Renegotiation Costs, Financial Contracting, and

Lender Choice

Elia Ferracutia,∗

, Arthur Morrisa

a

David Eccles School of Business, University of Utah

Abstract

This study exploits an exogenous change in renegotiation costs to analyze the relationship between renegotiation costs and initial contracting. TD9599 ma-terially reduces the tax burden of renegotiating syndicated loans, while leav-ing the taxation of renegotiatleav-ing sleav-ingle-lender loans and bonds unchanged. We use this setting to offer insights into the implications of incomplete con-tracting theory for three contract features: debt maturity, the initial likeli-hood of covenant violation, and the use of performance pricing provisions. Consistent with the incomplete contracting theory, we find that as renego-tiation costs fall the maturity of debt contracts lengthens, the likelihood of covenant violation increases, and the use of PPPs becomes less frequent. We further study whether renegotiation costs influence borrowers’ lender pref-erence. Consistent with TD9599 eliminating the asymmetric taxation of syndicated loans and public bonds during out-of-court renegotiation, we find that lower cost of renegotiation shift borrowers’ preferences away from public bonds and toward private loans.

Keywords: Renegotiation, Financial Contracting, Lender Choice

∗Corresponding author

Email addresses: [email protected](Elia Ferracuti),

[email protected](Arthur Morris)

1. Introduction

Debt contracts are curiously complex, and, paradoxically, prone to rene-gotiation (Roberts and Sufi, 2009b, Denis and Wang, 2014, Roberts, 2015). On the one hand, complete contracting theory imagines contracts so detailed as to anticipate every eventuality, rendering renegotiation unnecessary. On the other hand, the Coase theorem argues for simple contracts that are dy-namically completed by renegotiation that is frequent, costless, and perfectly informed (Coase, 1960). That debt contracts are simultaneously detailed and frequently renegotiated supports the hybrid notion from Grossman and Hart (1986) and Hart and Moore (1988) that borrowers and lenders complement theex-ante allocation of cash flow rights through the initial terms in the loan contract with theex-post reallocation of control rights through renegotiation. Garleanu and Zwiebel (2009) suggest that incomplete information and relatively inexpensive renegotiation can give rise to tighter covenants and more frequent renegotiations. Rather than to create a complete contract, the multitude of tight covenants observed in practice may be intended as a series of triggers for renegotiation. As lenders learn about the borrower and the borrower’s investment opportunities, renegotiations appear to allow the parties to complete the contract over time (Roberts and Sufi, 2009b, Roberts, 2015). This framework has implications not only for the frequency of renegotiation, but also for the relationship between renegotiation costs and initial debt contract design.

Our study explores this relationship between renegotiation costs and ini-tial debt contract design contracting. As we hypothesize that the ex-post ef-ficiency of debt contracts varies with renegotiation costs, we also expect that renegotiation costs have implications for lender choice and capital structure. Though debt contracts are economically important in their own right, and provide a potentially powerful laboratory for testing theories about contract-ing generally, testcontract-ing these theories empirically has proved difficult. Debt contract terms are simultaneously determined by renegotiation costs, moni-toring costs, macroeconomic factors, and agency concerns created by incom-plete information. Lack of random variation in the design of debt contracts and renegotiation costs has made inference about the relationship between renegotiation costs and initial contract design difficult (Roberts, 2015). In this study we exploit variation in renegotiation costs generated by a recent tax regulation change to investigate this relationship.

Internal Revenue Service Bulletin 2012-40: Property Traded on an

lished Market (TD9599), adopted on 12 September 2012, refined the defini-tion of an established market for tax purposes to include debt instruments for which a ‘soft quote’ is available. This redefinition significantly reduced the tax burden of renegotiating syndicated (multi-lender) loans, while leaving the taxation of single-lender loans and bonds unchanged (Campello et al., 2016). We use TD9599 to isolate the effect of renegotiation costs on initial contract terms and contract efficiency from the multitude of other determinants of debt contract terms.

Two features of the TD9599 setting are particularly useful in reducing endogeneity concerns. First, TD9599 produces economically significant vari-ation in renegotivari-ation costs (Campello et al., 2016) by reducing the tax bur-den of renegotiation. As taxes are a major determinant of the choice between renegotiation and bankruptcy (Gilson, 1997), we expect that if renegotiation costs do impact initial contract terms, TD9599 should induce an economically significant shift in initial contract terms.

Second, adoption of TD9599 appears unrelated to other determinants of the initial contract terms. While no regulation is truly exogenous, TD9599 would need to also reduce information asymmetry only between loan syn-dicates and their borrowers or reduce monitoring costs only for syndicated loans. It is difficult to see how a change in taxation would produce varia-tion in the underlying agency problems that debt contracts are hypothesized to address. Together, these attributes of TD9599 introduce variation in the renegotiation costs of syndicated loans without impacting agency costs, mon-itoring costs, and other factors that simultaneously determine initial contract terms.

Lenders and borrowers can modify three terms in the initial contract in response to changes in renegotiation costs: maturity, covenants, and per-formance pricing provisions. The maturity of the loan contract is a major determinant of the likelihood of renegotiation. Short maturities help miti-gate the problems associated with incomplete contracting by making debt less sensitive to changes in firm value and by allowing for more frequent repricing of debt (Childs et al., 2005). Moreover, if debt matures before growth options are exercised, the firm’s opportunity to deviate from a value maximizing growth option exercise policy is eliminated (Myers, 1977). The benefits of shorter maturities, however, come with some costs. Short-term borrowers are exposed to liquidity risk, i.e. the possibility that the lender will not allow refinancing when needed (Diamond, 1991a, Childs et al., 2005). Issuing new debt also has fixed costs that are spread over longer periods when

long-term debt is issued. By reducing the costs associated with renegotia-tion while leaving liquidity risk and the costs of debt issuance unchanged, TD9599 makes short-term loans less appealing compared to long-term agree-ments with the possibility of renegotiation. Hence, we expect loan syndicates and their borrowers to agree on longer maturities in the post-TD9599 period. Financial covenants are often set tightly and used as “tripwires” to transfer control rights to the lender in situations where the borrower is more likely to misbehave (Smith Jr, 1993, Dichev and Skinner, 2002). The initial likelihood that covenants will be violated, triggering the reallocation of control rights, depends on the trade-off between the benefits of transferring control, and the cost of renegotiation (Garleanu and Zwiebel, 2009). We predict that loan syndicates and their borrowers will agree to covenants that are more likely to be violated after TD9599 reduces the tax burden of renegotiation.

The third feature of debt contracts that contracting parties can use to deal with the incompleteness of financial contracts is the use of performance pricing provisions (PPPs). PPPs link the interest rate spread of loan debt to the borrower’s performance. Interest-decreasing PPPs reduce the spread if credit quality improves. Interest-increasing PPPs increase spreads if credit quality deteriorates. As pointed out in Asquith et al. (2005), PPPs provide a way to explicitly model the change in loan cost associated with the arrival of new information or occurrence of unanticipated events, reducing the need for future renegotiation. Roberts (2015) partially challenges this view and shows that PPPs do not prevent renegotiation but only delay it. Whether PPPs are intended to delay or avoid renegotiation, a reduction in renegotiation costs reduces the benefits of PPPs, making the inclusion of these features in loan contracts less appealing. We predict that loan syndicates and their borrowers will use fewer PPPs after TD9599 adoption.

We estimate that the probability of violation for syndicated loans increases nine percentage points relative to non-syndicated loans. This change rep-resents a 20 percent increase with respect to the sample mean. Finally we observe that the use of PPPs in syndicated loan contracts declines twenty-five percent relative to single lender loans after TD9599, and, consistent with Asquith et al. (2005) this decline is confined to interest decreasing PPPs.

To test our prediction that the adoption of TD9599 makes private debt financing more attractive to firms in pursuit of capital we perform two tests. First, we study how the likelihood that a firm issues a loan versus a bond changes after TD9599. Using a linear probability model, we observe that the adoption of TD9599 increased the likelihood of issuing a loan versus a bond by about 3 percentage points. Second, we examine the financing behavior of U.S. and international firms in the pre and post TD9599 periods. We predict that firms impacted by TD9599 (U.S. firms) shift their debt structure away from bonds toward loans, relative to their international peers. We estimate the share of U.S. firms’ debt that is private debt (loans) to increase by 3 percentage points, while the share of U.S. firms’ debt that is public (bonds) falls by 4 percentage points. Both results are consistent with our conjecture that reduced renegotiation costs make private debt more attractive to prospective borrowers.

Overall, the paper contributes to the nascent literature on the effects of ex-post renegotiation considerations on ex-ante security design (Roberts and Sufi, 2009a, Armstrong et al., 2010, Christensen et al., 2016). Our findings are largely consistent with the predictions from the incomplete contracting the-ory. We highlight the important role played by renegotiation, which is seen as an out-of-equilibrium outcome in agency theory, for the efficient design of debt contracts. Our study also informs practice and policy. Contracting parties can focus on creating a set of covenants that give information about the state of the world rather than attempting to anticipate optimal invest-ment choices ex-ante. We additionally shows that policy-makers influence the way contracts are written when they change the relative attractiveness of the ex-ante allocation of cash flow rights versus the ex-post allocation of decision rights.

