ACCELERATING SOUND POLICY TO

REGAIN FINANCIAL STABILITY:

THE UK APPROACH

by

Dr. Maximilian J. B. Hall

Dr. Maximilian J. B. Hall

Professor of Banking and Financial Regulation, Department of Economics,

Loughborough University

FOCUS OF PRESENTATION

The evolution of bank failure resolution policy since the

nationalisation of Northern Rock, involving a switch from

an ad hoc, piecemeal approach to a comprehensive,

system-wide approach.

BACKGROUND

Vulnerabilities of the UK Economy:

-

size of the local property bubble;

-

scale of consumer indebtedness; and

-

scale of the contribution of the “City”/financial services

sector to economic prosperity and tax revenues.

But some “silver linings”:

But some “silver linings”:

-

past fiscal rectitude had kept debt to GDP ratios at

relatively low levels (i.e. under 40 per cent), providing

some additional room for fiscal stimuli; and

-

ironically, a relatively-small manufacturing base

Weaknesses within the UK Banking System:

- widespread funding gaps (i.e. excessive reliance on wholesale funding);

- large “shadow banking” system;

- flawed executive/trader remuneration policies; - weak corporate governance; and

- reckless business strategies (e.g. quest for growth, organically or through acquisitions; expansion in proprietary trading).

expansion in proprietary trading).

Problems compounded by: - poor external oversight;

- inadequate regulatory framework (esp. with respect to failure resolution and deposit protection); and

The Main “Casualties” of the Financial Tsunami:

-

Northern Rock (nationalised in February 2008)

-

Alliance and Leicester

-

Bradford and Bingley

-

HBOS

-

HBOS

-

RBS

-

Lloyds TSB

Policy Mix Adopted for Restoring Financial

Stability

Standard IMF prescription comprising:

-

loose monetary policy (policy rates cut to 0.5 per cent

prior to introduction of “quantitative easing”);

-

loose fiscal policy (budget deficit allowed to increase

-

loose fiscal policy (budget deficit allowed to increase

substantially in short to medium term);

-

massive infusion (eventually) of emerging liquidity

- a variety of stabilisation measures (including the introduction of new legislation to allow for the nationalisation of failed

institutions and other resolution approaches, the reform of

deposit protection arrangements, the recapitalisation of sound but weak banks by the State, the brokering of takeover-rescues, government insurance of banks’ toxic assets and government guarantees of new bank debt issuance); and

- an intensification in supervision (initially under the FSA’s

“Supervisory Enhancement Programme” introduced in the wake “Supervisory Enhancement Programme” introduced in the wake of the Northern Rock affair). [Plans are also afoot to boost

banks’ liquidity buffers and revise bank capital adequacy rules by requiring bigger overall capital cushions, imposing higher

BANK ‘FAILURE’ RESOLUTION

POLICY POST-NORTHERN ROCK

Key components:

brokered takeover-rescues

brokered takeover-rescues

outright nationalisation

part-nationalisation under the October 2008 industry

bailout scheme

BROKERED TAKEOVER-RESCUES

- Table 1

Ailing UK Institutions Rescuer Need for Rescue

1. The Alliance and Leicester

Banco Santander (July 2008)

Crash in profits due to exposure to UK housing market (as a former building society); excessive exposure to wholesale funding markets; falling share price.

2. Halifax Bank of Scotland (HBOS)

Lloyds TSB

(September 2008)

Crash in profits due to exposure to UK property market (Halifax was a former Scotland (HBOS) (September 2008) property market (Halifax was a former

building society); excessive exposure to wholesale funding markets; precipitous fall in share price in wake of collapse of

Lehman Brothers.

3. Cheshire and Derbyshire Building Societies

Nationwide Building Society (planned

mergers announced in September 2008)

BROKERED TAKEOVER-RESCUES

- Table 1 (continued)

Ailing UK Institutions Rescuer Need for Rescue

4. Barnsley Building Society

Yorkshire Building Society (planned merger announced in October 2008)

To end the uncertainty associated with the Barnsley’s £10 million exposure to Icelandic banks.

