Disclaimer: The views expressed in this paper are entirely of the authors’ and do not reflect that of the Asian

Development Bank. The authors accept the responsibility for any errors, omissions, and accuracy of the information presented.

Costs and Benefits of the Price Adjustment Clause in FIDIC MDB

Prianka N. Seneviratne Asian Development Bank

6 ADB Avenue Mandaluyong City

Metro Manila Philippines

Tel: +63 2 632-4444 Fax: +63 2 636 2428 Email: [email protected]

(Abstract = 260)

ABSTRACT

Project owners, bidders, and construction supervision engineers continue to grapple with questions on the price adjustment clause in the Conditions of Contract developed by the International Federation of Consulting Engineers for Multilateral Development Banks. The first question faced by a project owner is whether the adjustment provision should be retained, and if not, why? If retained, the questions that ensue have to be dealt with by both the project owner and the bidders. These are about the adjustment terms and conditions—start date, base date, thresholds, and the adjustment formula parameters such as cost elements, indices, and weightings. Although answers to these questions are available from different sources and been legislated in some countries, clear, empirical evidence of the benefits of providing for adjustment—increased competition, lower bid prices, market stability, and less risk of contractors defaulting—is lacking. Also, the effect of changing default adjustment parameters is largely unknown. This paper first examines literature and experts’ views on the above questions in relation to Asian Development Bank financed road construction contracts in Central Asia and the Caucuses. Then, Monte Carlo simulation is used to evaluate alternative answers to the questions. Simulation results show that project owners and bidders can both benefit from the adjustment provision. Bidders can increase their competitiveness by not adding an inflation risk premium while the owner can expect more realistic bid prices and benefit from price drops during construction unlike in fixed price contracts. However, neither party will gain from changing the default parameters, which increases uncertainty and cause bidders to add risk premiums.

INTRODUCTION

Price adjustment clauses in construction contracts are intended to reduce the financial risk to project owners and contractors if the input costs rise or fall sharply during construction when the contract period is long. In theory, if a contractor knows at the bidding stage that payments for his work will be periodically indexed, he will have less of a need to add a premium to the bid price for possible cost increases during construction. This reduces his risk of losing the contract by adding the premium. Adjustment provision in a contract also lowers the risk of contractors underestimating cost increases, and later experiencing financial difficulties and defaulting on their obligations. A project owner, on the other hand, ideally can benefit from lower bid-prices, less likelihood of contractors going into bankruptcy mid stream of a project, and lower final Contract Price, especially when costs are declining. These rationales, which were postulated more than 30 years ago, have led to the price adjustment clause becoming a standard feature in most construction contracts worldwide. It is also a standard clause (Clause 13.8—Adjustments for Changes in Cost) in the General Conditions of Contract prepared by the International Federation of Consulting Engineers (FIDIC) for Multilateral Development Banks (1). The standard bidding documents of eight donors are based on this contract form since 2005, when its first version was released.

A typical adjustment clause specifies the method, the terms, and the conditions of adjustment. These include the timing (start date, end date, and frequency), trigger values (i.e., range of price change, over which a contractor can claim adjustments), definitions of the value of works that will be adjusted, and the computation method. This means that the clause designers must determine the terms and conditions that best suit the project in hand. They also have to choose from three common computation methods: invoices, formulae, and a hybrid of the first two methods (2). A good overview of the history of price adjustment is provided in Ndihokubwayo and Haupt (3).

The formula in FIDIC Conditions of Contract for Multilateral Development Banks (FIDIC MDB) is of the form:

Pn = a + b(Ln/ Lo) + c(En/Eo) + d(Mn/Mo) + ...

Where:

Pn = adjustment multiplier to be applied to the estimated contract value in the relevant currency of the work carried out in period ―n‖, this period being a month unless otherwise stated in the Contract Data;

a = fixed coefficient, stated in the relevant table of adjustment data, representing the non-adjustable portion in contractual payments;

b, c, d, etc. = coefficients representing the estimated proportion of each cost element related to the execution of the Works, as stated in the relevant table of adjustment data; such tabulated cost elements may be indicative of resources such as labor, equipment and materials;

Ln, En, Mn, etc. = current cost indices or reference prices for period ―n‖, expressed in the relevant currency of payment, each of which is applicable to the relevant tabulated cost element on the date 49 days prior to the last day of the period (to which the particular Payment Certificate relates); and

The project owner must specify either one formula for adjusting the total value of all the works completed in a period or different formulae for different work items. For each formula, a and all the cost elements-- L, M, E, etc--must also specified. The default Base Date for Lo, Eo, Mo, etc, is defined in FIDIC MDB as the date 28 days before the final bid closing date. Each bidder must propose the values of b, c, d, and unless the Owner has specified, the source(s) of the indices or reference prices for L, M, E, etc. The default adjustment frequency is once a month, but may be altered by the Owner. These data are provided in the ―table of adjustment data‖ and the particular conditions of contract in the bid document.

