THE INFLUENCE OF

EQUITY FINSANCING FUNDING RATE

AND RATE ON PROFITABILITY OF ISLAMIC BANK WINWIN YADIATI

Lectures, Department of Accountancy Faculty of Economics, Padjadjaran University

Abstract

The purpose of this research is to examine the influence of customer and short term funding total assets and equity financing rate on profitability of Islamic Bank simultaneously and partially. Sample of this research are Bank Muamalat Indonesia and Bank Syariah Mandiri for the year 1999-2005. This research are descriptive method with associative approach. Statistical method is used at significant level using multiple regression analysis. The result of these hypothesis shows that firs, hypothesis that states there are influence of customer and short term funding over total assets and equity financing rate to profitability of financing rate has no significant influence to profitability of Islamic Bank simultaneously. Second, hypothesis that states there are influence of customer and short term funding over total assets has significant influence to profitability of Islamic Bank partially. Third, hypothesis that states there are influence equity financing rate to profitability of Islamic Bank is rejected. It means that equity financing rate does not have significant influence to profitability of Islamic Bank partially.

Key Word: customer and short term funding over total assets, equity financing rate, profitability and Islamic Bank.

Introduction

amendment of UU No. 7 in the year of 1992 became UU no. 10 in the year of 1998 that gave a clearer operational base for Islamic banks.

The development of Islamic bank after the making of UU No 10 in the year of 1998 was as the replacement of UU No 7 in the year of 1992 was very rapid. It was seen from the number of fund of the third side and cost that had been given. The number of fund the third side that had been collected by the Islamic Banks incisively rose from Rp. 43,45 milliards in 1997, became 4,33 trillions on October 2003 and had a rapid increasing became Rp9,34 trillions on August 2004 or in the other word it rose as big as 72,5% than in the end of 2003. While, the cost that had been channeled by Islamic Banks also had an increasing from Rp.490,20 milliards in 1997 became Rp. 4,68 trillions in October 2003 and had a rapid increasing after the instructions from Majelis Ulama Indonesia (Indonesian 0Clergy Committee) on 16 December 2003, became Rp.9,54 trillions on August 2994 (source : Banks Indonesia, 2006). The increasing of fund on the third side that entered to Islamic Banking after the instruction have been concerned that would influence the liquidity level of bank side because the recent Islamic Banking appreciated does to roll the funds on the real economic sector. The excess of funds in the Islamic Banks cannot be transferred to help the cost of conventional banks because, in the way of operational principle, both banks are extremely different. /The excess of liquidity is caused by the imbalance between the absorption of DPK and the distribution of the costs that in another time will effect on the reduction of production sharing for the customers because the enrolled funds will be the ‘idle fund’ that inclined to be precipitated and does not make any profit: it can also affect to the reduction of the profitability of Islamic Banks.

Derived from UU No 10 in the year 1997 that: “The cost based on the Islamic principle is the supplying of money or claim that can be equaled with the cost according to the agreement between bank and another side which obligate the earned side to deport the money or claim after certain period of time with a production sharing compensation.”

According to Muhammad Syafi’I Antonio in his book that entitled Bank Syariah dari Teori ke Paraktik (2001), the Islamic operational principle that had been applied in the aggregation of society’s funds is Wadiah and Mudharabah principle :

1. Wadiah Ya adh Dhamanah Deposit Pricile (Guarantee Depository) that applied into wadiah deposit and wadiah deposit and wadiah saving

2. Invesment Principlem there are two kinds which are mhudarabah muthlaqah (general investment) that applied into mudharabah saving and mudharabah deposit, the second one is mudharabah muqayyadah (special investment) in which the customers give a limit to the bank in investing their fund savings.

increasing of society’s belief towards Islamic banks both in business activity or even daily activity.

The bank liquidity level itself is a very important matter to be kept. On the journal which is made by M. Kabir Hassan, PhD and Abdel-Hemeed M. Bashir, PhD entitled “ Determinants of Islamic Banking Profitability” mentioned that : : It is, therefore. Extremely important to monitor liquidity indicators because poor management of short-term liquidity may force solvent banks toward closure.”

The ratio of liquidity that discussed in this research is Costumer and Short Term Funding over Total Assets (CSTFTA) that is funds succeed to be collected by Islamic banks from the customer the third side and have a character of short term. The journal that mention about: “the ratio of consumer and short term funding over total assets (CSTFTA) is as liquidity ratio that comes from the liability side. It consist of current deposits, saving deposits, and investment deposits. Since liquidity holding represent an expense to the bank, the coefficient of this variable expected to be negative.”