5. Scarborough Skipton Building To restore regional stability in the 5. Scarborough

Building Society

Skipton Building Society (planned merger announced in November 2008)

To restore regional stability in the building society movement given Scarborough’s precarious financial situation. 6. Dunfermline Building Society Nationwide Building Society (March 2009)

Nationalisation of the Bradford and

Bingley (September 2008)

♦

Reasons for collapse:

- crash in profits due to exposure to UK property

market (another former building society), especially

with respect to buy-to-let and “self-certified”

with respect to buy-to-let and “self-certified”

mortgages;

-

downgrading of its credit rating;

-

a precipitous fall in its share price, which destabilised

its rights issue process; and

♦

Structure of the nationalisation process:

-

Government takes over the £42 billion

mortgage book, to be wound down in due

course;

-

The bank’s branches are sold to Banco

Santander for £612 million; and

-

The UK banking industry is asked to

Part-Nationalisation Under The October

2008 Bailout Scheme

•

On 8 October 2008 the UK government unveiled a

comprehensive £400 billion bailout/rescue plan for

the UK banking sector designed to restore financial

confidence, stability and credit flows to UK

businesses and individuals.

•

The plan comprised three elements:

- a massive expansion in the Bank of England’s

- a massive expansion in the Bank of England’s

provision of emergency liquidity to the market

through an increase in the amount of funding

available under the ‘Special Liquidity Scheme’ (under

which banks can swap certain asset-backed

-

up to £50 billion of taxpayers’ money being used to

recapitalise UK-incorporated banks and building

societies (and the UK bank subsidiaries of overseas

institutions with a significant presence in the UK

market); and

-

up to £250 billion worth of government funding will

-

up to £250 billion worth of government funding will

also be available to guarantee the new short and

medium-term debt issuance of those financial

Those institutions which seek government help in

recapitalising themselves will be subject to

restrictions on dividend payouts and executive

compensation, and will also be required to commit to

targets for the provision of loans to small businesses

and mortgage loans; whilst the funding guarantees,

available under the third part of the rescue plan, are

subject to the payment of a commercial fee.

subject to the payment of a commercial fee.

Under the terms of the agreement reached between

banks, the FSA and the Government and announced

on 13 October 2008, some £37 billion of public

Table 2 : Government-Funded Recapitalisation of

UK Banks in October 2008

Recipient Bank Nature of Capital Infusion Resultant Government Stake in the Bank (%)

1. RBS £15 billion in new equity; £5 billion in 5-year

preference shares paying 12 per cent per annum.

63

2. HBOS £8.5 billion in new equity; £3 billion in preference shares.

)

) 43.5* )

) 3. Lloyds TSB £4.5 billion in new equity;

£1 billion in preference shares.

On 19 January 2009 the UK Government unveiled a

comprehensive package of measures designed to support

lending in the economy and reinforce the stability of the financial system. Together with the fiscal stimulus package announced in the Pre-Budget Report of November 2008 and the provision of a 50 per cent guarantee on up to £20 billion of working capital loans to SMEs, the new measures are also designed to support

Extended Nationalisation Under the

Lending Support Package of January

2009

loans to SMEs, the new measures are also designed to support the wider economy.

The support package embraced the following elements:

- the introduction, from April 2009, of a new guarantee scheme for triple-A rated asset-backed securities – initially involving new mortgages but later to include corporate and consumer debt – designed to try and re-start the securitisation markets;

- an increase, from one month to one year, in the period for which banks can swap illiquid assets for Treasury bills under the new Discount Window Facility in order to ensure the availability of long-term bank liquidity;

- the establishment of a new “Asset Purchase Facility” under which the Bank of England can purchase up to £50 billion of “high quality” (i.e. investment grade or better) private sector “high quality” (i.e. investment grade or better) private sector assets in order to widen large corporates’ access to credit and reduce their cost of funding. [The Bank of England is

indemnified against loss by the Treasury, which issues an

equivalent amount of Treasury bills to fund the purchases. This proved a pre-cursor to the introduction of “quantitative easing”, under which the Bank of England undertook to purchase up to £150 billion of assets, comprising £100 billion of gilts and £50 billion of corporate securities, by end-June 2009, without

