Banking Booklet

2009

FOREWORD

The Indonesian Banking Booklet 2009 edition is designed to present key highlights on the banking system in Indonesia. From this booklet, it is expected that readers will obtain information on the banking system particularly in regard to banking regulation issued by Bank Indonesia until March 2009.

The subject presented in this booklet covers several aspects on developments in the banking system in concise form such as key points or highlights.

Should the readers require explanations and clarifications of banking regulations in depth may refer to the full text of the regulations issued by Bank Indonesia which is available on the Bank Indonesia website (www.bi.go.id).

While the information contained in the Indonesian Banking Booklet will inevitably have its limitations, we hope that it still will prove greatly useful to readers.

Jakarta, March 2009 BANK INDONESIA

C O N T E N T S

FOREWORD i

CONTENT ii

I BANK INDONESIA 1

A. Vision and Mission of Bank Indonesia 1 B. Shared Values of Bank Indonesia 1 C. Bank Indonesia»s Destination Statement 2013 1 D. Legal Basis of Bank Indonesia 1 E. Important Duties of Bank Indonesia 2 F. Detailed Description of Duties 2 G. Organization of Bank Indonesia 2

II OPERATION OF THE BANKING SYSTEM 5

A. Definition 5

B. Legal Basis of the Banking System 5

C. Operations of Banks 6

Conventional Commercial Banks 6

Sharia Commercial Banks 7

Conventional Rural Banks 10

Sharia Rural Banks 10

D. Operations Not Permitted for Banks 11

Conventional Commercial Banks 11

Sharia Commercial Banks 11

Conventional Rural Banks 11

Sharia Rural Banks 11

III BANK REGULATION AND SUPERVISION 12

A. Objectives of Banking Regulation and Supervision 12 B. Scope of Bank Regulation and Supervision 13

C. Bank Supervision 14

D. Banking Information System 16

IV BANKING POLICIES 24 A. Indonesian Banking Architecture (API) 24 B. Building The Indonesian Financial System Architecture 31 C. Adoption of the Basel II Accord 35 D. Development of Sharia Banking 41 E. The role and contribution of Rural Bank as Community

bank in the framework of Services to UMK 47 F. Promotion of Small, Medium, and Micro-Enterprises

(SMEs) 54

G. Development of Credit Bureau 60

V KEY BANKING REGULATIONS 66

A. Establishment of Banks and Bank Offices 66

1. Establishment of Banks 66

2. Bank Owners 68

3. Single Presence Policy In Indonesian Banks 69

4. Management of Banks 71

5. Sharia Supervisory Board 77

6. Sharia Banking Committee 78

7. Employing Foreign Worker and Transfer of

Technology Program in Banking Sector 79 8. Fit and Proper Test for Commercial Banks and

Rural Banks 80

9. Purchase of Shares in Commercial Banks 83 10. Merger, Consolidation, and Acquisition of Bank 84 11. Establishment of Bank Offices 85 12. Conversion of Bank Name and Logo 87 13. Conversion of Conventional Commercial Bank/

rural Bank Operations to Commercial Ban/rural Bank Based on Sharia Principles 87 14. Closure of Bank Branch Office 88 15. Upgrading of Non-Foreign Exchange Bank to

Foreign Exchange Status 88

16. License Modification from Commercial Bank to Rural Bank in the framework of Consolidation 88 17. Supervisory Actions and Designation of

18. Follow Up Action to Rural Bank under Special

Surveillance 91

19. Bank Liquidation 93

20. Revocation of Business License at the request

ofΩ Shareholders (Self Liquidation) 94 B. Regulations Pertaining to Business Operations

and Bank Product 95

1. Money Changer»s License for Bank 95

2. Derivative Transactions 95

3. Commercial Paper (CP) 96

4. Deposits 96

5. Product of Sharia Bank and Sharia Business Unit

(UUS) 98

6. The Implementaion of Sharia Principles in Mobilizing Fund and Fund Disbursement Activity as well as Sharia Bank Services 99

C. Prudential Regulations 100

1. Minimum Tier One Capital For Commercial Banks 100 2. The Minimum Capital Requirement 101

3. Net Open Position (NOP) 103

4. Legal Lending Limit (LLL) 104

5. Earning Assets Quality 105

6. Provision for Assets Losses 107

7. Debt Restructuring 111

8. Financing restructuring for Sharia Bank dan

Sharia Business Unit (UUS) 111

9. Statutory Reserves 112

10. The Implementation of Know Your Customer

(KYC) Principles 113

11. Transparency of Financial Condition of Bank 114 12. Transparency in Bank Product Information and

Use of Customer Personal Data 116 13. Prudential Principles in Equity Participation by

Commercial Banks 116

14. Prudential Principles in Asset Securitization for

D. Rating System 118

Commercial Banks 118

Sharia Commercial Bank 120

Rural Bank 121

E. Self-Regulatory Banking (SRB) Regulations 123 1. Guidelines for Formulation of Bank Credit Policy 123 2. Implementation of Good Corporate Governance

(CGC) For Commercial Banks 123 3. Internal Audit Unit at Commercial Banks 124

4. Compliance Director 125

5. Business Plan and Annual Budget 125 6. Application of Risk Management in the Use of

Information Technology by Commercial Banks 127 7. Application of Risk Management for Commercial

Banks 128

8. Consolidated Application of Risk Management 129 9. Application of Risk Management In Internet

Banking 130

10. Application of Risk Management for Bank

assurance 130

11. Application of Risk Management for Banks

Conducting Activities Related to Mutual Funds 131 12. Risk Management Certification For Management

and officer of Commercial Banks 132

F. Financing Regulations 133

1. Short Term Funding Facility (FPJP) for Commercial

Banks 133

2. Short Term Funding Facility (FPJP) for Rural Banks 134 3. Short Term Financing Facility for Sharia Banks

(FPJPS) 135

4. Intraday Liquidity Facility (FLI) 135 5. Intraday Liquidity Facility of Sharia Banks (FLIS) 136 6. The Emergency Financing Facility (FPD) for

Commercial Banks 136

G. Other Regulations 137

2. Bank Foreign Borrowings (PLN) 137 3. Interbank Money Market Based on Sharia

Principles (PUAS) 137

4. Certifying Institution for Rural Bank / Sharia

Rural Banks 138

5. Restrictions on Rupiah Transactions and Foreign

Currency Loans By Banks 138

6. National Clearing System 140

7. Real Time Gross Settlement (RTGS) 141 8. Bank Indonesia Certificates (SBI) 141 9. Bank Indonesia Certificates on Sharia Prinsiples

(SBIS) 142

10. Government Securities (SUN) 142

11. Bank Secrecy 142

12. Human Resources Development at Banks 143 13. Resolution of Customer Complaints 144

14. Banking Mediation 144

15 Incentives in The Framework of Bank

Consolidation 145

16. Special Treatment on Bank Credit for Certain

Areas In Indonesia Hit by Natural Disaster 146 17. Debtor Information System (SID) 147

H. Reporting by Banks 148

VI OTHER 150

A Deposit Insurance Agency 150

B Money Laundering 151

C Principles for Sharia Banking Operation 153

I. BANK INDONESIA

ank Indonesia is the Central Bank of the Republic of Indonesia. Bank Indonesia is an independent state institution, which is free from intervention of the government and or other parties, except for matters explicitly prescribed in Act concerning Bank Indonesia.