This paper has two objectives. One is to analyze the sources and rationales behind the common answers to questions about price adjustment in FIDIC MDB. These are questions frequently asked by agencies implementing Asian Development Bank (ADB) financed road projects in Central Asia and the Caucuses. The other is to propose an analytical tool that can help the agencies test and use these answers, and make the price adjustment process systematic. The paper is based on data from ADB-financed road works contracts, a review of literature on global experiences on price adjustment, and interviews with 10 staff from road agencies and ADB. Using Monte Carlo simulation, the present author presents that, intuitively, the price adjustment procedure in FIDIC MDB is beneficial to both the Owner and the Contractor. However, an owner can only gain small financial rewards by changing the default parameters such as Base Date, start date, and by increasing the non-adjustable portion.

GLOBAL PRACTICES AND VIEWS ON PRICE ADJUSTMENT

Price adjustment provision is standard in works contracts of 47 state Departments of Transportation (DOT) in the United States, and 85% of these states provide adjustments for fuel and 79% for both fuel and liquid asphalt (4). Adjustment provisions are included in about 75% of all contracts let by these states each year. The adjustment parameters are based mostly on the United States Department of Transportation’s Technical Advisory 158 (5).

Queensland Department of Main Roads in Australia and government legislation provide for formula-based adjustment (rise and fall provisions) in contracts of 365 days or more. The formula is applied to 85% of the value of a work item or material (minus the value of bitumen and the value of work completed after the Date for Practical Completion). The indices are taken from the Road and Bridge Construction Index published by the Australian Bureau of Statistics (7). The bitumen adjustment provision is applied separately to contractor-supplied bitumen at the rate of change in Class 170 bitumen price. Class 170 is used as the reference because it is assumed to represent all classes of bitumen. In the United Kingdom, the Building Cost Information Service (BCIS) publishes formulae and indices, and provides guidance on their use (8).

The government Hong Kong has a policy since 2008 that provides for contract value adjustment for labor and materials cost changes in all government capital works contracts of any duration (9). Previously it was applicable to only to contracts of 18 months or more. The monthly indices for labor and materials costs published by the Census and Statistics Department of Hong Kong are used with a formula similar to the BCIS formula. This change was brought in after a survey found that 61% of the bidders were small contractors, who are more likely to experience cashflow problems in inflationary times.

issued by the Engineering Council, which is the statutory body entrusted to regulate the engineering profession, must be followed for formulating and implementing price adjustment in all public works contracts (11). However, the cost elements and the other coefficients are still left to be determined by the project owner and the bidders.

Several other developing countries also have legislation on terms and conditions of adjustment to be followed, even when FIDIC MDB is used. However, the country guidelines are in the form of rules that make price adjustment mandatory--no instructions on how to determine the parameters. For example, the Ministry of Construction in Vietnam issued a circular in July 2010 specifying the FIDIC MDB formula (in Article 7--Method of adjusting contract prices for adjustable unit-price contracts- of the circular), but it does not specify thresholds or parameters (12). In Sri Lanka, formulae (same as FIDIC MDB) are specified by the Institute for Construction Training and Development for different work items (13), but the corresponding guidelines too are not helpful to a project owner or a bidder. The National Highway Authority of India permits formula based adjustments subject to certain conditions, but also does not prescribe parameters (14). This formula is similar to that specified by BCIS in the UK.

The effect of the adjustment provision in a contract is not widely reported. The most extensive of the few published findings is a survey of the state DOTs by Skolnick (4). That has not shown discernible difference in the overall bid prices, market stability (number of contractors entering and leaving the market), defaulting contractors, and the number of bids per contract as a result of adjustment provisions. However, the survey data differences in some items such as steel. Additionally, it showed that the Engineers spend 86 hours a month per contract on average administering the adjustment provision. On the other hand, the comparison of Kosmopoulouy and Zhou (6) of bid prices for Oklahoma State DOT contracts before and after the state allowed adjustment to asphalt binder items in 2006 has revealed a difference. They have found that post-2006 bid prices were on average 12.7% lower for items eligible for adjustment compared to ineligible items.

ADJUSTMENT PARAMETERS

According to ADB’s procurement guidelines, the price adjustment provision must be included in contracts longer than 18 months (15). Failure of a bidder to accept the price adjustment provision is a basis for rejecting his bid (16). If provided and accepted, the project owner and the bidders must determine the following parameters, terms, and conditions of adjustment:

(i) Base date and Start Date1 adjustment procedures, the decisions on these parameters can be challenging. Information in the donor’s guides is scant. They can indeed turn to textbooks (e.g., 17 and 18), periodic FIDIC seminars, and discussion groups on the internet. However, they generally lack experience and

1 Default start date is based on the start date of the program, which the Contractor must submit within 28 days of the

historical data needed to analyze each parameter in detail, and hence continually grapple with myriad questions. Among them, the following are some frequently asked questions:

(i) What are the optimum start and base dates?

(ii) Can upper and lower bounds be set to trigger the adjustments (i.e., adjustments are allowed only if a price or an index change stays with 3 and 10%)?

(iii) What are the appropriate cost elements and weightings?

(iv) What is the optimum non-adjustable portion (adjustment formula constant)? (v) What are the reliable and appropriate price or index sources?

(vi) When and how can a family of formulae (separate formula for separate for work items) be used?

(vii) Should bidders be allowed to propose the weightings?

