PLEASE SCROLL DOWN FOR ARTICLE

On: 14 December 2009

Access details: Access Details: [subscription number 912988913]

Publisher Routledge

Informa Ltd Registered in England and Wales Registered Number: 1072954 Registered office: Mortimer House,

37-41 Mortimer Street, London W1T 3JH, UK

Accounting Education

Publication details, including instructions for authors and subscription information:

http://www.informaworld.com/smpp/title~content=t713683833

Understanding Students' Choice of Academic Majors: A Longitudinal

Analysis

Lin Mei Tan a; Fawzi Laswad a a Massey University, New Zealand

To cite this Article Tan, Lin Mei and Laswad, Fawzi(2009) 'Understanding Students' Choice of Academic Majors: A Longitudinal Analysis', Accounting Education, 18: 3, 233 — 253

To link to this Article: DOI: 10.1080/09639280802009108 URL: http://dx.doi.org/10.1080/09639280802009108

Full terms and conditions of use: http://www.informaworld.com/terms-and-conditions-of-access.pdf

This article may be used for research, teaching and private study purposes. Any substantial or systematic reproduction, re-distribution, re-selling, loan or sub-licensing, systematic supply or distribution in any form to anyone is expressly forbidden.

Understanding Students’ Choice

of Academic Majors: A Longitudinal

Analysis

LIN MEI TAN and FAWZI LASWAD

Massey University, New Zealand

Received: July 2007 Revised: December 2007 Accepted: December 2007

ABSTRACT This study extends Tan and Laswad’s 2006a study by surveying the same students at the beginning and end of their degree programme at a New Zealand university regarding their major choices, beliefs and attitudes towards majoring in accounting or a non-accounting discipline. Using the theory of planned behaviour, the objectives are to compare intentions with behaviour in relation to majoring in accounting and other business disciplines and to examine changes in attitudes and beliefs between the beginning and end of university study. The results indicate many students choose majors that are consistent with their intentions at the beginning of their university study but some students also change their intentions and major in other areas. Some attitudes and beliefs change over time but the major choice tends to remain relatively stable. The results suggest that a higher proportion of accounting students than other business students decide on their major prior to university study. This may suggest that promoting accounting as a career may need to focus on pre-university students.

KEY WORDS: Accounting major, accounting education, accounting career, theory of planned

behaviour

Introduction

Over the past two decades, significant research in accounting education has been devoted to understanding how and why students major in an accounting or a non-accounting dis-cipline. Such research is pertinent—particularly when the number and quality of students majoring in accounting is declining (Ashworth, 1969; Adamset al., 1994; Karneset al., 1997; Stice and Swain, 1997; Saemann and Crooker, 1999; Mauldin et al., 2000; Heaton, 1999; Fedoryshyn and Tyson, 2003) and when accounting firms are facing difficulties in recruiting and retaining staff (Ahmedet al., 1997; Marshall, 2003).

Vol. 18, No. 3, 233 – 253, June 2009

Correspondence Address:Ms Lin Mei Tan, School of Accountancy, Massey University, Palmerston North, Private Bag 11222, New Zealand. Email: [email protected]

0963-9284 Print/1468-4489 Online/09/030233 – 21#2009 Taylor & Francis DOI: 10.1080/09639280802009108

Prior research on students’ choice of major has identified a multitude of factors that could influence students’ major decisions. They include: availability of employment and earnings (Paolillo and Estes, 1982; Adamset al., 1994; AuYeung and Sands, 1997; Lowe and Simons, 1997), job satisfaction, aptitude, and interest in subject areas (Paolillo and Estes, 1982; Gulet al., 1989; AuYeung and Sands, 1997), and the influence of stu-dents’ teachers and parents (Paolillo and Estes, 1982; Cangelosiet al., 1985; Gulet al., 1989; Geiger and Ogilby, 2000). Studies that surveyed students’ perceptions were primar-ily conducted at specific points in time, such as in the first, second, third, or fourth year of undergraduate study, and focused on either students’ chosen major or their intention to major in a particular discipline. Apart from a few studies (such as by Cohen and Hanno, 1993; Allen, 2004; Tan and Laswad, 2006a), many prior studies lack a conceptual framework, making it difficult to generalise predictions or explain career choice decisions (Cohen and Hanno, 1993, p. 221).

The theory of planned behaviour (Ajzen, 1988) is one conceptual framework that has been used to provide a better understanding of the factors that influence students’ choice of major. This theory has been used successfully in explaining intentions and behaviours in various decision-making situations such as exercising, purchasing goods, etc. Tan and Laswad (2006a) used this theory to examine first year students’ intentions to major in accounting and other business disciplines. They found that students’ attitudes, subjective norms and perceptions of behavioural control influence their intention to major in accounting or other business disciplines. However, they did not examine the relationship between intention and behaviour because students’ behaviour (i.e. ultimate major) could not be ascertained in their cross-sectional study, as the data was collected at the beginning of the introductory accounting course. The studies conducted by Allen (2004) and Cohen and Hanno (1993) were also cross-sectional and used surrogate measures of intention that were not antecedents of choosing a major. They further assumed that students would not change their major intentions during the students’ aca-demic career.

We extend Tan and Laswad’s (2006a) research by conducting a longitudinal study that allows us to

(i) examine the students’ attitudes and beliefs with respect to intentions to major in a business discipline (accounting or non-accounting) at the start of their first course in accounting that is mandatory for all business students; and

(ii) use this information to compare with their actual major choices three years later. Such a design not only allows us to test the theory of planned behaviour but also to understand whether there are changes in the students’ attitudes and beliefs about account-ing and non-accountaccount-ing disciplines over time as the students mature in terms of experience and knowledge. Students’ intentions may change because of changes in attitudes and beliefs, and the ultimate behaviour may therefore differ from their earlier intentions. The results of this study extend our understanding of students’ major choices and provide insights into ways to attract students or improve their attitudes and beliefs toward the study of accounting as an academic discipline.

This paper is organised as follows. The next section provides a review of the literature that examines the various influences on students’ choice of academic major. This is followed by an overview of the theory of planned behaviour, the research method, the data and the results. The final section discusses the conclusions and limitations of the study.

Literature Review

Considerable literature has emerged which examines the timing of students’ career choices and the major influences on their choices. The following is a brief review of relevant studies.1

Students vary as to when they make their academic major choices. Some students select their intended major prior to commencing university study (Karneset al., 1997; Jackman and Hollingworth, 2005), while others make such decisions during or at the completion of their first or second year of tertiary education (Hermanson and Hermanson, 1995; Mauldin

et al., 2000). Some students may even change their major in a later stage of their academic study when they realise that their intended major or chosen major does not suit them for various reasons.