Customer and short funding over total assets is a ratio between the funds of the third side with the total of assets of the Islamic Banks. This ratio measure the proportion of assets that are earned by the third side.

Table 1

Deposit Fund That Succeed To Be Collected by the Islamic Banks (In million Rupiah)

Deposit Fund Dec-05 Mar-06 Jun-06 Jul-06 Aug-06 Sep-06

Wadiah currency Account 2,046,333 2,257,372 2,657,588 2,292,559 2,632,552 2,747,786 Mudharabah Saving Account 4,370,668 4,501,201 4,971,785 5,250,390 5,298,025 5,604,591 Mudharabah Deposit Account 9,166,428 8,197,133 8,965,465 8,965,465 9,176,479 9,623,131

TOTAL 15,582,329 14,955,706 16,432,728 16,508,414 17,107,065 17,915,508

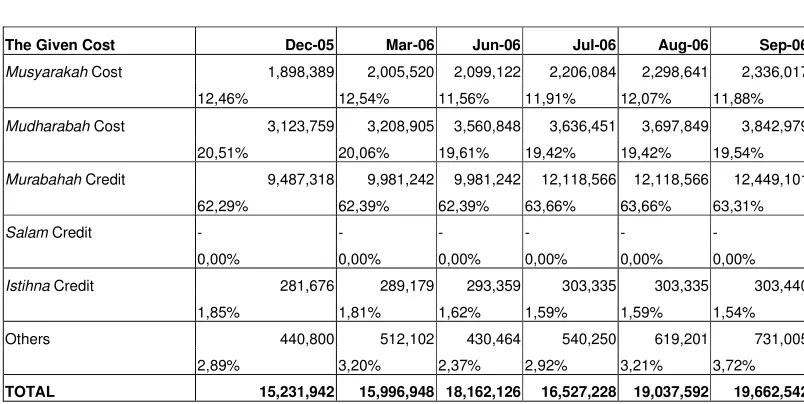

dan Studi Kebanksentralan Bank Indonesia), “internal obstacle is the existing of several problems such as the comprehension of Islamic Banking essence that are still low, the existing of business and effort orientation that become more important, quantity and quality of resource that are still inadequate, the attitude of ‘aversion to effort’ and ‘aversion to risk’. Whereas, the external obstacle is that the equity financing has high risk in the matter of loss that can happen in the time period of the cost; it is because the equity financing cost is not only dividing the profit but also dividing loss, in the term that that loss is not mistake of the earned side.”

Table 2

The Cost Given By Islamic Banks (in million Rupiah)

The Given Cost Dec-05 Mar-06 Jun-06 Jul-06 Aug-06 Sep-06

Musyarakah Cost 1,898,389 2,005,520 2,099,122 2,206,084 2,298,641 2,336,017

12,46% 12,54% 11,56% 11,91% 12,07% 11,88%

Mudharabah Cost 3,123,759 3,208,905 3,560,848 3,636,451 3,697,849 3,842,979

20,51% 20,06% 19,61% 19,42% 19,42% 19,54%

Murabahah Credit 9,487,318 9,981,242 9,981,242 12,118,566 12,118,566 12,449,101

62,29% 62,39% 62,39% 63,66% 63,66% 63,31%

Salam Credit - - - -

0,00% 0,00% 0,00% 0,00% 0,00% 0,00%

Istihna Credit 281,676 289,179 293,359 303,335 303,335 303,440

1,85% 1,81% 1,62% 1,59% 1,59% 1,54%

Others 440,800 512,102 430,464 540,250 619,201 731,005

2,89% 3,20% 2,37% 2,92% 3,21% 3,72%

TOTAL 15,231,942 15,996,948 18,162,126 16,527,228 19,037,592 19,662,542

The implementation of production sharing cost needs a very high level honesty from the side that gets the cost, In getting an adequate conviction that will be expensed by the profitable production sharing system and in a good prospect so that the Islamic Banks are not courageous yet in doing expansion in equity financing cost.