The remainder of the paper is organized as follows. Section 2 describes the identification and strategy and sample selection. Section 3 studies the rela-tionship between renegotiation costs and the initial terms in a debt contract. Section 4 studies how renegotiation costs shape the lender choice. Section 5 discusses the validity of the identification strategy. Section 6 concludes.

2. Identification Strategy

conclusions on the issue (Roberts, 2015). To answer the questions of interest in this paper, ideally we would need to identify a shock to renegotiation costs that possesses two characteristics:

• has no impact on the determinants of the initial terms in the contract

other than through renegotiation costs

• has a large enough impact on renegotiation costs to induce the

con-tracting parties to change the initial terms in the contract.

We argue that Internal Revenue Service Bulletin 2012-40: Property Traded on an Established Market (TD9599), which significantly modified the tax consequences of out-of-court debt restructuring faced by certain lenders, pos-sesses these characteristics. This section describes TD9599 and describes the various samples used in the paper.

2.1. TD9599

Significant out-of-court modifications of debt issues have tax consequences for both the borrower and the lender.1 The tax consequences of

restructur-ing depend on whether the debt instrument is qualified as publicly traded or private by the IRS.2 When the debt instrument is characterized as private,

the associated tax consequences are based on the difference between the face value of the “new” debt instrument and the face value of the pre-restructuring debt instrument. Given that in practice out-of-court restructuring rarely leads to changes in face value, the difference in face values between the new and old debt is usually zero. As a consequence, the borrower cannot rec-ognize any cancellation of debt income (CODI), which would increase its taxable income, nor be granted an equally-large tax credit associated with the original issue discount (OID). At the same time, the original lender fac-ing an economic loss cannot deduct the loss it for tax purposes because the issue price of the debt instrument does not change, while a secondary market

1

The regulation defines a modification to be significant when the issue’s principal, maturity, timing of interest payment, or yield (by more than 25 basis points) change. The evidence in Roberts and Sufi (2009b) suggests that renegotiations trigger modifications of the debt terms that would qualify as significant for tax purposes: renegotiations generate changes relative to the initial maturity, amount, and spread of the contract on the order of 64%, 43%, and 40%, respectively.

2

buyer pays taxes or receives a tax credit on the phantom gain/loss calculated as the difference between the original face value and the price paid on the secondary market.

When the debt instrument is instead characterized as publicly traded, the tax consequences of restructuring are based on the difference between the fair market value of the renegotiated debt and the debt’s original face value. The borrower recognizes CODI in an amount equal to the difference between the new issue price and the original face value, increasing its taxable income. However, the higher taxable income is likely to have no effect on the taxes paid by the borrower because (1) the borrower also benefits from OID of equal amount and (2) borrowers restructuring debt usually have very low marginal tax rates3

. From the original lender’s perspective, restructuring leads to the recognition of the economic loss for tax purposes, lowering taxable income4.

Secondary market buyers, instead, pay taxes or are granted a tax credit on the phantom gain/loss calculated as the difference between the fair market value of the new instrument, which is likely to be lower than the original face value, and the price they paid on the secondary market.

A consequence of the differential tax treatment of private and publicly traded debt instruments in out-of-court restructuring is that, while restruc-turing is at best tax-neutral for private debt instruments, it can lead to significant tax savings for the lenders and little to no additional taxes for the borrower when the debt instrument is qualified as public. Therefore, debt renegotiation is less costly when the debt instrument can be qualified as public.

The introduction of TD9599 by IRS on September 12, 2012 modified the tax consequences of out-of-court restructuring by changing the conditions a debt instruments must possess to qualify as publicly traded for renegotiation purposes. Before TD9599, a debt instrument qualified as publicly traded if (1) the issue was listed on a security exchange or traded in a market; (2) the issue’s price appeared in a quotation medium; or (3) a price quote could be obtained from dealers or traders. These conditions prevented all private loans from being classified as publicly traded. With TD9599 a fourth condition

3

Campello et al. (2016) finds that, in their sample, the marginal tax rate of distressed firms is about 4%.

4

was added: the availability of a “soft quote” from a broker, dealer, or pricing service suffices to qualify a debt instrument as public. This amendment opened the door for private loans traded in the secondary market to qualify as publicly traded for renegotiation purposes.

As described in Campello et al. (2016), a large number of syndicated loans were reclassified from private to public debt, while single-lender loans were left untouched. Moreover, listed bonds continued qualifying as public instru-ments and their tax treatment did not change with TD9599. We exploit this asymmetric effect of TD9599 on syndicated loans, single lender loans, and public bonds to study how changes in renegotiation costs affect the initial terms in the contract. Specifically, we use a difference in differences frame-work to investigate how initial contract terms of syndicated loans changed after TD9599, using single-lender loans and public bonds (when possible) as control samples.

The shock to renegotiation costs associated with TD9599 seems to broadly meet the two conditions listed at the beginning of the section. On the one hand, variation in renegotiation costs introduced by TD9599 appears exoge-nous to the other determinants of ex-ante security design. For example, there are no obvious reasons why TD9599 would impact information asymmetry between the borrower and the lender differently for syndicated and single lender loans. It is then difficult to envision reasons why TD9599 would change the average adverse selection problem faced by lenders in the private debt market. Furthermore, the absolute costs of monitoring faced by lenders to prevent moral hazard on the borrower’s side should also be unaffected by TD9599, reducing the likelihood that observed modifications to the ini-tial terms of the contracts are driven by changes in the underlying agency problem that are specific to syndicated loans. On the other hand, the ef-fect of TD9599 on renegotiation costs appears to be economically important: Campello et al. (2016) estimate that the aggregate reduction in expected renegotiation costs to affected loans amounts to approximately $100 billion.

2.2. Sample Description

TD9599 adopted, and provides us with four pre-adoption calendar years and four post adoption calendar years. We aggregate loan-facility level data to the loan-package level for our maturity and covenant analyses, while facility-level data is used in the case of performance pricing provisions.

We obtain data on borrower fundamentals from Compustat. Tradition-ally papers in this area have relied on the link table created by Sudheer Chava and Micheal Roberts (Chava and Roberts, 2008) which is distributed by the Wharton Research Data System. This link table, however, ends in 2012, the year that TD9599 is enacted. We extend the Chava and Roberts link table to 2016 with a three step algorithm. First, we search Compustat for GVKEYs identified by Chava and Roberts that remain active. Second, we use a Python token-matching script to identify candidate matches based on bor-rower names as reported in DealScan and Compustat. This matching script produces a confidence statistic, which we use to tag suspect matches. Finally , we verify by hand the suspect matches to create a DealScan-Compustat link that is active through our entire sample period. This link table is available upon request.

The purpose of linking firm fundamentals from Compustat with loan data from DealScan is to control for the attributes of the company at the time the loan is negotiated. In practice making this link requires assumptions about the negotiation process. Following Murfin (2012), we report the con-tracting date of a loan as 90 days prior to the DealScan reported date, i.e. one month prior to receiving a mandate and two months in the syn-dication/documentation process. After linking DealScan and Compustat we require that the loan package report covenant data, and non-missing val-ues for Compustat controls capital expenditure (CAPEX), leverage (LEV), market-to-book ratio (MTB), return on assets (ROA), size (SIZE), tangibility (TANG), and Z-score (ZSCORE). All variables are defined in Appendix B. The final DealScan sample includes 3,764 loan packages, of which 3,371 are syndicated and 393 are single-lender, and 2,573 bonds. Descriptive statistics, reported in Table 1 Panel A, are generally consistent with prior literature.

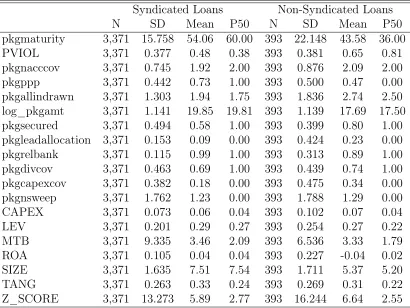

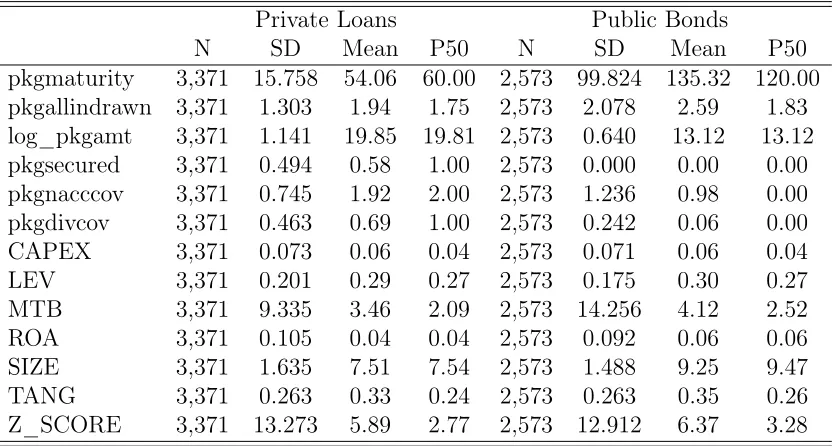

levered, have lower market-to-book, and lower ROA. Table 1 Panel C reports a similar comparison of the syndicated loan sub-sample, but with our second control group: public debt. Bonds and loans have somewhat different ini-tial characteristics: loans have lower iniini-tial maturity, and lower spreads, and a higher number of covenants. Bond firms are similar to loan firms, indeed many firms issue both types of debt, though bond firms tend to be somewhat larger on average.