A number of factors influence students’ discipline choice. Prior studies suggest that accounting students’ discipline choice is heavily influenced by earnings potential and job market conditions or opportunities (Paolillo and Estes, 1982; Gul et al., 1989; Inman et al., 1989; Adams et al., 1994; Felton et al., 1994; AuYeung and Sands, 1997; Lowe and Simons, 1997; Mauldin et al., 2000). For example, Ahmed et al.

(1997) found that New Zealand students who intend to pursue a career in chartered accountancy place significantly greater importance on financial factors. Lowe and Simons’ (1997) findings in the USA also indicate that future earnings are the most import-ant influence for accounting, finance and management majors.

Students’ experiences with uninteresting accounting coursework and rote learning may also discourage the best students from pursuing an accounting major (Immanet al., 1989). Students are more likely to choose an accounting major when they consider accounting interesting and enjoyable (Saeman and Crooker, 1999).

Students’ performance in the introductory accounting course is another possible factor that may influence their major choice, as students tend to perceive success in the introduc-tory course as a signal that they have an aptitude for accounting (Cohen and Hanno, 1993; Geiger and Ogilby, 2000). Poor performance, on the other hand, may be perceived by stu-dents as a signal that they may not have the required aptitude for accounting and, therefore, should pursue a non-accounting major. However, some studies (such as by Adamset al., 1994; Allen, 2004; Stice and Swain, 1997) suggest that course performance is not signifi-cantly related to high performing students’ decisions to major in accounting.

The intrinsic appeal of the job itself, such as job satisfaction, opportunity to be creative, autonomy, intellect, and a challenging and dynamic working environment, is another factor that may influence students’ academic major choice. A number of studies indicate that job satisfaction, for instance, is important in accounting students’ discipline choice (Paolillo and Estes, 1982; Gulet al., 1989; AuYeung and Sands, 1997) but not as import-ant as many other factors (Paolillo and Estes, 1982; Feltonet al., 1994).

Prior research suggests that college students choose specific majors that they perceive as being compatible with their particular personal styles (Gul, 1986; Wolk and Cates, 1994) or their own aptitude for the subject (Paolillo and Estes, 1982; Gulet al., 1989; AuYeung and Sands, 1997). Adamset al. (1994) and Mauldinet al. (2000) indicate that genuine interest in the subject is an important selection factor. Skills and background in mathemat-ics were also identified as factors that could facilitate or hinder students’ decisions to major in accounting (Cohen and Hanno, 1993).

In making career choices, students may be further influenced by their accounting instructors, parents, relatives, friends, or high school teachers. A secondary school career counsellor or adviser may shape students’ perceptions of accounting and the profession (Marshall, 2003). However, empirical evidence shows mixed results. Some

studies suggest that teachers or instructors do not play a significant role in students’ choice of majors (see Cangelosiet al., 1985; Gulet al., 1989) whereas other studies (Paolillo and Estes, 1982; Hermanson and Hermanson, 1995; Geiger and Ogilby, 2000; Mauldinet al., 2000) suggest that individual instructors have a profound influence on students’ decisions to major in accounting.

Empirical evidence regarding the influence of referents, other than instructors, was also inconclusive. Cangelosi et al.(1985) found that friends do not influence most students toward or away from accounting careers. Gulet al.(1989) note that parental influence is not a significant factor in students’ discipline choice decisions. Similarly, Paolillo and Estes (1982), Hermanson and Hermanson (1995), and Lowe and Simons (1997) indi-cate that friends, parents and high school teachers are less influential factors in students’ major choices. In contrast, Inmanet al.(1989) and Mauldinet al.(2000) found that parents followed by instructors, have a strong influence on students’ choice of majors.

One of the main deterrents to majoring in accountancy could be the poor public percep-tion of the stereotypical accountant as dreary, cautious and boring number crunchers (Luscombe, 1988; Horowitz and Riley, 1990; Fisher and Murphy, 1995; Hermanson and Hermanson, 1995; Cohen and Hanno, 1993). Such pre-conceived ideas can result in college students’ self-selection into or out of certain majors. Accountants’ work is also perceived by students to be excessively time-consuming and unpleasant (Mauldinet al., 2000), or as being narrow, audit-focused and restricted to ‘core’ accounting (Marshall, 2003).

The literature reviewed above indicates that a number of factors may influence students in choosing their academic majors. Moreover, students may regard some factors as more important than others and these factors may have a different impact in different cultures (AuYeung and Sands, 1997). The inconsistencies in results obtained from prior research make it difficult to draw generalisations about students’ choices of majors. A theoretical framework would provide a better understanding of the impact of various factors on students’ academic decisions.

Theory of Planned Behaviour

The theory of planned behaviour (TPB) developed by Ajzen (1988) is an extension of the theory of reasoned action (TRA) developed by Fishbein and Ajzen (1975). Both models consider attitudes, subjective norms, intentions and target behaviour. In summary, the TPB posits that people act in accordance with their intentions and perceptions of control over the behaviour, while intentions in turn are influenced by attitudes towards the behaviour, subjective norms, and perceptions of behavioural control (Ajzen, 2001, p. 43). The more favourable the attitude and subjective norm and the greater the perceived behavioural control are, the greater the likelihood the person’s intention to perform the behaviour. Figure 1 depicts the three factors that determine intentions, which lead to behaviour.

Individual attitudes toward the behaviour reflect the degree to which a person has a posi-tive or negaposi-tive perception of the behaviour. Attitudes about behaviour are determined by a person’s beliefs about the consequences of performing that behaviour, and each belief is weighted by the subjective value of the outcome in question (Ajzen, 2001; Tan and Laswad, 2006a).

Subjective norms, however, are linked to a person’s perceptions of social pressure to perform or not perform the behaviour. It reflects a person’s beliefs that other individuals or groups think he or she should perform the behaviour (i.e. normative beliefs). These nor-mative beliefs, in combination with a person’s motivation to comply with the different

referents, determine the prevailing subjective norm regarding the behaviour (Ajzen, 2001; Tan and Laswad, 2006a).

