W

ebster’s Dictionarydefines skepticism as “an attitude of doubt or a disposi-tion to incredulity either in general or toward a particular object.” In the accounting profession, skepti-cism has long been recognized as a fundamental princi-ple of auditing. The first codification of auditing standards, Statement of Auditing Standards No. 1 (SAS 1), “Codification of Auditing Standards and Proce-dures,” promulgates the idea that auditors must use professional skepticism when engaged in an audit. Skepticism is defined in the auditing standards as anattitude that includes a questioning mind, a critical assessment and objective evaluation of audit evidence, and a willingness to suspend judgment about the hon-esty of client management. In 2002, the American Insti-tute of Certified Public Accountants (AICPA) issued SAS 99, “Consideration of Fraud in a Financial State-ment Audit,” which addresses skepticism and empha-sizes the auditor’s responsibility to explicitly consider the possibility of fraud on every engagement.1The rationale behind these standards is that high levels of professional skepticism (i.e., assuming a more question-ing attitude) enhance the ability to detect fraud.

Skepticism and the

Management Accountant:

Insights for Fraud

Detection

A

SURVEY EXAMINES THE LEVEL OF PROFESSIONAL SKEPTICISM AMONG MANAGEMENTACCOUNTANTS

. W

ITH INCREASED EMPHASIS BEING PLACED ON DETECTING AND PRE-VENTING FRAUD

,

COMPANIES MAY BENEFIT FROM ENHANCING THE ABILITIES OF THEIREMPLOYEES TO EXHIBIT SKEPTICISM

.

BY KI M B E R L Y F. CH A R R O N, PH. D . , C M A , A N D D . JO R D A N LO W E, PH. D .

Winter

200

8

VOL.9 NO.2

Winter

200

8

Despite auditing standards that require professional skepticism, 60% of the Securities & Exchange Com-mission (SEC) cases against auditors cite a lack of pro-fessional skepticism as the cause for action.2In response to the SEC’s concern about the quality of audits, the Public Oversight Board (POB) issued a rec-ommendation that audit firms should teach the concept of professional skepticism more effectively.3The impli-cations are that professional skepticism is a learned skill that can be enhanced with training rather than strictly an innate quality.

Lending support to the SEC’s and POB’s concerns about the skepticism among auditors, a 2004 fraud sur-vey by the Association of Certified Fraud Examiners (ACFE) revealed that only 11% of the frauds commit-ted were deteccommit-ted by external auditors.4The survey shows it is far more likely that fraud will be uncovered by employees of the organization rather than by the external auditors. While internal auditors faired signifi-cantly better, detecting 24% of fraud cases, nearly 40% were discovered through a tip. Of the tips that led to the discovery of fraud, 60% came from company employees. The importance of employees as a source of fraud detection may be understated in these findings. Another 16% of the tips came from anonymous hot-lines, which are widely used by employees. The abun-dance of tips adds credibility to the Sarbanes-Oxley Act (SOX) mandate that audit committees establish internal reporting mechanisms such as hotlines.

TY P E S O F FR AU D A N D TH E I R CO S T S

There are three general categories of fraud: asset misap-propriation, corruption, and fraudulent financial state-ments. The majority of frauds (90% of reported cases) are in asset misappropriations, which involve the theft or misuse of an organization’s assets, such as skimming, stealing inventory, and payroll fraud. Fraudulent finan-cial statements make up the smallest percentage of reported fraud cases (7.9%), but they represent the highest median losses per case ($1,000,000) and are more likely to be publicized.5

The cost of fraud to an organization is staggering. The ACFE 2004 survey shows that the typical U.S. organization loses 6% of its annual revenue to fraud. Applying this statistic to the U.S. Gross Domestic

Prod-uct for 2003 translates to approximately $660 billion in total losses, up from $400 billion in 1996 and $600 bil-lion in 2002. Furthermore, once an organization has been defrauded, it is unlikely to recover its losses. The survey shows that victim organizations recover an aver-age of 20% of the original loss, and 40% of the compa-nies recover nothing at all. Small organizations

represent the greatest proportion of reported fraud cases (nearly 46%), but the cost per incident of fraud is often higher in large organizations. While the true cost of fraud to any single organization is hard to measure, the magnitude and prevalence of fraud in our society should put all organizations on alert.