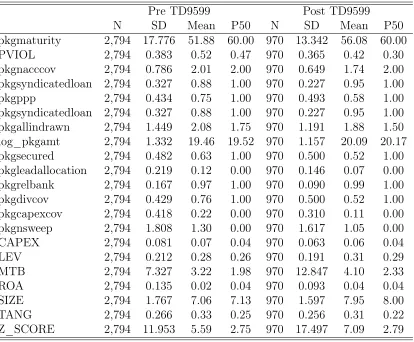

For reference, Table 1 Panel D splits the syndicated/single-lender loan sample into pre- and post- TD9599 sub-samples. Similar to the evidence provided in Campello et al. (2016), single-lender loans become less common and the concentration of the loan syndicate decreases (i.e. the lead arranger is allocated a lower proportion of the loan). At the same time, the use of covenants of all type (negative or financial), performance pricing provi-sions, and sweeps decreases. Table 1 Panel E presents pre- and post-TD9599 descriptives for each of the syndicated and single-lender loan sub-samples. Our main analyses investigate the differences across sub-samples in these changes from the pre-TD9599 period to post-TD9599 period. Similarly Ta-ble 1 Panel E presents pre- and post-TD9599 descriptives, but this time for each of the public and private debt sub-samples. Our main analyses inves-tigate the differences in maturity across sub-samples in these changes from the pre-TD9599 period to post-TD9599 period.

To test our hypothesis that TD9599 makes loans more attractive relative to bonds, we collect capital structure and firm headquarter data from Capi-talIQ. Table 2 Panel A reports descriptive statistics for the resulting dataset. Table 2 Panel B compares U.S. firms to non-U.S. firms. U.S. firms appear to frequent bond markets slightly more than their non-U.S. counterparts, issue more secured debt, and be less leveraged (DEBTEBITDA). Table 2 Panel D presents pre- and post-TD9599 descriptives for each of the U.S. and non-U.S. loan sub-samples. We use these sub-samples in our lender choice analysis.

3. Ex-ante Security Design

contract are adjusted as renegotiation cost decreases with TD9599: debt ma-turity increases and so does the initial likelihood of covenant violation, while the inclusion of performance pricing provisions declines.

3.1. Debt Maturity

The maturity of a debt contract is one of the attributes of debt in a firm’s capital structure that the contracting parties can use to design an efficient contract. Research on debt maturity dates back to Jensen and Meckling (1976) and Myers (1977). Jensen and Meckling (1976) describe the incen-tive that shareholders face to increase the riskiness of the firm after a debt contract has been signed. Myers (1977) shows how introducing debt into a firm’s capital structure may lead to debt overhang, i.e. the possibility that the firm rejects profitable investment opportunities because part of their net present values accrues to debtholders, while the associated costs are faced by shareholders. In both cases, a possible solution is represented by short debt maturity: if debt matures before the investment opportunity expires, contracting parties can reprice it in an efficient way Myers (1977).

The short-term maturity solution, however, does not come for free (Dia-mond and He, 2014). It is possible to identify two costs to short maturities: liquidity risk and roll-over costs. Liquidity risk represents the possibility that the lender will not allow refinancing when needed (Diamond, 1991a, Childs et al., 2005). If the firm needs to renew its short-term debt after a negative signal, it is possible that the debtholder will force an inefficient liq-uidation. Roll-over costs represent the fixed costs that must be borne when issuing debt. Since short-term debt involves more frequent renewal, it also translates into higher fixed costs.

Shortening debt maturity can represent a valuable instrument in deal-ing with the incompleteness of contracts as well. When the initial contract is incomplete, the parties are exposed to the risk that the arrival of new information makes the initial terms agreed upon inefficient, forcing a rene-gotiation5. Provided that renegotiation is not costless, the borrower and the

lender may prefer a shorter maturity that makes debt less sensitive to changes in firm value and allows for more frequent repricing of debt without having to incur renegotiation costs (Childs et al., 2005).

5

Overall, the choice between short maturity and long maturity with more likely renegotiation weights the benefits and costs of each solution, including renegotiation costs. Since TD9599 reduces renegotiation costs while leaving the other benefits and costs unchanged, it should shift the equilibrium to-ward longer maturity syndicated loans when compared to unaffected debt contracts. Therefore, we make the following conjecture.

H1a: Syndicated loan maturity increases after the adoption of TD9599

We test our conjecture using a difference-in-differences framework that com-pares the maturity of treated (i.e. syndicated loans) versus untreated (i.e. single lender loans and public bonds) debt contracts in the pre and post TD9599 adoption period. The use of two different control groups serves the purpose of reducing concerns over the possible endogenous differences exist-ing between treated and control observations. For example, syndicated loans and single lender loans differ significantly in terms of size, but are similar with respect to the number of contracting solutions that can be adopted. On the other hand, syndicated loans and bonds are closer in size, but do not share the same array of contracting features.

We use the following regression specification to test our conjecture:

M aturity = ↵+β1T reated+β2T Dad+β3T reated∗T Dad+

X

γControls

+XδControls∗T Dad+IndustryF E+RatingF E+✏ (1)

Maturity represents the maturity of the debt instrument in months. Treated represents two alternative variables: (1)pkgsyndicatedloan, an indicator vari-able equal to 1 if the observation is a syndicated loan, 0 if the observation is a single lender loan; or (2) LOAN, an indicator variable equal to 1 if the observation is a syndicated loan, 0 if the observation is a public bond. TDad is an indicator variable equal to 1 in the post-TD9599 adoption period (i.e. after September 2012), and equal to 0 in the pre-TD9599 adoption period. This specification includes a wide array of loan-controls6: pkgallindrawn, the

debt contract spread; log_pkgamt, the natural logarithm of the amount is-sued; pkgsecured, an indicator variable equal to 1 if the loan is secured, and 0 otherwise; pkgleadallocation, a variable describing how much of the loan

6

amount is allocated to the lead arranger; pkgrelbank, an indicator variable equal to 1 if the lead arranger has arranged at least one loan for the borrower in the previous three years, and 0 otherwise; pkgppp, an indicator variable equal to 1 if the loan has a performance pricing provision, and 0 otherwise; pkgnacccov,a variable counting the number of financial covenants included in the loan agreement; pkgdivcov, an indicator equal to 1 if the loan agreement includes a dividend covenant, and 0 otherwise;pkgcapexcov,an indicator vari-able equal to 1 if the loan agreement includes an investment covenant, and 0 otherwise; pkgnsweep, a count variable identifying the number of sweeps included in the loan agreement. The specification also includes borrower-specific controls: CAPEX, computed as capital expenditures scaled by total assets; LEV, calculated as short and long term debt over total assets;MTB, defined as the market value of equity over its book value; ROA, computed as net income over total assets;SIZE,the natural logarithm of the market value of equity; TANG, defined as the ratio of property, plans, and equipment over total assets; and Z_SCORE, calculated as in Altman (1968). We finally in-clude industry and rating fixed effects, while standard errors are clustered at borrower and year level.

The coefficient of interest is represented by β3, which describes how the difference in loan maturity between the treated and control groups changes after the adoption of TD9599.

Table 3, Panel A reports results from estimating equation 1 with single-lender loans as the untreated group. Results confirm our conjecture and consistently show that maturity increased in the post-TD9599 period: the coefficient of interest is in all cases statistically significant (at the 5% or 1% level). Moreover, the magnitude of the coefficient is also economically meaningful, with the difference in maturity between syndicated loans and single lender loans increasing by about 12 months, a 23 percentage points increase when compared to the sample mean.

Table 3, Panel B reports results from estimating equation 1 with public bonds as the untreated group. In this case results are less strong but in-dicative that the maturity of syndicated loans increases more than that of public bonds after TD9599 is adopted. The coefficient of interest is positive and statistically significant at the 1% level when the whole set of controls and interactions is included. The magnitude suggests that the maturity of syndicated loans decreases by about 50 percentage points when compared to the sample mean, or approximately 90 months.

in-complete contracting theory, lower renegotiation costs increase the equilib-rium debt contract maturity.