(viii) Is 6 to 12% of the Contract Amount specified by ADB (19) an adequate contingency for price adjustments to be provided in the project budget?

Base Date: The default Base Date in FIDIC MDB, which is ―the date 28 days prior to the latest date for submission and completion of the tender‖ (1), has been retained in most ADB contracts. A 48-month contract let in Afghanistan in 2011 is an exception. In that, the 28 days is counted from the first day of the 25th month or 692 days after the Commencement Date (that is Commencement Date + 720 days – 28 days). The date 28 days before the start of the 18th month was used in a contract in Armenia.

Start Date: This date, which is the first date of the first adjustment period, is important, because a default date is not specified in FIDIC MDB, most global guidelines and ADB (1, 16, and 19). The Philippines is the exception--the date six months after the date of signing the contract is defined as the default start date (10). With few exceptions, the Commencement Date (as defined in FIDIC MDB) is the start date in most ADB –financed contracts examined for this paper. In the Afghanistan contract mentioned above, the first adjustment period starts on the date 24 months after the Commencement Date. The reference date for the first set of current indices is the date 722 days after the Commencement Date (i.e., Commencement Date + 720 days + 30 days – 28 days). The underlying rationale for the late start—to discourage unrealistically low bids from firms expecting to delay the works and benefit from rising prices.

In a 2011 contract let in Tajikistan, the adjustments for asphalt works2 was set to start on the date 12 months after the Commencement Date, with the first set of current indices based on the date 311 days after the Commencement Date (i.e., Commencement Date + 360 days – 49 days). The remaining work items are adjusted starting on the Commencement Date. The rationale for this two-stage approach for the 13th-month start date is that asphalt works are programmed to commence in the 13th month. Hence, adjustments for cost changes in the first 12 months should not apply to asphalt works. The formulae used here are similar to those of Queensland Department of Main Roads (7).

Linking the base date to either commencement date or start date instead of tender submission date is risky for a contractor because they are dependent on the preceding approval stages and conditions that must be fulfilled. This uncertainty can cause a bidder to add a risk premium to the tender price, and undermine the advantages of the adjustment provision.

2

Triggers: The Philippines has set legal and technical thresholds for adjustment, starting 6-month after the effective date of the contract (10). The technical thresholds are either two standard deviations from the 30-month mean of the applicable price index or greater than 10% increase in the index (if historical data are not available). Upward and downward adjustments are permitted at a rate of the adjustment percentage plus or minus 5% for each period corresponding to the approved schedule and critical path. United States Department of Transportation suggests between 25% and 100% as the range for the ceiling (upper bound) for change in the index in which adjustments will be provided (5). It also suggests providing a contract cancellation clause if escalation exceeds 125% or 200%. Oklahoma DOT has opted to allow adjustments if the price increases by more than 3% in any period (6). Threshold-based adjustments are not common in aid-financed contracts. The donors’ guidelines make no reference to this option although it can be easily provided under FIDIC MDB. It can avoid the need for defining start dates and corresponding base dates, and indirectly show the level of risk that the owner is willing to take.

Cost Elements: FIDIC MDB cites labor, materials, and equipment as possible elements. Labor, bitumen, cement, steel, and equipment are the common elements in contracts examined for this paper as shown in Table 1. Ideally, the elements should be those making up the total cost of a particular work item, component, or all works. Pakistan has prescribed several steps for a user to follow in determining the elements (11), and the Philippines prescribes the elements for each of the 52 work items (10).

Weightings The project owner can include the weightings in the table of adjustment data in the tender document or require the bidders to propose them. The Philippines has preset the weightings for each element in the 52 formulae (10) and New Zealand’s Transport Agency for five types of road works (20). In India, project owners tend to set some and leave the other weightings to be proposed by the bidder (14). The disadvantage of this is that it allows higher weighting to be assigned to the most volatile element and zero to the least volatile element without reference to the cost composition. The Indian approach lowers this risk while also providing the bidders the opportunity to define their cost composition. The ranges of weightings assigned to common cost elements found in this study are shown in Table 1.

