Optimal monetary policy: is price-level targeting

the next step?

Patrick Minford and David Peel (Cardi® University)

¤revised 16 July 2003

Abstract

We examine whether in°ation targeting should be regarded as opti-mal. Targeting in°ation implies (undesirably) that price level variance tends to in¯nity: we produce some evidence from both a representative agent model and a long-used forecasting model that, once an endogenous indexation response is allowed for, price level targeting imposes no extra costs of macro variability, indeed gives signi¯cant gains.

The 1990s have been a rather successful period for monetary policy. In°ation has been low and the world economy rather stable, at least since the modest recession of 1990{92. Some (e.g. Clarida et al, 1999) have declared victory, lauding the `science' of using interest rate manipulation to achieve both low in°ation and output stability. However, concerns remain. The principal one is whether monetary policy should neglect the price-level as opposed to in°ation | and a number of papers have addressed this issue using a variety of frameworks. A second is whether we can treat Phillips Curves as stable relationships in terms of Lucas' critique (Lucas, 1976). This paper is an attempt to round up some of these issues and consider where we are in our search for the optimal monetary policy.

One issue we will not pursue here is that of de°ationary environments and the zero bound on interest rates. Price level targeting (around a rising deterministic trend) could, it has been argued, be a help in such environments in that it creates an automatic expectation of future in°ation when prices fall, so lowering real interest rates in a de°ation. Others have argued that it increases the risk of hitting the zero bound because after in°ationary episodes prices have to be forced downwards in a potentially de°ationary way back to the target trajectory. Our simulations throughout assume an environment in which the zero bound is avoided and so we cannot shed light on this issue here; we hope to return to it in future work.

¤We are grateful for useful comments, without implicating them in our errors, to Harris

In probing the idea of stationarity in targeting | that is, targeting the level of money rather than its growth rate, and the level of prices rather than in°a-tion | we are joining a growing literature that is investigating the possibility of `price stability', de¯ned to mean prices whose long-term variance is kept low (as opposed to `low in°ation' under which price variance tends to in¯nity as the horizon lengthens). As noted by Svensson (1999a, b), the consensus of ear-lier authors (Hall, 1984; Duguay, 1994; Bank of Canada, 1994; Fischer, 1994) has been that targeting prices rather than in°ation (and presumably also by implication money rather than its growth rate) would lower long-term price variance at the expense of higher short-term in°ation and output variance. As he puts it `The intuition is straightforward: in order to stabilize the price level under price-level targeting, higher-than-average in°ation must be succeeded by lower-than-average in°ation (apparently implying) higher in°ation variability (which) via nominal rigidities would then seem to result in higher output vari-ability.' One could add that the consensus on what monetary policy should be is an interest rate rule that targets in°ation and the output gap or variants of these such as nominal GDP growth | for example, Taylor (1993) who began this vogue following Henderson and McKibbin (1993), Clarida, Gali and Gertler (1999) and McCallum and Nelson (1999a). Svensson argues however that the consensus may be wrong: he gives an example where discretionary monetary policy facing a Phillips Curve with persistence in output actually raises in°ation variability (without bene¯ting output stability) if it targets in°ation rather than the price level | in e®ect the price level target is preventing some of the `useless' in°ationary discretion (useless because private agents fully anticipate it so that it has no e®ect on output). This result admittedly depends on there being no commitment that would rule out such useless discretion by other means | with such commitment price-targeting is inferior to in°ation-targeting. Kiley (1998) also notes that Svensson's set-up is one of `policy ine®ectiveness' on output (as in Sargent and Wallace's original paper, 1975) and hence no trade-o®s arise with output stability; there is, as Svensson puts it, a free lunch in the model as price-level targeting reduces the in°ation bias with no cost in output stability. Svensson's approach has been followed up by others, including Vestin (2000) and most recently Nessen and Vestin (2000); they ¯nd that within a Phillips Curve with forward- and backward-looking expectations (where there is no such free lunch) average in°ation targeting (a weighted average of a price level and in°ation target) can improve on both in°ation and price level targeting, again because of the e®ect that such targeting has in e®ectively limiting discretion.

ar-guments examined optimal monetary policy under commitment. Smets (2000) uses a model with Calvo-style Phillips Curve to examine the optimal horizon for bringing in°ation or the price-level back to their targets; he ¯nds that the optimal length becomes shorter the more forward-looking are the price expec-tations and the steeper is the Phillips Curve. Williams (1999) evaluates a va-riety of such rules in the FRB large-scale model of the US in which there is a forward/backward-looking Phillips Curve and inertial pricing dynamics as in Fuhrer and Moore (1995). He ¯nds that multi-period in°ation targeting ranks highly and that price-level targeting only causes minor output instability. With this family of models, interest rate rules of the Taylor-Henderson-McKibbin type give good results, with the optimal degree of inertia in response (the lagged in-terest rate coe±cient) depending on the degree of forward-lookingness. In this commitment context the addition of price level targeting at a suitably long hori-zon has little e®ect on the optimal trade-o® | as such it an innocuous optional extra for policy-makers desiring to anchor the long-run price level.