MA N A G E M E N T AC C O U N TA N T S A N D

FR AU D DE T E C T I O N

Preventing fraud is a big responsibility for all levels of financial management from staff accountant to CFO. As financial professionals, the accounting staff is often responsible for establishing cost-effective controls to prevent fraudulent behavior. It is unlikely that all frauds will be prevented with even the best internal controls. Therefore, every organization should have the goal of detecting fraud early in order to minimize its financial impact.

Manage-ment accountants would thus be in a better position to recognize some of these behavioral signs than an out-sider who has limited contact.

Because professional skepticism is the standard of behavior for fraud detection, it may be beneficial to understand how well management accountants utilize professional skepticism. The purpose of this study is to measure the professional skepticism of management accountants and compare it to the skepticism levels of internal and external auditors. This is the first study that we are aware of that has objectively measured the skep-ticism levels of management accountants. By having a better understanding of professional skepticism, the management accounting profession can develop guide-lines to implement it more effectively. We also look at different demographic characteristics that may correlate with higher levels of professional skepticism. Finally, we draw from the literature to provide suggestions on how organizations can increase the skeptical behaviors of those who may be inherently less skeptical.

ME A S U R I N G SK E P T I C I S M

The concept of skepticism has been discussed by philosophers throughout time. Despite all the concern with skepticism in the accounting profession, however, there is no universal way of measuring the construct. Accounting literature defines skepticism in a variety of ways. For example, Jeffrey J. McMillan and Richard A. White suggest that an auditor that uses an error-based explanation of questionable evidences (as opposed to naturally occurring) is more skeptical.7Skepticism has also been defined by the outcomes it manifests: con-fronting a client or performing extra work.8Other stud-ies support the contention that skeptical behaviors can be induced. Researchers found that auditors who were told to stress professional skepticism were more apt to increase their audit hours and perform a higher-quality audit than those encouraged to be efficient or objective.9 The inconsistent measurement of skepticism has cer-tainly hampered research efforts and the accounting pro-fession’s ability to apply findings to practice.

HU R T T SK E P T I C I S M SC A L E

Kathy Hurtt developed a skepticism scale to explicitly measure an individual’s level of skepticism, providing a

comprehensive measure of this construct.10Hurtt’s skepticism scale draws from philosophy as well as research in accounting and other disciplines. Her scale is based on characteristics and behaviors that historically have been associated with skepticism. It presumes pro-fessional skepticism is a multidimensional construct composed of six individual characteristics falling within three general categories: examining evidence, under-standing evidence providers, and acting on evidence.

Examining Evidence

Hurtt’s scale is drawn from the theoretical development of skepticism found in “Professional Skepticism: A Model with Implications for Research, Practice, and Education,” written by Hurtt, Martha Eining, and David Plumlee (HEP).11HEP argue that the three characteristics of skepticism that deal with examining evidence are a questioning mind, suspension of judg-ment, and a search for knowledge. A questioning mind means skeptics are unlikely to accept information at face value; instead, they require proof or justification. Skeptics can see the other side of arguments and often enjoy the role of “devil’s advocate.” It has also been argued that skeptics suspend judgments in order to make additional inquiry and obtain evidence. Suspen-sion of judgment means skeptics are slower to form judgments and not likely to jump to conclusions. Final-ly, a search for knowledge is equivalent to being gener-ally curious. Skeptics are individuals who enjoy the learning process and seek knowledge for knowledge’s sake.

Understanding Evidence Providers

The truth may be that they simply see things different-ly. A skeptic understands the other point of view and can investigate accordingly.

Acting on Evidence

The last portion of the skepticism scale focuses on per-sonal initiative to act on information. HEP define the characteristics in this section as self-confidence and determination. By exhibiting higher levels of self-confidence, a skeptic is more likely to take the initiative to act on the information he or she finds questionable.

With high levels of self-determination, a skeptic likely will continue to collect information until satisfied that there is sufficient information. Self-confidence and self-determination make the skeptic better able to value his or her personal insights and have the courage to chal-lenge the positions of others.