A. Vision and Mission 1. Vision

To be a Central Bank established as institution of trust with national and international credibility through reinforcing of its strategic values and achievement of stable, low inflation.

2. Mission

To achieve and maintain stability in the Rupiah through management of monetary stability and development of financial system stability in support of long-term, sustainable national development.

B. Strategic Values

Competency, integrity, transparency, accountability, cohesiveness

C. Bank Indonesia»s Destination Statement 2013 Following the reinforcement of institution integrity, enhancement of strategic partnership and optimization of performance through effective and efficient policy, Bank Indonesia would like to be a more beneficial institution for the public.

D. Legal Basis of Bank Indonesia

1. 1945 Constitution of the Republic of Indonesia 2. Act of the Republic of Indonesia Number 23 of 1999

concerning Bank Indonesia as amended by Act of the Republic of Indonesia Number 3 of 2004

E. Important Duties of Bank Indonesia

1. Establishment and implementation of monetary policy; 2. Regulation and ensuring the smooth operation of the

payments system;

3. Regulation and supervision of banks.

F. Detailed Description of Duties

1. Establish monetary targets, taking into account inflation targeting, conduct monetary control, extend credit or financing based on Sharia Principles to overcome short-term financial problem of banks (mismatch), provide Government-funded emergency financing in the event of a bank experiencing financial difficulties with systemic impact that may potentially set off a crisis endangering the financial system, implement exchange rate policy, and manage foreign exchange reserves

2. Determine the use of payment instruments, regulate the inter-bank clearing system, arrange the final settlement of inter-bank payment transaction, issue and circulate the Rupiah currency as well as to revoke, withdraw and destroy such currency from circulation.

3. Grant and revoke licenses of an institutional and certain business. Prescribe regulations, activities of a bank, conduct banking supervision and impose sanctions on banks in accordance with prevailing regulations.

G. Organization of Bank Indonesia

a. examination of the BI annual financial statement; b. examination of the operating and investment budget of

BI;

c. examination of the decision making procedures for operations outside monetary policy and the management of BI assets.

Indonesian Banking Booklet 2009 BANK INDONESIA ORGANIZATION STRUCTURE

BOARD OF GOVERNORS

Regional Offices (41 Offices)

Representative Offices (4 Offices) Head Office

Monetary

(5 Directorate) (8 Directorate)Banking Payment System(2 Directorate)

II. OPERATION OF THE BANKING SYSTEM

In this booklet, banking is defined as all that pertains to banks, including of banking entities and bank offices, scope of banking business, and methods and processes employed in the conduct of banking business.

The key principle for business operations conducted by the Indonesian banking system is economic democracy applied with the use of prudential principles The primary function of the banking system in Indonesia is to mobilize and disburse funds belonging to the public and to support national development to bring about improved equitable distribution, economic growth, and national stability aimed at improving the welfare of the population at large.

The banking system has a strategic role in supporting the smooth operation of the payment system, implementing monetary policy, and achieving financial system stability. To achieve these aims, it is essential to have a sound, transparent, and accountable banking system.

A. Definition

1. Bank is a business entity that mobilizes deposit funds from the public and channels these funds to the public in credit and/or other forms in order to improve the living standards of the population at large

2. Conventional Bank is a bank conducting conventional business and based on its types consists of Commercial Conventional Bank and Rural Bank.

3. Islamic Bank is bank conducting business based on Sharia Principles and according to its types consists of Islamic Commercial Bank and Islamic Rural Bank.

4. Sharia Principles are principles based on Islamic law in banking activities which are in accordance with fatwa published by institution authorized in defining fatwa in compliance with Sharia Principles.Ω

B. Legal Basis of the Banking System

concerning Banking as amended by Act of the Republic of Indonesia Number 10 of 1998.

2. Act of the Republic of Indonesia Number 23 of 1999 concerning Bank Indonesia as amended by Act of the Republic of Indonesia Number 3 of 2004

C. Operations of Banks

Operations of Commercial Banks

1. Mobilizing funds from the public in the form of deposits comprising demand deposits, time deposits, certificates of deposit, savings deposits, and/or other equivalent form;

2. Extending credit; 3. Issuing notes;

4. Purchasing, selling, or guaranteeing against own risk or on behalf of and/or at the request of a customer :

Bills of exchange, including banker»s acceptances of which the maturity is no longer than the common practice of trading such documents;

Notes and other commercial paper of which the maturity is no longer that the common practice of trading such documents;

Treasury bills and government guarantees; Bank Indonesia Certificates (SBIs); Bonds;

Commercial paper with a maturity of up to 1 (one) year;

Other securities with a maturity of up to 1 (one) year; 5. Transferring money, either on own behalf or at the

request of a customer;

6. Placing funds in, borrowing funds from, or lending funds to other banks, whether by letter, telecommunications device, or by sight draft, cheques, or other means; 7. Accepting payments in respect or claims for securities,

settling accounts with or among third parties;

9. Undertaking custodial activities on behalf of another party based on contracts;

10. Undertaking placement of funds among customers in the form of securities not listed in the stock exchange; 11. Conducting business in factoring, credit cards, and

trusteeship;

12. Providing financing and/or conducting other activities based on Sharia Principles in accordance with the regulations stipulated by Bank Indonesia;

13. Conducting other business commonly undertaken by banks providing that such activities shall not be in contravention of Act concerning Banking and prevailing laws;

14. Conducting activities in foreign currencies with due observance to the regulation of Bank Indonesia; 15. Conducting equity participation in other banks or

business entities operating in financial services, such as leasing, venture capital, securities houses, insurance, and securities clearing house and custodian, with due observance of the regulation stipulated by Bank Indonesia;

16. Conducting temporary equity participation to settle problem of bad debt or bad financing based on Sharia Principles, on the condition that in due time the equity participation shall be withdrawn, with due observance to the regulation stipulated by Bank Indonesia; and 17. Acting as founder and the management of a pension

fund in accordance with the prevailing laws on pension funds.

Operations of Sharia Commercial Banks

1. Mobilizing fund in the form of saving comprising demand deposit, saving deposit or other equivalent form based on wadi»ah agreement or other agreement not in contravention with Sharia principles;Ω

based on mudharabah agreement or other agreement not in contravention with Sharia principles;Ω

3. Disbursing profit sharing financing based on mudharabah agreement, musyarakah agreement or other agreement not in contravention with Sharia principles;Ω

4. Disbursing financing based on murabahah agreemnet, salam agreement, istishna» agreement, or other agreement not in contravention with Sharia principles;Ω 5. Disbursing financing based on qardh agreement or other agreement not in contravention with Sharia principles;Ω

6. Disbursing financing of rental of moving object or non moving object to customer based on ijarah agreement and/or leasing in the form of ijarah muntahiya bittamlik or other agreement which is not in contravention with Sharia principles;Ω

7. Taking over of receivables based on hawalah agreement or other agreement which is not in contravention with Sharia principles;Ω

8. Conducting business on debit and/or financing cards based on Sharia principles;Ω

9. Purchasing, selling or guaranteeing at own risk third party securities issued based on underlying transaction and based on Sharia principles, such as, ijarah, musyarakah, mudharabah, murabahah, kafal or hawalah agreements;Ω 10. Purchasing securities based on Sharia principles published

by the government and/or Bank Indonesia;Ω

11. Accepting payment of liabilites on securities and negotiating with a third party or among third parties based on Sharia principles;Ω