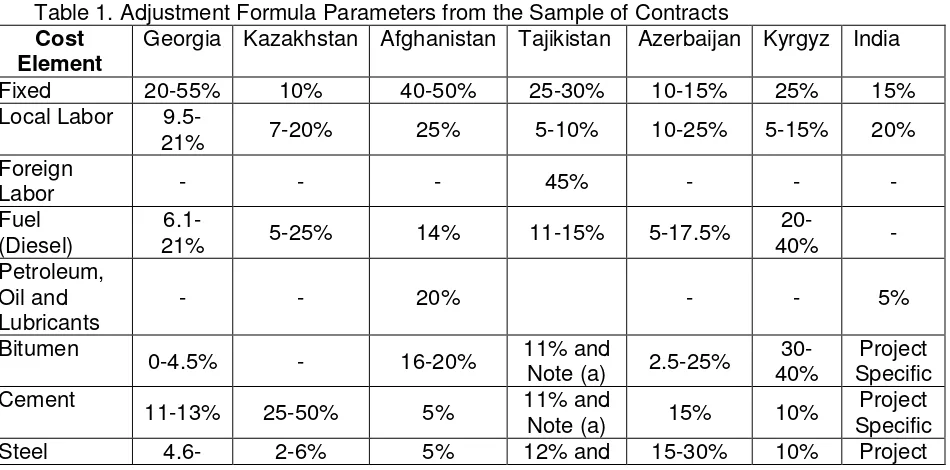

Table 1. Adjustment Formula Parameters from the Sample of Contracts Cost

Element

Georgia Kazakhstan Afghanistan Tajikistan Azerbaijan Kyrgyz India

20% Note (a) Specific

Note (a): Apply only to 2011 contracts

Non-Adjustable Portion (adjustment formula constant): This is defined by the UK Institution of Civil Engineers (21) as the portion of the inflation risk the owner wants the contractor to share. It can also be viewed as the share of overheads and profits, deemed to be unaffected by inflation. There are different views on the appropriate value of ―a” depending on whether it is considered the contractor’s risk or his profit (22). In the UK, BCIS Highways Term Maintenance Price Adjustment Formula for highway maintenance works has it fixed at 10% (8). South Africa, the Philippines, and India (2, 10, and 14) have set it at 15%, but Pakistan (11) has set upper and lower-bounds of 35% and 65% respectively. The values used in Central Asian and the Caucuses countries in ADB financed projects ranged from 10-55% as shown in Table 1.

Index and Price Sources: Under FIDIC MDB, a project owner can require bidders to use national sources or ask them to propose sources. In the latter case, if the element is an imported good, bidders can propose either an official source-country index, a global index, or a national index, if available. Because this index will be used to price the bid and future adjustments, it should be representative, easily accessible, and regularly published. A concern that contracting parties may have about each other’s proposed sources, which can later lead to disagreement, is their reliability, continuity, and timeliness. Countries such as New Zealand and the UK provide for using alternative national sources in case one source is discontinued (20 and 8). Timeliness is particularly important to keep the Engineer’s workload to a minimum. If late, adjustments have to be done twice--once with interim data and subsequently when the final data are available—at an added cost to the owner and payment delay to the contractor. At the state DOTs, engineers spend 85 hours a month on administration (4). This cost will increase with the frequency of adjustments.

ADJUSTMENT PARAMETER SELECTION

The various guidelines and advisory notes cited in this paper indicate that the parameters must fit the cost structure of the works and the economic conditions. However, parameter selection at road agencies in Central Asia is still an ad hoc process, driven partially by donors. There is a large spread in the adjustment parameter values (see Table 1) even in the same country in the same time period. For instance, in Georgia, the fixed portion range is from 20 to 55% in five relatively similar contracts financed by two different donors between May 2009 and December 2011. This is partly attributable to the lack of information and guidance. There is a dearth of examinations like those by Skolnik (4), Kosmopoulouy and Zhou (6), and Weidman (23) that highlight lessons learned from design and application of adjustment provisions in aid-financed contracts.

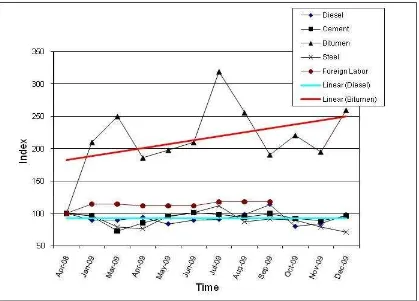

In Tajikistan, in 2011, equal weightings were assigned to all cost elements and 45% to foreign labor. However, bitumen was the most volatile cost element in the 2008-2009 period and the

3

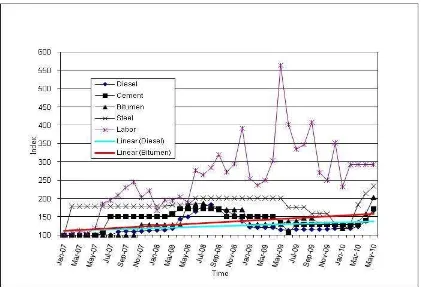

other cost elements either remained unchanged or declined as shown in Figure 1. In Kyrgyz, the most volatile element between 2007 and 2010 was local labor (See Figure 2). However, weightings between 30 and 40% were assigned to bitumen and between 20 and 30% to equipment. These inconsistencies suggest that both project owners and bidders have not given sufficient consideration to the cost composition, and current and past economic conditions. Whether this is because the project owners lacked experience and the donors’ guidance came from different sources is not apparent from the preliminary data. But the adjustment provisions in the sample of contracts analyzed here have few commonalities despite the similarities of the project scopes.

Figure 2. Kyrgyz Indices

RISK-BASED PARAMETER EVALUATION

An adjustment provision based on wrong assumptions can be worthless to both the owner and the contractor. Therefore, project owners must use their knowledge as well as analytical tools to formalize and improve the adjustment provisions. One such tool is Monte Carlo simulation, which is used by leading global companies to forecast returns and manage risk (24). A road agency can use it to test the sensitivity of the final Contract Price to different economic scenarios with and without adjustments and the sensitivity to different adjustment parameters. Its sensitivity to different level of uncertainty about future market conditions, especially when historical data are unavailable or unreliable, can also be tested. Simulation allows prices and indices to be represented, and the final Contract Prices to be computed as probability distributions. Indeed, it does not produce the ultimate or final result, but simulation allows more systematic assessments compared to the traditional binary sensitivity analyses, and can provide all parties a higher level of comfort about how adjustment provisions will address their respective inflation risk. Touran and Lopez (25) have previously shown the usefulness of Monte Carlo simulation compared to other methods for representing the uncertainty of price volatility.