Commitment thus basically removes the bene¯ts of price-level targeting. However, little attention in this work has been paid to the e®ect of changes in wage contract structure in evaluating price level targeting | an `interesting issue', Svensson notes, as yet unexplored. Minford, Nowell and Webb (2003) set out a model in which the structure of wage contracts responded to the behaviour of the economy. Ascari (2000) and Casares (2002) have examined respectively how the parameters of Taylor-type overlapping ¯xed-wage contract and of Calvo-type price-setters respond. Minford et al use instead a model in which an overlapping wage contract sets wages that do not have to be the same in every contract period; this has the attractive `natural rate property' (Minford and Peel, 2003) according to which expected in°ation at the time of contract-signing does not a®ect expected real wages and so expected output. This property is not possessed by Taylor-type ¯xed-wage or Calvo contracts.

Within the model of Minford et al it turned out that if monetary policy targeted, at the shortest time horizon, the level of a nominal variable (there it was the money supply), then wage indexation would fall because the persistence of shocks to real wages would be reduced; the slope of the Phillips Curve would thus become °atter (while that of the aggregate demand curve would become steeper). These two things in turn caused output stability to increase in the face of real shocks; thus provided monetary shocks could be kept within tight limits such a nominal-level target improved welfare. In this paper we adopt this model to examine the question of whether such level-targeting is optimal and if so whether it should take the form of price-level targeting (as pioneered by the Bank of Sweden in the inter-war period, Berg and Jonung 1999).

model ¯rst and secondly within a long-used forecasting model of the UK. Within both we allow the degree of indexation to respond to the monetary regime. We conclude by suggesting that price level targeting could be a natural next step for monetary rules.

1

The standard approach

One familiar approach to monetary policy optimisation is to assume some sort of Phillips Curve together with a quadratic social objective function in terms of output and in°ation. The latter is justi¯ed as an approximation to the welfare of the representative agent; when expectations of it are taken in forming the best intertemporal plan for monetary policy, it implies a trade-o® between the variances of in°ation and output. Since monetary policy cannot raise the expected level of output and provided there is commitment, the expected rate of in°ation can be set equal to the in°ation target, so that this trade-o® is the focus of policy.

Let us follow the set-up in Svensson (1997), for example. Let the Phillips curve (model) with persistence be:

yt=½yt¡1+®(¼t¡¼et) +²t (1)

The set-up is that the central bank has scope to react to shocks | implicitly because the wage contract underlying this Phillips Curve is longer than the publication/reaction time to the shock. Hence although this appears to be a non-contract supply curve, we are to think of the `period' as being one equal to the length of a contract so that within it policy can react (one can also extend the analysis to explicit overlapping contracts without much di±culty). We also assume that the central bank can set the in°ation rate exactly using its tools of monetary policy; this is obviously unrealistic but it does remind us usefully that it would be optimal if it could | as we shall see it implies that the central bank should totally o®set `demand' shocks occurring elsewhere than in the Phillips Curve. As for `supply' shocks in the Phillips Curve, here represented by ²; we now discover how they should be optimally reacted to.

Using the usual utility function the problem under commitment is:

V (yt¡1) =M ax(wrt¼t; ¼et)Et¡1 n

¡0:5 (¼t¡¼

¤

)2¡0:5¸(yt¡y

¤

)2+¯ V (yt)

o

(2)

The reaction function that emerges is:

¼t =¼

¤

¡ ®¸

1 +®2¸¡¯½2²t

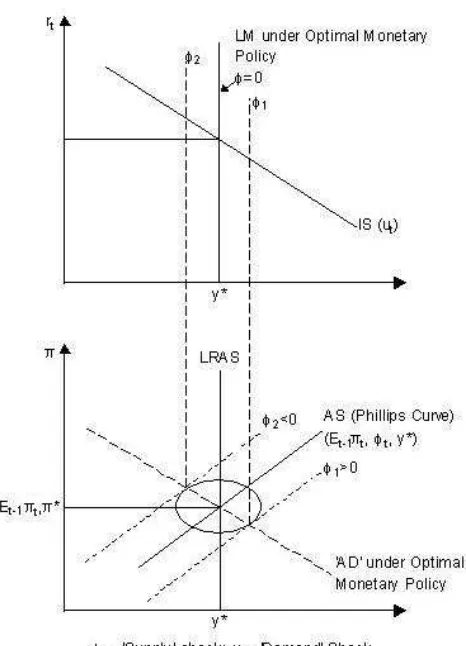

Figure 1: Optimal Monetary Policy

Under the assumption that the central bank can observe current shocks we can then write down the optimal central bank deployment of its instruments. Let the IS curve be:

yt=¡¯ rt+ut (3)

and let the money demand function be:

Mt=¡°(rt+¼

¤

) +±yt+pt+vt (4)

where pt = ¼t+pt¡1 is the log of prices, r is the real rate of interest and

u; vare respectively the aggregate demand and the money demand shocks. Then the optimal real interest rate target will be obtained by substituting for optimal output into (3) as:

b

rt=

1

¯fut¡½yt¡1¡(1 +®b)²tg (5)

and the optimal money supply target will be obtained by substituting the optimal output, real interest rate and price level into (4) to obtain

c

Of course in practice the above set-up needs careful reinterpretation in terms of both the exact speci¯cation of overlapping contracts and the information available to the monetary authorities. The central bank does not observe these shocks and so the practical debate over monetary policy rules is in terms of `e±cient surrogates' for these shocks. For example one could rationalise a `Taylor Rule' under which real interest rates are optimally related (all positively) to the output gap, the in°ation gap (over target) and past real interest rates as follows from (5): the current output gap is a good indicator of the demand shock, u; the current in°ation gap is a good inverse indicator of the supply shock; ¯nally the lagged output gap will also be inversely related (see Fig. 1) to lagged real interest rates. The di±culty in validating this rationalisation is that every model di®ers in detail over these indicator relations. This therefore leads naturally to a discussion of the practical assessment of alternative monetary policy rules, which we will pass over at this stage.

1.1

Optimal monetary policy under Calvo contracts |

another basis for price targeting?

consumption and leisure. The usual derivation also assumes a Calvo contract set-up which gives rise to a rather di®erent Phillips Curve. In this Calvo set-up a similar in°ation-output optimal response can be found as above under such a contract set-up | though there is an issue about the inclusion of lagged output in the response, see also Svensson and Woodford, 2003; McCallum, 2003); in this case in°ation deviations from the target represent distortions of relative prices while output deviations from the natural rate (the °exible-price equilibrium, made optimal by o®setting imperfect competition distortions via a production subsidy) represent output distortions, so that half their squared values represent lost consumer surplus

If one suppresses the error term in the Calvo Phillips Curve on the grounds that it has no easy interpretation, then the usual dilemma for monetary policy | trading o® in°ation versus output variance | disappears. Optimal monetary policy with commitment should then stabilise the price level at its existing level provided there are no other distortions than those associated with shocks to prices and hence also output relative to its °exprice equilibrium | Clarida et al, 1999; Woodford, 2000, Goodfriend and King (2001). Khan, King and Wolman (2002). The reason is that this will imply no further distortions due to price changes: existing distortions, due to past in°ation, cannot be a®ected since each period those changing price are chosen randomly hence one is as likely to add a new distortion by changing prices as one is to o®set a previous price change.

Recent work has explored how sensitive this optimising strategy is to the introduction of capital and adjustment costs and of a demand for cash (e.g. via money in the utility function) and to the removal of the production subsidy so that the °exible price equilibrium is non-optimal | most recently Collard and Dellas (2003) ¯nd that it remains close to optimal, when the non-linearity of the solution is allowed for by higher order Taylor series approximation.

The di±culty with such rules is that there is a potential for time-inconsistency. If for example the history of price shocks has generated a highly skewed relative price distribution or the capital stock is depressed, there is an incentive to pro-duce price changes that would at least partially unwind this history. In general how much can one rely on the policy of price ¯xing being carried out without error? Should prices rise for some reason (e.g. a control failure by the cen-tral bank), then carrying out the commitment by reducing prices subsequently implies that those whose relative prices are already out of equilibrium (due to the price error) will not necessarily be bene¯ted because they may not have the chance to change prices back, while those others still in equilibrium whose prices did not change will be driven out of it if it is their turn to change prices. The time-inconsistent optimum is now to validate the price rise | implying base drift, an in°ation not a price level ¯xing rule. Therefore the commitment optimum of price level stability is fragile | perhaps incapable of credibility. If so, then the Calvo set-up most naturally gives rise to in°ation rules not price level ones.

do not care about price stability. They clearly must, in the sense that if only in°ation is stabilised, this makes the price level a random walk, and so causes the variance of prices to tend to in¯nity the longer the time horizon. This means that the value of longer term contracts set in nominal terms is subject to unacceptable variance; so nominal contracts will be shortened. It does not seem likely that such a forced shortening (or equivalently indexation) of contracts is optimal; indexation is known to su®er from imperfections.

There is also a theoretical reason for questioning the usual Calvo set-up, as argued by Minford and Peel (2003). Calvo contracts must be `indexed up' by agents to allow for ongoing in°ation. Thus:

¼t =¹Et¼t+1+¸(yt¡y

¤

t) +ut (7)

is the Calvo forward-looking Phillips Curve in which e®ectively the whole path of future output (marginal costs) a®ects current price rises. What this implies is that prices are rising because some (relative) prices are rising | which given that there is no general expected in°ation implies that they also rise by this much in nominal terms | and the other prices are held ¯xed in nominal terms (because the menu cost is greater than the cost of them staying out of equilibrium). Thus the basic Calvo equation is conditioned on the assumption that the expected general in°ation rate is zero. To extend the Calvo model it is assumed (e.g. Erceg, Henderson and Levin, 2000; Gali and Monacelli, 2002; Christiano et al, 2002) that it is costless for all agents to uprate prices or wages by the generally expected (or `core') rate of in°ation | this being like a `relabelling' or `indexing' of all prices on the `menu'. Call this core rate of in°ation¼et. Then the equation should be rewritten:

¼t¡e¼t =¹(Et¼t+1¡Ete¼t+1) +¸(yt¡y

¤

t) +ut (8)

Following di®erent practices of di®erent authors, we could emerge with three forms of Phillips Curve:

(a) e¼t=¼t, core in°ation:

¼t=¹Et¼t+1+ (1¡¹)¼t+¸(yt¡y

¤

t) +ut (9)

(b) e¼t=¼t¡1, lagged in°ation:

¼t=

¹

1 +¹Et¼t+1+

1

1 +¹¼t¡1+ ¸

1 +¹(yt¡y ¤

t) +

1

1 +¹ut (10)

(c) e¼t=Et¡1¼t;rational expectations using available (lagged) information:

¼t=Et¡1¼t+¸(yt¡y

¤

Of these three only (c) would be adopted by agents with rational expec-tations. Yet notice that it is merely the original Sargent and Wallace (1975) `surprise Phillips Curve' in which output responds to unexpected prices (or equivalently unexpected in°ation). It no longer implies that in°ation deviations from target produce distorted relative prices; only the current surprise one does so.

Now it remains true under such a rewritten Calvo contract that by the same logic as above we can represent welfare losses by the squared in°ation surprise and squared output deviation. However now we have truly thrown out the baby with the bathwater; not only is there no case for price level targeting, there is also none for in°ation targeting since any in°ation rate is as good as any other | only its predictability matters.

2

Assessing targeting rules in terms of consumer

welfare

It seems unlikely that unconditional variability cannot matter in either in°ation or prices. The rate of in°ation is routinely included in social objective functions; we would wish to use a model in which in°ation did indeed matter for agents' welfare. We would also argue that people must care about price level stability. Chadha and Nolan (2003) argue that macro outcomes are not too di®erent if a price level rule is substituted for a low in°ation rule; e®ectively this is what we wish to examine here. To anticipate our results, we tend to ¯nd the contrary, especially when the contract structure is varied endogenously; but while we would accept that their result comes partly from legitimate di®erences of model speci¯cation, it is this endogeneity of contracts that we believe is likely to be important in making price level targeting a signi¯cant macro factor in most models.

informed by simpler models of what rules can work well, we can only check by trial and error with these stochastic simulations.

The rules we investigate are those that target either the price level or in°ation in the coming period, using information in the current period. The rules set the money supply to hit the planned target exactly; but there is a stochastic error in execution. The money supply therefore does not respond to other current shocks, as would occur for example in an interest-rate setting regime.

To approach optimal monetary policy from this angle we use two sorts of model. First we set out a representative-agent model based on micro foundations and experiment with this; while still too complex to evaluate analytically it is simple enough to develop some insights into the mechanisms involved. Second, we use a UK forecasting model, the Liverpool Model, which has both been in use for two decades reasonably successfully and is based on an IS/LM approximation to the same micro-foundation used in our representative-agent model. Our results are, as above, only preliminary; but we do have some indications of where this approach may lead.

2.1

Targeting within a representative-agent model:

In a recent paper Minford, Nowell and Webb (2003) set up a model where an employed representative agent chooses an optimal degree of wage indexation (to prices and the auction wage) in response to the monetary regime. The model has two exogenous shocks driving it, a demand shock (to the money supply presumed to originate from monetary policy), and a supply (productiv-ity) shock. The productivity shock is (rather naturally) modelled as a random walk throughout. Of course whether the money supply shock is transitory or permanent depends on the monetary rule; if it targets for example the level of money it will be transitory, if targets the money supply growth rate, it will be turned into a random walk The authors then asked whether the monetary regime should target the growth rate or the level of the money supply; or of prices? And should the current money supply be exogenous (as in `monetary base control'), or endogenously ¯xed by an interest rate rule, as is the general practice of central banks? They suggested that these familiar choices appear in an unfamiliar light when indexation is endogenous. When the monetary regime moves to a price level rule with exogenous stationary money supply shocks, the aggregate supply curve °attens (as we have seen already above in our Phillips Curve set-up) and the aggregate demand curve steepens, generating a high de-gree of macro stability (i.e. in the face of supply shocks) provided that money supply shocks themselves are low-variance and stationary.

there is a trade-o® between the interests of the employed (who prefer the price rule) and the unemployed (who prefer the money rule).

They embed the representative household in an environment of pro¯t-maxim-izing competitive ¯rms which on a large proportion of their capital sto ck face a long lag before installation (a simple time-to-build set-up) and a government that levies taxes and pays unemployment bene¯ts (which distort households' leisure decisions and introduce a `social welfare' element into monetary pol-icy). Firms and governments use the ¯nancial markets costlessly and settle mutual cash demands through index-linked loans; since there is no binding cash constraint on these agents, these loans are assumed to be una®ected by the imperfections of the price index which are short term in nature. This model is too simpli¯ed in many ways to match the data of a modern economy whether in trend or dynamics; however its focus is purely on the wage contract decision and its simplicity is justi¯ed in terms of its ability to match the OECD facts about wage contracts.