From the phenomenon above, it is seen that in its development, the Islamic Banks has been succeed to collect funds from the third side or customer and short term funding that will be allocated to the cost in order to produce gains or bank’s profits; beside that, the Islamic Banks also want to keep the level of liquidity by committing the giving of cost carefully, however, in the other sides, Islamic Banks with its production sharing characteristic exactly is still demanded to be always increase the cost based on the equity financing principle. Therefore, the writer interests to do a research which is entitled: “the influence of customer and short term funding over total assets and the level of equity financing towards the profitability of Islamic Banks”

Problem Identifications

According to the explanations above, then the problems that will be analyzed in this research are:

1. Are customer and short term funding over total assets and the level of equity financing influenced simultaneously towards the profitability of Islamic Banks

2. Are customer and short term funding over total assets and the level of equity financing influenced partially towards the profitability of Islamic Banks

The Intentions of Research

1. To Know whether there are the influence of customer and short term funding over total assets and the level of equity financing simultaneously towards the profitability of Islamic Banks or not

2. To Know whether there are the influence of customer and short term funding over total assets and the level of equity financing partially towards the profitability of Islamic Banks or not

The Usefulness of Research

This research is expected can be useful and beneficial for the writer and another side that concerned.

1. For the bankers

The research can give a useful contribution for the Islamic Banking management towards policies that will be taken, particularly in taking a policy about the effort for increasing the profitability and also towards a policy in deciding a cost portion that will be given concerning about the Islamic Bank’s responsibility over the development of economy.

2. For another Researcher

3. For another side

This research is expected to be useful for another side particularly in the development of the analytic science of the financial report in order to know how much the financial ratio with others and release another point of view from the assessment of financial work performance particularly in Islamic Banks.

Theory Base

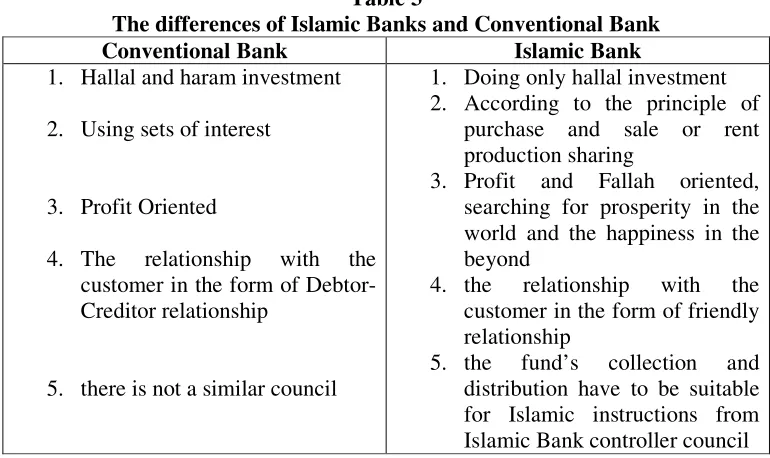

The Differences of Islamic Bank and Conventional Bank

The differences between Islamic bank and conventional bank are showed in the following table 3

Table 3

The differences of Islamic Banks and Conventional Bank

Conventional Bank Islamic Bank

1. Hallal and haram investment 2. Using sets of interest

3. Profit Oriented

4. The relationship with the customer in the form of Debtor-Creditor relationship

5. there is not a similar council

1. Doing only hallal investment 2. According to the principle of

purchase and sale or rent production sharing

3. Profit and Fallah oriented, searching for prosperity in the world and the happiness in the beyond

4. the relationship with the customer in the form of friendly relationship

5. the fund’s collection and distribution have to be suitable for Islamic instructions from Islamic Bank controller council Fund Sources of Islamic Banks

The Definition of Bank Fund Source

In a book “manajemen perbankan”, 2000, Kasmir defines a bank fund source as an effort of a bank in collecting funds from society, in his opinion, the achievement of fund depends on the banks it self, whether it is from society’s savings, or another organization. Then, to cost its operation, the funds can also be gotten by own capital that is by publishing or selling stocks. The Achievement of funds is adjusted with the intention of the usage of the cost. The selection of fund source will determine the measurement of the guaranteed cost. Therefore, the selection of fund source has to be done properly.

gotten by several kinds of saving, while if the need of cost need is used for a new investment or an expansion of corporation therefore, it is gotten from own capital.

Marginally, the fund source for the Islamic Banks can be gotten from: 1. Funds from the bank it self (the first side funds)

2. Funds from another organization (the second side funds) 3. Funds from broad society (the third side funds)

Principle in Trade Murabahah Meaning

Murabahah bi tsaman ajil is more known as Murabahah. Murabahah is taken from word ribhu (profit) is trade transaction where bank tells the amount of profit. Bank has function as seller, while customer as buyer. Sell price as bank’s buy price from supplier plus profit. Both parties need to agree the sell price and payment range of time. In banking, murabahah is usually done by credit (bitsaman ajil). In this transaction, properties are given immediately while payment is done gradually.