As many factors can interfere with an individual’s control over an intended behaviour (Cohen and Hanno, 1993, p. 222), Ajzen’s (1988) theory of planned behaviour refines the TRA by including the concept of behavioural control. Unlike attitude and subjective norms, this third factor, perceived behavioural control, is a non-motivational factor and represents the degree of control a person has over performance of the behaviour. To the extent that people are realistic in their judgements of behaviour difficulties, Ajzen posits that a measure of perceived behavioural control can act as a surrogate for actual control. The theory further assumes that perceived behavioural control has motivational implications for intentions. Those who believe that they have neither the means nor the opportunities to perform certain behaviour are unlikely to form strong behavioural inten-tions to engage in it, even if they hold favourable attitudes toward the behaviour and believe that important individuals would approve of their performing such behaviour (Ajzen, 1988, p. 134).

The TPB, therefore, provides a suitable framework for examining the factors that influ-ence students’ academic major decisions, and it has been used by Tan and Laswad (2006a), Allen (2004), and Cohen and Hanno (1993), in their studies of students’ academic major choices or intentions.

Based on the TPB framework, this study extends Tan and Laswad (2006a) by compar-ing intentions with behaviour and examincompar-ing whether specific personal, referents, and control factors influence students’ intentions and ultimate decisions to major or not to major in accounting.

Research Method

Subjects

Prior studies have used a cross-sectional design to examine students’ major decisions, either using accounting/non-accounting major students or accounting graduates who have completed their career choice process (Cherry and Reckers, 1993; Cohen and Hanno, 1993; Ahmedet al., 1997). This study, however, provides a longitudinal examin-ation of students’ attitudes, beliefs and major decisions. Data about attitudes, beliefs and major intentions were collected from business students in their first year at university when they enrolled in the introductory accounting course, a compulsory course for the business degree. Data was also collected in the third year of study for the same students, when most students have confirmed their major choices.2

Questionnaire

The questionnaire contained items designed to assess the three major constructs in the TPB: attitudes, subjective norm and perceived behavioural control. These constructs were assessed by means of several direct questions, which were modelled on Cohen

Figure 1.Ajzen’s (1988) theory of planned behaviour

and Hanno’s (1993) questionnaire, with some minor modifications to reflect the New Zealand academic environment. Prior studies have identified these constructs as having significant effects on students’ choice of academic major or career (such as by Paolillo and Estes, 1982; Gulet al., 1989; Inmanet al., 1989; Adamset al., 1994; Feltonet al., 1994; AuYeung and Sands, 1997; Lowe and Simons, 1997; Mauldinet al., 2000).

The questionnaire was divided into two parts. Part 1 of the questionnaire solicited infor-mation about their major. In the first year, students were asked about the discipline in which they intended to major. In the third year survey, students were asked their study major, the timing of their major choice and the reasons for changing their major if they did so.

Part 2 of the questionnaire was further divided into Sections A, B and C. Section A sought the respondents’ attitudes (personal perceptions) to particular outcomes (see Table 1) and the likelihood of achieving those outcomes if they major in accounting or non-accounting disciplines. The steps involved:

1. evaluating 10 outcome statements on a five-point scale (1¼extremely bad to 5¼

extremely good);

2. indicating the likelihood that each of the outcomes would occur if they choose account-ing as their major, usaccount-ing a five-point scale (1¼very unlikely to 5¼very likely);

3. indicating the likelihood that each of the outcomes would occur if they choose a non-accounting major, using a five-point scale (1¼very unlikely to 5¼very likely).

Section B sought the respondents’ normative perceptions of the referents’ views of their choice of major and the degree of importance they placed on the referents’ views. Using a five-point scale (1¼strongly disagree to 5¼strongly agree), respondents were asked to

indicate their agreement or disagreement with the statement that their parents/other rela-tives/friends/career counsellor (see Table 1) thought that they should or should not major in accounting. To ascertain their motivation to comply with the above referents, respon-dents were further asked to indicate how important that person’s opinion is to them using a five-point scale (1¼very unimportant to 5¼very important).

Section C ascertained the respondents’ perceived behavioural control. Respondents were asked to indicate the extent of their agreement on a five-point scale (1¼strongly

disagree to 5¼strongly agree) with each statement that relates to control beliefs (see

Table 1).

Research Design

As the TPB requires measurement of students’ differential perceptions of the three con-structs (personal, referents, and control) towards academic major choices, the differential score as used by Cohen and Hanno (1993) and Allen (2004) was adopted. For personal beliefs, respondents’ evaluations of each of the ten outcomes were first multiplied by the likelihood of the outcome occurring if accounting was their chosen major. They were then summed (a) to provide a measure of the beliefs toward choosing accounting as a major. The ten outcome evaluations were also multiplied by the likelihood of the outcome occurring if a non-accounting major was chosen. The sum (b) of these ten out-comes provides a measure of the beliefs towards choosing a non-accounting major. A differential score is obtained by deducting b from a. Since the theory predicts that positive scores are associated with choice of accounting major, a positive differential score indicates that the student is more favourable towards the choice of accounting as an academic major. Differential scores for perception of important people (referents) and control beliefs were computed in a similar manner.

A path analysis, which is an extension of the regression model, was used to test the TPB in predicting students’ choice of major as shown in Figure 1. The model is specified by the following path equations:

Model 1: Major Choice¼a0þb1Major Intentionþb2Controlþ]

Model 2: Major Intention¼a0þb1Personalþb2Referents1þb3Control1þ]

where:

Major intention¼the self-reported intention to major in an accounting or non-accounting

discipline at the beginning of first year, which assumes a value of 1 if the respondent intends to major in accounting and 0 otherwise

Major choice¼the major choice in an accounting or non-accounting discipline at the end

of third year, which assumes a value of 1 if the respondent majors in accounting and 0 otherwise

Personal¼the differential personal perception of choosing an accounting versus a

non-accounting major at the beginning of first year

Referents¼ the differential perception of important referents about an accounting and a

non-accounting major at the beginning of first year

Control¼ the perceived differential control over choosing an accounting or a

non-accounting major at the beginning of first year

Data Collection

The study was conducted in a large multi-campus New Zealand University with 1422 stu-dents enrolled in the introductory accounting course. The first survey was conducted in

Table 1.Factors (outcomes) used to examine students’ intentions to major in accounting or other business disciplines

Section A—Personal Perception

Section B—Important Referents

Section C—Perceived Control

Career that deals with a lot of numbers

Parents Required workload

Allows one to earn a high initial salary

Relative(s) Skills and background in mathematics

Broad exposure to business Close friend(s) Allows one a chance to establish

a private practice

Career counsellor/adviser Performance in accounting course

Career that is challenging Job opportunities

Career with high future earnings and advancement potential

Interest in accounting

Major that demands a heavy workload

Less involvement in extracurricular activities Career that provides a high social

status

Major that prepares one for a career with more job opportunities

An academic major that is boring

class at the beginning of the introductory accounting course and 1009 students partici-pated, giving a response rate of 71%. The second survey was conducted three years later when most students were in their third and final year of study. Since it would be dif-ficult to conduct the survey in class for the same group of students, as they would be taking different courses depending on their majors, the questionnaire was posted to all students who participated in the first year study. Out of the 1009 questionnaires posted, 225 ques-tionnaires were returned undelivered (either due to students changing address, dropping out of study without official notification, or graduating). 304 respondents returned com-pleted questionnaires giving a usable response rate of 39%.