In calibrating the model the authors chose parameters perceived as plausible for modern OECD economies. The contract length is set at 4 quarters; the elasticity of leisure supply at 3; the share of stocks and other `short-term' capital at 0.3; the average life of other capital at 20 quarters; the share of labour income in value-added at 0.7 (the production function is Cobb-Douglas); the elasticity of the o±cial price index to unanticipated in°ation at 0.2 (implying that a 1% unexpected rise in in°ation would result in a 0.2% temporary overstatement of the price level faced by the representative consumer). The initial values assume 10% unemployment; a capital-output ratio of 6; an average (=marginal) tax rate of 0.10; a real interest rate of 5%.

The government is assumed to smooth both the tax rate and the growth rate of the money supply by borrowing (from ¯rms). Nevertheless it cannot avoid noise in its money supply setting | the source of this could be its inability to monitor the money supply quickly or even at all (for example in the USA the use of dollars by foreigners around the world makes it impossible to know what the domestic issue of dollars is).

Money supply raises prices in the long run, and in the short run also raises output, with persistence extending up to 15 quarters but with most e®ect over after 10. In the high-indexed case there is less real e®ect and less persistence than in the high-nominal case.

the UK which we discus and use in the next section.

Minford et al found that in the face of stationary productivity and money supply shocks indexation would be minimal with only a slight tendency to rise as the variance of money shocks rose dramatically. However when shocks to ei-ther became highly persistent indexation to prices or to their close competitor, auction wages, (which together we term `real wage protection') become large, becoming largest when both shocks are persistent. The reason was that pro-ductivity shocks would disturb prices and so the real worth of nominal wage contracts; indexation was of little use in remedying this disturbance if it was temporary because by the time the indexation element was spent the shock would have disappeared, but with a permanent disturbance indexation can help o®set it with a lag. If into this already-indexed world of persistent productiv-ity shocks, monetary persistence is also injected, indexation rises further, to help alleviate the increased disturbance to real wages. This higher indexation also helps to alleviate the instability in unemployment which accompanies the greater shock persistence of money | the point being that this persistence in-duces persistence in the economy's departure from its baseline and so disturbs unemployment too for longer.

The authors looked at experience in the OECD in the 1970s where it is well-known that real wage protection was substantial; their calibrated model, when estimated variances and persistence of money and productivity shocks were fed into it, predicted high protection in all countries they could cover, apparently in line with the facts. They also found, contrary to much casual comment, that there was little evidence of any diminution of real wage protection in the 1990s; the model also predicted as much, for even though the variance of money supply shocks fell by then, their persistence remained essentially unchanged.

In order to assess the welfare of society from di®erent monetary policy rules the model gives the average household the standard Constant Relative Risk Aversion utility function with Cobb-Douglas preferences across consumption and leisure. The resulting welfare function for the policy-maker to maximize is therefore:

implying that leisure time is equal to working time when unemploymentat is

zero. We setv= 0:7, based on the marginal valuation of leisure at wages net of unemployment bene¯t. Because households get unemployment bene¯t on their spells of eligible unemployment, at, this implies that their choice is distorted;

course they must pay for the bene¯t burden via taxes; the present discounted value of this tax burden is the same as this bene¯t bill and so we deduct this from their consumption to obtain total private utility.

In subsequent work Minford and Nowell, 2003, use this model to examine the relative merits of in°ation | and price-level targeting. The target rule holds current money supply exogenous at last period's target setting and chooses a money supply for next period that forces the expected in°ation (price level) to be on target in this next period; this money supply plan is however executed with an error, the model's 'monetary shock.' (which can in practice be interpreted as a shock on either the supply or demand side of the money market; it is the model's demand shock).. There is thus no current response of money supply to shocks; nor any implied interest rate smoothing in the current period.

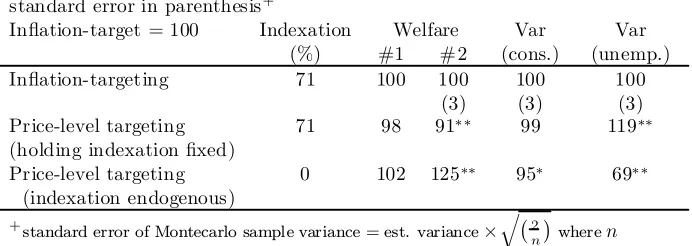

Their results can be summarised simply. In°ation-targeting generates a high degree of indexation. When price-level targeting is undertaken but indexation is assumed constant, welfare falls, because the variability of unemployment rises sharply. But when indexation is allowed to change endogenously, it drops to nil and the result is a rise in welfare, with the variance of consumption down somewhat and that of unemployment down substantially.