Application in Banking

Generally, murabahah KPP can be applied on financing product to buy investment’s properties, either domestic or international, such as through Letter of Credit (L/C). This scheme is most used because it is simple and familiar to those who accustomed with bank transaction general.

Liquidity Ratio

This ratio is used to evaluate a bank’s ability in fulfilling its short term responsibilities or be due responsibilities. The liquidity ratio mentioned in this research is Customer and Short Term Funding over Total Assets (CSTFTA), is ratio between funds that collected by Islamic Bank from customer or third party which has short term character with owned total assets, where mentioned in the journal: “the ratio of consumer and short term funding over total assets (CSTFTA), is a liquidity ratio that comes from the liability side. It consists of current deposits, saving deposits, and investments deposits”. Customer and Short Term Funding over Total Assets (CSTFTA) can be counted with:

Equity financing level

Abdus Samad and M. Khabir in their journal “The Performance of Malaysian Islamic Bank During 1984-1997: An Exploratory Study” mentioned that in evaluating commitment in economy and Moslem community of Islamic Bank we could use, one of which, Mudharabah- Ratio partnership which has aim to evaluate commitment to development of Moslem community through equity financing.

According Accounting guidelines of Indonesia’s Islamic Banking: Mudharabah financing is cooperate business contract between bank as funds owner (shalibul maal) and customer as funds developer (mudharib) to do business with equity ratio (profit and loss) according previous agreement”.

“Musyarakah is cooperation ratio between capital owner (partner) to unite the capital and do the business together in a partnership. With equity ratio match with agreement, while loss are carried proportionally match with capital contribution”. Mudharabah- Ratio partnership can be counted by the following formula:

Mudharabah-Musyarakah ratio= Mudharabah-Musyarakah Total financing

Profitability Ratio

There are several profitability ratio mentioned either by several expert or several literatures. There are also several ratios used by several financial institutions and interrelated institutions in counting the bank profitability level. Those are:

1. Gross Profit Margin

This ratio is used to knowing the percentage business profit pure from bank before it is decreased by burdens.

2. Net Profit Margin

This ratio is used to measure the bank ability in produce net income from main operation for bank

3. Return on Equity (ROE)

This ratio is used to measure the management ability of a bank in develop the available capital to obtain net income. From owner’s perspectives, ROE is the more important measurement because it can be reflect their ownership.

4. Return on Assets (ROA)

The number of Return on Assets (ROA) can be counted by the following formula:

ROA= Profit after Tax Total Assets

Islamic Bank

Islamic Bank’s Work Activities

Collecting Society’s Funds

Distributing Funds/ Contributing to the increase of society economy qualities

Current deposits, saving deposits

& investment deposits Equity Financing

Islamic Bank Income

ROA (Return On Assets) Profitabilitiy

Research Hypothesis :

Customer & Short Funding over Total Assets and Equity Financing level have simultaneous and partial effects on Islamic Bank

Profitability

Figure 1

Research Object and Method Research Object

The object used by writer in this research is Customer and Short Term Funding over Total Assets, which is ratio between collectible funds by Islamic bank from customer or third party and has short term character with total assets; Equity Financing Rate by using Mudharabah and Musyarakah ratio proxy, is ratio that shows Islamic bank commitment to development the Moslem communities through equity financing; and also Islamic bank Return on Assets

Profitability, is ratio to measure the Islamic bank management ability simultaneously from owned asset development.

Research Method

1. Used Research Method

In this research, writer used description method by associative approach 2. Population And Sample

Populations in this research are all banks that operated in Islamic way and have form as general Islamic Bank. While sampling technique used in this research is purposive sample.

