Refer to Important disclosures in the last page of this report

Stock DataTarget price (Rp) Rp1,250

Prior TP (Rp) Rp1,370

Encore Energy PTE LTD 35.7%

Credit suisse Group 20.7%

Mitsubishi UFJ 15.0%

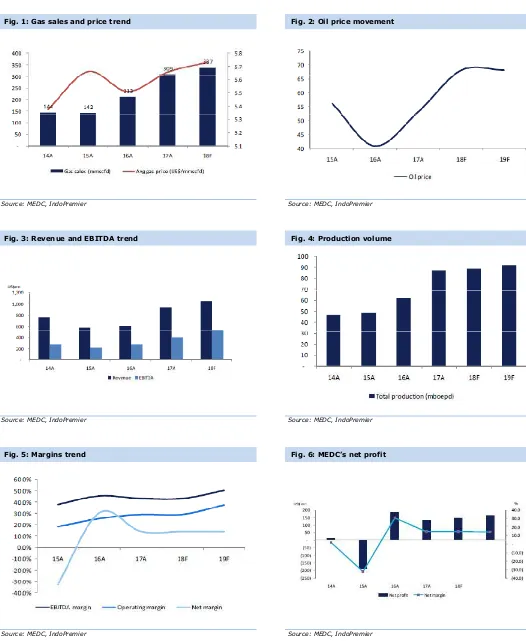

Net profit declined by 50% but EBIT/EBITDA was up by 50%/86%.

Margins expansion due to higher ASP both oil and gas.

Amman’s phase 7 development is on track.

Maintain Buy with lower TP of Rp1,250 (from Rp1,370).

Net profit declined by 50.4% yoy.

Medco Energi Internasional posted net profit

amounted to US$41.4mn, down 48.6% yoy. Forming only 23.3%/17.3% of

ours/consensus FY18 estimates. Nevertheless, revenue increased by 42.4% yoy

to US$578.6mn (c. 55% to our FY18 estimates) while EBITDA and operating profit

grew by 50.5% yoy and 86.7% yoy. Earnings was mainly dragged by tax expense

that inclined by 60% yoy as the tax rate stood at 65.3% in 1H18 (vs. 40.5% in

1H17). On quarterly basis, net profit decreased by 41.2% qoq to US$15.3mn

albeit its operating profit and EBITDA grew by 16.2% qoq and 4.3%. Amman still

recorded a net loss of some US$10.6mn due to lower production volume with

higher stockpiles content that erode Amman’s overall margins.

Operational margins expand due to higher ASP.

On operational data, the

company posted relatively stable production rate with oil and gas production was

stood at 82.4 mboepd in 1H18. But the company optimists they could meet their

production target of around 85 mboepd as Block A Aceh gas sales will ramp up in

early August 2018. MEDC posted higher ASP with average realized prices were

US$66.8/bbl (+35.4%yoy) for oil and US$6/mmbtu (+8.6% yoy) for gas. Oil and

gas unit cash costs were US$8.5/bbl, in line with company’s target to maintain

unit cash costs below US$10/bbl. This led the company posted better margins in

1H18, with operating margin of 31.9% (+990bps) and EBITDA margin of 49.3%

(+280bps). Medco Power Indonesia’s gross installed capacity rose 20% yoy to

2,795MW in 1H18 following commercial operation in May of the third and final unit

of phase one of the Sarulla Geothermal facility.

Positive progress from phase 7 development.

In 1H18 AMNT has ramped up

phase 7 developments to full capacity and secured its first facility from an

international bank. Amman is in the process of appointing the smelter Front End

Engineering and Design contractor. Operational wise, Amman’s copper/gold

production decreased by 45.8%/77.5% yoy, respectively in 1H18.

Maintain Buy.

We trim our earnings forecasts for 2018F by 42.6% to US$102mn

as we revise up our tax rate assumption from previously 50% to 65% in 2018F.