12. Undertaking custodial activities for the interest of other party pertaining to an agreement based on Sharia principles;Ω

14. Transferring money, either on own behalf or at customer»s interest based on Sharia principles;Ω

15. Conducting trusteeship operation based on wakalah agreement;Ω

16. Providing letter of credit or bank guarantee based on Sharia principles; andΩ

17. Conducting other activities normally undertaken in the field of banking and social insofar as not in contravention with Sharia principles and in accordance with provisions of the applicable laws and regulations;Ω

18. Conducting activities in foreign currency based on Sharia principles;Ω

19. Conducting investment activity in Islamic Commercial Bank or financial institution conducting business based on Sharia principles;Ω

20. Conducting temporary equity participation due to bad financing based on Sharia principles subject to requirement of subsequent withdrawal from equity participation;Ω

21. Acting as the founder and the manager of pension fund based on Sharia principles;Ω

22. Conducting activity in capital market insofar as not in contravention with Sharia principles and provisions of applicable laws and regulations in the field of capital market;Ω

23. Organizing activity or banking products based on Sharia principles using electronic facilities;Ω

24. Publishing, offering and trading short term securities based on Sharia principles, directly or indirectly through money market;Ω

25. Publishing, offering and trading longterm securities based on Sharia principles, directly or indirectly through capital market;Ω

Operations of Conventional Rural Banks

1. Mobilizing funds from the public in the form of deposits comprising time deposits, savings deposits, and/or other equivalent form;

2. Extending credit;

3. Placing funds in Bank Indonesia Certificates (SBIs), time deposits, certificates of deposit, and/or savings deposits in other banks.

Operations of Sharia Rural Banks 1. Public fund collecting in the form of:

Saving in the form of saving deposit or equivalent based on the wadi»ah or other agreement which is not in contravention with Sharia principles; and Investment in the form of time deposit or saving deposit or other equal form based on mudharabah agreement or other agreement which is not in contravention with Sharia principles;

2. Fund distribution to public in the form of:

Profit sharing financing based on mudharabah or musyarakah agreement;

Financing for buying and selling transaction based on murabahah, salam or istishna agreement; Lending and borrowing based on qardh agreement; Leasing of moving or non moving objects to customers based on ijarah or leasing agreement in the form of ijarah muntahiya bittamlik; and Undertaking custodial activities of liabilities based on hawalah agreement;

3. Placing fund in other Islamic bank in the form of depository based on wadi»ah agreement of investment based on mudharabah agreement and/or other agreement which is not in contravention with Sharia principles;

5. Providing product or conducting business of other islamic bank in accordance with Sharia principles and subject to the approval of Bank Indonesia.

D. Operations Not Permitted for Banks

Operations Not Permitted for Conventional Commercial Banks

1. Conducting equity participation, with the exception of those referred to No. 15 and 16 operation for commercial bank above;

2. Conducting business in insurance;

3. Undertaking business other than those referred to in letter C above.

Operations Not Permitted for Sharia Commercial Banks 1. Conducting business activities in contravention with

Sharia principles;

2. Conducting activities related to direct buying and selling of shares in capital market

3. Equity participation except as referred to in point 19 and 20 in Islamic bank business activities.

4. Conducting business in insurance, except if acting as agent of product marketing of islamic insurance.Ω

Operations Not Permitted for Conventional Rural Banks 1. Accepting deposits in the form of demand deposit and

participating in transaction

2. Conducting business in foreign currencies except as money changer;

3. Conducting equity participation; 4. Conducting business in insurance;

5. Conducting other business other than those referred to in letter C.

Operations Not Permitted for Sharia Rural Banks 1. Conducting business activities in contravention with

2. Accepting saving in the form of demand deposit and participating in payment traffic;

3. Conducting business activities in foreign currency, except foreign currency exchange with the approval of Bank Indonesia;

4. Conducting insurance business activities, except as product marketing agent of Islamic insurance; 5. Participation in investment, except in institution

established to overcome liquidity difficulties of Islamic Rural Bank; and

6. Conducting business other than business activities as referred to in section C.Ω

III. BANK REGULATION AND SUPERVISION

As part of its mandate for bank regulation and supervision, Bank Indonesia enacts regulations; issues and revokes licenses for incorporation, establishment of bank offices, and specific bank activities; conducts bank supervision; and imposes sanctions.

A. Objectives of Banking Regulation and Supervision The primary focus of banking regulation and supervision is to ensure the optimum functioning Indonesia»s banking system as:

1. An institution of public trust in respect of funding and disbursement of funds;

2. An institution for implementation of monetary policy; 3. An institution contributing to economic growth and

equity;

With the aim of creating a sound banking system (both overall and in terms of individual banks) capable of safeguarding the public interest, achieving sound growth, and contributing in a useful capacity to the national economy.

To achieve these objectives, the approaches used are as follows:

1. Deregulation

3. Self-regulatory banking, in which banks consistently implement their own internal regulations for operational activities within the overall guidelines of prudential principles.

B. Scope of Bank Regulation and Supervision

1. Right to license, comprising the right to establish procedures for the licensing and establishment of a bank. The scope of licensing by Bank Indonesia includes issuance and revocation of operating licenses for banks; issuance of licenses for establishment, closure, and change of address of bank offices; approval of bank owners and management; and issuance of licenses for banks to conduct certain business operations.

2. Right to regulate, comprising the right to establish regulations governing banking operations and activities for the purpose of fostering a sound banking system capable of delivering banking services as desired by the public.

4. Right to impose sanctions in accordance with laws and regulations in the event that a bank is not fully compliant or is in non-compliance with regulations. Such actions contain elements of guidance to encourage banks to operate in compliance with sound banking principles.

C. Bank Supervision

To perform its bank supervision tasks, BI has introduced a system for supervision applying the twin approaches of compliance-based supervision and risk-based supervision (RBS). The use of the RBS approach does not mean doing away with compliance-based supervision, but represents an effort to improve the supervisory system and thus strengthen the effectiveness and efficiency of bank supervision. Over time, the supervisory approach applied by BI will be progressively changed over to fully risk-based supervision. 1. Compliance based supervision

The compliance-based supervision approach essentially stresses the monitoring of bank compliance for enforcement of the regulatory provisions relevant to bank operations and management. This approach refers to the past condition of the bank with the objective of obtaining assurance that the bank is operated and managed properly in compliance with prudential banking principles.

2. Risk based supervision

Risk based supervision is focused on the kind of risks below:

Credit Risk : Risk is the Risk arising from default by a counterparty in meeting its obligations.

Market Risk Market Risk Market Risk Market Risk

Market Risk : Risk arising from adverse movement in the market variables of the portfolio held by the Bank that may in cur losses for the bank. In this letter, market variables are interest rates and exchange rates.

Liquidity Risk Liquidity Risk Liquidity Risk Liquidity Risk

Liquidity Risk : Risk including but not limited to Risk caused by default of the Bank on liabilities at due date.

Operational Risk Operational Risk Operational Risk Operational Risk

Kind of Risks

Legal Risk Legal Risk Legal Risk Legal Risk

Legal Risk : Risk caused by weaknesses in juridical matters. Weaknesses in juridical matters include but are not limited to weaknesses resulting from legal claims, absence of legal framework, or contractual weaknesses such as failure to meet the requirements for legal.

Reputational Risk Reputational Risk Reputational Risk Reputational Risk

Reputational Risk : Risk including but not limited to Risks caused by negative publicity pertaining to the business operations of the Bank or negative perceptions of the Bank.