Simulation Example

Monte Carlo simulation is a useful method of testing the sensitivity of the contract price to adjustment parameters. To demonstrate this, an Excel-based software program (26) was used with the set of input parameters given in Table 2. The simulation model for the base case (Scenario 1) was formulated as follows:

(ii) value was assumed to be comprised of three cost elements, and the coefficients a, b, c, and d in the adjustment formula were assumed to be given;

(iii) monthly relative index for each cost element (Ii/Io ) was assumed to have a triangular distribution. Touran and Lopez (25) have used a normal distribution. The triangular distribution is useful for subjectively describing a population with only limited sample data. One only requires some knowledge of the minimum and maximum and an inspired guess as to what the modal value might be (27);

(iv) distribution parameters--lowest, most likely, and highest values—were assumed to be given;

(v) base index of each cost element was assumed to be equal to 1; and

(vi) simulated adjustment factor for each month was multiplied by the value of work determined in step (i) above to arrive at a distribution of adjusted value of works for each month, and the distribution of the total adjusted price (the final Contract Price).

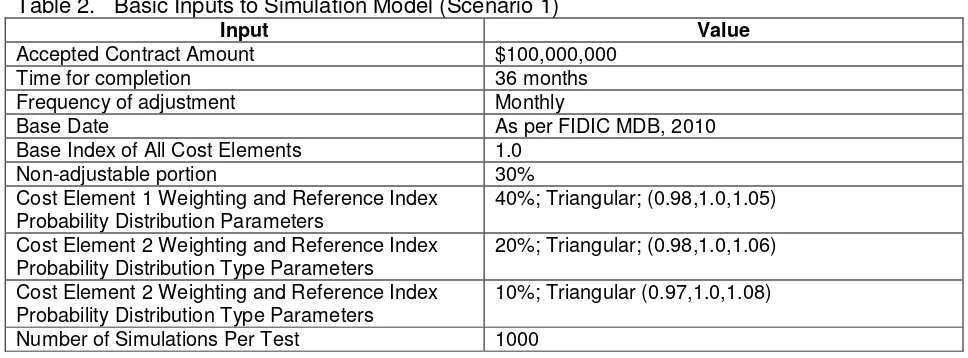

Table 2. Basic Inputs to Simulation Model (Scenario 1)

Input Value

Accepted Contract Amount $100,000,000

Time for completion 36 months

Frequency of adjustment Monthly

Base Date As per FIDIC MDB, 2010

Base Index of All Cost Elements 1.0

Non-adjustable portion 30%

The simulated results of the different scenarios tested in this example are summarized below:

(i) Start Date: If start date is different from the Commencement Date, a bidder can use simulation to determine what premium, if any, to include in the bid price to cover inflation until adjustments start under FIDIC MDB Sub clause 13.84. Likewise, the owner can estimate the final Contract Price under different start dates and the level of confidence, and decide whether or not to postpone, and determine the contingency to include in the budget.

The simulated values shown in Table 3 suggest that when the start date is the default date (Commencement Date), the mean final Contract Price is $100.8 million. If adjustments start 24 months after the Commencement Date, it will be $100.4 million or about 0.4% lower than the default case. In other words, the owner will save $400,000 by starting adjustments later. However, there is a possibility that even risk-averse bidders will include a premium in their bids for the expected loss in the first 24 months. Therefore, there seems little value in delaying the start date.

4

Table 3. Sensitivity of Final Contract Price (in $ million) to Start Date Under Scenario 1

Statistic Default Date Start Date After

12 Months 18 Months 24 Months

Minimum 100,437,700 100,272,900 100,152,000 100,076,800 Maximum 101,147,900 101,045,900 100,950,400 100,768,400 Mean 100,800,000 100,640,000 100,520,000 100,400,000

Std Deviation 130,122 122,184 119,243 100,944

% Change Mean -0.2% -0.3% -0.4%

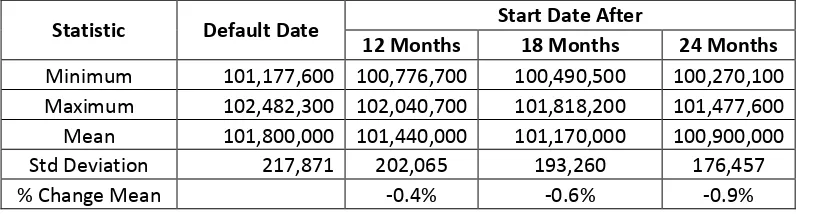

What if the volatility is much higher (Scenario 2)? To test this, the maximum value of the relative index probability distribution of each cost element was increased to 1.1. This means a possible maximum rise in any adjustment period (month) is 10%. The average savings accruing to the owner by delaying the adjustment start date by 24 months in this case were about $900,000 as seen from Table 4. It can also be seen that the savings from the 24-month start date is $500,000 higher under Scenario 2 (Table 4) than Scenario 1 (Table 3). However, given the higher volatility and uncertainty over the 24 months are likely to cause bidders to add a higher premium to the tender prices.

