trust may ease access to credit and allow SMEs to negotiate better terms when borrowing from their banks. Further, as our limitations suggest, researchers may collect longitudinal data with which to examine the strength of our results during differing economic environments. Additionally, as we noted, our data do not include mutual data on shared values and trust. Thus, future research might help in understanding how banks’ shared values with their SME customers, or the level of trust they have in their SME customers, might affect SME– bank relationships or the outcomes of those relationships.

Second, while our research focused on the positive aspects of social capital within the context of the bank–SME relationship, social capital has potential downsides (Edelman, Bresnen, Newell, Scarbrough, & Swan, 2004). For instance, there is the potential for overcommitment or loss of objectivity about partners in deeply embedded relationships (Edelman et al.). This has particular import for the investor–SME context. Objective and rational investment evaluation is an essential element to efficient debt markets (Berger & Udell, 1998). Whether social capital in bank–SME relationships influences loan evaluation objectivity would therefore be an interesting line of future research.

To conclude, social capital is a complex concept to understand and predict. Yet, because of its use in a variety of researcher disciplines, we urge researchers to pursue other antecedents relevant to their particular domains. Our research identifies three bureaucratic controls important to social capital development in SME–bank relationships, but this is only a first step for future research.

REFERENCES

Adler, P. & Kwon, S. (2002). Social capital: Prospects for a new concept.Academy of Management Review,

27, 17–40.

Aldrich, H. & Auster, E.R. (1986). Even dwarfs started small: Liabilities of age and size and their strategic implications. In B.M. Staw & L.L. Cummings (Eds.), Research in organizational behavior (Vol. 8, pp. 165–198). Greenwich, CT: JAI Press.

Barnard, C. (1938).The functions of the executive. Cambridge, MA: Harvard University Press.

Berger, A. & Udell, G. (1998). The economics of small business finance: The roles of private equity and debt markets in the financial growth cycle.Journal of Banking and Finance,22, 613–673.

Bloom, M. & Milkovich, G.T. (1998). Relationships among risk, incentive pay, and organizational perfor-mance.Academy of Management Journal,41, 283–297.

Burns, T. & Stalker, G. (1961).The management of innovation. London: Tavistock Publications.

Burt, R. (1992).Structural holes: The social structure of competition. Cambridge, MA: Harvard University Press.

Byrk, A.S. & Raudenbush, S.W. (1992).Hierarchical linear models. Newbury Park, CA: Sage.

Chen, M., Fahr, J., & MacMillan, I. (1993). An exploration of the expertness of outside informants.Academy of Management Journal,36, 1614–1632.

Churchill, G.A. (1991).Marketing research: Methodological foundations. Chicago, IL: Dryden.

Coleman, J.S. (1990).Foundations of social theory. Cambridge, MA: Harvard University Press.

Das, T.K. & Teng, B.-S. (1998). Between trust and control: Developing confidence in partner cooperation in alliances.Academy of Management Review,23, 491–512.

Doz, Y.L. (1996). The evolution of cooperation in strategic alliances: Initial conditions or learning processes?

Strategic Management Journal,17, 55–83.

Edelman, L., Bresnen, M., Newell, S., Scarbrough, H., & Swan, J. (2004). The benefits and pitfalls of social capital: Empirical evidence from two organizations in the United Kingdom.British Journal of Management,

15, S59–S69.

Granovetter, M. (1985). Economic action and social structure: The problem of embeddedness. American Journal of Sociology,78, 1360–1380.

Haines, G., Riding, A., & Thomas, R. (1991). Small business bank shopping in Canada.Journal of Banking and Finance,15, 1041–1056.

James, L.R., Demaree, R.G., & Wolf, G. (1993). An assessment of within-group interrater agreement.Journal of Applied Psychology,78, 306–309.

Lange, J., Warhuus, J.P., & Levie, J. (1999).Entrepreneur/banker interaction in young growing firms: A large scale international study. Frontiers of Entrepreneurship Research. Wellesley, MA: Center for Entrepreneurial Research, Babson College.

Le, N. & Nguyen, T. (2009). The impact of networking on bank financing: The case of small and medium-sized enterprises in Vietnam.Entrepreneurship Theory and Practice,33(4), 867–887.