Strategic Risk Strategic Risk Strategic Risk Strategic Risk

Strategic Risk : Risk including but not limited to Risks caused by adoption and implementation of an inappropriate strategy for the Bank, inappropriate decision making in the business affairs of the Bank, or lack of responsiveness of the Bank to external change.

Compliance Risk Compliance Risk Compliance Risk Compliance Risk

Compliance Risk : Risk caused by failure of the Bank to comply with or implement prevailing laws and regulations and other legal provisions. Management of Compliance Risk takes place through consistent application of an internal control.

Implementation of number of risk based on complexity and size of each bank.

D. Banking Information System

1. Management Information System √ Bank Indonesia Banking Sector (SIM-SPBI)

activities encompassing collection, calculation and presentation of data/information. In addition, the objective of establishing this system is to develop an integrated information centre that will constantly provide information to support duties related to banking surveillance, examination, reserach, regulatorty.Ω Availability of complete, accurate and timely information on bank condition is expected to support the process of decision making by Bank Indonesia and to be used by other party to the extent that it is implemented in accordance with the applicable provisions.Ω

SIM-SPBI application has the objective of:

Enhancing the effectiveness and efficiency of banking surveillance and examination system;

Establishing standardization in the implementation of banking surveillance and verification tasks; Optimizing Bank Supervisor and Examinor in analyzing bank condition with the objective of improving the quality of bank surveillance and examination;

Facilitating audit trail by relevant stakeholders; Improving security and integrity of data and information.

SIM-SPBI is expected to reinforce the integrity and competence of bank surveillance and examination as well as to enhance the effectiveness of bank supervision that will lead to a sound banking system.ΩΩΩΩΩΩ Ω

a. Supervision Management Information System (SIMWAS)

Internal Circular Letter No. 9/52/INTERN dated December 12, 2007 regarding Management Information System √ Bank Indonesia Banking Sector. SIMWAS is a developed information system to enhance effectiveness and efficiency of Commercial Bank surveillance system.With the implementation of SIMWAS, bank supervisors will be able to optimize analysis activities and to expedite the collection of information regarding bank financial condition (including Bank Soundness Rating and Risk Profile), reinforcing security and integrity of banking information and data.Ω

The SIBADI information system was developed to improve administrative discipline and Modules available in SIMWAS application are classified into the following items:

a. Bank Basic Data; b. Financial Data;

c. Bank Soundness Rating; d. CAMELS & RBS; e. Regular Report; f. Special Report;

g. Early Warning System (EWS); h. Supervisor Analysis;

i. Research;

j. Indonesian Banking Information; k. Consolidated Fit and Proper test

to support the functions of investigation of a criminal act in the banking system, as well as measures of mediation between a client and a bank involving cases with a value of up to Rupiah 500 million.Ω Pertaining to its function and activities, the application of SIBADI is divided into two groups of modules, namely investigation module and mediation module:

Investigation Module Investigation ModuleInvestigation Module Investigation Module Investigation Module

This module has the objective of improving administration regulatory and facilitating monitoring investigation task of banking criminal. This module will enable monitoring on investigation development of crime committed by a bank since the reception of deviation report (from one working unit of banking or public surveillance), investigation schedule, measures that have been taken up to the final result of the concerned investigation.Ω

Mediation Module Mediation ModuleMediation Module Mediation Module Mediation Module

With reference to the extension of DIMP duties and functions as mediation agency between customers and banks., the need for information from user is increased. The function of this application has been extended with data of mediation results on dispute cases between customer and bank, realisation of mediation efforts as well as mediation result in the form of agreement between both parties.Ω

SIBADI application is expected to:

Facilite the administration of database system especially for confidential data.

Support decision making process by Bank Indonesia and other relevant parties insofar as not in contravention with the applicable provisions Enhance the investigator integrity and competence and to improve effectiveness and efficiency of criminal act investigation in the field of banking and mediation of disputed cases between customers and bank in order to finally generate a sound banking system.

c. Data Mart /Bank Basic Data

The Data Mart software application provides information related to the institutionalization, ownership and management as well as operation and supervision strategy adopted by a bank, thus, the system is expected to optimize the information required for bank supervision and development.Ω The objective of Data Mart Bank Basic Data application is described as follows :

enhancing speed, accuracy and completeness in fulfilling user»s need of information.

Facilitating the implementation of user»s duties, accelerating the search of information regarding condition of a bank required by user,

Facilitating user in performing analysis about the condition of a bank.

2. Debtor Information System (SID)

in submitting Credit Report of Commercial Banks. In line with development in information technology, this system has then been upgraded from time to time. Information management that formerly performed by using cards has lately benefited from computer automation. Currently SID has developed into an on-line and realtime web based system accessible to Reporters.

3. Rural Bank Supervision Management Information System (SIMWAS BPR)

In the effort of improving implementation effectiveness of the functions related to supervision, examination and research of rural banks, Bank Indonesia has developed Rural Bank Supervision Management Information System (SIMWAS BPR) which has been officially effective since July 2005. SIMWAS BPR will enable BPR supervisors to optimize their analysis activities pertaining to BPR performance, to accelerate access to information regarding BPR financial condition (including BPR Soundness rating), and to increase the security and integrity of banking data and information.

various institutions or news providing sites. The SIP is also aimed at providing the means in conducting Scenario Analysis that will enable the user in performing the simulation on the effect of internal and external factors on bank condition. In order to facilitate information and data search, SIP is equipped with information search facilities. The scope of the search facilities will continuously expanded gradually.Ω

E. Banking Investigation and Mediation Banking Investigation

Banking investigation performed byΩ Bank Indonesia is one of the efforts to support banking as a sound and reliable industry for the public by implementing law enforcement on criminal act committed by members of Board of Commissioners, Board of Directors, bank employees, shareholders and/or affiliated parties in banking sector. In line with the objective of easing, accelerating and optimising criminal act handling in banking, a collaboration agreement has been set up since 1997 between the Attorney General, National Police and Bank Indonesia. This collaboration has been officialized in the form of a Joint-Decree No. KEP-126/JA/1/1997, KEP/10/XI/1997, 30/6/KEP/ GBI dated November 6, 1997 and has been revised by SKB No. KEP-902/A/J.A/12/2004, No.POL:SKep/924/XII/2004, No. 6/91/KEP.GBI/2004 regarding Collaboration in Handling Criminal Act in Banking industry dated December 20, 2004. In handling cases of banking criminal acts, the coordination of SKB is implemented in an intensive and sustainable way. Moreover, meeting of PENGARAH team on December 24, 2008 has indicated that cases of presumed criminal acts on BPR with operational scale smaller than conventional bank are subject to special attention and need to be handled carefully and in short time considering its potential to disturb overall banking stability.

government institutions such as Bapepam-LK with respect to law enforcement on law infringement related to crisis in global finance and/or Tipibank, and with Bappenas in the framework of UN convention focusing on corruption eradication (UNCAC).