Table 4. Sensitivity of Final Contract Price (in $ million) to Start Date Under Scenario 2

Statistic Default Date Start Date After

12 Months 18 Months 24 Months

Minimum 101,177,600 100,776,700 100,490,500 100,270,100

Maximum 102,482,300 102,040,700 101,818,200 101,477,600

Mean 101,800,000 101,440,000 101,170,000 100,900,000

Std Deviation 217,871 202,065 193,260 176,457

% Change Mean -0.4% -0.6% -0.9%

What if the prices are constantly increasing with minor monthly rises and falls (Scenario 3)? To test this, all distribution parameters were assumed to increase by 5% of the previous month’s rate in the 12th, 18th, and 24th month and remain at the elevated rate in between. The figures in Table 5 show that the average saving to the owner from starting adjustment in the 25th month is about $1.5 million. Once again, a bidder may seek to recover the loss due to price rises in the first 24 months through a higher bid price.

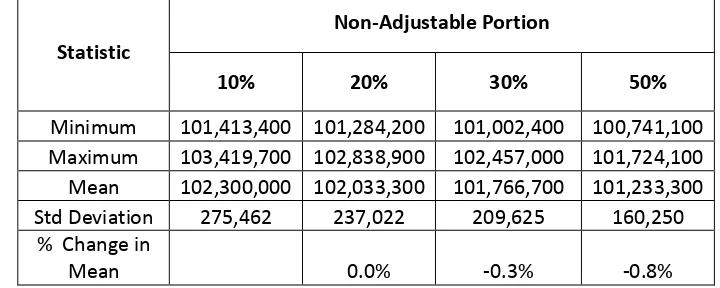

savings in the very high volatility case may be offset by the bidder’s risk premium, and that there will be no substantial gain from increasing the non-adjustable portion. This is particularly true if the increase is from 10% to 30%.

Table 5. Sensitivity of Final Contract Price (in $ million) to Start Date Under Scenario 3

Table 6. Sensitivity of Final Contract Price (in $ million) to Non Adjustable Portion Under Scenario 2

Statistic

Non-Adjustable Portion

10% 20% 30% 50%

Minimum 101,413,400 101,284,200 101,002,400 100,741,100 Maximum 103,419,700 102,838,900 102,457,000 101,724,100 Mean 102,300,000 102,033,300 101,766,700 101,233,300

Std Deviation 275,462 237,022 209,625 160,250

% Change in

Mean 0.0% -0.3% -0.8%

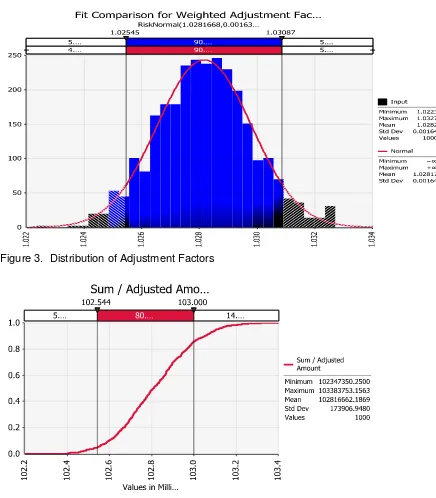

Figures 3 and 4 below show the distributions of the adjustment factor and the adjusted final Contract Price when the volatility is high (the distribution parameters of all three cost elements are set at 1.0, 1.03, and 1.10). The other parameters were assumed to remain unchanged. The resultant adjustment factor does not change much. It is normally distributed with a mean of 1.02 with a very small standard deviation, and there is less than 15% chance of the mean final Contract Price exceeding $103 million.

12Months 18 Months 24 Months

Minimum 105,922,133 104,841,448 104,170,140 103,595,347 Maximum 105,893,183 105,699,965 105,011,823 104,267,752 Mean 105,383,330 105,223,348 104,578,334 103,933,323

Std Deviation 134,914 125,678 120,038 106,725

% Change Mean -0.2% -0.8% -1.7%

Figure 3. Distribution of Adjustment Factors

Figure 4. Distribution of Mean Final Contract Price

quote unrealistically low prices and expect to recover the losses from adjustments under Sub clause 13.8 in FIDIC MDB by delaying work, even in a highly volatile environment.

The bid price discussion above is based on the assumption that the Engineer’s estimate is robust and a bidder will not be able to leverage much lower prices for the inputs. Also, only the volatility of Cost Element 1 was considered by setting b=1 with default start and base dates. Regardless, bid price estimation is a separate topic and has been reported elsewhere (28, 29, 30), but the impact of an adjustment provision on bid prices is not considered there.