Table 1: Price-level and in°ation targeting compared within a calibrated repre-sentative agent model

standard error in parenthesis+

In°ation-target = 100 Indexation Welfare Var Var (%) #1 #2 (cons.) (unemp.) In°ation-targeting 71 100 100 100 100

(3) (3) (3) Price-level targeting 71 98 91¤ ¤

99 119¤¤

(holding indexation ¯xed)

Price-level targeting 0 102 125¤¤

95¤

69¤ ¤

(indexation endogenous)

+

standard error of Montecarlo sample variance = est. variance£q¡2

n

¢

wheren

is the number of sample observations (here 2000) | source Wallis, 1995 De¯nition: #1 is the standard CRRA formula in the text; #2 is the weighted average (weight on consumption= 0:7, on unemployment= 1:0) of the two (inverted) variances.

¤

signi¯cant at10%level

¤

signi¯cant at1%level

2.2

Targeting within the Liverpool forecasting model of

the UK

they would need to see evidence that they perform adequately in a variety of possible macro structures. Thus we would like a full menu of shocks within a model that has been estimated empirically and that has withstood the test of forecasting as well as applied policy analysis; preferably this model should be one that is derivable from the sort of micro-foundations of our simple model. Fortunately we have available a model that answers roughly to this description: the Liverpool Model of the UK. This is an open economy version of a rational expectations IS-LM model, such as can be derived from a micro-founded model by suitable approximations (McCallum and Nelson, 1999b) | thus for example the Liverpool Model IS curve has the expectation of future output in it, the hallmark of this approximation. The model's Phillips or Supply curve assumes overlapping wage contracts as in our simple model. The labour market under-pinning it is explicit and the model solves for equilibrium or natural rates of output, unemployment and relative prices. In recent work a new FIML algo-rithm developed in Cardi® University (Minford and Webb, 2000) has been used to reestimate the model parameters: it turns out that the new estimates are little di®erent from the model's original ones, based partly on single-equation estimates, partly on calibration from simulation properties.

The model has been used in forecasting continuously since 1979, and is now one of only two in that category. The other is the NIESR model, which however has been frequently changed in that 20-year period: the only changes in the Liverpool Model were the introduction of the explicit natural rate supply-side equations in the early 1980s and the shift from annual data to a quarterly version in the mid-1980s. In an exhaustive comparative test of forecasting ability over the 1980s, Andrews et al (1996) showed that out of three models extant in that decade | Liverpool, NIESR, and LBS | the forecasting performance of none of them could `reject' that of the others in non-nested tests, suggesting that the Liverpool Model during this period was, though a newcomer, at least no worse than the major models of that time. For 1990s forecasts no formal test is available, but the LBS model stopped forecasts and in annual forecasting post-mortem contests the NIESR came top in two years, Liverpool in three. Thus we would suggest that the Liverpool Model has a respectable forecasting record, at least on a par with the only other model available of the general type we seek | viz. micro-founded and suitably estimated. Comparative work on the NIESR model would also be of interest; so far it has not been possible. There are also models in the public sector | those of the Treasury and the Bank of England | however, we would question the extent to which they have suitable micro-foundations for our purpose and their forecasting record is also unclear.

Lastly, in respect of simulation properties and use of these for policy analysis, we note that the Liverpool Model has been extensively used in policy analysis bearing on the `monetarist' and `supply-side' reforms of the Conservative gov-ernments of Margaret Thatcher. It is now generally conceded that these reforms have been broadly successful; the Liverpool Model acted to some degree as in-tellectual underpinning for them at a time of general academic hostility from UK macroeconomists.

suit-able vehicle for checking the `realism' of our policy conclusion on the simple model that level rules are preferable to rate of change rules for monetary policy. Our method is as before to run these rules in the model in the face of stochastic simulations (further details can be found in Matthews, Meenagh, Minford and Webb, 2003) . We shock the full range of endogenous and exogenous errors, exactly as in the model speci¯cation. The model's wage equation is written in terms of the real wage reacting to the real bene¯t rate and to unemployment, which are the auction wage components (implicitly the auction wage element has a weight of 0.2), and negatively to the di®erence of the price level from the average forecast of it at the times of wage contracting, then positively to this di®erence lagged.

For our purposes here we adapt it as follows:

Wt =vPt+wEt¡jPt+®(Pt) +w

¤ : : :=

(®+v)(Pt¡Et¡jPt) +Et¡jPt+w ¤

: : :

Now we lag the auction and indexed elements two periods because of a delay due to the ¯rm's internal checking procedures in adjusting pay to the unexpected change in the price level and obtain the real wage as:

Wt¡Pt=¡(Pt¡Et¡jPt) + (®+v)(Pt¡2¡Et¡j¡2Pt¡2) +w

¤ : : :

Hence the two-period-lagged term carries the extent of real wage protection. It is this part that is adjusted endogenously by the employed to minimise the variance of their real wage.