Hurtt’s scale, which uses these characteristics as the basis to measure professional skepticism, consists of a series of 30 questions designed to elicit respondents’ self-assessment of their skepticism characteristics (see Figure 1). The scale has been exhaustively pilot tested

Examining Evidence

◆ Questioning Mind (0.638)*

●

● I often reject statements unless I have proof that they are true

●

● My friends tell me that I often question things that I see or hear

●

● I frequently question things that I see or hear

◆ Suspension of Judgment (0.832)

●

● I wait to decide on issues until I can get more information

●

● I take my time when making decisions

●

● I dislike having to make decisions quickly

●

● I don’t like to decide until I’ve looked at all of the available information

●

● I like to ensure that I’ve considered most available information before making a decision

◆ Search for Knowledge (0.958)

●

● The prospect of learning excites me

●

● Discovering new information is fun

●

● I think that learning is exciting

●

● I like searching for knowledge

●

● I enjoy trying to determine if what I read or hear is true

●

● I relish learning

Understanding Evidence Providers

◆ Interpersonal Understanding (0.883)

●

● I am interested in what causes people to behave the way that they do

●

● Other people’s behavior doesn’t interest me*

●

● I like to understand the reason for other people’s behavior

●

● I seldom consider why people behaving in a cer-tain way*

●

● The actions people take and the reason for those actions are fascinating

Acting on Evidence

◆ Self-confidence (0.933)

●

● I feel good about myself

●

● I am confident of my abilities

●

● I am self-assured

●

● I don’t feel sure of myself*

●

● I have confidence in myself

◆ Self-determination (0.779)

●

● I often accept other people’s explanations without further thought*

●

● I tend to immediately accept what other people tell me*

●

● I usually accept things I see, read, or hear at face value*

●

● I usually notice inconsistencies in explanations

●

● Most often I agree with what the others in my group think*

●

● It is easy for other people to convince me*

* These questions were reverse coded.

and refined to arrive at its final state. It was also tested and retested several weeks later to provide validation for intrasubject test-retest reliability. Researchers using the Hurtt scale have provided consistent evidence of its robustness across internal auditors, external auditors, and accounting students. The use of the skepticism scale also has been validated in studies that link the level of skepticism with expected behaviors associated with skepticism. In this study, we focus our attention on the professional skepticism levels among management accountants.

TH E ST U DY

The Hurtt Skepticism Scale was administered to 59 members of the Institute of Management Accountants (IMA®) in the southwestern United States. Participants were directed to the survey website through a link on their chapter website. The questionnaire was complet-ed entirely online. This allowcomplet-ed respondents to main-tain anonymity and enabled them to take the survey at their convenience, ensuring they had adequate time to respond to the questions.

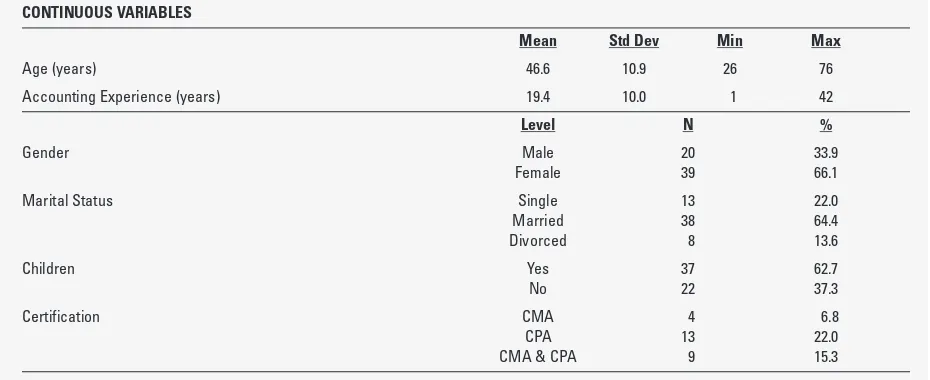

Management accountants who participated in this study held a wide variety of positions ranging from staff accountant to CEO, with the majority in the controller position (34%). Sixty-six percent of the respondents

were women. Respondents had an average of 19.4 years of experience and an average age of 46.6. Twenty six of the respondents were certified as a Certified Manage-ment Accountant (CMA®), Certified Public Accountant (CPA), or both. Other demographic details can be seen in Table 1.