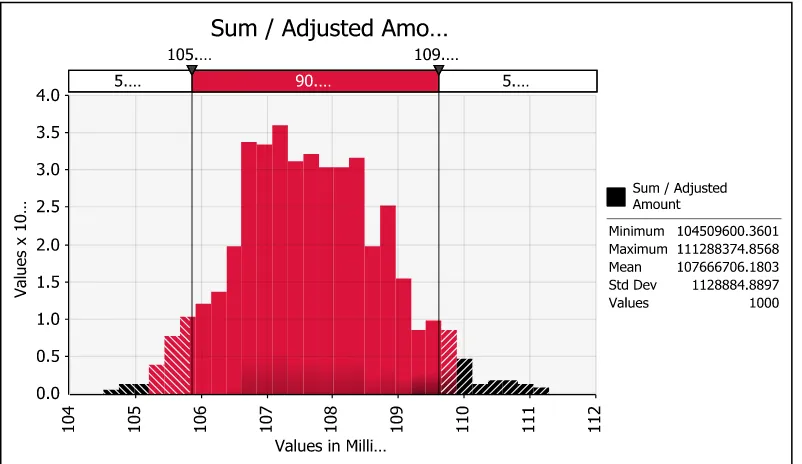

Figure 5. Distribution of Final Contract Price After Adjustments

SUMMARY AND CONCLUSIONS

The empirical data, interviews with ADB and road agency staff, the literature review, and simulation results, although limited, revealed the following:

(i) there are no published empirical and theoretical studies of the adjustment provision in FIDIC MDB. However, there are many internet sites (e.g., reference 31) that post opinions on myriad topics;

(ii) only about half the interviewees cited inflation risk sharing and increasing competition as rationales behind providing for price adjustment while the other half considered it a donor requirement;

(iii) some interviewees supported establishing specific national practices, like what the Philippines has done, to reduce uncertainty:

(iv) some supported changing parameters such as the start date and the non-adjustable portion, and using a family of formulae;

(v) the reasons for changing default adjustment parameters ranged from discouraging low bidders and slow work (i.e., prevent bidders benefitting from price rises) to limiting eligible work items and material (e.g., only asphalt paving and not all works);

(vii) Monte Carlo simulation can be used to estimates the final Contract Price, provided that all other conditions such as designs, scope, etc., remain unchanged;

(viii) simulation results can help decide whether to retain the adjustment provision in a contract or opt for a fixed price contract with no adjustments for inflation, and save on the adjustment provision administration cost; and

(ix) simulation can help test the adequacy of a projects’ budget under different inflation scenarios.

The following is a summary of the impact of adjustment provisions under different scenarios: (i) net adjustment to the Accepted Contract Amount (negotiated price) will be always

positive if the index probability distributions are positively skewed like in Tajikistan and Kyrgyz, for which the monthly data from 2008 to 2010 were tested in the present example;

(ii) this pattern is likely to cause bidders to add premiums in the absence of an adjustment provision. It is likely that the premium will be higher than the simulated mean of the adjustments, especially if price and index data are unavailable and unreliable;

(iii) final Contract Price is not very sensitive to the adjustment start date, and hence the likelihood of the default start date encouraging low bids (because the contractors expect to make money later) is small;

(iv) savings to an owner from delaying the adjustment start date will be reduced by the increased administration cost of implementing a complicated adjustment provision as in the case in Tajikistan referred to earlier;

(v) final contract price is also not very sensitive to the adjustment formula constant and weightings;

(vi) when future conditions are uncertain, pushing back the start date can be expected to create a perception of risk in the minds of bidders, particularly of international bidders, resulting in higher bid prices;

(vii) bidders’ perceptions and behavior are likely to be the same as above when the non-adjustable portion is increased although its financial implications are minimal in a high value contract.

(viii) whether a later start date and a large non-adjustable portion (high value of the coefficient a) will make some bidders add high premiums and make themselves uncompetitive, decide against bidding, or underbid and run into financial difficulty cannot be determined through simulation. However, in an actual tender, simulation can be used to compare the bid prices with simulated final contract prices to determine whether it is unrealistically low and the contractor can absorb the risk.

Based on the foregoing, it can be concluded that:

(i) in the absence of sufficient empirical evidence, project owners will continue to grapple with questions regarding the adjustment provision in FIDIC MDB. It will require a harmonized effort similar to that for producing FIDIC MDB to collate data and conduct the tests required to answer these questions with certainty;

(ii) simulation provides an additional perspective on the impact of various underlying assumptions, but it is not panacea. It can help answer some, but questions like adjustment provision’s impact on the number of bidders per tender and market stability require well-designed and controlled surveys;

REFERENCES

1. Federation Internationale Des Ingenieurs-Conseils (FIDIC MDB). 2010. Conditions of Contract for Construction. Multilateral Development Bank Harmonised Edition. General Conditions. June.

2. Cesar, Scott. 2009. Price adjustment clauses: a solution for dealing with changing materials costs. Construction Executive.

http://www.constructionexec.com/Issues/June_20092/Legally_Speaking.aspx. Accessed 17 June 2012.

3. Ndihokubwayo, Ruben and Haupt, Theo. 2009. Theories and Concepts for an Increased Cost Adjustment (ICA©) Formula for Optimum Cost Escalation Recovery. Journal of Construction 2.1 (2009): pp 7-13. (Available at:

http://works.bepress.com/ruben_ndihokubwayo/12).

4. Skolnik, Jonathan. 2011. Price Indexing in Transportation Construction Contracts. Prepared for The Transportation Research Board, AASHTO Standing Committee on Highways. Jack Faucett Associates. Bethesda, MD. January.