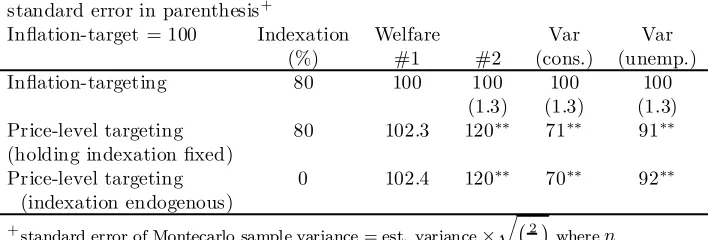

The results within the Liverpool Model (Table 2) are about as favourable to price-level targeting as in the representative-agent model. Again, they show that under in°ation-targeting there is a high degree of indexation and that this would drop to nil under price-level targeting. Similarly, too, they show that if indexation is assumed endogenous, welfare will rise signi¯cantly if price-level targeting is introduced; in the Liverpool Model the variance of consumption falls more and that of unemployment falls less than in the representative agent model but both fall signi¯cantly. The di®erence is that when indexation is held ¯xed, the variances behave very much the same in the Liverpool Model as when index-ation is endogenous; there is still a substantial gain over in°index-ation targeting. One reason for this seems to be that in the Liverpool wage equation the indexation we have assumed as feasible is rather imperfect. Thus real wages even under the fullest indexation are disrupted by a persistent price shock; eliminating this persistence gives gains that are almost as large as under zero indexation. A fur-ther reason for the improved stability under price-level targeting is that, on the demand side, ¯nancial wealth e®ects are dampened since price shocks (to the real value of long-term nominal bonds) are temporary rather than permanent.

2.3

Conclusions

Table 2: Price-level and in°ation targeting compared within the Liverpool Model

standard error in parenthesis+

In°ation-target = 100 Indexation Welfare Var Var (%) #1 #2 (cons.) (unemp.) In°ation-targeting 80 100 100 100 100

(1.3) (1.3) (1.3) Price-level targeting 80 102:3 120¤¤

71¤¤

91¤¤

(holding indexation ¯xed)

Price-level targeting 0 102:4 120¤¤

70¤¤

92¤¤

(indexation endogenous)

+

standard error of Montecarlo sample variance = est. variance£q¡2n

¢

wheren

is the number of sample observations (here 12078) | source Wallis, 1995 De¯nition: #1 is the standard CRRA formula in the text; #2 is the weighted average

(weight on consumption= 0:7, on unemployment= 1:0) of the two (inverted) variances.

¤

signi¯cant at 5% level

¤

signi¯cant at 1% level

or the price level both within a representative-agent model and within a `live' forecasting model of the UK. We found in both some con¯rmation of the idea: that targeting the price level would bring a signi¯cant gain in output stability, rather than the loss usually assumed,. because the endogenous response of reduced indexation would enhance the economy's stability..

References

[1] Andrews, M.J., P. Minford and J. Riley (1996) `On comparing macroeco-nomic models using forecast encompassing tests', Oxford Bulletin of Eco-nomics and Statistics, Vol. 58, No. 2, 1996, pp. 279-305.

[2] Ascari, G. (2000) `Optimising agents, staggered wages and persistence in the real e®ects of money shocks',Economic Journal, 110 (July), 664-686.

[3] Bank of Canada (1994) Economic behaviour and Policy Choice under Price stability, Ottawa.

[4] Berg, Claes and Lars Jonung (1999) `Pioneering price level targeting: the Swedish experience 1931-37', Journal of Monetary Economics, 43(3), June 1999, pp525-551.

[5] Casares, M. (2002) `Price setting and the steady-state e®ects of in°ation', European Central Bank working paper no.140, May 2002, ECB, Frankfurt.

[7] Christiano, L., Eichenbaum, M. and Evans, C. (2002) `Nominal rigidities and the dynamic e®ects of a shock to monetary policy', Mimeo, Northwest-ern University.

[8] Clarida, R., J. Gali, and M. Gertler (1999) `The science of monetary policy: a New Keynesian perspective', Journal of Economic Literature, 37(4), pp. 1661-1707.

[9] Collard, F., and H. Dellas (2003) 'In°ation targeting', mimeo, University of Bern

[10] Duguay, Pierre (1994) `Some thoughts on price stability versus zero in°a-tion', working paper, Bank of Canada | presented at the conference on Central Bank Independence and Accountability, Universita Bocconi, Milan, March 1994

[11] Erceg, C.J., Henderson, D.W., and Levin, A.T. (2000) `Optimal monetary policy with staggered wage and price contracts',Journal of Monetary Eco-nomics, 46, October, 281-313.

[12] Fischer, S. (1994) `Modern central banking', in Capie, F. et al The Future of Central Banking.

[13] Fuhrer, J. and G. Moore (1995) `In°ation persistence', Quarterly Journal of Economics, 110(1), 127-159.

[14] Gali, J., and Monacelli, T. (2002) `Monetary policy and exchange rate volatility in a small open economy', Mimeo, Universitat Pompeu Fabra.

[15] Goodfriend, M. and King, R. (2001) 'The case for price stability', NBER working paper 8423.

[16] Hall, Robert E. (1984) `Monetary strategy with an elastic price standard', in Price Stability and Public Policy, Federal Reserve Bank of Kansas City, Kansas City, 137-159.