RE S U LT S

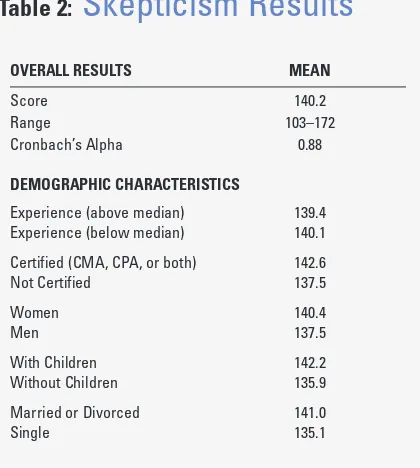

Respondents answered the 30 skepticism scale ques-tions shown in Figure 1 in random order using a six-point scale where one was “strongly disagree” and six was “strongly agree.” The eight questions that are reverse coded are adjusted accordingly. Factor analysis was run on the 30 questions, and the individual loading factors did not exactly correspond with the pre-identified constructs that Hurtt defined. But Hurtt indicates that the focus of the professional skepticism model should be on the measure as a whole and that the subscales are not necessarily designed to be used independently. As such, the responses are then summed to generate an overall skepticism score that ranges from 30 (low skepticism) to 180 (high skepti-cism). In assessing the inter-item reliability of the 30-question scale, our analysis provides a Cronbach’s alpha score of 0.88. This indicates a high inter-item reliability for the scale as a whole. In addition, Cronbach’s alpha is

Table 1:

Demographic Profile of Respondents

CONTINUOUS VARIABLESMean Std Dev Min Max Age (years) 46.6 10.9 26 76 Accounting Experience (years) 19.4 10.0 1 42 Level N % Gender Male 20 33.9

greater than 0.70 for five of the six constructs, with two constructs having scores greater than 0.90. These results are similar to the results found for samples of internal and external auditors, suggesting the scale is consistent and reliable for use across the accounting profession.

Overall, the skepticism score for management accoun-tants is 140.2, ranging from a low of 103 to a high of 172. This score is significantly higher than that of business students (132.7).12The score is very similar to the aggre-gate score of internal auditors (140.3) and slightly above the scores of external auditors (138.7) from other studies. This suggests that the skepticism of management accountants is similar to that of auditors—whether inter-nal or exterinter-nal. Moreover, this study shows that while others may conjecture that external and/or internal audi-tors have greater skepticism skills in detecting fraud or questioning red flags, this clearly is not the case.

We also examined demographic characteristics to determine whether they have any relationship (correla-tion) with levels of skepticism (see Table 2). For exam-ple, other researchers have found that, as a result of having little exposure to fraud over time, auditors tend to become less skeptical as they advance in their careers.13The results of our study find no relation between experience and skepticism. The respondents above and below the median experience levels had

sim-ilar skepticism scores (simsim-ilar results were also found for age). One interesting result, however, it that respon-dents with a CMA, CPA, or both have higher skepti-cism scores than those without certification. This result is consistent with the study of internal auditors by Cindy Durtschi and Rosemary Fullerton.14We also found that women scored higher than men, and respon-dents with children scored higher than those without children. Single, unmarried individuals scored lower than married or divorced respondents. While there is no preconceived expectation that gender, children, or mari-tal status would impact skepticism, these results indi-cate that life situations can alter the degree of skepticism within individuals. Future research should examine the relationship between demographic charac-teristics and skepticism to provide additional insights.

IM P L I C AT I O N S

The level of professional skepticism displayed by employees likely will vary. Yet these differences do not imply that employees who are less skeptical do not have the potential to improve their abilities. While researchers have found that higher levels of skepticism are associated with individuals questioning data and col-lecting more evidence to support decisions, individuals who score low on the skepticism scale can be trained to exhibit behaviors consistent with those who score higher.15

Understanding the differences in skepticism levels can help firms in developing their training strategy. Staff members who are less skeptical may need addi-tional training at regular intervals to reinforce the types of skills needed to detect fraud. Ongoing fraud training may help employees identify risk factors and help them become more sensitive to clues and red flags that sug-gest fraudulent behavior. Research shows that even novices who receive practice and feedback with fraud detection exhibit higher levels of skepticism and are better able to detect fraud when it exists.16

Unlike auditors, who have a responsibility to explicit-ly consider fraud in every engagement, management accountants have no similar requirement. It is important to note, however, that increasing fraud awareness can facilitate fraud detection. Accountants can be made aware of fraudulent activities that are discovered within

Table 2:

Skepticism Results

OVERALL RESULTS MEAN Score 140.2 Range 103–172 Cronbach’s Alpha 0.88 DEMOGRAPHIC CHARACTERISTICSthe firm or in other firms through newsletters or other forms of communication. Providing all employees with the common signs of individuals who commit fraud can help them identify potential fraud activities. Even sub-tle reminders at staff meetings or company-wide events that emphasize the importance of having a skeptical attitude may help deter fraud.