We also assess whether borrowers and lenders respond to the announce-ment of TD9599 by adjusting the initial terms in the contract. The retroac-tive nature of TD9599 makes the regulation apply to loans issued before the adoption date as well. However, the response at announcement depends on the beliefs that the contracting parties have about the likelihood that the regulation will be adopted and the time to adoption. If borrowers and lenders believe that adoption is rather likely and the need for renegotiation will occur after the adoption date, then they will start adjusting the equi-librium contracting maturity after the announcement of TD9599. Therefore, we conjecture the following:

H1b: Syndicated loan maturity increases after the announcement of TD9599

We use the following regression specification to test our conjecture:

M aturity = ↵+β1T reated+β2T Dan+β3T reated∗T Dan+

X

γControls

+XδControls∗T Dad+IndustryF E+RatingF E+✏ (2)

The only difference with equation 1 is the variable TDan. TDan is an indicator variable equal to 1 in the post-TD9599 announcement period (i.e. after January 2011), and equal to 0 in the pre-TD9599 announcement period. Table 3, Panel C reports results from estimating equation 2 with single-lender loans as the untreated group. Results are weakly in support of our con-jecture: the coefficient of interest is positive but only marginally statistically significant (at the 10% level) when the full set of controls and interactions is considered.

Table 3, Panel D reports results from estimating equation 2 with public bonds as the untreated group. Results are in this case strongly in support of the conjecture that the maturity of syndicated loans increase more than that of public bonds in the post-TD9599 announcement period: the coefficient is not only positive and highly statistically significant (at the 1% level), but also economically meaningful.

3.2. Initial Likelihood of Covenant Violation

Maturity is not the only tool that the borrower and the lender can use to deal with the incompleteness of contracts. A second aspect that can be adjusted is covenants, and in particular by the likelihood that a covenant will be violated during the debt contract maturity. Financial covenants are often set tightly and used as “tripwires” to give lenders control rights in situations where the borrowers are more likely to misbehave (Smith Jr, 1993, Dichev and Skinner, 2002). As discussed in Garleanu and Zwiebel (2009), the probability of violation set at inception depends on the ease of renegotiation and on the dead-weight losses that the renegotiation process involves. If these costs decrease, then the equilibrium initial probability of covenant violation should increase.

Two papers that we are aware of study the implications of future renegoti-ations for ex-ante covenant design. Saavedra (2015) shows that coordination costs in the renegotiation process, as proxied by the number of lenders in the syndicate, affect the inclusion of covenants that restrict the borrower’s financial flexibility in the debt contract. Shan et al. (2015) use the advent of Credit Default Swaps as a laboratory to study the implications of ex-post renegotiation for ex-ante security design, under the assumption that the in-troduction of CDSs reduces the importance of control rights to debtholders and should therefore make tight covenants less desirable. Their results are consistent with their prediction and show that covenants loosen after CDS on the borrowing firm become available. Our paper differs from Saavedra (2015) and Shan et al. (2015) in that we focus on a different renegotiation consideration, the tax cost of renegotiation. While a change in coordination costs or the need for renegotiations change the underlying economics of debt financing, our tax setting does not impact the underlying economics of the debt. In our setting, TD9599 only reduces renegotiation costs for certain type of debt contracts. As a consequence, we expect affected debt contracts to set a higher probability of violation implicit in the initial contract in the post TD9599 period. Our conjecture is expressed as follows:

H2a: The initial likelihood of covenant violation implicit in syndicated loan contracts increases after the adoption of TD9599

pre-and post-TD9599 adoption period. Lack of details on the initial covenant thresholds prevents us from using public bonds as control group. For this reason, we try to reduce concerns over the validity of the analysis using two different measures for the initial probability of covenant violation in the loan sample.

The regression specification employed to test H2a is defined as follows:

P V = ↵+β1pkgsyndicatedloan+β2T Dad+β3pkgsyndicatedloan∗T Dad+

X

γControls+XδControls∗T Dad+IndustryF E+RatingF E+(3)✏

PV represents a proxy for the initial probability of violation implicit in the debt contract. We measure PV in two ways. The first proxy (PVIOL) comes from Demerjian and Owens (2015). We follow their methodology and estimate the likelihood that at least one covenant in the loan contract will be violated during the first year after the loan is initiated. This proxy has the advantage of capturing the various determinants of covenant violation, i.e. the number of covenants, the initial distance from the performance thresh-old, the volatility in the underlying performance metric, and the covariance between the various performance metrics included. The second proxy (pkg-nacccov) is defined as the number of financial covenants included in the loan agreement. This proxy considers only the number of covenants agreed upon, and it is therefore expected to capture the underlying construct of interest, i.e. the initial likelihood of covenant violation, with error, reducing the power of the tests (Demerjian and Owens, 2015). Pkgsyndicatedloan represents an indicator variable equal to 1 if the observation is a syndicated loan, and equal to 0 if it represents is a single lender loan. TDad is an indicator variable equal to 1 in the post-TD9599 adoption period (i.e. after September 2012), and equal to 0 in the pre-TD9599 adoption period. The specification includes the same set of loan-controls and borrower-specific controls included in equation 1, with the only difference being the exclusion of the number of financial covenants and the inclusion of pkgmaturity, i.e. the loan maturity measured in months. Standard errors are clustered at borrower and year level.

The coefficient of interest is represented by β3, which describes how the difference in the initial likelihood of covenant violation between the treated and control groups changes after the adoption of TD9599.

Results fully support our conjecture when PVIOL is used: the coefficient of interest is positive and statistically significant at the 1% level. The coeffi-cient is also economically important: when the whole battery of controls is considered, for example, the coefficient is 0.09, representing a 9 percentage point change when compared to the sample mean. Evidence is instead weaker when pkgnacccov is used, with the coefficient of interest being positive but marginally insignificant (p-value of 0.115) when the whole set of controls is included.

Results are overall in support of renegotiation costs influencing the initial likelihood of covenant violation, as predicted in Garleanu and Zwiebel (2009). As for maturity, we additionally assess whether borrowers and lenders respond to the announcement of TD9599 by adjusting the initial terms in the contract. We test the following conjecture:

H2b: The initial likelihood of covenant violation implicit in syndicated loan contracts increases after the announcement of TD9599

using the following regression specification:

P V = ↵+β1pkgsyndicatedloan+β2T Dan+β3pkgsyndicatedloan∗T Dan+

X

γControls+XδControls∗T Dan+

IndustryF E+RatingF E +✏ (4)

The only difference with equation 3 lies inTDan, which in this case splits the sample in the post-TD9599 announcement period (i.e. after January 2011) and pre-TD9599 announcement period.

Results forPVIOLare reported in Table 4, Panel C, while Table 4, Panel D shows results for pkgnacccov. As in the maturity analysis, borrowers and lenders seem to respond to the TD9599 announcement by adjusting the terms in the contract. Specifically, we observe a larger positive change in the ini-tial likelihood of covenant violation for the treated group when compared to the untreated group, consistent with our conjecture. The coefficient of interest is positive but not statistically different from zero when the number of covenants is considered, which may be a reflection of the highest measure-ment error that characterizes this analysis.

3.3. Performance Pricing Provisions

(PPPs). Performance pricing provisions are contractual agreements that de-scribe at loan inception how the interest charged will be adjusted as a func-tion of either some financial performance metric or the credit rating of the borrower (Asquith et al., 2005, Manso et al., 2010). This feature makes performance pricing provisions particularly well suited to deal with the im-possibility of writing complete contracts.7

Instead of having to rely on costly renegotiation if/when new information makes the initial terms in the contract inefficient, the parties can agree on how the interest rate charged changes as a function of the borrower’s performance and riskiness. Performance pricing provisions, however, are not costless. PPPs may represent only a partial solution to the incompleteness of contracts. While the grid agreed upon at inception may be correct on average, it is possible that unexpected changes in the borrower’s economic condition lead to the need for renegotiation. In support of this possibility, Roberts (2015) shows that PPPs do not prevent renegotiation, but merely delay it. Since setting up the initial grid involves costs, the contracting parties will trade-off these costs with the benefits of preventing or delaying renegotiation. If TD9599 reduces the costs of renego-tiation while leaving the costs and benefits of PPPs unchanged, as we con-jecture, then the use of PPPs in debt instruments affected by the regulation should become less prevalent. Hence, we make the following prediction:

H3a: The likelihood that a PPP is included in a syndicated loan contracts decreases after the adoption of TD9599

We test our prediction using the following linear probability model, run over a sample of loans evaluated at facility level:

P P P = ↵+β1pkgsyndicatedloan+β2T Dad+β3pkgsyndicatedloan∗T Dad+

X

γControls+XδControls∗T Dad+

IndustryF E+RatingF E+✏ (5)

PPP is an indicator variable equal to 1 if the loan facility includes a performance pricing provision, 0 otherwise. The specification includes the same controls considered in previous tests, expanded to include additional

7

determinants of PPPs identified in Asquith et al. (2005): PROB_PREPAY, constructed from five years of historical data collected by Moody’s in an aver-age rating transition matrix (2008) as the sum of the probability of a credit upgrade and the probability that the debt is withdrawn; PROB_DOWN, constructed as the probability that the borrower’s credit quality will decline but not default using Moody’s rating transition matrix (2008); forecaster-ror_qtr, calculated as the ratio of the mean earnings-per-share forecast error of forecasts made in the quarter proceeding origination to the firms actual earnings per share; VolCreditSpread, calculated as the annual variance of spreads for a given risk class for firms included in DealScan; MoralHazard, estimated using the two step process employed in Asquith et al. (2005, p. 116); ExpVolRet, defined as the average standard deviation of return for the firm’s industry measured at the SIC two-digit level in the year prior to loan initiation, multiplied by loan maturity;Predictability,calculated as described in Asquith et al. (2005, p. 115); Revolver, an indicator variable equal to 1 if the loan is revolving, and 0 otherwise; and TakeOver, an indicator variable equal to 1 if the loan is used for a merger or acquisition, and 0 otherwise.