[17] Henderson, D.W., and McKibbin, W.J. (1993) `An assessment of some basic monetary-policy regime pairs: analytical and simulation results from simple multi-region macroeconomic models', in R.C. Bryant, P. Hooper and C.L. Mann (eds.), Evaluating policy regimes | new research in empirical macroeconomics, Washington DC: Brookings Institution.

[18] Khan, A., King, R., and Wolman A.L. (2002) 'Optimal monetary policy', Federal Reserve Bank of Philadelphia working paper no. 02-19.

[19] Kiley, M. T. (1998) `Monetary policy under neoclassical and new-Keynesian Phillips Curves, with an application to price level and in°ation targeting',

[20] Lucas, R.E. Jr (1976) `Econometric policy evaluation : A critique', in K. Brunner and A.H. Meltzer (eds),The Phillips Curve and Labour Markets, Carnegie Rochester Conference Series on Public Policy No. 1, Supplement to the Journal of Monetary Economics.

[21] McCallum, Bennett T. and Edward Nelson (1999a) `Nominal income tar-geting in an open economy optimising model', Journal of Monetary Eco-nomics, 43(3), June 1999, pp. 553-578.

[22] McCallum, Bennett T. and Edward Nelson (1999b) `An optimising IS-LM speci¯cation for monetary policy and business cycle analysis', Journal of Money, Credit and Banking, 31(3), August 1999, Part 1, pp. 296-316.

[23] McCallum, Benett T. (2003) 'Comment on "Implementing Optimal Policy Through In°ation-Forecast Targeting"' forthcoming in edited proceedings of the NBER Conference on In°ation Targeting, January 23-25, 2003, in Bal Harbour, Florida.

[24] Matthews, K., D. Meenagh, P. Minford and B. Webb (2003) `Stochas-tic simulations of monetary policy using the Liverpool Model of the UK', mimeo, Cardi® University.

[25] Minford, A.P.L. (1980) `A rational expectations model of the United King-dom under ¯xed and °oating exchange rates', in K. Brunner and A.H. Meltzer (eds)On the State of Macroeconomics, Carnegie Rochester Con-ference Series on Public Policy,12, Supplement to the Journal of Monetary

Economics.

[26] Minford, A.P.L. (1995) `Time-inconsistency, democracy and optimal con-tingent rules',Oxford Economic Papers,47, 195{210.

[27] Minford, P., E. Nowell and B. Webb (2003) `Nominal contracting and mon-etary targets | drifting into indexation'Economic Journal, January,113,

65-100.

[28] Minford, P. and E. Nowell (2003) `Optimal monetary policy with endoge-nous wage contracts: is there a case for price level targeting?' revised version of CEPR discussion paper no. 2616, 2000,; mimeo, Cardi® Univer-sity.

[29] Minford, P., and D. Peel (2003) `Exploitability as a speci¯cation test of the Phillips Curve', mimeo, Cardi® University.

[30] Minford, P. and Bruce Webb (2000) `Estimating large rational expectations models by FIML | a new algorithm with bootstrap con¯dence limits', mimeo Cardi® University, revised 2003.

[32] Rotemberg, J.J. and M. Woodford, `An optimization-based econometric framework for the evaluation of monetary policy', in B.S. Bernanke and J.J. Rotemberg, eds., NBER Macroeconomics Annual 1997, 297-346.

[33] Sargent, T.J. and Wallace, N. (1975) `Rational expectations, the optimal monetary instrument and the optimal money supply rule',Journal of Po-litical Economy,83, 241{54.

[34] Smets, F. (2000) `What horizon for price stability?' European Central Bank working paper no. 24, July 2000, ECB, Frankfurt.

[35] Svensson, L. E.O. (1997) `Optimal in°ation targets, \conservative" central banks, and linear in°ation contracts',American Economic Review,87, 98{

114.

[36] Svensson, Lars E.O. (1999a) `Price level targeting versus in°ation targeting: a free lunch?' Journal of Money Credit and Banking, 31(3), pp277-295, August, 1999.

[37] Svensson, Lars E.O. (1999b) `Price stability as a target for monetary sta-bility: de¯ning and maintaining price stability', discussion paper no. 2196, August 1999, Centre for Economic Policy research, London.

[38] Svensson, Lars E. O., and Michael Woodford (2003) 'Implementing opti-mal policy through in°ation-forecast targeting' Working Paper, Princeton University.

[39] Taylor, J.B. (1993) `Discretion versus policy rules in practice', Carnegie-Rochester Series on Public Policy 39, pp. 195-214.

[40] Vestin, David (2000) `Price-level targeting versus in°ation targeting in a forward-looking model', mimeo, IIES, Stockholm University.

[41] Wallis, K.F. (1995) `Large-scale macroeconometric modelling' in H.Pesaran and M.Wickens (eds.)Handbook of Applied Econometrics, Blackwell.

[42] Williams, J. C. (1999) `Simple rules for monetary policy', mimeo, Federal Reserve Board, February 1999, Washington D.C.