Writer chooses Bank Syariah Mandiri (BSM) as sample because from three general Islamic Banks in Indonesia, BSM has the biggest assets and Islamic financing. The total assets distributed by BSM are 39.62% or almost 40% from Islamic banking total assets. BSM also has the highest ability in developing Islamic bank network with total funds collected from the third party is 46.2%. 3. Data Collecting Technique

The data used in this research are quantitative data, which are secondary data in form of BSM yearly financial report. Those data are obtained by library research and internet research. Writers takes period 1999-2005 because starting 1999, BSM start its operation until present. The data taken which total assets, total funds of third party (current deposits, saving deposits and investment deposits),

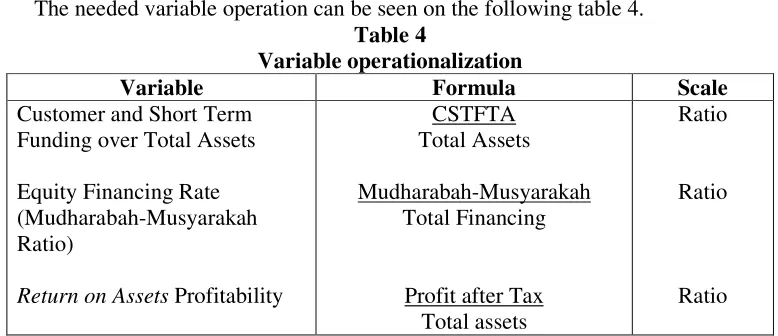

mudharabah financing, total given financing and net income. 4. Variable Operation

The needed variable operation can be seen on the following table 4. Table 4

Variable operationalization

Variable Formula Scale

Customer and Short Term Funding over Total Assets Equity Financing Rate (Mudharabah-Musyarakah Ratio)

Return on Assets Profitability

CSTFTA Total Assets Mudharabah-Musyarakah

Total Financing

Profit after Tax Total assets

Ratio

Ratio

Sources: - Journal “the performance of Malaysian Islamic Bank During 1984- 1997: an exploratory study” by Abdus Samad and M. Kabir Hasan

- Journal “Determinants of Islamic Banking Profitability” by M. Kabir Hasan and Abdel Hamed M. Bashir.

5. Hypothesis Planning Data Analysis

In doing analysis, the writer through the following steps:

a. Collecting data, which related with interrelated variables such as customer and short term funding over total assets, equity financing rate, and profitability. Determining the value of interrelated variables match with determined formula from previous data that already collected.

b. Doing statistic testing to test hypothesis and also interpret and make analysis over the result of hypothesis testing.

c. Making summary according to the result of statistic testing.

Hypothesis determination Simultaneously:

Ho1: µ = 0 there are no significant influence happened simultaneously between customer and short term funding over total assets and equity financing rate over Islamic bank profitability

Ha1: µ ≠ 0 there are significant influence happened simultaneously between customer and short term funding over total assets and equity financing rate over Islamic bank profitability

Partially:

1. Customer and Short Term Funding over Total Assets

Ho2:β = 0 There are no significant influence happened partially to customer and

short term funding over total assets over Islamic bank profitability.

Ho2:β≠ 0 there are significant influence happened partially to customer and short

term funding over total assets over Islamic bank profitability. 2. Equity financing rate

Ho3β = 0 There are no significant influence happened partially to equity financing

rate over Islamic Bank profitability.

Ho3β≠ 0 There are significant influence happened partially to equity financing

rate over Islamic bank profitability.

The steps on hypothesis testing in regression and correlation analysis are:

1. Normality Test

Normality test is done to knowing whether or not each variable distributes normally.

Regression analysis is used to predict the value of variable Y based on the value of variable X and also the changing prediction on variable Y for every changing unit of variable X. the equation form of this multiple regression linear is:

Y = α + β1 + β2X2 + ε Where:

Y = Profitability (Return on Assets)

X1 = Customer and short Term Funding over Total Assets X2 = Equity Financing rate (Mudharabah- Musyarakah ratio)

α = Constantan, is dependent value, which in this matter is Y when the independent variable is 0 (X1,X2=0)

β1 = Multiple regression coefficient between independent variable X1 over dependent variable Y, if the independent variable X2, and considered constant.

β2 = Multiple regression coefficient between independent variable X2 over dependent variable Y, if dependent variable X1, and considered constant.

Regression Classic Assumption test a. Multicolinearity Test

b. Autocorrelation Test c. Heteroscedacity Test

F Test

In testing regression model which explain the relation form and influence between independent variable over dependent variable, F which can be formulated as follows.