The coefficient of interest is represented by β3, which describes how the difference in the likelihood that a PPP is included in the loan agreement between the treated and control groups changes after the adoption of TD9599. Table 5, Panel A reports the coefficients resulting from estimating equa-tion 5. In all cases, the coefficient of interest is negative and statistically significant at the 1% level, consistent with our conjecture. The coefficient is economically large too, representing a reduction in the use of PPPs of twenty to forty-seven percent when relative to forty-four percent frequency of PPP use in the sample.

con-tracting theory is correct, and renegotiation costs influence initial terms of the contract, then we would expect TD9599 to reduce the use of interest-decreasing PPPs only. Therefore, we hypothesize that:

H3b: The likelihood that an interest-decreasing PPP is included in a syndi-cated loan contracts decreases after the adoption of TD9599

H3c: The likelihood that an interest-increasing PPP is included in a syndi-cated loan contracts does not change with the adoption of TD9599

We test our conjectures through the following linear probability model:

P P P Incr(P P P Decr) = ↵+β1pkgsyndicatedloan+β2T Dad+

β3pkgsyndicatedloan∗T Dad+

X

γControls+ X

δControls∗T Dad+IndustryF E+RatingF E+(6)✏

PPPIncr is an indicator variable that takes the value of 1 if an interest-increasing performance pricing provision is included in the loan facility, and 0 otherwise, while PPPDecr is an indicator variable that takes the value of 1 if an interest-decreasing performance pricing provision is included in the loan facility, and 0 otherwise. We include PPPDecr as a control when using PPPIncr as dependent variable, and vice versa, to account for the fact that, once the borrower agrees to include one form of performance pricing provi-sion, the cost to include the other performance pricing provision is reduced. The coefficient of interest is represented by β3, which describes how the difference in the likelihood that an interest-increasing (interest-decreasing) PPP is included in the loan agreement between the treated and control groups changes after the adoption of TD9599, controlling for the likelihood that an interest-decreasing (interest-increasing) PPP is also included.

Table 5, Panels B and C report the coefficients from estimating equation 6. Results are mostly consistent with our conjecture: while the coefficient of interest is never statistically different from zero when PPPIncr is used as dependent variable (Panel B), it turns negative and statistically significant at the 5% in two specifications when PPPDecr is considered (Panel C).

As in the case of maturity and the initial likelihood of covenant violation, we also assess whether the borrower and the lender modify their use of per-formance pricing provisions after the announcement of TD9599. We test the following conjectures:

H3d: The likelihood that a PPP is included in a syndicated loan contracts decreases after the announcement of TD9599

H3e: The likelihood that an interest-decreasing PPP is included in a syndi-cated loan contracts decreases after the announcement of TD9599

H3f: The likelihood that an interest-increasing PPP is included in a syndi-cated loan contracts does not change with the announcement of TD9599

using the following linear probability model:

P P P (P P P Incr, P P P Decr) = ↵+β1pkgsyndicatedloan+β2T Dan+

β3pkgsyndicatedloan∗T Dan+

X

γControls+XδControls∗T Dan+

IndustryF E+RatingF E +✏ (7)

where variables are defined as in the previous analyses.

Table 5, Panel D shows the results whenPPP is considered, while Table 5, Panels E and F concern PPPIncr and PPPDecr, respectively. Results are consistent with the previous sections in that the borrower and the lender appear to adjust their behavior at TD9599 announcement: the likelihood that a performance pricing provision is included in a loan contract decreases after the adoption of TD9599, and the effect is concentrated among interest-decreasing performance pricing provisions.

4. Lender Choice

loans. A second consequence may be a shift in the equilibrium debt structure of borrowers away from public bonds and towards private loans.

The choice between public and private lenders has been investigated both theoretically (Diamond, 1991b, Rajan, 1992, Chemmanur and Fulghieri, 1994, Hackbarth et al., 2007, Morellec et al., 2014) and empirically (Bharath et al., 2008, Denis and Mihov, 2003). This choice matters because of the institutional differences that characterize the two types of lenders. First off, banks and bondholders differ in their access to private information: while banks have access to private information both before granting a loan and during the loan term, bondholders make their decisions based on publicly available information.

Second, private lenders have a better ability to monitor the borrower because of the lower number of participants. The ownership of bondhold-ers is usually widely spread, making coordination for monitoring purposes extremely challenging. On the contrary, the ownership of syndicated loans is usually concentrated on a limited number of lenders, with one of these lenders coordinating the activity of the participants.

A third difference consists in the flexibility and costs of renegotiating the terms in the contract. Bonds are not flexible. The large number of bondholders makes coordination difficult, the Trust Indenture Act of 1939 – requiring unanimous consent – makes material modifications to the bond contract all but impossible. On the cost side, in the pre-TD9599 period renegotiation of private debt faced a larger tax burden than renegotiation of public debt. With adoption of TD9599 the tax disadvantage of syndicated private debt is eliminated. If the difference in taxation associated with rene-gotiations represents a driver in the choice between private and public debt and TD9599 did not affect other differences between public and private debt other than renegotiation costs, the adoption of TD9599 is expected to make the choice of private loans relatively more attractive, causing a shift in the capital structure, and in particular in the debt composition, of borrowing firms. Therefore, we hypothesize the following:

H4: The adoption of TD9599 causes borrowers to shift their preference away from public bonds and toward private loans

Overall, we find that borrowers behave consistently with our predictions: the bond versus loan test shows that the likelihood of issuing loans over bonds increases in the post TD9599 adoption period, while the debt composition test shows that U.S. firms (i.e. treated firms) increase the weight of loans and decrease the weight of bonds more than their international peers (i.e. untreated firms) in the post TD9599 adoption period. Both results point at borrowers shifting toward private loans as renegotiation costs decrease.

4.1. Bond versus Loans

In this section, we study how the likelihood that a firm issues a loan versus a bond changes with the adoption of TD9599. We test the choice between loans and bonds using the following linear probability model:

LOAN = ↵+β1T Dad+β2AQ+β3LEV +β4M T B

+β5SIZE +β6T AN G+β7ZSCORE+

+IndustryF E+RatingF E+Y earF E+✏ (8)

LOAN is an indicator variable equal to 1 if the borrower issues a loan, and equal to 0 if the borrower issues a bond. TDad is an indicator variable equal to 1 in the post-TD9599 adoption period (i.e. after September 2012), and equal to 0 in the pre-TD9599 adoption period. AQ represents discre-tionary accruals. The variable is multiplied by negative 1 to be consistent with the way accounting quality is defined in Bharath et al. (2008); LEV is calculated as short and long term debt over total assets; MTB is defined as the market value of equity over its book value; SIZE is the natural log-arithm of the market value of equity; TANG is the ratio of property, plans, and equipment over total assets; Z_SCORE is defined as in Altman (1968). The specification also includes industry, rating, and year fixed effects, while standard errors are clustered at borrower and year level.The coefficient of interest is β1, which describes how the likelihood of choosing a loan over a bond changes after the adoption of TD9599.

The model is estimated over the whole sample and over a sub-sample that includes only firms existing in both the pre and post TD9599 period, used in order to reduce concerns over the possibility that results are driven by banks expanding their credit supply to the marginal borrower.

(columns 3 and 4). The coefficient of interest is in all cases positive and statistically significant at the 1% level, as expected, and suggests that the likelihood of choosing a loan over a bond increases by about 3 percentage points in the post-TD9599 period.

4.2. Capital Structure Composition

In this section, we test whether H4 holds true in the data by examining the debt structure of U.S. and international firms in the pre and post TD9599 periods. This sample enables us to observe whether the capital structure of U.S. firms, i.e. treated firms, shifted toward loans when compared to the cap-ital structure of untreated firms, i.e. international firms, after the adoption of TD9599. We test our conjecture through the following regressions:

%Loans = ↵+β1T Dad+β2U S∗T Dad+

+XγControls+XδControls∗T Dan+

+BorrowerF E+CountryF E+✏ (9)

%Bonds = ↵+β1T Dad+β2U S∗T Dad+

+XγControls+XδControls∗T Dan+

+BorrowerF E+CountryF E+✏ (10)

%Loans is calculated as outstanding loans over total debt, while%Bonds represents outstanding bonds over total debt. Both equations include the fol-lowing controls: SECUREDPCT, the percentage of debt secured; SENIOR-PCT,the percent of debt that is senior;REVOLVINGPCT,the percentage of debt that is revolving; andDEBTEBITDA, the debt to ebitda ratio that the firm achieved during the fiscal year. The specification also includes borrower and country fixed effects, while standard errors are clustered at borrower and year level.

decrease the weight of bonds in their debt structure more than their inter-national counter-parties in the post-TD9599.