Table 2 provides the respondents’ demographics. About 47% of the respondents were international students. Most respondents (87%) were between the ages of 18 and 25. There was also about an equal balance of female (54%) and male (46%) students. A comparison between the self reported major intentions in the first year and the actual beha-viour in relation to major choice reveals that of the 68 students who intended to major in accounting in the first year, only 37 students (54%) did major in accounting. Alternatively, of the 236 students who had indicated their intention to major in non-accounting disci-plines, 24 (10%) chose to major in accounting.

Table 2 also shows when students decided on their majors. A high proportion of students selected their majors prior to commencing university study. In particular,

Table 2.Demographic characteristics of respondents

Accounting majors Non-accounting majors Total

n¼61 n¼243 n¼304

Gender

Female 41 123 164

Male 20 120 140

Nationality

New Zealander 35 125 160

International students 26 118 144

Age groupings

18220 25 104 129

21225 18 117 135

26229 8 10 18

30239 9 9 18

40249 1 3 4

Intention to major In accounting as indicated

in first year

37 31 68

In non-accounting as indicated in first year

24 212 236

When major decided

Before starting study at university 39 64 103

By end of 1st semester of 1st year study

5 33 38

By end of first year of study 12 123 135

By end of second year of study 3 19 22

Other times 2 4 6

64% of accounting majors reported that they have selected their major prior to university compared with only 26% for non-accounting majors. This may be attributed to the visibility of an accounting career in comparison with other business disciplines.

Results

The Models

To test the prediction of the TPB, a path analysis was conducted. The Chi square statistic for goodness of fit is 41.275 with three degrees of freedom and aP value of 0.001. As shown in Figure 2, both students’ intention to major in a particular discipline and per-ceived behavioural control predicted students’ choice of major (Model 1). These two factors accounted for 32% of the variance in major choice. The coefficients (b¼Beta)

for the independent variables, personal and referents, in Model 2 are positive and signifi-cantly different from zero (P,0.001). However, the perceived control variable is not significant which is inconsistent with prior results. Thus, only two of the three factors made significant contributions to the prediction of intentions to major: personal factors (P,0.01) and referents (P,0.001).3The perceived behavioural control as suggested in the TPB literature requires one to be able to make a realistic judgment of a behaviour difficulty (Davieset al., 2002).

Table 3 shows the correlation coefficients of the three constructs (the independent vari-ables) in Model 2 for all respondents. All three constructs were significantly correlated with major intention (P,0.01).

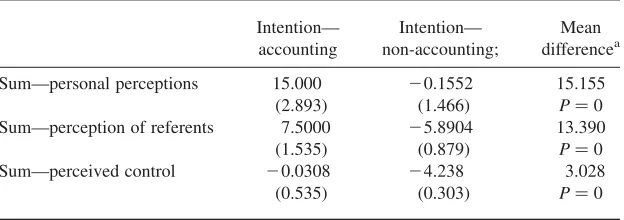

Table 4 reports the overall mean response for the constructs in Model 2 for intention to major in accounting and non-accounting disciplines. The results show that, for each construct, the mean response for accounting majors as predicted was higher than the mean response for non-accounting majors and the difference was significant (P,0.001).

Figure 2.Theory of planned behaviour.

Significant at the 5% level; Significant at the 1% level;

Significant at the 0.1% level

Accounting Versus Non- accounting Majors

In this section, we examine each construct at the beginning of first year in greater depth. This provides further insights into the specific beliefs and attitudes that discriminate between students who indicated that they intended to major in accounting, and students who indicated that they intended to major in other business disciplines.

Table 5 presents the mean differential beliefs and the motivation to comply with refer-ents for studrefer-ents who intended to major in accounting and non-accounting disciplines in their first year. Positive scores indicate normative beliefs that favour intentions to major in accounting while negative scores indicate normative beliefs that favour a business area other than accounting.

With respect to the differential normative beliefs, Table 5 (columns 1 and 2) shows that students who intended to major in accounting believed that each referent (parents, other relatives, friends, and career advisors and counsellors) thought that they should major in accounting, while students who intended to major in non-accounting disciplines believed that each referent thought that they should major in a non-accounting discipline. The t-test results indicate significant differences between the two groups’ beliefs. This result is consistent with prior findings (Cohen and Hanno, 1993; Allen, 2004; Tan and Laswad, 2006a).

Table 3.Correlations: Major intentions and constructs at first year

Model 2: Major intention¼a0þb1Personalþb2Referents1þb3Control1þ]

Differential perceived control

Differential personal perceptions

Differential perception of referents

Major intentions 0.275

0.303

0.391

Differential perceived control

0.281

0.375

Differential personal perception

0.380

Significant at 0.1% level.

Table 4.Mean (and standard error of the mean) response—major intentions and con-struct at first year

Intention— accounting

Intention— non-accounting;

Mean differencea

Sum—personal perceptions 15.000 20.1552 15.155

(2.893) (1.466) P¼0

Sum—perception of referents 7.5000 25.8904 13.390

(1.535) (0.879) P¼0

Sum—perceived control 20.0308 24.238 3.028

(0.535) (0.303) P¼0

a

Tests for differences in means are based ont-tests.

Table 5 (columns 3 and 4) shows the differences in motivation to comply with each referent. All four referents’ views were considered as being important to the students; parents’ views were ranked as most important followed by career advisors and friends. Thet-test results indicate no significant differences between the two groups’ motivation to comply with referents.

Table 6 presents the differential personal beliefs and outcome evaluations for first year students intending to major in accounting or non-accounting. A positive differential score indicates that choosing accounting is more likely to lead to the specific outcome than choosing some other business major, while the opposite is true for a negative differential belief score. As shown in Table 6, there are some significant differences between students who intended to major in accounting and students who intended to major in other business disciplines.