March, J. & Simon, H. (1958).Organizations. New York: Wiley.

Morse, E.A., Fowler, S.W., & Lawrence, T.B. (2007). The impact of virtual embeddedness on new venture survival: Overcoming the liabilities of newness.Entrepreneurship Theory and Practice,31(2), 139–159.

Nahapiet, J. & Ghoshal, S. (1998). Social capital, intellectual capital and the organizational advantage.

Academy of Management Review,23, 242–266.

Neter, J., Wasserman, W., & Kunter, M.H. (1990). Applied statistical models(3rd ed.). Burr Ridge, IL: Richard D. Irwin, Inc.

Nohria, N. & Ghoshal, S. (1994). Differentiated fit and shared values: Alternatives for managing headquarters-subsidiary relations.Strategic Management Journal,15, 491–502.

Nonaka, I. (1994). A dynamic theory of organizational knowledge creation.Organization Science,5, 14–37.

Ouchi, W.G. (1980). Markets, bureaucracies, and clans.Administrative Science Quarterly,25, 129–141.

Packalen, K.A. (2007). Complementing capital: The role of status, demographic features, and social capital in founding teams’ abilities to obtain resources.Entrepreneurship Theory and Practice,31(6), 873–891.

Payne, G.T., Moore, C.B., Griffis, S.E., & Autry, C.W. (2011). Multilevel challenges and opportunities in social capital research.Journal of Management,37, 491–520.

Petersen, M. & Rajan, R. (1994). The benefits of firm-creditor relationships: Evidence from small business data.Journal of Finance,49, 3–37.

Portes, A. (1998). Social capital: Its origins and applications in modern sociology. Annual Review of Sociology,24, 1–24.

Riding, A., Haines, G., & Thomas, R. (1994). The Canadian small business-bank interface: A recursive model.

Entrepreneurship Theory and Practice,18(4), 5–24.

Ring, P.S. & Van de Ven, A.H. (1994). Developmental processes of cooperative interorganizational relation-ships.Academy of Management Review,19, 90–118.

Rousseau, D.M. (1985). Issues of level in organizational research. In B.M. Straw & L.L. Cummings (Eds.),

Research in organizational behavior(Vol. 7, pp. 1–37). Greenwich, CT: JAI Press.

Rousseau, D.M., Sitkin, S.B., Burt, R.S., & Camerer, C. (1998). Not so different after all: A cross-discipline view of trust.Academy of Management Review,23, 405–421.

Saparito, P., Chen, C., & Sapienza, H. (2004). The role of relational trust in bank-small firm relationships.

Academy of Management Journal,47, 400–410.

Sapienza, H. & Korsgaard, M. (1996). The role of procedural justice in entrepreneur-venture capitalist capital relations.Academy of Management Journal,39, 544–574.

Shane, S. & Cable, D. (2002). Network ties, reputation, and the financing of new ventures. Management Science,48(3), 364–381.

Simon, H. (1945).Administrative behavior. New York: Free Press.

Tsai, W. & Ghoshal, S. (1998). Social capital and value creation: The role of intrafirm networks.Academy of Management Journal,41, 464–478.

Uzzi, B. (1999). Embeddedness in the making of financial capital: How social relations and networks benefit firms seeking financing.American Sociological Review,64, 481–505.

Wallace, C. & Chen, G. (2006). A multilevel integration of personality, climate, self-regulation, and perfor-mance.Personnel Psychology,59, 529–557.

Yli-Renko, H., Autio, E., & Sapienza, H. (2001). Social capital, knowledge acquisition, and knowledge exploitation in young technology-based firms.Strategic Management Journal,22, 587–613.

Zhang, J., Souitaris, V., Soh, P., & Wong, P. (2008). A contingent model of network utilization in early financing of technology ventures.Entrepreneurship Theory and Practice,32(4), 593–613.

Patrick A. Saparito is an Assistant Professor in the Department of Management at Saint Joseph’s University, Philadelphia, PA, USA.

Joseph E. Coombs is an Associate Professor at Virginia Commonwealth University, Richmond, VA, USA.