Table 6, Panel B reports results from estimating equation 9. Results are consistent with the expectation in that the coefficient of interest is pos-itive and statistically significant at the 10% or 5% level. The magnitude of the coefficient suggests that the difference between the percentage of loans composing U.S. and international firms’ debt structure increases in the post period by about 0.03, an 8.7% increase with respect to the sample mean.

Table 6, Panel C reports results from estimating equation 10. Results are again consistent with expectation: in this case, the coefficient of interest is negative and statistically significant at the 5% level. The magnitude of the coefficient suggests that the difference between the percentage of bonds composing U.S. and international firms’ debt structure decreases in the post period by about 0.05, an 8.2% decrease with respect to the sample mean.

5. Validity of the Identification Strategy

5.1. Parallel Trend Assumption

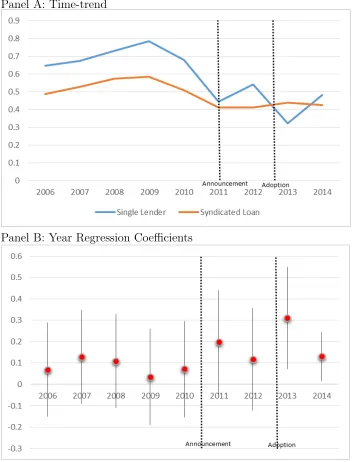

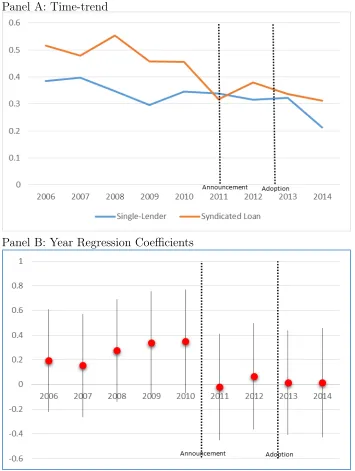

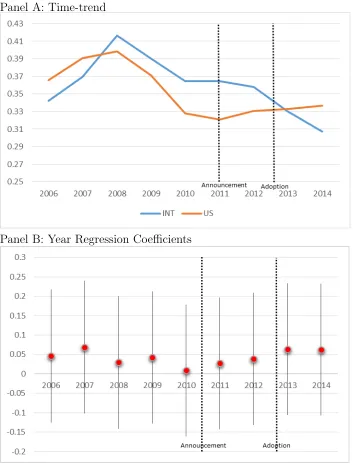

Our identification strategy leans heavily on the assumption that syndi-cated loans would have had parallel trends in initial contract terms to bonds and single lender loans had TD9599 not been announced and adopted in 2012. We verify the validity of the parallel trend assumption in two ways. First, we plot the time trend in maturity, initial likelihood of covenant vio-lation, and performance pricing provisions separately for the treatment and control group over time. This test enables us to sense whether the variable of interest is moving similarly in the two samples. However, this methodology does not account for potential changes over time in other determinants of the initial terms in the contract. For this reason, we also follow CHRISTENSEN et al. (2015) and examine pre-TD9599 trends in maturity, probability of vi-olation, and performance pricing provisions by testing for treatment effects in each of our sample periods. We repeat our linear regression analysis with controls, industry, and rating fixed effects, but instead of estimating an ag-gregate treatment effect for the post period we estimate an annual treatment effect relative to the benchmark year of 2005.

these plots does not reveal any discernible treatment effect in the direction of our hypotheses until after announcement of TD9599.

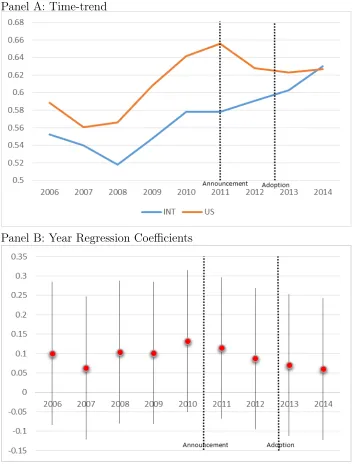

We repeat the same analysis to assess the validity of using international firms as control group in the capital structure tests. Figure 4 reports the graphs when %Loans is considered, while figure 5 uses %Bonds. Visual in-spection of the graphs confirm that the two samples follow a similar trend in the pre-TD9599 period.

Hence, we conclude that the parallel trend assumption holds true in the data, and that our empirical approach does not suffer from major econometric problems.

5.2. Placebo Test

To further support the validity of our empirical approach we supplement the parallel trend assumption analysis with a placebo that attempts to repli-cate the main findings using a randomly selected adoption date in the pre-TD9599 adoption period.

The process works as follows. First, we assign a random adoption date. Second, we we run the regression specification using the newly created adop-tion date and the associated interacadop-tions. Third, we save the coefficient on the difference-in-differences estimator and associated standard error. Fourth, we replicate the process fifty times. Finally, we then analyze how often in these fifty replications the estimated coefficient is consistent with our hypotheses. Failing to find placebo tests consistent with our hypotheses supports the argument that the parallel trends assumption holds in the data.

6. Conclusion

Debt contracting provides a rich laboratory in which to study contract-ing theory, and at the same time are economically important in their own right. However, debt contracts regulate complex systems and are simulta-neously shaped by incomplete information, monitoring costs, renegotiation costs, and macroeconomic conditions. We use adoption of TD-9599 to inves-tigate the relationship between renegotiation costs and initial contract terms predicted by the incomplete contracting theory. In this setting we are able to both characterize the relationship between renegotiation costs and ini-tial debt contract terms and show that renegotiation costs affect the choice between public and private debt.

Our tests show that lower renegotiation costs translate into longer debt maturity, higher initial likelihood of covenant violation, and lower frequency in the use of performance pricing provisions. There results are consistent with the incomplete contracting theory and show that ex-post renegotiation considerations determine the initial terms in the debt contract. These results also rationalize the tension between debt contract complexity, suggestive of complete contracting, and frequent renegotiations, suggestive of incomplete contracting. We also find that TD9599 makes borrowers shift their preference toward private loans and away from bonds.

References

Edward I Altman. Financial ratios, discriminant analysis and the prediction of corporate bankruptcy. The journal of finance, 23(4):589–609, 1968.

Christopher S Armstrong, Wayne R Guay, and Joseph P Weber. The role of information and financial reporting in corporate governance and debt contracting. Journal of Accounting and Economics, 50(2):179–234, 2010.

Paul Asquith, Anne Beatty, and Joseph Weber. Performance pricing in bank debt contracts. Journal of Accounting and Economics, 40(1):101– 128, 2005.

Sreedhar T Bharath, Jayanthi Sunder, and Shyam V Sunder. Accounting quality and debt contracting. The Accounting Review, 83(1):1–28, 2008.

Murillo Campello, Tomislav Ladika, and Rafael Matta. Debt restructuring costs and corporate bankruptcy: Evidence from cds spreads. Available at SSRN 2586176, 2016.

Sudheer Chava and Michael R Roberts. How does financing impact invest-ment? the role of debt covenants. The Journal of Finance, 63(5):2085– 2121, 2008.

Thomas J Chemmanur and Paolo Fulghieri. Reputation, renegotiation, and the choice between bank loans and publicly traded debt. Review of Finan-cial Studies, 7(3):475–506, 1994.

Paul D Childs, David C Mauer, and Steven H Ott. Interactions of corporate financing and investment decisions: The effects of agency conflicts.Journal of financial economics, 76(3):667–690, 2005.

HANS B CHRISTENSEN, ERIC FLOYD, L Yao Liu, and MARK MAF-FETT. The real effects of mandatory non-financial disclosures in financial statements. Technical report, Working paper, 2015.

Hans B Christensen, Valeri V Nikolaev, and Regina Wittenberg-Moerman. Accounting information in financial contracting: The incomplete contract theory perspective. Journal of Accounting Research, 54(2):397–435, 2016.

Peter R Demerjian and Edward L Owens. Measuring the probability of fi-nancial covenant violation in private debt contracts.Journal of Accounting and Economics, 2015.

David J Denis and Vassil T Mihov. The choice among bank debt, non-bank private debt, and public debt: evidence from new corporate borrowings. Journal of financial Economics, 70(1):3–28, 2003.

David J Denis and Jing Wang. Debt covenant renegotiations and creditor control rights. Journal of Financial Economics, 113(3):348–367, 2014.

Douglas W Diamond. Debt maturity structure and liquidity risk. The Quar-terly Journal of Economics, 106(3):709–737, 1991a.

Douglas W Diamond. Monitoring and reputation: The choice between bank loans and directly placed debt. Journal of political Economy, 99(4):689– 721, 1991b.

Douglas W Diamond and Zhiguo He. A theory of debt maturity: the long and short of debt overhang. The Journal of Finance, 69(2):719–762, 2014.

Ilia D Dichev and Douglas J Skinner. Large–sample evidence on the debt covenant hypothesis. Journal of accounting research, 40(4):1091–1123, 2002.

Nicolae Garleanu and Jeffrey Zwiebel. Design and renegotiation of debt covenants. Review of Financial Studies, 22(2):749–781, 2009.

Stuart C Gilson. Transactions costs and capital structure choice: Evidence from financially distressed firms. The Journal of Finance, 52(1):161–196, 1997.