Although students who intended to major in accounting perceived a higher likelihood that accounting would lead to such outcomes, both groups perceived that accounting, as a major was more likely to lead to a career that deals with numbers and demands a heavy workload. This suggests that those who intended to major in non-accounting disci-plines have not chosen accounting as their intended major because they perceived account-ing as too numbers-oriented and too demandaccount-ing in terms of workload. Both groups perceived that their major would lead to a high initial salary and future earnings, provide them with a chance to establish a private practice, give broad exposure to business, and offer a challenging career and greater job opportunities. Thet-tests indicate significant differences in the two groups’ perceptions.

Interestingly, students who intended to major in non-accounting believed significantly more than those who intended to major in accounting that accounting was likely to be a boring academic major. Such perceptions might have further discouraged them from choosing accounting as their intended major. Overall, the differential outcome beliefs were similar to the results of Cohen and Hanno (1993), Allen (2004), and Tan and Laswad (2006a).

In comparing the outcome evaluation scores (columns 3 and 4) in Table 6, students who intended to major in accounting perceived a career in a field that deals with numbers, high initial salary, and entering a career that provides high social status as significantly (P,0.001) more favourable than did non-accounting majors. Students who intended to

Table 5.Mean differential perception of referents and motivations to comply at first year for students intending to major in accounting versus non-accounting

Referents

Differential perceptions Motivation to comply

Intention—

Parents 0.791 20.461

3.51 3.39

Other relatives 0.403 20.389

2.93 2.86

Friends 0.462 20.646

3.09 3.05

Career advisors and counsellors

0.296 20.452

3.31 3.24

Tests for differences in means are based ont-tests.

Significance at the 0.1% level.

1¼very unimportant to 5¼very important.

major in non- accounting viewed broad exposure to business more favourably than stu-dents who intended to major in accounting (P,0.05).

In summary, nine of the ten outcomes (see Table 6, Columns 1 and 2) for accounting majors are positive, indicating that these students believed that their intended majors were more likely to lead to the outcomes evaluated. In comparison, a business major other than accounting was perceived as more likely to lead to six of the ten outcomes by those who intended to major in non-accounting disciplines. For all ten outcomes, there were seven significant differences (P,0.01) between the two groups’ personal beliefs.

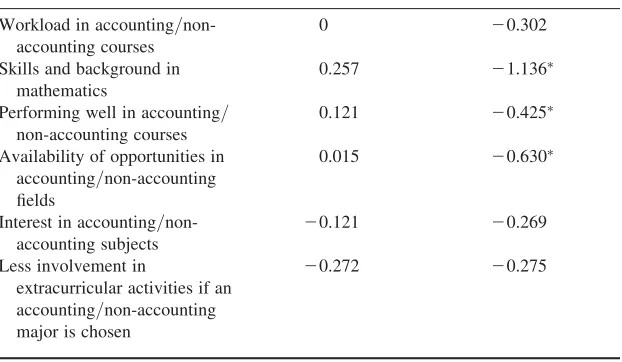

Table 7 presents the differential perceived control for those who intended to major in accounting and non-accounting in their first year. A positive differential score indicates that the factor would facilitate choosing accounting as a major. A negative differential control belief score indicates that the factor facilitated choosing a business field other than accounting. The results in Table 7 indicate that three out of the six differential control beliefs were perceived differently by the two groups.

Table 6.Mean differential personal beliefs and outcome evaluations at first year for students intend-ing to major in accountintend-ing versus non-accountintend-ing

Differential perceptions Outcome evaluations

A career that deals with numbers

A career with a chance to establish a private

An academic major that is boring

20.020 0.892

2.03 2.07

A career with high future earnings

0.458 20.000 4.42 4.33

A major that demands a heavy workload

0.333 0.215 3.09 2.96

A career that provides high social status

0.145 20.132 3.94 3.70

A major that prepares for a career with greater job opportunities

0.291 20.436

4.51 4.41

Tests for differences in means are based ont-tests.

Significant at the 5% level.

Significant at the 1% level.

Significant at the 0.1% level.

1¼very unlikely to 5¼very likely.

Skills and background in mathematics and performing well in accounting courses appeared to be significant factors in facilitating the intention to major in accounting. However, those who intended to major in non-accounting felt more strongly than those who intended to major in accounting that skills in mathematics would hinder their choice of accounting as their major. Performing well in accounting course(s) appeared to hinder their intention to major in accounting, whereas performing well in a non-accounting course appeared to facilitate their intended major. Their perceptions of the availability of opportunities in their intended major also appeared to influence their inten-tions. These results are generally consistent with the findings of Cohen and Hanno (1993) and Allen (2004).

Changes in Students’ Perceptions

Students develop their attitudes and beliefs through experience. Accordingly, their atti-tudes and beliefs may change over time as experience may validate, reinforce or modify their beliefs and attitudes.

As shown in Table 2, 37 of the 68 students who intended to major in accounting have majored in accounting by the third year and 24 of the 226 students who intended to major in non-accounting have majored in accounting by the third year. A Chi-square test indi-cates a significant difference (P¼0.001) between intention to major and actual major

choice. This suggests that attitudes and beliefs about study majors may have changed during the period from when the intentions were expressed at the beginning of university study and when the major choice was confirmed.

To examine changes in attitudes and beliefs, the respondents were divided into two main groups—the ‘No change’ group and the ‘Change’ group. The ‘No change’ group comprises two sub-groups: those who intended to major in accounting and have actually majored in

Table 7.Mean perceived differential control at first year

Intention—accounting Intention—non-accounting

Workload in accounting/ non-accounting courses

0 20.302

Skills and background in mathematics

0.257 21.136

Performing well in accounting/ non-accounting courses

0.121 20.425

Availability of opportunities in accounting/non-accounting fields

0.015 20.630

Interest in accounting/ non-accounting subjects

20.121 20.269

Less involvement in

extracurricular activities if an accounting/non-accounting major is chosen

20.272 20.275

Tests for differences in means are based ont-tests.

Significance at the 0.1% level.

1¼strongly disagree to 5¼strongly agree.