In 2009, the National level of SKB Team will reinforce coordination with agenda among other the enhancing the capacity building of SKB team both at national and regional levels as wellas other investigators in the form of socialization, periodical training of banking criminal act, mutual consultation among institutions and training centers from Bank Indonesia concerning products, banking provisions and modus of banking criminal act. In response to the more complex banking operations and products, handling banking criminal act cases through effective communication in SKB forum will be enhanced with the objective of maintaining banking system stability as part of national financial system.Ω

Banking Mediation

The establishment of an independent banking mediation institution as referred to in Bank Indonesia Regulation No. 8/5/PBI/2006 dated January 30, 2006 regarding Banking Mediation cannot be realized yet due to constraints related to funding and human resources aspects. With reference to that, Bank Indonesia has published a Regulation of Bank Indonesia No. 10/1/PBI/2008 dated January 29, 2008 regarding Amendment of Bank Indonesia Regulation No. 8/ 5/PBI/2006 concerning Banking Mediation to be effective temporarily untl the establishment of independent banking mediation byΩ banking association.

the following documents which are necessary for dispute settlement through banking mediation:

Form related to dispute settlement submission; Copy of letter provided by bank to client related to claim submission;

Copy of client»s valid proof of identity;

A letter of statement duly signed on proper stamp duty indicating that the claim is not in the process of settlement or has been decided by an arbitration agency, court or other mediation agency and has not been submited to banking mediation facilitated by Bank Indonesia;

Copy of documents relevant to the dispute; and Copy of special power of attorney without substitution right (in case of dispute settlement is represented) From January to December 2008 Bank Indonesia had handled a total of 307 cases or an average of 77 cases quarterly and most of them are related to banking system products/services involving payment, fund disbursement and fund collection systems. There were 278 cases of disputes handled while 29 cases are still under process.

Concluding that the implementation of banking mediation as alternative solution for banking disputes is useful to protect customer as well as bank reputation, Bank Indonesia will continue its program of banking mediation socialization.

IV. BANKING POLICIES

A. Indonesian Banking Architecture (API)

The Indonesian Banking Architecture (API) is a comprehensive, basic framework and sets forth the direction, outline, and working structures for the banking industry over the next five to ten years. This policy initiative is founded on a vision of creating a sound, strong, and efficient banking system for achieving financial system stability in support of national economic growth.

1. Creation of sound domestic banking structures, capable of meeting the needs of the public and promoting sustainable economic development.

2. Creation of an effective system for bank regulation and supervision in line with international standards. 3. Creation of a strong, highly competitive banking industry,

resilient in the face of risks.

4. Building of good corporate governance for internal strengthening of the national banking industry. 5. Provision of a complete range of infrastructure to support

the creation of a healthy banking industry.

6. Empowerment and protection of the consumers of banking services.

The six objectives are depicted below as six pillars for achievement of the API vision.

Since its launch on 9 January 2004, API has received varying responses in the form of recommendations and constructive criticism to make the API programs more integrated with the national economy. Furthermore, the development of the global banking industry has demanded adjustment of the API programs so that later the national banking industry shall be able to compete at the international level with better-quality human resources, adequate information technology and sufficient support infrastructure.

A sound, strong, and efficient banking system to create financial system stability in support

In light of this need, Bank Indonesia has updated the API programs. Basically, the revised API programs have more concrete aims and strategies related to national banking system consolidation, long-term development of sharia banking, increased financing of Micro/Small/Medium Scale Enterprises (UMKM) and institutionalization development of Rural Bank. Overall, these revisions have resulted in additional API programs and activities, increasing from 19 programs involving 34 activities to 20 programs involving 55 activities, which shall be implemented in phases through 2013. The API programs are explained in the following table:

1. Program for reinforcing the structure of the national banking system

No. Activity (Pillar I)

1 Improvement of bank capital

a. Increase the minimum core capital requirement of conventional and sharia banks (including BPD) to Rp 80 billion

b. Increase the minimum core capital requirement of conventional and sharia banks (including BPD) to Rp 100 billion

c. Maintain minimum paid up capital requirement of Rp 3 trillion for establishment of a conventional bank until 1 January 2011

d. Set the minimum paid up capital requirement at Rp 1 trillion for establishment of sharia banks

e. Set the capital requirement at Rp 500 billion for sharia banks that are a spinoff of a Sharia Business Unit f. Shorten the deadline for Rural Bank compliance with the

minimum paid up capital requirement from 2010 to 2008

2. Building the competitiveness and institutionalization of Rural Banks and Sharia Rural Banks

a. Strengthen the linkage program between conventional banks and Rural Banks

No. Activity (Pillar I)

c. Promote the establishment of Rural Banks and Sharia Rural Banks outside of Java and Bali

d. Facilitate the opening of Rural Banks and Sharia Rural Banks branch offices for those that fulfill the criteria e. Expedite the formation of joint service facilities for Rural

Banks and Sharia Rural Banks (including APEX Institutions)

3. Improving UMKM access to credit and financing a. Facilitate the formation and monitoring of credit and

financing guarantee scheme

b. Encourage banks to increase financing of UMKM, particularly for low-income and village inhabitants c. Increase access to sharia financing for UMKM through

development of guarantee programs for sharia financing d. Encourage sharia banks to increase the percentage of

profit-sharing based financing

2. Program for Improved Quality of Bank Regulation

No. Activity (Pillar II)

1 Formalizing the syndication process in policymaking for the banking system

a. Involve a third party in banking system policymaking b. Form a panel of banking experts

c. Facilitate the formation of banking research institutes at the central level and certain regions

2. Phase implementation of international best practices a. 25 Basel Core Principles for Effective Banking Supervision b. Basel II

c. Islamic Financial Service Board (IFSB) for sharia banks

3. Program for Improvement of Supervisory Function

No. Activity (Pillar III)

No. Activity (Pillar III)

2. Reorganization of banking sector at Bank Indonesia a. Revise High Level Organization Structure (HLOS) of the

Banking Sector at Bank Indonesia

b. Consolidation of supervision and examination units, including the establishment of special team of specialist examiners

c. Consolidation of Rural Bank Supervision Directorate and Credit Bureau at Bank Indonesia, including the transfer of functions of:

• UMKM research and development of the Credit Bureau to the Special Assets Management Unit • Examination of credit from the Credit Bureau to the

Conventional Bank Supervision Directorate d. Revise the organization of the Bank Perkreditan Rakyat

Supervision Directorate (DPBPR) to allow the transfer of the guarantee role of Rural Banks to a Deposit Insurance Agency, and the transfer of the licensing of new Rural Banks, along with research and supervision to other work unit at Bank Indonesia

e. Revise the organization of the Sharia Banking Directorate

3. Improve Support Infrastructure for Banking Supervision a. Improve the competency of supervision of both

conventional and sharia banks and Rural Banks through a certification program and attachment to international supervision agencies

b. Train Supervision Specialists c. Improve IT for banking supervision d. Improve the Rural Bank reporting system

e. Improve banking supervision documentation management

4. Improve the implementation of the risk-based supervision system

a. Improve the guidelines and supervision instruments to improve the implementation of risk-based supervision of conventional and sharia banks

5. More effective enforcement

a. Improve the process of investigation of banking crimes b. Increase the transparency of supervision to support

effective enforcement

4. Quality Improvement Program for Bank Management and Operations

No. Activity (Pillar IV)

1. Building Good Corporate Governance (GCG)

a. Establish minimum standards of GCG for conventional and sharia banks

b. Require banks to perform self-assessment of CGC implementation

c. Encourage banks to go public

2. Improve the quality of bank risk management

a. Require certification for risk managers at conventional and sharia banks

b. Improve the quality and standard of Rural Banks and Sharia Rural Banks human resources through professional certification programs for Rural Banks and Sharia Rural Banks bank directors

