Refer to Important disclosures in the last page of this report

Stock DataTarget price (Rp) Rp4,500

Prior TP (Rp) Rp4,500

Shareprice (Rp) Rp3,070

Upside/downside (%) +46.6

Sharesoutstanding (m) 9,936 Marketcap. (US$ m) 2,006

Sumitomo Metal Mining Co.

Ltd. 20.1%

Estimate Change; Vs. Consensus 2018F 2019F Latest EPS (USD

Cents) 0.8 1.2

PT Indo Premier Sekuritas [email protected] +62 21 5793 1170

Strong results despite challenges

Earnings grew 14.5% qoq despite unplanned maintenance in 3Q18.

Production has return to normal and would increase in 4Q18.

We maintain our price estimates and expect supply deficit in 2019.

Maintain Buy rating with 47% upside to our unchanged TP.

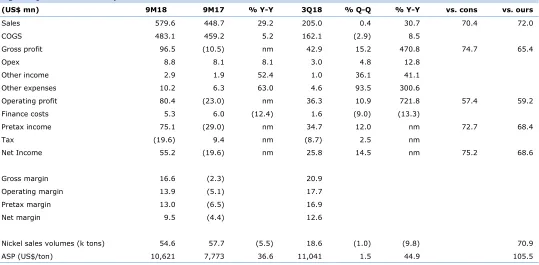

Strong 3Q18 earnings.

Despite unplanned maintenance in 3Q18, INCO recorded

strong earnings of US$25.8mn, up 14.5% qoq and jumped more than 12 fold yoy

(due to low base earnings in 3Q17). Sound earnings were mostly backed by

higher nickel matte average selling price (ASP) of US$11k per ton (+1.5% qoq,

+45% yoy). Net profit was recorded at US$55.2mn in 9M18 (vs. net loss of

-US$19.6mn in 9M17) which we see came in above consensus (75% of FY18F) but

inline with our earnings forecast (69%). We believe INCO would be able to book

net profit of US$25mn (flat qoq) in 4Q18F on the back of normalized production

post maintenance activities in 3Q18, allowing the company to meet our earnings

forecast of US$80mn for FY18F.

Production has return to normal.

Post the overpressure incident in INCO’s

electric furnace system in 3Q18, the management stated that production has now

returned to normal without any additional major maintenance activities in 4Q18.

INCO decided to move the planned maintenance activities earlier in 3Q18 (from

initial plan in 4Q18) as “bag house overpressure” incident in electric furnace #1

required two weeks shutdown for reparation. Bag House is equipment that

captures dust from the furnace to improve emission quality during the smelting

process which had been an effective and reliable tool for company’s operations

since its installation in 2005 and 2007.

Nickel industry outlook remains positive.

We maintain our nickel price

assumption of US$13,000-US$14,000 per ton for FY18F-19F, respectively. To

note, despite nickel price volatility, YTD18 nickel price average of US$13,560 per

ton remained higher than our assumption for FY18F. We maintain our positive

view on nickel industry’s long term outlook as we share the same view with the

consensus on potential supply deficit in 2019, which will be supportive for price.

Maintain Buy with 47% potential upside.

With these inline results we

maintain our Buy recommendation for INCO with unchanged DCF-based (WACC:

12.7%; TG: 3%) target price of Rp4,500. INCO revised down its production

volumes target to 75k tons for FY18F due to the “Back-House” incident in 3Q18.

Nonetheless, without any major maintenance activities in 4Q18, production

volumes could reach 20k tons (vs. 18.2k tons in 3Q18). Thus, we believe our

earnings forecast of US$80mn for FY18F (4Q18F: US$25mn) would be achievable.

Vale Indonesia

(

INCO IJ

)