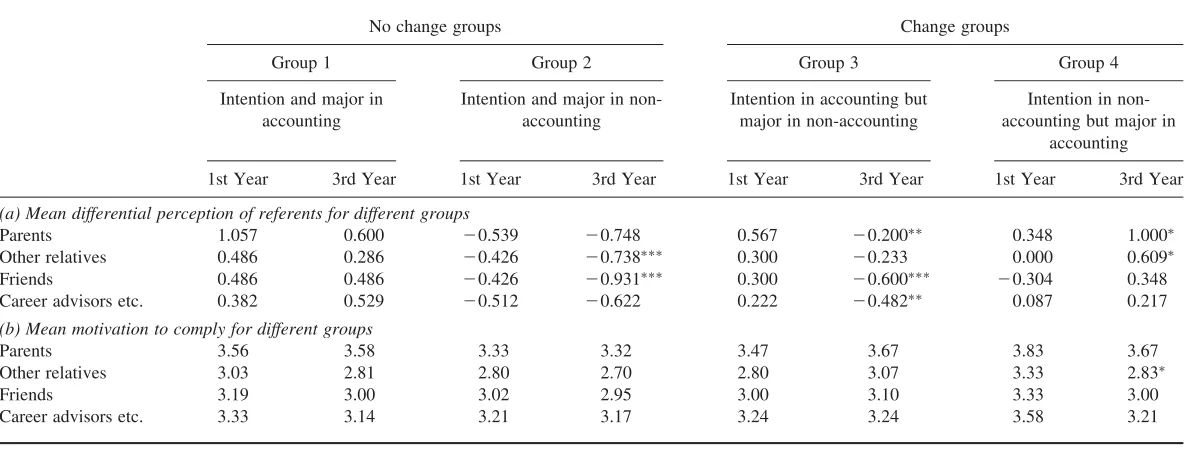

accounting (Group 1), and those who intended to major in non-accounting and actually majored in non-accounting (Group 2). The ‘Change’ group comprises two sub-groups: those who intended to major in accounting but majored in non-accounting (Group 3), and those who intended to major in non-accounting but majored in accounting (Group 4). Table 8(a) presents the mean differential perception of referents for the four groups.

There were no significant differences in Group 1’s perceptions of referents between first and third year. For Group 2, there were significant changes in perceptions of their relatives and friends’ views. In the third year as compared to the first year, this group had stronger beliefs that their relatives and friends thought they should major in non-accounting.

There was also a significant difference in Group 3’s perceptions of referents in the first and third year. In the third year, this group perceived that their referents thought they should major in non-accounting. This is in sharp contrast to their perceptions in the first year when they perceived that their parents, friends and career advisors thought they should major in accounting. Perhaps they had reassessed their perceptions after the views of their referents had changed. Group 4’s perception of referents is interesting. There is a significant difference in perceptions that relate to the parents and the relatives’ views in the first year. In the first year, even though they perceived that their parents and relatives thought they should major in accounting, their intention was to major in non-accounting. In the third year, they had stronger beliefs that their parents and relatives thought that they should major in account-ing and they ultimately did major in accountaccount-ing. This findaccount-ing suggests that these students might have been influenced by their parents and relatives in their decisions to change majors.4 Table 8(b) presents the results for the four different groups’ motivations to comply with referents. The paired samples t-test showed no significant differences in views from first year to third year for all groups except for Group 4. This group perceived their relatives’ views as being less important when they were in the third year as compared to when they were in their first year. Generally, the results indicate that the four groups’ perceptions of referents remained relatively stable.

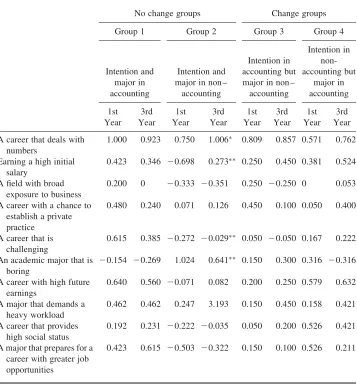

Table 9 shows the four groups’ results for differential personal beliefs in the first year and third year. There were no significant differences in beliefs for Groups 1, 3 and 4 between the first year and third year. Significant changes were found for Group 2’s percep-tions. This group appeared to have higher beliefs in the third year than in the first year that accounting dealt a lot with numbers but had lower beliefs that a non-accounting career is more challenging and that an accounting major is boring. The perceptions of Group 2 also changed with regard to a high initial salary. In their third year as compared with their first year, this group had higher perceptions that an accounting major has the potential to earn a high initial salary. However, this group did not change their intended major to accounting even though some of their beliefs had changed.

Table 10 shows the results for outcome evaluations for the four groups. Group 1, 3 and 4’s views did not change over the years. Group 2’s evaluation of ‘a field with broad exposure to business’ changed significantly. They had stronger beliefs in the third year that their non- accounting major would provide them with a broad exposure to business, as compared to their belief in first year.

Table 11 provides a comparison between control factors for the four groups. For Groups 1 and 3, there were no changes in the perceptions of control factors. Group 2’s views have changed with regard to performing well in accounting and the availability of job opportu-nities. This group’s perception of availability of opportunities in accounting was more positive from the first to the final year of study. The results further show improvement in their perception that performance in non-accounting study would facilitate selection of non-accounting as a major. The significant change in Group 4’s views is interesting.

No change groups Change groups

Group 1 Group 2 Group 3 Group 4

Intention and major in accounting

Intention and major in non-accounting

Intention in accounting but major in non-accounting

Intention in non-accounting but major in

accounting

1st Year 3rd Year 1st Year 3rd Year 1st Year 3rd Year 1st Year 3rd Year

(a) Mean differential perception of referents for different groups

Parents 1.057 0.600 20.539 20.748 0.567 20.200 0.348 1.000

Other relatives 0.486 0.286 20.426 20.738

0.300 20.233 0.000 0.609

Friends 0.486 0.486 20.426 20.931

0.300 20.600

20.304 0.348

Career advisors etc. 0.382 0.529 20.512 20.622 0.222 20.482 0.087 0.217

(b) Mean motivation to comply for different groups

Parents 3.56 3.58 3.33 3.32 3.47 3.67 3.83 3.67

Other relatives 3.03 2.81 2.80 2.70 2.80 3.07 3.33 2.83

Friends 3.19 3.00 3.02 2.95 3.00 3.10 3.33 3.00

Career advisors etc. 3.33 3.14 3.21 3.17 3.24 3.24 3.58 3.21

Tests for differences in means are based ont-tests.

Significant at the 5% level.

Significant at the 1% level.

Significant at the 0.1% level.

Understanding

Students’

Choice

of

Academic

Majors

247

They appeared to have developed some interest in accounting between their first and third year of study.

