Refer to Important disclosures in the last page of this report

Stock DataTarget price (Rp) Rp6,000

Prior TP (Rp) Rp6,000

Share price (Rp) Rp7,050

Upside/downside (%) (14.9)

Shares outstanding (m) 9,585

Market cap. (US$ m) 4,112

Asia Financial (Indonesia) 67.4%

Estimate Change; Vs. Consensus

2018F 2019F

PT Indo Premier Securities [email protected] +62 21 5793 1168

Still stagnant but drag is diminishing

Weak top-line growth but micro business unwinding is nearly over.

NIMs are maintained (for now) despite rising rates this year.

Credit cost improved as loan mix shifts towards lower-risk assets.

Reiterate Hold given upside from MUFG acquisition/merger plans.

Still no earnings growth. BDMN reported net profit of Rp3.0tn in 9M18 (flat),

in-line with our FY18F forecast albeit slightly below consensus estimate. As such,

the bank continued with no earnings growth in the past five years on the back of

its unwinding of micro lending business to focus on SME, home mortgages,

commercial and automotive lending through subsidiary Adira Finance. However,

the growth drag from micro lending business appears to be over soon as its micro

loans, which declined 58% yoy, has fallen to just Rp3.2tn or contributing only

2.4% of loans, from 6.1% a year ago, and its peak contribution of 16% in 2013.

Stable NIMs. BDMN’s loan portfolio (including trade finance) grew 6% in 9M18 or

10% if excluding its declining micro loans. The bank’s key loan growth drivers are

Adira Finance’s automotive loans (+12% yoy), followed by SME loans (+11%) and

consumer (+16%), mainly driven by its strong mortgage loans (+35%), while

corporate loans grew 7%. Meanwhile, although the bank’s high NIMs narrowed by

30bps yoy to 9.0% in 9M18, NIMs were maintained stable at this level in the past

3 quarters despite BI’s 1205ps rate hikes and the bank’s loan mix shifting away

from high-margin loans, due to lack of funding growth and its CASA improvement

strategies. However, we expect lower NIMs in coming years as the bank starts to

grow loans more rapidly.

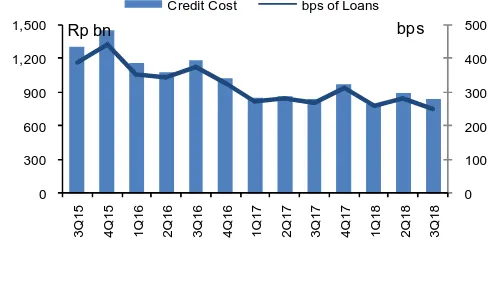

Asset quality. BDMN’s asset quality has been stable with credit cost improving

marginally to 2.6% in 9M18 (vs. 2.7% in 9M17) with lower credit cost of 2.5% in

3Q vs. 2.8% in 2Q. NPL ratio has also declined to 3.0% in 3Q, from 3.3% in 2Q

and a year earlier, while provision/NPL coverage also improved to 126%, from

116% a year ago. However, we expect scope for BDMN’s further credit cost

improvement to be more limited in the coming years and thus its earnings growth

will have to come from top-line growth.

Valuation. We maintain our earnings forecasts, TP of Rp6,000 and HOLD rating

despite the bank’s weak fundamentals in light of potential upside from ongoing

M&A. Although we believe BDMN’s valuation is unattractive, given the bank’s slow

earnings growth prospect with headwinds from rising rates, we believe its share

price will continue to be well supported by MUFG acquisition and merger plans (at

premium valuation), which has received regulatory approval and is proceeding to

the next stage in the process.

Bank Danamon

(

BDMN IJ

)

25 October 2018

Results Note

HOLD

(Unchanged)

Year To 31 Dec 2016A 2017A 2018F 2019F 2020F

Operating income (RpBn) 18,472 18,519 19,017 20,539 22,503

PPOP (RpBn) 9,375 9,098 9,314 10,247 11,491

Source: BDMN, IndoPremier Share Price Closing as of : 24-October-2018

BDMN IJ Results Note

2

Refer to Important disclosures in the last page of this report

Fig. 1: Net Interest Income (Rp bn) and NIMs (%) Fig. 2: Non-Interest Income (Rp bn; % of Gross Income)

Source: Company, IndoPremier Source: Company, IndoPremier

Fig. 3: Operating Expense (Rp bn) and Cost/Income Ratio (%)

Fig. 4: Pre-Provision Profit (Rp bn; % of Average Assets)

Source: Company, IndoPremier Source: Company, IndoPremier

Fig. 5: Net Loan Provisioning (Rp bn; bps of Average Loans) Fig. 6: Net Profit (Rp bn) and ROAA (%)