Sanford J Grossman and Oliver D Hart. The costs and benefits of owner-ship: A theory of vertical and lateral integration. The Journal of Political Economy, pages 691–719, 1986.

Dirk Hackbarth, Christopher A Hennessy, and Hayne E Leland. Can the trade-off theory explain debt structure? Review of Financial Studies, 20 (5):1389–1428, 2007.

Michael C Jensen and William H Meckling. Theory of the firm: Manage-rial behavior, agency costs and ownership structure. Journal of financial economics, 3(4):305–360, 1976.

Gustavo Manso, Bruno Strulovici, and Alexei Tchistyi. Performance-sensitive debt. Review of Financial Studies, 23(5):1819–1854, 2010.

Erwan Morellec, Philip Valta, and Alexei Zhdanov. Financing investment: the choice between bonds and bank loans. Management Science, 61(11): 2580–2602, 2014.

Justin Murfin. The supply-side determinants of loan contract strictness. The Journal of Finance, 67(5):1565–1601, 2012.

Stewart C Myers. Determinants of corporate borrowing. Journal of financial economics, 5(2):147–175, 1977.

Raghuram G Rajan. Insiders and outsiders: The choice between informed and arm’s-length debt. The Journal of Finance, 47(4):1367–1400, 1992.

Michael R Roberts. The role of dynamic renegotiation and asymmetric in-formation in financial contracting. Journal of Financial Economics, 116 (1):61–81, 2015.

Michael R Roberts and Amir Sufi. Financial contracting: A survey of em-pirical research and future directions. Available at SSRN 1356944, 2009a.

Michael R Roberts and Amir Sufi. Renegotiation of financial contracts: Evi-dence from private credit agreements. Journal of Financial Economics, 93 (2):159–184, 2009b.

Daniel Saavedra. Renegotiation and the choice of covenants in debt contracts. Available at SSRN 2626942, 2015.

Susan Chenyu Shan, Dragon Yongjun Tang, and Andrew Winton. Does credit protection lower the value of creditor control rights? 2015.

Figures

Figure 1: Maturity

Panel A: Time-trend

Figure 2: PVIOL

Panel A: Time-trend

Figure 3: Performance Pricing Provisions

Panel A: Time-trend

Figure 4: Capital Structure: % of Loans

Panel A: Time-trend

Figure 5: Capital Structure: % of Bonds

Panel A: Time-trend

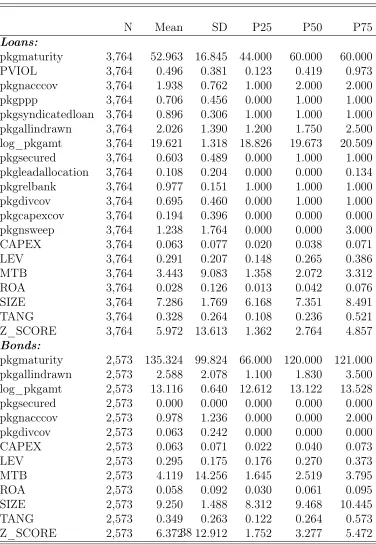

Table 1: Descriptive Statistics

Panel A: Full Sample

N Mean SD P25 P50 P75

Loans:

pkgmaturity 3,764 52.963 16.845 44.000 60.000 60.000

PVIOL 3,764 0.496 0.381 0.123 0.419 0.973

pkgnacccov 3,764 1.938 0.762 1.000 2.000 2.000

pkgppp 3,764 0.706 0.456 0.000 1.000 1.000

pkgsyndicatedloan 3,764 0.896 0.306 1.000 1.000 1.000 pkgallindrawn 3,764 2.026 1.390 1.200 1.750 2.500 log_pkgamt 3,764 19.621 1.318 18.826 19.673 20.509

pkgsecured 3,764 0.603 0.489 0.000 1.000 1.000

pkgleadallocation 3,764 0.108 0.204 0.000 0.000 0.134

pkgrelbank 3,764 0.977 0.151 1.000 1.000 1.000

pkgdivcov 3,764 0.695 0.460 0.000 1.000 1.000

pkgcapexcov 3,764 0.194 0.396 0.000 0.000 0.000

pkgnsweep 3,764 1.238 1.764 0.000 0.000 3.000

CAPEX 3,764 0.063 0.077 0.020 0.038 0.071

LEV 3,764 0.291 0.207 0.148 0.265 0.386

MTB 3,764 3.443 9.083 1.358 2.072 3.312

ROA 3,764 0.028 0.126 0.013 0.042 0.076

SIZE 3,764 7.286 1.769 6.168 7.351 8.491

TANG 3,764 0.328 0.264 0.108 0.236 0.521

Z_SCORE 3,764 5.972 13.613 1.362 2.764 4.857

Bonds:

pkgmaturity 2,573 135.324 99.824 66.000 120.000 121.000 pkgallindrawn 2,573 2.588 2.078 1.100 1.830 3.500 log_pkgamt 2,573 13.116 0.640 12.612 13.122 13.528

pkgsecured 2,573 0.000 0.000 0.000 0.000 0.000

pkgnacccov 2,573 0.978 1.236 0.000 0.000 2.000

pkgdivcov 2,573 0.063 0.242 0.000 0.000 0.000

CAPEX 2,573 0.063 0.071 0.022 0.040 0.073

LEV 2,573 0.295 0.175 0.176 0.270 0.373

MTB 2,573 4.119 14.256 1.645 2.519 3.795

ROA 2,573 0.058 0.092 0.030 0.061 0.095

SIZE 2,573 9.250 1.488 8.312 9.468 10.445

Table 1: Descriptive Statistics

Panel B: Syndicated and Single-Lender Loans

Syndicated Loans Non-Syndicated Loans

N SD Mean P50 N SD Mean P50

pkgmaturity 3,371 15.758 54.06 60.00 393 22.148 43.58 36.00

PVIOL 3,371 0.377 0.48 0.38 393 0.381 0.65 0.81

pkgnacccov 3,371 0.745 1.92 2.00 393 0.876 2.09 2.00

pkgppp 3,371 0.442 0.73 1.00 393 0.500 0.47 0.00

pkgallindrawn 3,371 1.303 1.94 1.75 393 1.836 2.74 2.50 log_pkgamt 3,371 1.141 19.85 19.81 393 1.139 17.69 17.50 pkgsecured 3,371 0.494 0.58 1.00 393 0.399 0.80 1.00 pkgleadallocation 3,371 0.153 0.09 0.00 393 0.424 0.23 0.00 pkgrelbank 3,371 0.115 0.99 1.00 393 0.313 0.89 1.00

pkgdivcov 3,371 0.463 0.69 1.00 393 0.439 0.74 1.00

pkgcapexcov 3,371 0.382 0.18 0.00 393 0.475 0.34 0.00

pkgnsweep 3,371 1.762 1.23 0.00 393 1.788 1.29 0.00

CAPEX 3,371 0.073 0.06 0.04 393 0.102 0.07 0.04

LEV 3,371 0.201 0.29 0.27 393 0.254 0.27 0.22

MTB 3,371 9.335 3.46 2.09 393 6.536 3.33 1.79

ROA 3,371 0.105 0.04 0.04 393 0.227 -0.04 0.02

SIZE 3,371 1.635 7.51 7.54 393 1.711 5.37 5.20

TANG 3,371 0.263 0.33 0.24 393 0.269 0.31 0.22

Table 1: Descriptive Statistics

Panel C: Syndicated Loans and Public Bonds

Private Loans Public Bonds

N SD Mean P50 N SD Mean P50

pkgmaturity 3,371 15.758 54.06 60.00 2,573 99.824 135.32 120.00 pkgallindrawn 3,371 1.303 1.94 1.75 2,573 2.078 2.59 1.83 log_pkgamt 3,371 1.141 19.85 19.81 2,573 0.640 13.12 13.12 pkgsecured 3,371 0.494 0.58 1.00 2,573 0.000 0.00 0.00 pkgnacccov 3,371 0.745 1.92 2.00 2,573 1.236 0.98 0.00 pkgdivcov 3,371 0.463 0.69 1.00 2,573 0.242 0.06 0.00