- the introduction of a new scheme to insure banks against extreme, unexpected losses on their existing loans and

investments – in return for a fee payable in cash or preference investments – in return for a fee payable in cash or preference shares and verifiable commitments to support lending to

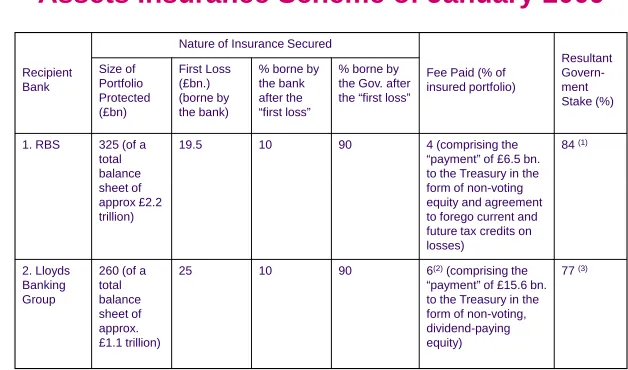

Table 3 : Implementation of the Banks’

Assets Insurance Scheme of January 2009

Recipient Bank

Nature of Insurance Secured

Fee Paid (% of insured portfolio) Resultant Govern-ment Stake (%) Size of Portfolio Protected (£bn) First Loss (£bn.) (borne by the bank)

% borne by the bank after the “first loss”

% borne by the Gov. after the “first loss”

1. RBS 325 (of a total balance sheet of

19.5 10 90 4 (comprising the “payment” of £6.5 bn. to the Treasury in the form of non-voting

84 (1)

sheet of approx £2.2 trillion)

form of non-voting equity and agreement to forego current and future tax credits on losses)

2. Lloyds Banking Group

260 (of a total balance sheet of approx. £1.1 trillion)

25 10 90 6(2)(comprising the “payment” of £15.6 bn. to the Treasury in the form of non-voting, dividend-paying equity)

Notes:

(1) This represents the Government’s economic interest in the bank following the Treasury’s conversion of its preference shares in the bank to common equity (which raised the Government’s interest to 70 per cent) and the bank’s acceptance of a £13 billion capital infusion via the issuance of non-voting, dividend-paying “B” shares to the

Treasury. This will rise to around 95 per cent if the bank exercises its option to subscribe to an additional £6 billion of such funding,

option to subscribe to an additional £6 billion of such funding,

although the State’s voting stake is likely to be capped at 75 per cent.

(2) The fee is higher than that paid by RBS (as a proportion of protected assets) because a bigger reduction in risk-weighted assets is

secured, thereby delivering a bigger boost to capital ratios.

(3) This reflects the Government’s potential economic interest in the bank following payment of the fee and conversion of the

- forcing the Government-owned Northern Rock to slow the rate of contraction in its lending activities, thereby reversing the previous policy of trying to extract the fastest possible

repayment of the bank’s loan from the Bank of England, in order to limit the contraction in housing-related loans in the UK; and

- a revision to the terms of the October 2008 bailout of RBS – the

- a revision to the terms of the October 2008 bailout of RBS – the preference shares, which pay a 12 per-cent coupon and must be redeemed before dividends can be paid to ordinary

shareholders, are to be swapped for common stock, thereby

boosting the State’s stake in the bank to 70 per cent – designed, in part, to stimulate the bank’s lending activities by up to £6

The FSA also did its bit to increase banks’ lending capacity by announcing, on the same day, that banks can, henceforth:

- treat a ‘post stress test’ 4 per cent core tier one ratio (roughly equivalent to a 6-7 per cent tier one ratio) as an “acceptable” equivalent to a 6-7 per cent tier one ratio) as an “acceptable” regulatory minimum capital requirement; and

- switch from a ‘point-in-time’ to a ‘through-the-cycle’ assessment basis – thereby averaging the probability of loan default over the economic cycle – when using internal models to generate