Source: Company, IndoPremier Source: Company, IndoPremier

5%

Net Interest Income Net Interest Margin

Rp bn

Other Income Other Income % of Total

Rp bn

Operating Expenses Cost-Income Ratio

Rp bn

Pre-Provision Profit Pre-Provision Profit ROAA

Rp bn

Credit Cost bps of Loans

bps

Net Profit Net Profit ROAA

3

Refer to Important disclosures in the last page of this report

Year To 31 Dec (RpBn) 2016A 2017A 2018F 2019F 2020F

Income Statement

Interest income 20,655 20,052 20,505 22,407 24,771

Interest expense (6,876) (5,903) (6,308) (7,216) (8,030)

Net interest income 13,779 14,149 14,197 15,191 16,741

Fees and commissions 3,644 3,428 3,770 4,147 4,562

Trading income 425 325 350 400 400

Other operating income 623 617 700 800 800

Total operating income 18,472 18,519 19,017 20,539 22,503

Personnel expenses (4,879) (5,023) (5,173) (5,535) (5,923)

G&A expenses (4,217) (4,398) (4,530) (4,757) (5,090)

Other operating expenses 0 0 0 0 0

Pre-provision operating profit 9,375 9,098 9,314 10,247 11,491

Provisions (4,441) (3,513) (3,298) (3,408) (3,633)

Short-term investments 17,408 16,060 17,666 19,432 21,375

Government bonds 9,563 10,974 10,974 10,974 10,974

Gross loans 122,385 124,766 138,733 154,863 173,311

Loan provisions (4,568) (4,271) (4,283) (4,515) (4,704)

Other assets 11,975 13,395 14,722 16,182 17,788

Total Assets 174,087 178,257 197,507 218,682 242,783

Customer deposits 103,740 101,897 110,240 119,382 129,408

Deposits from other banks 2,873 4,635 5,098 5,608 6,169

Securities and borrowings 19,813 19,965 22,710 25,842 29,416

Other liabilities 11,284 12,588 17,581 22,736 28,913

Total Liabilities 137,709 139,085 155,629 173,567 193,905

Share capital 13,151 13,158 13,158 13,158 13,158

Reserves and others 76 121 0 0 0

Retained earnings 22,716 25,382 28,209 31,445 35,209

Shareholders' equity 35,943 38,660 41,367 44,603 48,366

Minority interest 435 512 512 512 0

Total Liabilities & Equity 174,087 178,257 197,507 218,682 242,271

BDMN IJ Results Note

4

Refer to Important disclosures in the last page of this report

Year To 31 Dec 2016A 2017A 2018F 2019F 2020F

Growth Ratios (% yoy)

Gross loans (5.4) 1.9 11.2 11.6 11.9

Total assets (7.4) 2.4 10.8 10.7 11.0

Customer deposits (9.9) (1.8) 8.2 8.3 8.4

Net interest income 1.0 2.7 0.3 7.0 10.2

Non-interest income 1.8 (6.9) 10.3 10.9 7.8

Total operating income 25.1 13.2 7.7 13.7 14.9

Operating expense (1.5) 3.6 3.0 6.1 7.0

PPOP 3.9 (3.0) 2.4 10.0 12.1

Net profit 11.5 37.9 11.8 13.6 15.5

Profitability Ratios

ROAA (%) 1.50 2.11 2.19 2.25 2.34

ROAE (%) 7.6 9.9 10.3 10.9 11.6

NIM (%) 8.60 8.91 8.36 8.09 8.03

Credit cost (bps) 356.5 287.6 250.4 232.2 221.4

Cost/income (%) 49.2 50.9 51.0 50.1 48.9

LDR (%) 118.0 122.4 125.8 129.7 133.9

CAR (%) 23.7 25.0 24.3 23.6 23.0

NPL ratio (%) 2.7 2.3 2.1 2.1 2.1

Provisions/NPL (%) 138.3 150.3 147.5 140.4 130.9

Head Office

PT INDO PREMIER SEKURITAS

Wisma GKBI 7/F Suite 718

Jl. Jend. Sudirman No.28

Jakarta 10210 - Indonesia

p +62.21.5793.1168

f +62.21.5793.1167

INVESTMENT RATINGS

BUY : Expected total return of 10% or more within a 12-month period HOLD : Expected total return between -10% and 10% within a 12-month period SELL : Expected total return of -10% or worse within a 12-month period

ANALYSTS CERTIFICATION.

The views expressed in this research report accurately reflect the analyst;s personal views about any and all of the subject securities or issuers; and no part of the research analyst's compensation was, is, or will be, directly or indirectly, related to the specific recommendations or views expressed in the report.

DISCLAIMERS