Another fraud prevention and detection strategy organizations may want to consider is encouraging their finance and accounting employees to earn a certifica-tion. Accountants who study for certification expand their knowledge base, which in turn may make them more cognizant of irregularities when they encounter them and increase their levels of skepticism. Certifica-tion may also increase self-confidence, giving these individuals more courage to question situations, transac-tions, or the behavior of colleagues.

In conclusion, research on professional skepticism has been a difficult construct to administer and mea-sure. With the Hurtt Skepticism Scale, however, an objective measure of skepticism can be obtained. This study is the first to examine the skepticism levels of management accountants. While it offers some initial findings and conclusions, future research should expand on these results. For example, research should examine whether management accountants who are identified as being highly skeptical would also rate high in certain behaviors such as information search, contradiction detection, alternative generation, and expanded scruti-ny of interpersonal information. That is, does a higher level of skepticism among management accountants lead to increased fraud detection? Are management accountants who are more skeptical also more likely to work slower than their counterparts? Finally, which teaching and training methods have the most potential for instilling an understanding of and ability to exhibit appropriate levels of skepticism? ■

Data used in this study is available from the authors upon request.

We wish to thank the Institute of Management Accountants for their cooperation in obtaining participants for this research study.

Kimberly F. Charron, Ph.D., CMA, is an associate professor at the University of Nevada, Las Vegas. You can contact her at (702) 895-3975 or [email protected].

D. Jordan Lowe, Ph.D., is a professor at the School of Global Management and Leadership at Arizona State Uni-versity. You can contact him at [email protected].

EN D N O T E S

1 American Institute of Certified Public Accountants (AICPA), SAS No. 99, “Consideration of Fraud in a Financial Statement Audit,” AICPA, New York, N.Y., 2002.

2 Mark S. Beasley, Joseph V. Carcello, and Dana R. Hermanson, “Top 10 audit deficiencies,” Journal of Accountancy, April 2001, pp. 63-66.

3 The Panel on Audit Effectiveness, Report and Recommendations, Public Oversight Board (POB), Stamford, Conn., August 31, 2000.

4 Association of Certified Fraud Examiners (ACFE), 2004 Report to the Nation on Occupational Fraud and Abuse, ACFE, 2004. 5 Ibid.

6 W. Steve Albrecht, Gerald W. Wernz, and Timothy L. Williams, Fraud: Bringing Light to the Dark Side of Business, McGraw Hill, New York, N.Y., 1995.

7 Jeffrey J. McMillan and Richard A. White, “Auditors’ Belief Revisions and Evidence Search: The Effect of Hypothesis Frame, Confirmation, and Professional Skepticism,” The Accounting Review, July 1993, pp. 443-465.

8 Michael K. Shaub and Janice E. Lawrence, “Ethics, Experi-ence and Professional Skepticism: A Situational Analysis,”

Behavioral Research in Accounting, Volume 8 Supplement, 1996, pp. 124-157.

9 Audrey A. Gramling, “External Auditors’ Reliance on Work Performed by Internal Auditors: The Influence of Fee Pres-sure on this Reliance Decision,” Auditing: A Journal of Practice and Theory, Supplement 18, 1999, pp. 117-135.

10 Kathy Hurtt, “Development of an Instrument to Measure Pro-fessional Skepticism,” University of Wisconsin, working paper, 2003.

11 Kathy Hurtt, Martha Eining, and David Plumlee, “Profession-al Skepticism: A Model with Implications for Research, Prac-tice, and Education,” University of Wisconsin, working paper, 2003.

12 Hurtt, “Development of an Instrument to Measure Profession-al Skepticism,” 2003.

13 Michael K. Shaub and Janice E. Lawrence, “Differences in Auditors’ Professional Skepticism across Career Levels in the Firm,” Advances in Accounting Behavioral Research, September 1999, pp. 61-83.

14 Cindy Durtschi and Rosemary Fullerton, “The Effects of Pro-fessional Skepticism on the Fraud Detection Skills of Internal Auditors,” Utah State University, working paper, 2006. 15 Cindy Durtschi and Rosemary Fullerton, “Teaching Fraud

Detection Skills: A Problem-Based Learning Approach,”

Journal of Forensic Accounting, June 2005, pp. 187-212. 16 Tina Carpenter, Cindy Durtschi, and Lisa M. Gaynor, “The