Policy Errors Made

The main ones comprise:

- the initial Bank of England lethargy in providing system-wide emergency liquidity support (Obsession with moral hazard? Under-estimation of the severity and durability of the crisis?);

- the slowness with which the Monetary Policy Committee - the slowness with which the Monetary Policy Committee

cut policy rates (i.e. “behind the curve” for too long). (Inadequate models? Poor judgement?);

- the Government’s promotion of the takeover-rescue of HBOS by Lloyds TSB; and

THE FUTURE

♦

OUTSTANDING ISSUES

Questions for the Bank of England:

Will it have to change its approach to ‘quantitative easing’ (e.g. Will it have to change its approach to ‘quantitative easing’ (e.g. to expand its scale and scope to drive down long-term yields, reduce the likelihood of another failed gilts auction, and reverse the emergence of a two-tier corporate bond market)?

Does it have an “exit strategy” for when circumstances dictate an unravelling of its accommodative stance?

Will it seek to prevent or “prick” asset price bubbles in the future (rather than just clearing up the mess once bubbles have

burst)?

Has its reputation been damaged by its lethargy in reacting to the global financial crisis and its slowness in getting “ahead of the curve” on the interest rate front?

Has its independence been undermined by the political pressure Has its independence been undermined by the political pressure bought to bear on the Monetary Policy Committee (inflation

targets are still being overshot, numerous letters of explanation of which have been sent to the Chancellor, despite record low policy rates) and by the introduction of quantitative easing

Questions for the Government

Is current fiscal policy sustainable? [Despite the optimistic

forecasts made in the April 2009 budget concerning economic growth, the likely scale of losses on existing financial

stabilisation measures and possible public sector “efficiency

savings”, public sector net borrowing is still expected to be £175 savings”, public sector net borrowing is still expected to be £175 bn. in 2009/10 (equivalent to 12.4 per cent of GDP), £173 bn. in 2010/11 (11.9 per cent), falling to £97 bn. (5.5 per cent) in

To date, the foreign exchange market’s reaction to these figures, which have necessitated an increase in gross gilt issuance for 2009/10 to £220 bn. compared with a figure of £146.5 bn. for 2008/09, has been relatively-sanguine, although the cost of insuring UK government debt against default in the CDS

Why did the Government risk damaging the hitherto

conservatively-run and successful Lloyds Bank and significantly reducing competition in UK banking markets by “promoting” the merger with HBOS?

merger with HBOS?

Questions for the FSA

Were its pre-Turner “failings” systemic rather than a one-off (as argued in its internal post mortem on Northern Rock)?

Questions for the Treasury

Is the Tripartite system fatally flawed?

Do the authorities’ proposals for deposit protection reform go far enough (e.g. issues concerning pre-funding, risk-related premia, etc. are largely ignored)? Is a new Deposit Protection Agency desirable?

desirable?

Should the FSA (or a new independent agency?), rather than the Bank of England, have been given operational control over the new ‘Special Resolution Regime’?

♦

THE LESSONS TO BE LEARNT

The current level of globalisation in finance and trade means there is no hiding place from financial and economic shocks, such as those deriving from the current financial tsunami (the myth of “decoupling”).

A carefully co-ordinated, global response is therefore necessary if global stability is to be restored.

While the IMF has been quite successful in securing

All parties – from bankers and traders to central bank officials, politicians, finance ministers, regulators, supervisors, investors, rating agencies, bank boards, auditors, etc., etc.) – have to

accept personal responsibility for the parts they played in

creating/exacerbating the crisis; only then can we move on to fix those areas of the system in need of remedial action.

Given the depth of the global recession and the necessary ‘deleveraging’ yet to be undertaken by banks and consumers alike, anaemic recovery at best is probably all that can be hoped for in the medium term. Avoidance of the nightmare of deflation may give way to the spectre of ‘stagflation’ as unemployment rises remorselessly and inflation returns, both because of central banks’ failure to reverse their accommodative stance