− − =

k k n

F 1

−R R

1 2

Where:

R2 = Determination Coefficient n = Sample Measure k = Amount of independent variable

Value F from the result of previous counting then to be compared to F table which is gained by using risk rank 5% and degree of numerator and denominator namely VI = k and V2 – n=k=1 by using following criteria:

If the acceptance of Ho takes place it can be meant that multiple regression model is significant which makes result that the influence of independent variables are also simultaneously insignificant to the dependen variable.

t Test

to test influence of dependent variables partially to independent variables. It uses regression coefficient partially (test), namely by comparing If ttable and tcounting which can be formulated as following:

t=Rxi

rx k n

( 1

1 −

− −

Each t results of this counting then to be compared to ttable which is gained using real level 0,005. Criteria which is used as a comparison basic is following:

Hypothesis test uses 2 parties partially, with criteria: Ho is accepted if : -t 1/2α< t < t 1/2α

Ho is rejected if : t< -t 1/2α t> t 1/2α Result and Discussion

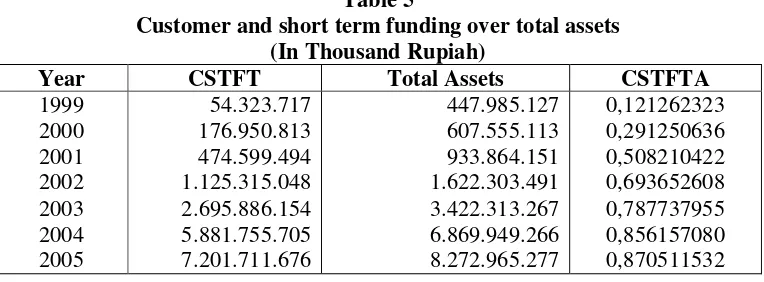

Customer and short term funding over total assets is a ratio between the amount of Customer and short term funding namely the fund of member or third party which consist with the amount of giro wadiah, mudharabah saving, and mudharabah deposit; with total assets or total a total assets owned by Bank Syariah Mandiri.

Table 5

Customer and short term funding over total assets (In Thousand Rupiah)

Year CSTFT Total Assets CSTFTA

1999 2000 2001 2002 2003 2004 2005

54.323.717 176.950.813 474.599.494 1.125.315.048 2.695.886.154 5.881.755.705 7.201.711.676

447.985.127 607.555.113 933.864.151 1.622.303.491 3.422.313.267 6.869.949.266 8.272.965.277

0,121262323 0,291250636 0,508210422 0,693652608 0,787737955 0,856157080 0,870511532 Level of Equity Financing

(Mudharabah-Musyarakah Ratio)

musyarakah cost skim or cost of sharing profit (equity financing) to the total of amount of cost which is given.

The component of this ratio is kind of the amount of mudharabah and musyarakah also the total amount of cost which is gained from the financial report of Bank Syariah Mandiri.

Profitability (Return Assets)

So profitability uses the ratio of Return On Assets (ROA) is kind of ratio between profit after tax or net profit with total assets (total activa ) which is owned by Bank Syariah Mandiri. This ratio is used to measure the ability of bank management in obtaining the profit totally through managing the asset which is owed by bank.

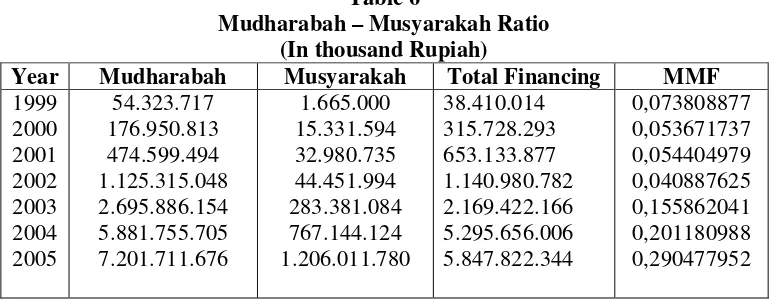

Table 6

Mudharabah – Musyarakah Ratio (In thousand Rupiah)

Year Mudharabah Musyarakah Total Financing MMF

1999 2000 2001 2002 2003 2004 2005 54.323.717 176.950.813 474.599.494 1.125.315.048 2.695.886.154 5.881.755.705 7.201.711.676 1.665.000 15.331.594 32.980.735 44.451.994 283.381.084 767.144.124 1.206.011.780 38.410.014 315.728.293 653.133.877 1.140.980.782 2.169.422.166 5.295.656.006 5.847.822.344 0,073808877 0,053671737 0,054404979 0,040887625 0,155862041 0,201180988 0,290477952

So Profitability uses the ratio of Return on Assets (ROA) is kind of ratio between profit after tax or net profit with total assets (total activa) which is owned by Bank Syariah Mandiri. This ratio is used to measure the ability of bank management in obtaining the profit totally through managing asset which is owed by the bank.