Summary and Conclusions

This study extends the literature that uses Ajzen’s (1988) theory of planned behaviour in examining the factors that impact on students’ intentions and their eventual decision to major in accounting or a non-accounting discipline. A sample of business students enrolled in an introductory accounting course participated in the study. A follow up survey was conducted at the end of their third year of university study. The results show that major intentions and perceived behavioural control were determinants of

Table 9.Mean differential personal beliefs for different groups

No change groups Change groups

Group 1 Group 2 Group 3 Group 4

Intention and

A career that deals with numbers

1.000 0.923 0.750 1.006

0.809 0.857 0.571 0.762

Earning a high initial salary

0.423 0.346 20.698 0.273 0.250 0.450 0.381 0.524

A field with broad exposure to business

0.200 0 20.333 20.351 0.250 20.250 0 0.053

A career with a chance to establish a private practice

0.480 0.240 0.071 0.126 0.450 0.100 0.050 0.400

A career that is challenging

0.615 0.385 20.272 20.029 0.050 20.050 0.167 0.222

An academic major that is boring

20.154 20.269 1.024 0.641 0.150 0.300 0.316 20.316

A career with high future earnings

0.640 0.560 20.071 0.082 0.200 0.250 0.579 0.632

A major that demands a heavy workload

0.462 0.462 0.247 3.193 0.150 0.450 0.158 0.421

A career that provides high social status

0.192 0.231 20.222 20.035 0.050 0.200 0.526 0.421

A major that prepares for a career with greater job opportunities

0.423 0.615 20.503 20.322 0.150 0.100 0.526 0.211

Tests for differences in means are based ont-tests.

Significant at the 5% level.

Significant at the 1% level.

major choices and two factors (personal and referents) were determinants of students’ major intentions.

Further analysis of these factors revealed that the students’ academic major intentions (whether accounting or non-accounting) were influenced by the perceptions of important referents, particularly their parents.

Students’ outcome evaluations showed that market-related factors (high initial salary and future earnings, and greater job opportunities) were perceived favourably by all stu-dents. This result is similar to the findings of prior studies in other countries. As indicated in Tan and Laswad’s (2006a) study, students, regardless of the country from which they originate, consider these factors in making decisions about their major intentions.

Comparison of differential personal perceptions of the two groups revealed that those who intend to major in accounting generally hold positive attitudes towards the accounting

Table 10.Mean differential outcome evaluations for different groups

No change groups Change groups

Group 1 Group 2 Group 3 Group 4

Intention and

A career that deals with numbers

3.78 3.70 3.23 3.25 3.55 3.23 3.63 3.79

Earning a high initial salary

4.46 4.32 4.19 4.10 4.55 4.19 4.46 4.54

A field with broad exposure to business

3.94 3.83 3.90 4.06

3.97 3.87 4.27 4.23

A career with a chance to establish a private practice

3.94 3.86 3.93 3.99 4.03 3.93 4.17 4.04

A career that is challenging

3.94 3.88 3.99 4.04 4.00 3.93 4.30 4.35

An academic major that is boring

1.94 2.03 2.07 1.96 2.13 2.23 1.95 1.91

A career with high future earning

4.41 4.43 4.32 4.35 4.43 4.23 4.61 4.70

A major that demands a heavy workload

3.00 2.91 2.92 2.88 3.18 3.04 3.26 3.00

A career that provides high social status

3.82 3.85 3.72 3.62 4.06 3.94 3.64 4.09

A major that prepares for a career with greater job opportunities

4.62 4.57 4.39 4.32 4.40 4.33 4.61 4.48

Tests for differences in means are based ont-tests.

Significant at the 5% level.

profession and the study of accounting. It appeared that those who intended to major in accounting were not deterred by the heavy workload, as the higher workload would perhaps be compensated for by other benefits, such as higher initial salary and the potential to establish a private practice in the future. These results suggest that the accounting pro-fession is attracting students who are favourably disposed to the traditional characteristics of the profession.

In contrast, those who intended to major in non-accounting might have been discour-aged from pursuing an accounting major due to their perception of accounting as demand-ing a heavy workload and dealdemand-ing a lot with numbers. This suggests that there are opportunities for promoting accounting study to influence non-accounting students’ beliefs about the accounting profession and the study of accounting. Taking into account the beliefs held by respondents who intend to major in disciplines other than accounting and the importance of referents, the profession should perhaps promote

Table 11.Mean perceived differential control

No change groups Change groups

Group 1 Group 2 Group 3 Group 4

Intention and

20.037 20.333 0.091 0.046

Availability of opportunities in accounting/ non-accounting fields

0.139 0.694 20.371 20.142

20.214 0.107 0.318 0.864

Interest in accounting/

Significant at the 5% level.

Significant at the 1% level.

Tests for differences in means are based ont-tests.

the positive aspects of an accounting career, not only to pre-university students but also to the public. This strategy would enhance the public profile of members of the profession. The results further indicate that there were significant differences in the control percep-tion between students who intend to major in accounting and those who intend to major in non-accounting disciplines. Mathematical skills, academic performance, and employment opportunities appeared to be the control perceptions that distinguished between those who intend to major in accounting and non-accounting.

The comparison of beliefs and attitudes between students in the first and third year of study indicates some changes of perceptions for three out of the four sub-groups. There were no significant changes in beliefs and attitudes of those who intended to major in accounting and actually majored in accounting. This group appeared to have chosen their career path at an early stage and was determined to continue with it. Although there were some significant changes in beliefs and attitudes exhibited by the second group (i.e. those who intended to major in non-accounting and majored in accordance with their intention), the changes were merely in the form of stronger or weaker beliefs; in most cases there were no changes in the directions of their beliefs and attitudes except for their perception on earning a high initial salary. Perhaps this explained why they followed through with their intended non- accounting major.

The results for the change groups are interesting. Those who intended to major in account-ing but ultimately majored in a non-accountaccount-ing major had changed perceptions of their refer-ents’ views (parents, friend, and career advisors). Either this group had modified their perceptions of the views of their referents, or their referents themselves had changed. For example, they may have had different friends between the first and last year of study. Apart from this, their other beliefs and attitudes did not change significantly over the three years. For those who intended to major in non-accounting but ultimately majored in accounting, their perception of accounting was also significantly changed. This finding suggests that the accounting profession and the accounting academics have the potential to influence students’ perceptions of accounting during their studies at university.

Overall, there were very few changes in students’ personal attitudes and perceived control between their first and third years of study. This suggests that attitudes developed early in university are generally stable and tend to last, further suggesting that attempts to influence these attitudes should be made early. Generating students’ interest in a subject area during their first year is also an important determinant as it has an impact on change of major. Stimulating students’ interest in accounting starting from their first year of study may perhaps sway them to consider accounting as their major.

Lastly, there are limitations to making generalisations of our results to the population as this study was conducted on one particular multi-campus university. Our longitudinal study permits measurement of differences in beliefs and attitudes from one period to another, but it has the disadvantage of some participant attrition. This may bias the results and affect their generalisability.