3. Strengthening bank operational capacity

a. Encourage banks to initiate sharing of use of operational facilities to curb costs

b. Facilitate education and training to strengthen bank operational capacity

5. Program for Development of Banking Infrastructure

No. Activity (Pillar V)

1 Development of Credit Bureau

a. Initiate the establishment of the Credit Bureau b. Develop the Debtor Information System for Non Bank

Financial Institutions

2. Promote the development of Islamic Financial Market a. Draft and develop Islamic financial market regulations] b. Draft regulations related to Islamic financial market

instruments

6. Program for Improvement of Customer Protection

No. Activity (Pillar VI)

1. Formulation of standards for customer complaints mechanism a. Establish minimum criteria for customer complaints

mechanism

b. Monitor and evaluate the compliance to regulations governing customer complaints mechanism

2. Establishment of independent mediation agency

- Facilitate the establishment of independent mediation agency

3. Drafting of regulations on transparency of product information a. Facilitate the drafting of minimum standards for

transparency of banking product information

b. Monitor and evaluate the implementation of regulations governing transparency of product information

4. Promoting public education for customers

a. Encourage banks to educate customers regarding financial products

b. Upgrade the effectiveness of public education programs regarding sharia banking through the Sharia Economics Communications Center (PKES)

Under the program for structural reinforcement of the national banking system, the banking structure envisaged to take shape in the next 10 to 15 years is as follows:

Structure of Indonesian Banking System Envisaged in API

Capital Rp trillions

International Banks

Domestic Banks

Specialized Banks

Regional Corporate Retail Others

Rural Banks 50

10

B. Building the Indonesian Financial System Architecture (ASKI)

Indonesian Financial System Architecture (ASKI) is a strategic direction of Indonesian financial system development implemented in stages, overall and mid-long term. ASKI was designed with basic framework reflecting Indonesian financial system comprising various inter-related financial sub-sectors supported by six pillars for the achievement of ASKI vision and mission.Ω

Scale Total Assets Capital 10-15 year (Rp) (Rp) projection

(number of banks)

International 1,000 trillion > 50 trillion 2 √ 3 banks National 200 trillion 10 √ 50 trillion 3 √ 5 banks Focus: - 100 billion √ 10 30 √ 50 banks - Regional trillion

- Corporate - Retail - Others

Rural Banks - up to 100 billion

Figure 1

Basic Framework of Indonesian Financial System ArchitectureΩ

- Trade, Restaurant and Hotel - Public Social Services - Mining - Electricity, gas and

water

System Sound, Stableand Liquid Structure and

Non-Banking Financial System : 1. Insurance

2. Pension Fund 3. Financing Institution 4. Pawn Services 5. Micro Financial Institution

REAL SECTOR Indonesian financial system functioning

efficiently, securely, soundly and in a stable way, high sustainability in playing optimal role to improve the prosperity of Indonesian people

- Stable Monetary and Fiscal System - Conducive Political, Social, Legal and Security Environment

ASKI vision ASKI vision ASKI vision ASKI vision

ASKI vision is Indonesian financial system set forth for an efficient, secure, sound, robust function with optimal role in improving the prosperity of Indonesian people. ASKIASKIASKIASKIASKI mission

missionmission mission

mission will be to reach future Indonesian financial system through fundamental and stability reinforcement by taking into consideration the synergized development among sub-sectors in financial system.

The ASKI divides the financial system into various sectors that will be developed until 2025 encompassing banking, capital market, money market, pension funds, insurance, financing institutions, pawn shops and micro financial institutions. In reaching ASKI vision and implementing its mission, all financial sub sectors is supported by six principal pillars of ASKI. The six pillars are formulated as follows:Ω

Pillar 1. Pillar 1. Pillar 1. Pillar 1.

Pillar 1. Human Resources Pillar 2.

Pillar 2. Pillar 2. Pillar 2.

Pillar 2. Management and Risk Management Pillar 3.

Pillar 3. Pillar 3. Pillar 3.

Pillar 3. Information System and Infrastructure Pillar 4.

Pillar 4. Pillar 4. Pillar 4.

Pillar 4. Institution and Market Structure Pillar 5.

Pillar 5. Pillar 5. Pillar 5.

Pillar 5. Regulation and Supervision Pillar 6.

Pillar 6. Pillar 6. Pillar 6.

Pillar 6. Protection and Empowerment of Investors and ConsumersΩ

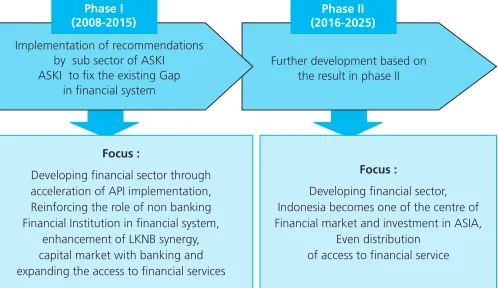

The framework of ASKI development is directed to the reinforcement of real sector to support economic growth and to create job opportunities as well as to enhance the prosperity and the social welfare of Indonesian people through the implementation of six ASKI pillars in each sub sector of financial system (figure 2). In facilitating achievement indicator accompanied by evaluation of ASKI implementation, the target and strategy of ASKI program is divided into the two following phases (figure 3):

Phase I Phase I Phase I Phase I

Phase I starts from 2008 to 2015 with the establishment of Asean Economic Community (AEC).

Phase II Phase II Phase II Phase II

Furthermore, with the objective of reaching ASKI vision each financial sub-sector will develop its own strategy of implementation for each phase of development.

Figure 2

Direction of ASKI DevelopmentΩ

Figure 3

Phases and Focus of Indonesian Financial System Development

- Indonesia becomes centre of Financial market and investment in ASIA

- Access to financial service: wide and even - Banking: sound, strong

and efficient - Capital Market: More

efficient, deep. - Insurance and Pension

fund: higher penetration

- Macro economy: stable, but still fragile - Banking: Consolidation - Capital Market: inefficient, - Insurance and Pension

Fund: Low Penetration - Infrastructure of

financial system: insufficient

-Access to Financial

Servicefor poor people

and micro business:

Further development based on the result in phase II Implementation of recommendations

by sub sector of ASKI ASKI to fix the existing Gap

in financial system Indonesia becomes one of the centre of Financial market and investment in ASIA,

Even distribution of access to financial service

Focus :

Developing financial sector through acceleration of API implementation, Reinforcing the role of non banking Financial Institution in financial system,

enhancement of LKNB synergy, capital market with banking and expanding the access to financial services

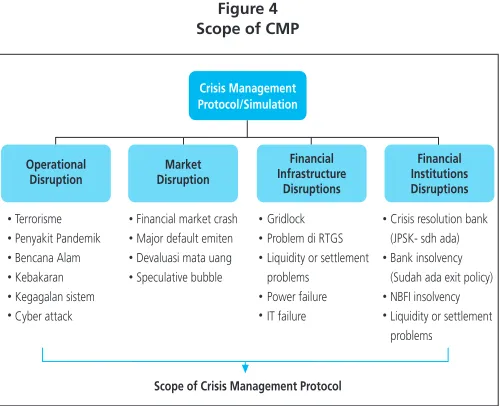

Financial crisis is not only affected by financial risk but also by the risk arising from important disruption stemming from non financial risk. Anticipation in overcoming crisis on financial system management is often known as Financial System Continuity Planning (FSCP) or the term adopted in a wider scope is Crisis Management Protocol (CMP).Ω Crisis Management Protocol (CMP) is a framework designed to minimize the impact of financial distress (MAS, 2003). CMP also symbolizes a plan to maintain financial system stability rapidly and with effective cost (PWC). The scope of CMP includes operational disruptions, market disruption, financial infrastructure disruption and financial institutions disruption (Figure 4). Each financial sub-sector is currently preparing CMP including those at the level of Financial System Stability Committee (KSSK) in the frameworkrk of preventing and handling crisis in financial system. Relevant financial authorities will conduct stress test or crisis simulation on regular basis on CMP and will continuously make improvement in compliance with domestic and global financial market. Ω