From the early processing data which is resulted values obtained from independent variables and dependent variables of research as presented in the table 8. the values of those variables will be processed further by using the support of software SPSS 13.0 in order to answer the identified problem.

Table 7

Return on Assets (In thousand Rupiah)

Year Profit After Tax Total Assets ROA

Table 8

Value of Research Variables

Year CSTFTA MMF ROA

1999 2000 2001 2002 2003 2004 2005 0,121262323 0,291250636 0,508210422 0,693652608 0,787737955 0,856157080 0,870511532 0,073808877 0,053671737 0,054404979 0,040887625 0,155862041 0,201180988 0,290477952 0,000383125 0,015701275 0,017886553 0,018588156 0,004679964 0,015057878 0,010131709

Description of Research Result

At the below is presented the result of Descriptive statistic of processing the variables processing is gained by assisting SPSS 13.0.

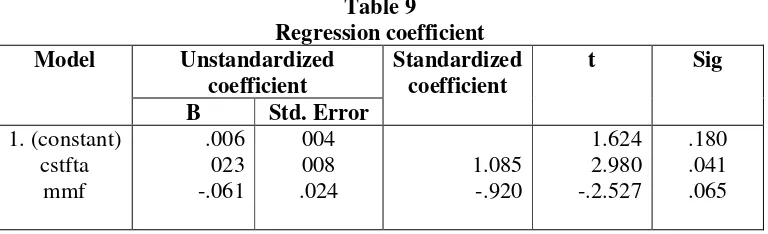

Table 9

Regression coefficient

Model Unstandardized

coefficient

Standardized coefficient

t Sig

B Std. Error 1. (constant) cstfta mmf .006 023 -.061 004 008 .024 1.085 -.920 1.624 2.980 -.2.527 .180 .041 .065

Analysis of double linear regression

From the above table 9, it is obviously can be seen that the functional relation between customer and short term funding over total assets with return on assets (ROA) is in versely proportional whereas the relation between the level of equity financing and

ROA is inversely proportional. It means, every increasing which takes place at CSTFTA will be followed the increasing of ROA bank, and every increasing the level of equity financing will be followed by the decreasing of ROA bank and vise versa.

Dependent Variable: roa For BSM:

Y=0,006+0,023X1.-.061X2+Σ Where Y=

Profitability (Return on Assets/ROA)

X1 = Customer and Short Term Funding over Total Assets (CSTFA)

Coefficient of Correlation and Multiple Determination

In a research on the relation between dependent variables and independent variables, some powers of X1, X2 which together explain the change of Y are often wanted to be known. Determination coefficient (R*) can be seen through the result of counting by using SPSS 13.0. at the below:

Table 10 Summary Model Model R R Square Adjusted R

Square

Std. Error of the Estimate

Dustin – Watson

1 .838(a) .702 .553 004185603930 2.218

Then obtained that Ftable is 6.94. the summary of hypothesis 1 testing result is as follows:

Table 11

F Test Result Model Summary Anovab

Model Sum of

Square

Df Mean

Square

F Sig.

Regression Residual Total .000 .000 .000 2 4 6 .000 .000

4.714 .089a

a. Predictors: (constant), mmf, cstftfa b. Dependent Variables: roa

Table 12

t Test Result Coefficient

Model Unstandardized

Coefficient

Standardized Coefficient

t Sig

B Std. Error Beta

t Test

Partially testing is done to knowing the existence of relation or influence one of independent variable with dependent variable with assumption that the other variables are constant. The test result with helps from SPSS 13.0. can be seen on the following table 12.

In testing this hypothesis, the criteria which can be used is a criteria where: Ho is accepted when: -t1/2 <tcount< -t1/2 . Ho is rejected when: tcount <-t1/2 or tcount> t1/2 with df = n-k-1 = 7-2-1 = 4 then the obtained ttable is 2.7764. from table 4.10, can be known that value of tcount for Customer and Short Term Funding over Total Assets is 2.980 an for equity financing rate (Mudharabah- Musyarakah Ratio) is -2.527. since 2.980 >2.7764 or tcount> t1/2 , so Ho is in the rejection area, it means that the relation and the influence happened between variable Customer and Short Term Funding over Total Assets with Return in Assets is significant. Meanwhile, -2.527 <-2.7764<2.527or -t1/2 <tcount< t1/2 , so Ho is in the acceptance area, it means that the relation and influence happened between variable Equity Financing Rate with Return on Assets is non-significant.