Notes

1

This literature was extensively reviewed by Tan and Laswad (2006a). 2

Introductory accounting is usually taken by students in their first year of study. For those who intend to major in accounting, the intermediate and advanced accounting courses are taken in their second and third year of study respectively.

3

Testing whether gender is an explanatory variable in models 1 and 2 indicates that gender is not a significant variable in both models.

4We did not explore the potential effects of students’ grades in the introductory accounting course on the change in majors as we have adopted the TPB as the conceptual framework for examining the factors

that influence major choices. However, using the same database, we examined this factor in another study on students’ performance. The results show that intention to major in accounting is not associated with the strength of students’ academic ability in the discipline (Tan and Laswad, 2006b).

References

Adams, S. J., Pryor, L. and Adams, S. L. (1994) Attraction and retention of high-aptitude students in accounting: an exploratory longitudinal study,Issues in Accounting Education, 9(1), pp. 45 – 58.

Ahmed, K., Alam, K. F. and Alam, M. (1997) An empirical study of factors affecting accounting students’ career choice in New Zealand,Accounting Education: an international journal, 6(4), pp. 325 – 335.

Ajzen, I. (1988)Attitudes, Personality and Behavior(Chicago: The Dorsey Press).

Ajzen, I. (2001) Nature and operation of attitudes,Annual Review of Psychology, 52(1), pp. 27 – 58.

Allen, C. L. (2004) Business students’ perception of the image of accounting,Managerial Auditing Journal, 19(2), pp. 235 – 258.

Ashworth, J. (1969) The pursuit of high quality recruits,The Journal of Accountancy, 127(2), pp. 53 – 58. Auyeung, P. and Sands, J. (1997) Factors influencing accounting students’ career choice: a cross cultural

vali-dation study,Accounting Education: an international journal, 6(1), pp. 13 – 23.

Cangelosi, J. S., Condie, F. A. and Luthy, D. H. (1985) The influence of introductory accounting courses on career choices,Delta Phi Epsilon Journal, 27(1), pp. 60 – 68.

Cherry, A. A. R. and Reckers, P. M. J. (1983) The introductory financial accounting course: its role in the curri-culum for accounting majors,Journal of Accounting Education, 1(1), pp. 71 – 82.

Cohen, J. and Hanno, D. M. (1993) An analysis of underlying constructs affecting the choice of accounting as a major,Issues in Accounting Education, 8(2), pp. 219 – 238.

Davis, L. E., Ajzen, I., Saunders, J. and Williams, T. (2002) The decision of African American students to com-plete high school: an application of the theory of planned behaviour,Journal of Educational Psychology, 94(4), pp. 810 – 819.

Fedoryshyn, M. W. and Tyson, T. N. (2003) The impact of practitioner presentations on student attitudes about accounting,Journal of Education for Business, 78(5), pp. 273 – 283.

Felton, S., Buhr, N. and Northey, M. (1994) Factors influencing the business student’s choice of a career in char-tered accountancy,Issues in Accounting Education, 9(1), pp. 131 – 141.

Fishbein, M. and Ajzen, I. (1975)Belief, Attitude, Intention and Behavior: An Introduction to Theory and Research(Reading, MA: Addison-Wesley).

Fisher, R. and Murphy, V. (1995) A pariah profession? Some student perceptions of accounting and accountancy, Studies in Higher Education, 20(1), pp. 45 – 58.

Geiger, M. A. and Ogilby, S. M. (2000) The first course in accounting: students’ perceptions and their effect on the decision to major in accounting,Journal of Accounting Education, 18(2), pp. 63 – 78.

Gul, F. A., Andrew, B. H. and Leong, S. C. (1989) Factors influencing choice of discipline of study—accoun-tancy, engineering, law and medicine,Accounting and Finance, 29(2), pp. 93 – 101.

Heaton, G. (1999) Developing customer focus in accounting education,Chartered Accountants Journal, 78(1), pp. 22 – 25.

Hermanson, D. R. and Hermanson, R. H. (1995) Are America’s top businesses students steering clear of account-ing?,Ohio CPA Journal, 54(2), pp. 26 – 30.

Horowitz, K. and Riley, T. (1990) How do students see us?,The Human Resource, 106(1165), pp. 75 – 77. Inman, B. C., Wenzler, A. and Wickert, P. D. (1989) Square pegs in round holes: are accounting students

well-suited to today’s accounting profession?,Issues in Accounting Education, 4(1), pp. 29 – 47.

Jackman, S. and Hollingworth, A. (2005) Factors influencing the career choice of accounting students: a New Zealand study,New Zealand Journal of Applied Business Research, 4(1), pp. 69 – 83.

Karnes, A., King, J. and Hahn, R. (1997) Is the accounting profession losing high potential recruits in high school by default?,Accounting Educators’ Journal, 9(2), pp. 28 – 43.

Lowe, D. R. and Simons, K. (1997) Factors influencing choice of business majors—some additional evidence: a research note,Accounting Education: an international journal, 6(1), pp. 39 – 45.

Luscombe, N. (1988) My Christmas wish-list,CA Magazine, 121(11), p. 3.

Marshall, R. (2003) Calling on tomorrow’s professionals,Chartered Accountants Journal, 82(1), pp. 4 – 9. Mauldin, S., Crain, J. L. and Mounce, P. H. (2000) The accounting principles instructor’s influence on students’

decision to major in accounting,Journal of Education for Business, 75(3), pp. 142 – 148.

Paolillo, J. G. P. and Estes, R. W. (1982) An empirical analysis of career choice factors among accountants, attor-neys, engineers and physicians,The Accounting Review, LVII(4), pp. 785 – 793.

Saemann. G. P. and Crooker, K. J. (1999) Student perceptions of the profession and its effect on decisions to major in accounting,Journal of Accounting Education, 17(1), pp. 1 – 22.

Tabachnick, B. G. and Fidell, L. S. (1996)Using Multivariate Statistics(New York: HarperCollins College Publishers).

Tan, L. M. and Laswad, F. (2006a) Students beliefs, attitudes and intentions to major in accounting,Accounting Education: an international journal, 15(2), pp. 167 – 187.

Tan, L. M. and Laswad, F. (2006b) Performance in introductory accounting and student diversity, paper presented at the British Accounting Association Annual Conference, University of Portsmouth, UK, 11 – 13 April. Wolk, C. M. and Cates, T. A. (1994) Problem-solving styles of accounting students: are expectations of

inno-vation reasonable?,Journal of Accounting Education, 12(4), pp. 269 – 281.