5. U.S. Department of Transportation. 1980. Development and Use of Price Adjustment Contract Provisions. Federal Highway Administration Technical Advisor Number 158. December 10.

6. Kosmopoulouy, Georgia and Zhou, Xueqi. 2011. Price Adjustment Policies in Procurement Contracting: An Analysis of Bidding Behavior. May. http://students.ou.edu/Z/Xueqi.Zhou-1/working_paper_2.pdf) Accessed 20 June 2012.

7. Queensland Department of Main Roads. 2005. Road Construction Contract Supplementary Conditions of Contract, USER GUIDE, No. C6838. September.

8. Highways Term Maintenance Association (HTMA). 2010. Price Adjustment Formulae Indices (Highways Maintenance) 2010 Series – Guidance Notes. Prepared in association with the Civil Engineering Contractors' Association and Building Cost Information Service. www.mhaweb.org.uk/htm_indices_final_guidance_notes.doc. Accessed 26 May 2012.

9. Hong Kong Bureau of Development. 2008. Note For Finance Committee--Application of Contract Price Fluctuation. FCRI (2008-09)5, July. (http://www.legco.gov.hk/yr07-08/english/fc/fc/papers/fi08-05e.pdf). Accessed 30 June 2012.

10. The Government of the Philippines. 2008. Revised Guidelines for Contract Price Escalation. (http://www.gppb.gov.ph/issuances/Guidelines/2008/Price%20Escalation.pdf). Accessed on 24 May 2012.

11. Pakistan Engineering Council (PEC). 2009. Standard Procedure and Formula for Price Adjustment. (First Edition). March.

(http://www.pec.org.pk/downloadables/PEC_Bidding_Docs/4mPICC/Std%20Procedure%20 and%20Formula%20for%20Price%20Adjustment.pdf.) Accessed 30 June 2012.

13. Institute for Construction Training and Development (ICTAD). 2008. Sri Lanka Country Report. The 14th Asia Construct Conference, 23 – 24 October Tokyo, Japan.

14. National Highway Authority of India (NHAI). 2006. NHAI Works Manual. http://www.scribd.com/doc/79241208/NHAI-Works-Manual-2006-new). Accessed 25 May 2012.

15. Asian Development Bank. 2010. Procurement Guidelines. Mandaluyong City, Philippines. April.

16. Asian Development Bank. 2010. Guide on Bid Evaluation. Mandaluyong City, Philippines. October.

17. Totterdill, B. W. 2006. FIDIC Users' Guide: A Practical Guide to the 1999 Red and Yellow Books-Incorporating changes and additions to the 2005 MDB Harmonised Edition. Thomas Telford Ltd.

18. Ramus, Jack, Birchall, Simon and Griffiths, Phil. 2006. Contract Practice for Surveyors. 4th Edition. Elsevier Ltd.

19. Asian Development Bank. 2010. User’s Guide: Procurement of Works. Standard Bidding Document. Mandaluyong City, Philippines. September.

20. Transfund New Zealand. 1997. Competitive Pricing Procedures Manual. Volume 1: Physical Works & Professional Services. Second Revision. February. Wellington, New Zealand. http://www.smartmovez.org.nz/references/refs/manuals/competitive_pricing_procedures_ma nual/competitive_pricing_procedures_manual_-_appendices/4. Accessed 20 June 2012.

21. Institution of Civil Engineers. 1995. Engineering and Construction Contract: Guidance note. Second Edition. Published by Thomas Telford, London. November.

22. Perry, J.A. and Thompson, P.A. 1978. Construction Finance and Cost Escalation. Proc. Instn. Civ. Engrs., Part 1, 1978, 64, May, 347-351.

23. Weidman, Justin. 2010. Best Practices for Dealing with Price Volatility In Utah Commercial Construction. A thesis submitted to the faculty of Brigham Young University in partial fulfillment of the requirements for the degree of Master of Science. School of Technology, Brigham Young University. August.

24. Temasek. 2012. Review Highlights. www. temasecreview.com.sg. (accessed 7 June 2012).

25. Touran, Ali and Lopez, Ramon. 2006. Modeling Cost Escalation in Large Infrastructure Projects. ASCE Journal of Construction Engineering and Management. Pp 853-860.

26. Palisade Corporation. 2012. @Risk. http://www.palisade.com/risk/

28. Sammoura, Rola and Elsayed, Aziz Ezzat 2008. A Stochastic-Simulation Model for Lowest Bid Price Evaluation: A Case Study in Road Construction and Rehabilitation Projects In Lebanon. Proceedings of the First International Conference on Construction In Developing Countries August 4-5. Karachi, Pakistan.

29. Drew, D.S., Lo, H.P., and Skitmore, R.M. (2001) The Effect Of Client and Type and Size Of Construction Work On a Contractor's Bidding Strategy. Building and Environment 36(3): Pp. 393-406.

30. Ioannou, P. G. and Sou-Sen, L. 1993. Average Bid-Method--Competitive Strategy. ASCE Journal of Construction Engineering and Management. Vol 119. No. 1. Pp131-147.