Conclusion and Suggestions Conclusion

From the research that has been done and also explained on the previous chapters, can be concluded as follows:

1. The result of hypothesis test simultaneously between Customer and Short Term Funding over Total Assets and Equity Financing Rate over profitability (Return on Assets)shows that zero hypothesis is accepted. This shows that there are no significant influence from Customer and Short Term Funding over Total Assets and Equity Financing Rate simultaneously over Islamic Bank.

2. The result of Hypothesis test partially on Customer and Short Term Funding over Total Assets (CSTFTA) over profitability (ROA) Islamic Bank shows that zero hypothesis is rejected. This means CSTFTA has significant influence over profitability (ROA) with positive way. Positive influence means that the increase (decrease) Customer and Short Term Funding over Total Assets (CSTFTA) will be followed with the increase (decrease) Islamic bank profitability (ROA). This happens because most funds that accepted by Bank Mandiri Syariah are invested in financing form, which has the biggest portion from profitable assets. 3. The result of hypothesis test partially between Equity Financing

(mudharabah – Musyarakah Ratio/ MMF) over profitability (ROA). This

Suggestion

For those who interested in doing advanced research, writer would like to give several suggestion, as in follows:

1. Using other profitability ratio such as Return on Equity, Gross Profit Margin, or Net Profit as independent variable.

2. Researching other factors that influence Islamic bank profitability, such as financing distribution (financing to work capital sector, investment, and consumptive) and equity ratio rate

References

Ajiwarman karim. 2004. Bank Islam: Analisis Fiqh dan keuangan, 2nd ed. Jakarta: IIIT Indonesia

A.Wirman syafe’i. 200. “Pengukuran Kinerja Bank Syariah”.Majalah Ekonomi Syariah. Jakarta.EKABA Universitas Trisakti.

Ascarya. 2005. “Dominasi Pembiayaan non Bagi hasil Perbankan Syariah di Indonesia: Masalah & Alternatif solusi”. Majalah Ekonomi Syariah.

Jakarta. EKABA Universitas Trisakti.

Bank Indonesia. 2002. Certakan Biru Perkembangan Perbankan Syariah 2002-2011. Jakarta: www.bi.go.id

Bank Indonesia. 2006. Statistik Perbankan Syariah September 2006. Jakarta:

www.bi.go.id

Ikatan Akuntan Indonesia. 2003. Pedoman Akuntansi Perbankan Syariah Indonesia. Jakarta: Biro Perbankan Syariah Bank Indonesia.

Ikatan Akuntan Indonesia. 2004. Standar Akuntansi Keuangan per 1 Oktober 2004. Jakarta . Penerbit Salemba.

Gujarati. Damodar. 2003. Basic econometrics 4th. Singapore: McGrawhill.

Kabir, hasan and Abdel – Hameed. Bashir. 2002. “Determinants of Islamic Banking profitability”. ERF Paper. www.google.com

Lukman Dendawijaya. 2003. Manajemen Perbankan. Jakarta. Ghalia Indonesia. Kasmir. 2002. Manajemen Perbankan. Jakarta. Raja Grafindo Persada.

Moch. Nazir. 2003. Metode Penelitian. Edisi lima. Jakarta. Ghalia Indonesia. Muhammad. 2002. Manajemen pembiayaan bank Syariah. Yogyakarta.UPP-AMP

YKPN.

Muhammad Syafi’i Antonio. 2001. bank Syariah: dari teori ke Praktik. Jakarta. Gema Insani Press.

Undang- Undang No.10 1998, Perbankan Syariah, Bank Indonesia

Nur Indriantoro dan Bambang Supomo. 2002. Metodologi Penelitian Bisnis Untuk Akuntansi. Yogyakarta. BPFE

Samad, Abdus,. And M. Khabir hassan. 1999. ”Islamic International Journal of Financial Service: The performance of Malaysian Islamic bank During 1984-1997: An Exploratory Study”. www.google.com

Sarker, Md Abdul Awwal. 1999. “Islamic International journal of Financial Service: Islamic Banking in Bangladesh Performance problems & Prospects” www.google.com

Sugiono. 2003. Statistika untuk Penelitian. Bandung. Alvabeta

Wiroso. 2005. Penghimpunan Dana dan Distribusi Hasil Usaha Bank Syariah.

Jakarta. Gramedia Widiasarana Indonesia.

www.syariahmandiri.co.id

Yulia Mustika Wati. 2004. Prospek Perbankan Syariah Pasca Fatwa MUI. www.esyariah.com