CAPEX 3,371 0.073 0.06 0.04 2,573 0.071 0.06 0.04

LEV 3,371 0.201 0.29 0.27 2,573 0.175 0.30 0.27

MTB 3,371 9.335 3.46 2.09 2,573 14.256 4.12 2.52

ROA 3,371 0.105 0.04 0.04 2,573 0.092 0.06 0.06

SIZE 3,371 1.635 7.51 7.54 2,573 1.488 9.25 9.47

TANG 3,371 0.263 0.33 0.24 2,573 0.263 0.35 0.26

Table 1: Descriptive Statistics

Panel D: Pre- and Post-TD9599 Adoption

Pre TD9599 Post TD9599

N SD Mean P50 N SD Mean P50

pkgmaturity 2,794 17.776 51.88 60.00 970 13.342 56.08 60.00

PVIOL 2,794 0.383 0.52 0.47 970 0.365 0.42 0.30

pkgnacccov 2,794 0.786 2.01 2.00 970 0.649 1.74 2.00

pkgsyndicatedloan 2,794 0.327 0.88 1.00 970 0.227 0.95 1.00

pkgppp 2,794 0.434 0.75 1.00 970 0.493 0.58 1.00

pkgsyndicatedloan 2,794 0.327 0.88 1.00 970 0.227 0.95 1.00 pkgallindrawn 2,794 1.449 2.08 1.75 970 1.191 1.88 1.50 log_pkgamt 2,794 1.332 19.46 19.52 970 1.157 20.09 20.17

pkgsecured 2,794 0.482 0.63 1.00 970 0.500 0.52 1.00

pkgleadallocation 2,794 0.219 0.12 0.00 970 0.146 0.07 0.00

pkgrelbank 2,794 0.167 0.97 1.00 970 0.090 0.99 1.00

pkgdivcov 2,794 0.429 0.76 1.00 970 0.500 0.52 1.00

pkgcapexcov 2,794 0.418 0.22 0.00 970 0.310 0.11 0.00

pkgnsweep 2,794 1.808 1.30 0.00 970 1.617 1.05 0.00

CAPEX 2,794 0.081 0.07 0.04 970 0.063 0.06 0.04

LEV 2,794 0.212 0.28 0.26 970 0.191 0.31 0.29

MTB 2,794 7.327 3.22 1.98 970 12.847 4.10 2.33

ROA 2,794 0.135 0.02 0.04 970 0.093 0.04 0.04

SIZE 2,794 1.767 7.06 7.13 970 1.597 7.95 8.00

TANG 2,794 0.266 0.33 0.25 970 0.256 0.31 0.22

Table 1: Descriptive Statistics

Panel E: Syndicated and Single-Lender Loans around TD9599 Adoption

Syndicated Loans Non-Syndicated Loans

Pre Post Pre Post

SD Mean SD Mean SD Mean SD Mean

pkgmaturity 16.741 52.96 12.295 57.00 22.510 44.12 19.510 40.15

PVIOL 0.380 0.50 0.364 0.42 0.368 0.68 0.375 0.40

pkgnacccov 0.768 1.98 0.652 1.75 0.890 2.16 0.596 1.62

pkgppp 0.410 0.79 0.492 0.59 0.500 0.47 0.504 0.47

pkgallindrawn 1.366 1.98 1.112 1.85 1.793 2.79 2.084 2.42 log_pkgamt 1.142 19.71 1.057 20.21 1.160 17.63 0.912 18.07

pkgsecured 0.490 0.60 0.500 0.52 0.363 0.84 0.504 0.53

pkgleadallocation 0.162 0.10 0.122 0.07 0.432 0.25 0.361 0.15

pkgrelbank 0.127 0.98 0.074 0.99 0.323 0.88 0.233 0.94

pkgdivcov 0.431 0.75 0.500 0.52 0.413 0.78 0.504 0.47

pkgcapexcov 0.404 0.21 0.303 0.10 0.482 0.36 0.395 0.19

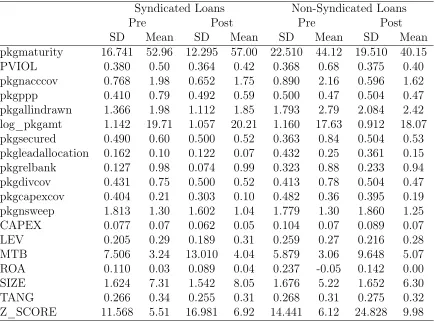

pkgnsweep 1.813 1.30 1.602 1.04 1.779 1.30 1.860 1.25

CAPEX 0.077 0.07 0.062 0.05 0.104 0.07 0.089 0.07

LEV 0.205 0.29 0.189 0.31 0.259 0.27 0.216 0.28

MTB 7.506 3.24 13.010 4.04 5.879 3.06 9.648 5.07

ROA 0.110 0.03 0.089 0.04 0.237 -0.05 0.142 0.00

SIZE 1.624 7.31 1.542 8.05 1.676 5.22 1.652 6.30

TANG 0.266 0.34 0.255 0.31 0.268 0.31 0.275 0.32

Table 1: Descriptive Statistics

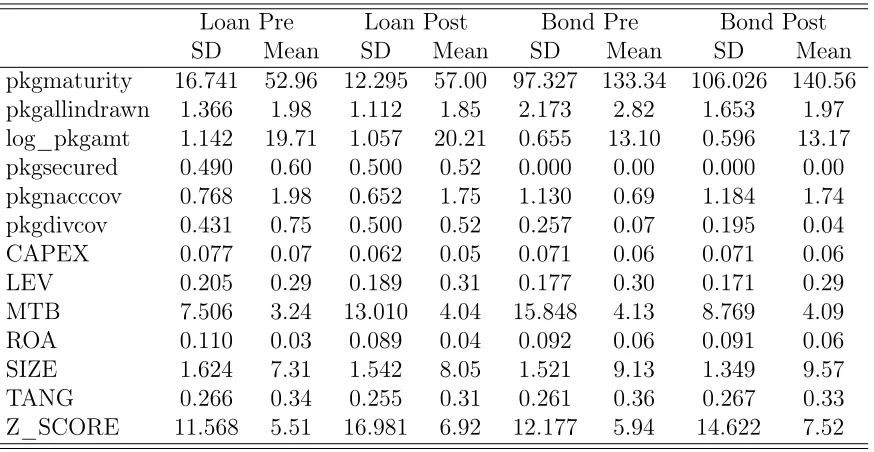

Panel F: Bonds and Syndicated Loans around TD9599 Adoption

Loan Pre Loan Post Bond Pre Bond Post

SD Mean SD Mean SD Mean SD Mean

pkgmaturity 16.741 52.96 12.295 57.00 97.327 133.34 106.026 140.56 pkgallindrawn 1.366 1.98 1.112 1.85 2.173 2.82 1.653 1.97 log_pkgamt 1.142 19.71 1.057 20.21 0.655 13.10 0.596 13.17 pkgsecured 0.490 0.60 0.500 0.52 0.000 0.00 0.000 0.00 pkgnacccov 0.768 1.98 0.652 1.75 1.130 0.69 1.184 1.74

pkgdivcov 0.431 0.75 0.500 0.52 0.257 0.07 0.195 0.04

CAPEX 0.077 0.07 0.062 0.05 0.071 0.06 0.071 0.06

LEV 0.205 0.29 0.189 0.31 0.177 0.30 0.171 0.29

MTB 7.506 3.24 13.010 4.04 15.848 4.13 8.769 4.09

ROA 0.110 0.03 0.089 0.04 0.092 0.06 0.091 0.06

SIZE 1.624 7.31 1.542 8.05 1.521 9.13 1.349 9.57

TANG 0.266 0.34 0.255 0.31 0.261 0.36 0.267 0.33

Z_SCORE 11.568 5.51 16.981 6.92 12.177 5.94 14.622 7.52

Table 2: Descriptive Statistics

Panel A: Capital Structure - Full Sample

All Firms

N Mean SD P25 P50 P75

Table 2: Descriptive Statistics

Panel B: U.S. Firms and Non U.S. Firms

U.S. Firms Non U.S. Firms

N SD Mean P50 N SD Mean P50

LOANPCT 8,305 0.287 0.34 0.31 4,849 0.290 0.34 0.29

BONDPCT 8,305 0.295 0.62 0.65 4,849 0.297 0.59 0.60

SECUREDPCT 8,305 5.990 0.63 0.55 4,849 0.371 0.48 0.47 SENIORPCT 8,305 5.994 0.89 0.86 4,849 0.237 0.82 0.88 REVOLVINGPCT 8,305 0.790 0.14 0.03 4,849 0.194 0.12 0.04 DEBTEBITDA 8,305 0.382 0.00 0.00 4,849 16.108 0.23 0.01

Table 2: Descriptive Statistics

Panel C: Around TD9599 Adoption

Pre TD9599 Post TD9599

N SD Mean P50 N SD Mean P50

LOANPCT 7,080 0.290 0.36 0.32 6,074 0.285 0.33 0.26

BONDPCT 7,080 0.298 0.60 0.62 6,074 0.293 0.62 0.65

SECUREDPCT 7,080 6.485 0.63 0.54 6,074 0.388 0.51 0.52 SENIORPCT 7,080 6.490 0.90 0.85 6,074 0.265 0.83 0.89 REVOLVINGPCT 7,080 0.852 0.14 0.04 6,074 0.192 0.12 0.03 DEBTEBITDA 7,080 0.786 -0.00 0.01 6,074 14.374 0.19 0.00

Table 2: Descriptive Statistics

Panel D: U.S. and Non-U.S. Firms around TD9599 Adoption

U.S. Pre Syndicated Post Non-U.S. Pre Non-U.S. Post

SD Mean SD Mean SD Mean SD Mean

LOANPCT 0.285 0.35 0.289 0.34 0.300 0.37 0.279 0.32

BONDPCT 0.295 0.62 0.295 0.63 0.302 0.57 0.291 0.61

SECUREDPCT 7.828 0.69 0.403 0.54 0.379 0.49 0.363 0.47

SENIORPCT 7.838 0.93 0.297 0.84 0.261 0.82 0.216 0.82