Source: INCO, IndoPremier Share Price Closing as of : 24-October-2018

2

Refer to Important disclosures in the last page of this report

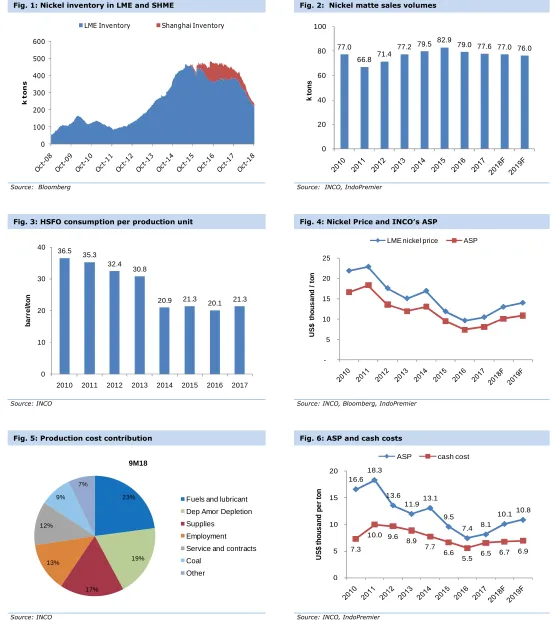

Fig. 1: Nickel inventory in LME and SHME Fig. 2: Nickel matte sales volumes

Source: Bloomberg Source: INCO, IndoPremier

Fig. 3: HSFO consumption per production unit Fig. 4: Nickel Price and INCO’s ASP

Source: INCO Source: INCO, Bloomberg, IndoPremier

Fig. 5: Production cost contribution Fig. 6: ASP and cash costs

Source: INCO Source: INCO, IndoPremier

0

LME Inventory Shanghai Inventory

77.0

66.8 71.4

77.2 79.5 82.9

79.0 77.6 77.0 76.0

0

2010 2011 2012 2013 2014 2015 2016 2017

b

LME nickel price ASP

3

Refer to Important disclosures in the last page of this report

Fig. 7: 3Q18 results summary

(US$ mn) 9M18 9M17 % Y-Y 3Q18 % Q-Q % Y-Y vs. cons vs. ours

Sales 579.6 448.7 29.2 205.0 0.4 30.7 70.4 72.0

COGS 483.1 459.2 5.2 162.1 (2.9) 8.5

Gross profit 96.5 (10.5) nm 42.9 15.2 470.8 74.7 65.4

Opex 8.8 8.1 8.1 3.0 4.8 12.8

Other income 2.9 1.9 52.4 1.0 36.1 41.1

Other expenses 10.2 6.3 63.0 4.6 93.5 300.6

Operating profit 80.4 (23.0) nm 36.3 10.9 721.8 57.4 59.2

Finance costs 5.3 6.0 (12.4) 1.6 (9.0) (13.3)

Pretax income 75.1 (29.0) nm 34.7 12.0 nm 72.7 68.4

Tax (19.6) 9.4 nm (8.7) 2.5 nm

Net Income 55.2 (19.6) nm 25.8 14.5 nm 75.2 68.6

Gross margin 16.6 (2.3) 20.9

Operating margin 13.9 (5.1) 17.7

Pretax margin 13.0 (6.5) 16.9

Net margin 9.5 (4.4) 12.6

Nickel sales volumes (k tons) 54.6 57.7 (5.5) 18.6 (1.0) (9.8) 70.9

ASP (US$/ton) 10,621 7,773 36.6 11,041 1.5 44.9 105.5

4

Refer to Important disclosures in the last page of this report

Year To 31 Dec (US$Mn) 2016A 2017A 2018F 2019F 2020F

Cash & Equivalent 186 222 345 461 530

Receivable 147 166 80 88 97

Inventory 130 118 106 117 129

Other Current Assets 137 92 227 251 275

Total Current Assets 599 597 759 917 1,031

Fixed Assets - Net 1,533 1,494 1,451 1,421 1,423

Goodwill 0 0 0 0 0

Non Current Assets 94 94 88 97 106

Total Assets 2,225 2,185 2,297 2,435 2,560

ST Loans 36 37 37 37 37

Payable 64 61 0 96 106

Other Payables 31 32 27 30 33

Current Portion of LT Loans 0 0 0 0 0

Total Current Liab. 132 129 151 163 175

Long Term Loans 73 36 36 36 36

Other LT Liab. 186 200 210 220 231

Total Liabilities 391 365 397 419 443

Equity 414 414 414 414 414

Retained Earnings 1,420 1,405 1,486 1,601 1,703

Minority Interest 0 0 0 0 0

Total SHE + Minority Int. 1,835 1,819 1,900 2,016 2,117

Total Liabilities & Equity 2,225 2,185 2,297 2,435 2,560

5

Refer to Important disclosures in the last page of this report

Year to 31 Dec 2016A 2017A 2018F 2019F 2020F

Cash Flow

Net Income (Excl.Extraordinary&Min.Int) 2 (15) 80 116 145

Depr. & Amortization 121 125 113 110 108

Changes in Working Capital (116) (12) 126 (8) (9)

Others (124) 136 (9) (125) (22)

Cash Flow From Operating (116) 234 311 93 222

Capital Expenditure (59) (87) (64) (89) (119)

Others 2 3 2 3 4

Cash Flow From Investing (57) (84) (61) (86) (116)

Loans (37) (37) 0 0 0

Operating Margin (%) 3.8 (0.8) 16.9 20.9 23.4

Pre-Tax Margin (%) 0.9 (3.7) 13.6 17.8 20.3

Net Margin (%) 0.3 (2.4) 10.0 13.0 14.9

ROA (%) 0.1 (0.7) 3.6 4.9 5.8

ROE (%) 0.1 (0.8) 4.3 5.9 7.0

ROIC (%) 0.2 (0.7) 4.3 5.9 7.0

Acct. Receivables TO (days) 70.2 90.5 55.6 34.4 34.5

Acct. Receivables - Other TO (days) 0.0 0.0 0.0 0.0 0.0

Inventory TO (days) 4.7 5.0 5.9 6.2 6.0

Payable TO (days) 49.7 36.7 41.1 48.6 50.3

Acct. Payables - Other TO (days) 0.0 0.0 0.0 0.0 0.0

Debt to Equity (%) 6.0 4.0 3.8 3.6 3.4

Interest Coverage Ratio (x) 0.4 (1.0) 0.0 0.0 0.0

Net Gearing (%) (4.1) (8.2) (14.3) (19.3) (21.6)

Head Office

PT INDO PREMIER SEKURITAS

Wisma GKBI 7/F Suite 718

Jl. Jend. Sudirman No.28

Jakarta 10210 - Indonesia

p +62.21.5793.1168

f +62.21.5793.1167

INVESTMENT RATINGS

BUY : Expected total return of 10% or more within a 12-month period HOLD : Expected total return between -10% and 10% within a 12-month period SELL : Expected total return of -10% or worse within a 12-month period

ANALYSTS CERTIFICATION.

The views expressed in this research report accurately reflect the analysts personal views about any and all of the subject securities or issuers; and no part of the research analyst's compensation was, is, or will be, directly or indirectly, related to the specific recommendations or views expressed in the report.

DISCLAIMERS