Scope of Crisis Management Protocol

CMP framework in Indonesia encompasses CMP established by each financial authority (Bank Indonesia, Saving Guarantee Agency, and Ministry of Finance) and coordination and decision on who will do what as well as the nomination of a PIC (person in charge) must be initiated. Meanwhile, the legal base for the financial authorities in crisis prevention and handling is regulated in the law of the Safety Network of Financial System.Ω

Coordination

The scope of ASKI Blueprint, which encompasses various authorities, is so extensive that it requires strong, concrete and sustainable support, involvement, cooperation and commitment of each authority involved in the finalization and implementation. Moreover, the role and support from policy maker level for the finalization of ASKI Blueprint needs also to be enhanced.Ω

C. Adoption of the Basel II Accord

The Basel Capital Accord is a capital measurement system launched by the Basel Committee on Banking Supervision (BCBS) in 1988. Initially the BCBS recommendation was designed as reference for Bank Supervisory Authority in G 10 countries however as a result of its development this recommendation has also become the reference of Supervisory Authority in countries other than G 10. In line with the growing sophistication of financial market instruments, application of risk management, BCBS considered that one-size fits-all approach has lost relevance and it thus became necessary for revision. The revision was published in June 2004 in a document entitling ≈International Convergence of Capital Measurement and Capital Standards - A Revised Framework∆ or more known as Basel II.Ω

In an outline the framework of Basel II comprises 3 (three) following Pillars:Ω

Pillar 1. Minimum Capital Requirements

Calculation of minimum capital requirement is performed on 3 (three) types of the biggest risks faced by banking, namely credit risk, market risk and operational risk. There are several approaches available for each risk that can be used by bank based on product and activity complexitiy level of the bank. The implementation of a more complex approach in calculating minimum capital requirement is voluntary for each risk depending also on bank readiness and it is subject to the approval of supervisory authority.Ω Ω

Pillar 2. Supervisory Review Process

There are 4 (four) main principles in Pillar 2 desgined to complete Pillar 1 with respect to calculation of minimum capital requirement and they are:Ω

Principle 1. Principle 1. Principle 1. Principle 1.

Principle 1. Bank has the obligation to have an assessment process of overall capital adequacy related to risk profile and strategy in maintainingΩ capital level (Internal Capital Adequancy Assessment Process √ ICAAP)Ω

Principle 2. Principle 2. Principle 2. Principle 2.

Principle 2. Supervisor is obliged to review and evaluate internal capital adequacy assessment process and bank strategies including bank capability to monitor and confirm compliance to capital ratio provision. Supervisor has the obligation to take correct supervisory measures in case of failure in accepting the process result (Supervisory Review and Evaluation Process √ SREP).Ω

Providing a flexible, risk sensitive capital management framework Basel II

3 Pillar

Supervisory Review Process

Market Discipline Minimum

Principle 3. Principle 3.Principle 3. Principle 3.

Principle 3. Supervisor has the obligation to require bank to operate over the defined capital ratio and to require bank to provide capital over minimum limit.Ω

Principle 4. Principle 4.Principle 4. Principle 4.

Principle 4. Supervisor is obliged to make intervention as soon as possible to avoid any capital decrease to below minimum level required to support banking risk characteristics and is obliged to require bank to conduct an immediate supervisory action in a situation where bank capital cannot be maintained or remedied.Ω

In performing supervisory review and evaluation process as referred to in Principle 2, supervisor will be able to calculate bank capital adequacy on:

Risks that have not been fully estimated in Pillar 1 due to the use of standard approach by bank, such as concentration risk;

Risks that have not been calculated in Pillar 1 such as liquidity risk, interest rate risk in banking book, reputational risk and strategic risk. Some of those risks cannot be calculated quantitatively therefore they will be qualitatively interpreted. Risks stemming from bank external factor due to applicable policy, and economic or business condition.

Should the Supervisor face an evaluation with insufficient bank capital (undercapitalized) an accurate supervisory action will be immediately implemented such as additional capital or improvement of risk management quality.Ω

Pillar 3. Market Discipline

The application of Basel II by a country is not obligatory; however, in line with the objective of Basel II of creating a stable financial system, BI opted to apply the principles of Basel II. BI decided to apply Basel II due to the following reasons: to have a risk sensitive oriented bank capital structure, to motivate bank to increase it risk management capability, to adopt a more comprehensive scope, as well as to raise understanding between supervisor and bank especially in using a more complex approach by bank.Ω The following conditions should be prepared in the application of Basel II in Indonesia:Ω

Pillar 1. Minimum Capital Requirement

1. Banking industry is required to perform gap analysis including the follow up needed to to be undertaken in fulfilling the arising gap. This activity is conducted in order to know the actual condition of the bank with regards to the roadmap of Basel II implementation. 2. In regulating credit risk several policies will be adopted in

preparing the provisions related to national discretions. This process allows other stakeholders to participate, including banks to be in compliance with national banking condition.Ω 3. Guidelines have to be prepared for the acknowledgement of rating agency especially domestic rating agency in order to fulfill eligibility criteria). This acknowledgement process should be coordinated with BAPEPAM-LK being the authority in publishing licenses to rating agency.Ω 4. Quantitative Impact Study-QIS 5) has been performed

5. Several provisions related to calculation of bank capital are designed such as:

a. External Circular Letter No.9/31/DPNP dated December 12, 2007 and External Circular Letter No.9/33/DPNP dated December 18, 2007 regarding to the use of standard and internal methods in calculating KPMM of market risk.

b. Bank Indonesia Regulation No.10/15/PBI/2008 dated September 24,Ω 2008 regarding Minimum Capital Requirement for commercial bank.

c. External Circular Letter No.11/3/DPNP dated January 27, 2009 related to the adoption of basic indicator method for calculation of operational risk of Minimum Capital Requirement (KPPM).Ω

Pillar 2. Supervisory Review Process

1. Policy related to bank capital adequacy assessment process (ICAAP), review process and supervisor evaluation, capital determination for individual bank and supervising action to be taken for certain banks needs to be promulgated. This policy must include the approach to be performed in the framework of home-host supervisory approach. With regards to this, BI has prepared and sent Consultative Paper (CP) to stakeholders pertaining to the application of Pillar 2.Ω 2. BI is reviewing the framework of risk based supervision

including identifying the existing gap based on the standard of Pillar 2 and the effort of fulfilling 25 Basel Core Principles for Effective Banking Supervision (BCP). The improvement of bank supervisory frame is expected to support supervisor in reviewing bank capital in accordance with bank risk profile.Ω

4. BI needs to prepare Specialist Supervisor Group to anticipate the development of internal model such as market risk that has been communicated by bank since 2008. BISMI (Bank Indonesia Internal Model System) has been particulary developed to assist KPS in validating internal model of market risk. It will be followed by setting up a validator of credit risk with duties to validate Internal Rating Based (IRB) model developed by bank for the calculation of credit risk of capital weight as well as a validator for operational risk with duties to validate Advanced Measurement Approach (AMA) model developed by bank for the calculation of operational risk of capital weight.Ω