Downward revisions on our earnings forecasts has led to our DCF-based TP

Source: MEDC, IndoPremier Share Price Closing as of : 2-August-2018

MEDC IJ Results Note

2

Refer to Important disclosures in the last page of this report

Fig. 1: Gas sales and price trend Fig. 2: Oil price movement

Source: MEDC, IndoPremier Source: MEDC, IndoPremier

Fig. 3: Revenue and EBITDA trend Fig. 4: Production volume

Source: MEDC, IndoPremier Source: MEDC, IndoPremier

Fig. 5: Margins trend Fig. 6: MEDC’s net profit

3

Refer to Important disclosures in the last page of this report

Year To 31 Dec (US$Mn) 2016A 2017A 2018F 2019F 2020F

Cash & Equivalent 231 661 477 477 360

Receivable 535 635 678 767 857

Inventory 70 89 82 85 86

Other Current Assets 298 590 572 556 540

Total Current Assets 1,134 1,975 1,809 1,885 1,843

Fixed Assets - Net 926 1,176 1,082 726 627

Goodwill 0 0 0 0 0

Non Current Assets 499 1,033 1,156 1,174 1,191

Total Assets 3,597 5,161 5,036 4,779 4,658

ST Loans 16 42 42 42 42

Payable 105 140 0 141 143

Other Payables 345 747 174 181 184

Current Portion of LT Loans 395 365 500 250 0

Total Current Liab. 861 1,294 851 614 369

Long Term Loans 1,522 2,182 2,197 2,161 2,125

Other LT Liab. 324 283 688 567 585

Total Liabilities 2,707 3,758 3,735 3,342 3,079

Equity 256 499 499 499 499

Retained Earnings 631 672 656 793 935

Minority Interest 3 145 145 145 145

Total SHE + Minority Int. 891 1,316 1,301 1,437 1,579

Total Liabilities & Equity 3,597 5,074 5,036 4,779 4,658

MEDC IJ Results Note

4

Refer to Important disclosures in the last page of this report

Year to 31 Dec 2016A 2017A 2018F 2019F 2020F

Cash Flow

Net Income (Excl.Extraordinary&Min.Int) 185 132 102 161 180

Depr. & Amortization 263 96 (26) 391 135

Changes in Working Capital (306) 169 (332) (81) (86)

Others 2 71 (141) (101) 166

Cash Flow From Operating 157 492 (398) 369 394

Capital Expenditure (86) (879) (3) (53) (52)

Others (547) (13) 205 67 67

Cash Flow From Investing (634) (892) 202 13 15

Loans 353 656 149 (286) (285)

Equity (1) 194 0 0 0

Dividends 45 (46) (33) (26) (41)

Others (166) (28) 296 (331) (201)

Cash Flow From Financing 231 776 412 (643) (527)

Changes in Cash (245) 375 216 (261) (118)

Financial Ratios

Gross Margin (%) 41.7 45.5 50.5 50.6 51.6

Operating Margin (%) 25.5 29.1 37.2 37.3 38.3

Pre-Tax Margin (%) 43.4 31.9 28.0 29.5 32.0

Net Margin (%) 30.8 14.2 9.7 14.7 15.9

ROA (%) 5.7 3.0 2.0 3.3 3.8

ROE (%) 23.2 11.9 7.8 11.7 11.9

ROIC (%) 7.5 5.0 4.2 5.9 6.7

Acct. Receivables TO (days) 85.6 74.8 74.2 88.5 108.4

Acct. Receivables - Other TO (days) 144.2 155.9 154.4 152.7 153.2

Inventory TO (days) 6.3 6.3 6.1 6.5 6.4

Payable TO (days) 95.1 88.4 96.7 93.3 94.4

Acct. Payables - Other TO (days) 92.4 99.2 77.9 34.3 34.7

Debt to Equity (%) 217.1 196.7 210.5 170.6 137.3

Interest Coverage Ratio (x) 0.7 0.5 0.5 0.5 0.5

Net Gearing (%) 198.6 159.5 175.9 139.2 116.1

Head Office

PT INDO PREMIER SEKURITAS

Wisma GKBI 7/F Suite 718

Jl. Jend. Sudirman No.28

Jakarta 10210 - Indonesia

p +62.21.5793.1168

f +62.21.5793.1167

INVESTMENT RATINGS

BUY : Expected total return of 10% or more within a 12-month period HOLD : Expected total return between -10% and 10% within a 12-month period SELL : Expected total return of -10% or worse within a 12-month period

ANALYSTS CERTIFICATION.

The views expressed in this research report accurately reflect the analysts personal views about any and all of the subject securities or issuers; and no part of the research analyst's compensation was, is, or will be, directly or indirectly, related to the specific recommendations or views expressed in the report.

DISCLAIMERS