5. Sustainable trainings are needed for supervisor related to risk management, innovative financial instrument, modeling techniques and etc in order to improve supervisors» quality.Ω

6. Surveys and studies on types of risk which are deemed material for banking in Indonesia and not included in Pillar 1 such as Interest Rate Risk in The Banking Book (IRR-BB), Liquidity Risk and Credit Concentration Risk have been compiled and will be considered as input in preparing provisions related to that subject.Ω

Pillar 3. Market Discipline

1. BI with Indonesian Accountant Association (IAI) needs to determine policy related to International Accounting Standards (IAS) 39 and 32 in Standard Statement of Indonesian Accountancy (PSAK) No. 50 and 55 which will be implemented starting January 1, 2010. A guideline of Indonesian Banking Accoutancy has been prepared as the follow up of the concerned PSAK. 2. The improvement of Commercial Bank Monthly Report

3. Gap identification between the current transparency obligations with the standard defined in Pillar 3 that will lead to the improvement of the existing provisions related to transparency of bank financial condition and publication of financial report of commercial banks.Ω 4. Dissemination and socialization of Basel II substance

should be continued to Bank Indonesia internal, banks and other stakeholders.Ω

D. Development of Sharia Banking

The policy of Islamic banking development is applied with respect to the Blue Print of Islamic Banking Development that actually enters its second phase. The policy adopted in this phase was set into force in 2005 and focused on the strengthening of industrial structure of Islamic banking. In addition to that, the validation of Law No. 21 of 2008 regarding Islamic Banking has contributed a strong support to legal aspect. The law, direct or indirect one, has become a guideline in developing national Islamic banking in the future and it is expected that this Law will be the milestone of the growth of Islamic banking industry in Indonesia. Ω One important measure of the program to clarify the position and strategy of Islamic banking development within national financial system is through the synchronization of policies of Islamic banking development in the Blue Print in line with the strategic plan of Bank Indonesia to develop the banking and finance industry, namely, the Indonesian Banking Architecture (API) and Indonesian Financial System Architecture (ASKI).Ω

competitiveness efficiency, (4) system stability and benefit to economy, (5) enhancement of professionalism competence of human resources, and (6) optimization of social function of sharia banks in facilitating voluntary sectors with people»s economy development program. Ω

The policy that supports compliance to Sharia principles in The policy that supports compliance to Sharia principles in The policy that supports compliance to Sharia principles in The policy that supports compliance to Sharia principles in The policy that supports compliance to Sharia principles in banking operation

banking operationbanking operation

banking operationbanking operation has been supported by the validation of Law No. 21 of 2008 regarding Islamic Banking. This Law has conditioned the establishment of Islamic Banking Committee (KPS) with duties to support Bank Indonesia in the implementation of fatwa of Majelis Ulama Indonesia (MUI) to become provisions that will be stipulated in Bank Indonesia Regulation (PBI). The existence of KPS has also been regulated in PBI No. 10/32/PBI/2008 dated November 20, 2008 regardig Islamic Banking Committee. In order to complete the guideline of implementing islamic financial agreement in banking operation, a Study on Monetary Agreement based on Sharia Principles has been prepared and it ise expected to be used a guideline in formulating monetary policies based on Sharia principles and bank will dominantly be involved as market player. Ω

Policy in the scope of reinforcing compliance to prudential Policy in the scope of reinforcing compliance to prudential Policy in the scope of reinforcing compliance to prudential Policy in the scope of reinforcing compliance to prudential Policy in the scope of reinforcing compliance to prudential principle in Islamic banking operation

principle in Islamic banking operationprinciple in Islamic banking operation

standard in Islamic Financial Service Board (IFSB). Standard that has been in completion stage (finalization)Ω in 2008 is the standard of The Guiding Principles on Sharia Governance and The Guiding Principles on Business Conduct. Standards which are still under completion process include the standard related to supervisory review process and standard transparency and market discipline. Ω

In the framework of operation efficiency development and In the framework of operation efficiency development andIn the framework of operation efficiency development and In the framework of operation efficiency development and In the framework of operation efficiency development and competitiveness of Islamic banking

competitiveness of Islamic banking competitiveness of Islamic banking competitiveness of Islamic banking

hand, in the framework of enhancing competitiveness of the industry, with reference to the grand strategy of Islamic banking development, promotions and public educational programs were introduced in 2008 focusing on beneficial aspects and uniqueness of Islamic banking, both in terms of product or its implication to the economic and social aspects. Adopting the jargon ≈Beyond Islamic Banking∆ it is expected to be able to provide a better industrial image and a wider social segment being the target of users on Islamic banking services.Ω

Meanwhile in the effort of supporting systemic stability and Meanwhile in the effort of supporting systemic stability and Meanwhile in the effort of supporting systemic stability and Meanwhile in the effort of supporting systemic stability and Meanwhile in the effort of supporting systemic stability and providing benefits to national economy

providing benefits to national economyproviding benefits to national economy

providing benefits to national economyproviding benefits to national economy a Study of Islamic Financing Model for UMKM in the agricultural sector that will generate a description and recommendation both for Islamic banking and UMKM (especially in the agricultural sector) about the Islamic financing condition in the sector. This study is the follow up of linkage program conducted in the previous year in several regions as the reinforcement on the trainer competence or the associate from UMKM both in government institutions or Islamic banking. The dominant financing of Islamic banking ton UMKM and the effort shown by this sector in maintaining the performance and growth of Islamic banking industry despite the global financial crisis condition has become an important base for the efforts in reinforcing this business sector. One of the efforts is to conduct a study in the field of UMKM and to provide sufficient information for banking sector in optimizing the role and activities of UMKM sectors.Ω Ω Development of human resources in the field of IslamicDevelopment of human resources in the field of IslamicDevelopment of human resources in the field of IslamicDevelopment of human resources in the field of IslamicDevelopment of human resources in the field of Islamic

banking bankingbanking

bankingbanking, in terms of management of Islamic bank, employees of Bank Indonesia or the public is continuously implemented through sistematic, focused and sustainable educational program.Ω

has become essential and obligatory in developing this young Islamic banking industry. On the other hand the need of human resources also depends on product innovation development in the industry, complexity of business activity requiring a good risk management, and the demand of users on the quality of Islamic banking services. With respect to this fact, a number of strategic programs have been implemented in 2008 representing the long term initiative to support the availability of human resources in Islamic banking both in terms of quantity or quality in response to future needs and challenges. Human resources development programs in islamic banking are, among others, as presented below:Ω

(a) Certification program for the Board of Director of Islamic Rural Banks

In enhancing and obtaining minimum standard of Islamic banking capacity and capability particularly Islamic Rural Bank, Bank Indonesia has worked in collaboration with Profession Standard Agency Micro Financial Institution (LSP LKM) CERTIF and Indonesian Banking Development Institution (LPPI) since 2006 in implementing certification program for the Board of Directors of Islamic Rural Bank. There were 252 Islamic Rural Bank Directors from all over Indonesia who had obtained certifications from 2006 to December 31, 2008. Ω

(b) Organization of Training for Conventional Bank Employees envisaging of opening Islamic Services and for New Employees of Islamic Business Unit and Islamic BUS