Changing Environment

Kevin Devine

XAVIERUNIVERSITYPriscilla O’Clock

XAVIERUNIVERSITYDavid Lyons

LYONSACCOUNTINGSERVICES,INC.

Concerns over escalating health-care costs have brought about significant change. Health-care providers (HCPs) that customarily fo-changes in the way health-care organizations and professionals are com- cused on increasing revenues by providing a variety of services pensated for their services. Capitation, the payment of a fixed fee to and maintaining high occupancy rates must now seek to con-health-care providers in exchange for providing medical care when it is trol costs, while still providing quality service. The impact of needed, has been a significant element of change in the health-care indus- this change is confounded by the fact that many HCPs have try. The purpose of this paper is to propose a framework for the evolution inadequate cost-accounting systems.

of management accounting systems in a changing health-care environment. Failure to manage health-care costs and to obtain accurate This framework suggests that the role of activity-based costing, life cycle cost information may leave HCPs ill-equipped to negotiate costing, and value chain analysis becomes increasingly important as the capitation agreements with provider networks and threaten payment for health-care services moves from fee for service reimbursement their ability to remain competitive. Improved cost manage-to capitation arrangements between insurance companies and health-care ment systems, such as activity based costing (ABC) that identi-providers. Health-care organizations that design and implement accurate fies all activities associated with a specific treatment, and their costing and evaluation systems will enhance their ability to compete corresponding cost, can improve financial cost management. successfully in this rapidly changing environment. J BUSN RES 2000. These systems are expensive to implement, but may allow

48.183–191. 2000 Elsevier Science Inc. All rights reserved. health-care organizations to more accurately determine and trace costs of services and develop a better understanding of the cost of services provided. Such advanced cost management practices as life cycle costing and value chain analysis provide

T

otal health-care expenditures between 1980 and 1994 the opportunity for integrated health-care providers to better increased 400% from $250 billion dollars to over $1 manage total health care costs. Life cycle costing could provide trillion (Standard and Poors, 1995). In response tointegrated networks with the ability to understand total patient escalating health-care costs, the health-care industry, led by

health-care cost over the life of an illness or even the patient’s insurance companies, physicians’ groups, and hospitals, has

entire lifetime. Similarly, value chain analysis can assist health-established health maintenance organizations (HMOs) and

care providers in managing total patient health-care cost other integrated delivery systems. Typically, these health

through the elimination of redundant services and increased maintenance organizations enter into capitation agreements

efficiencies in dealing with other value chain participants, with participating physicians, and/or hospitals, thereby,

pro-including doctors, hospitals, and insurance companies. To viding an essentially fixed revenue stream in exchange for

compete in the rapidly changing health-care environment, some form of guaranteed care for the covered group.

HCPs must develop an information system that provides finan-With the emergence of this new way of doing business, the

cial and nonfinancial feedback in support of more advanced financial focus of hospitals and physicians must significantly

cost management methods. The HCP’s ability to develop the information necessary to benefit from life cycle costing and Address correspondence to Dr. Kevin Devine, Department of Accounting and value chain analysis is positively related to the degree of inte-Information Systems, Xavier University, 3800 Victory Parkway, Cincinnati, OH

45207-5161, USA. gration within the network.

Journal of Business Research 48, 183–191 (2000)

2000 Elsevier Science Inc. All rights reserved. ISSN 0148-2963/00/$–see front matter

The purpose of this paper is to discuss the role of manage- able, making cost control a more significant issue. HCPs tradi-rial accounting in assisting HCPs to reduce cost and remain tionally emphasized increasing revenues to increase profits competitive. The first section provides an overview of financial and/or return on investment (ROI). The emphasis is shifting trends affecting hospitals and other health-care providers. The from revenues to controlling costs. Cost control will become second section presents a framework for applying ABC, life the primary financial management responsibility and the way cycle costing, and value chain analysis in the health-care set- to increase profits.

ting. Next, a more complete discussion of the application of According to Fromberg (1996), capitation models generally these tools is provided. Finally, a discussion of control and fall into three basic types of contract between the payor, performance evaluation systems is presented, followed by a typically the HMO, and the service providers. The first type,

summary and conclusions. with lowest degree of integration, is an agreement between

the HMO and primary care physicians, specialists, and hospi-tals. The primary care physicians are paid on a capitated basis,

The Changing Health-Care

but specialists are not capitated, and hospitals are paid on aEnvironment

per diem basis. With the next higher level of integration,specialists as well as primary care physicians are capitated. Historically, hospitals have focused on generating revenues

The highest integration occurs in a global capitation model through increasing bed capacity, occupancy rates, fee for

ser-in which the HMO enters ser-into a contract for all health services vice rates, and the number of patients treated per day. This

with a physician–hospital organization. focus leads to a strategy of bringing more people into the

Capitation can drastically affect the staffing procedures at facility for treatment by providing more and better services.

hospitals. Some hospitals are trying to buy into the practices The exact costs of these services to the hospital or their impact

of primary care physicians and physician groups in order to on profitability had not been a major consideration. Revenues

provide an integrated primary care network to the public were increased by marketing the treatment, with little concern

(Pallarito, 1994). Capitation also creates an incentive to in-for the cost of the specific treatment.

crease the emphasis on preventative health care; providing Managed care organizations emerged in response to

pres-the patient with preventative education and treatment to re-sure to slow the increase in health-care costs. These

organiza-duce and eliminate illness and disease over the patient’s life-tions vary in scope from health maintenance organizalife-tions

time. Hospital networks that develop wellness programs to (HMOs) to large integrated delivery systems. Integrated

deliv-promote healthy lifestyles may benefit from lower health-care ery systems are conglomerations of organizations that work

costs in the future. An example of this approach to health together to provide health-care services to a population of

pa-care is discussed by Scott Goodspeed (as reported in Greene, tients, enabling higher quality care, more specialized services,

1995) who indicates that many hospitals are talking about and lower risks and costs to the provider. These networks

“developing community-care networks to improve the health usually cover a specific geographic area to provide needed

status of a geographic population.” Goodspeed, however, goes health-care services to a given population. The impetus for

on to say, “Unfortunately, there’s not enough action” (p. 86). integrated delivery systems comes from four different sectors:

The importance of hospitals developing wellness programs is hospitals, physicians or physician groups, a combination of

provided by Carroll (1995) who states that: hospital and physician groups, and insurance companies

(Shortall, 1995). Under capitation, we have already received a per-member,

The idea of an integrated network is to develop a network per-month rate and are at economic risk for the cost of all of health-care services through exclusive relationships, capi- services over and above the monthly premium paid by or tation agreements, and mergers that will provide quality, con- for the member. The incentives under capitation are to venience, and affordable health-care services to the covered keep the member healthy and to reduce the need for costly population. A large integrated network should be able to in- acute care services. (p. 28)

crease cost efficiency by reducing duplicate services and

pa-Integrated delivery systems with fixed revenues may reduce perwork. In addition, the network provides for a dilution of

health-care costs by increasing the number of procedures that the risk sharing involved with capitation.

are performed on an out-patient basis, while still maintaining Capitation agreements between insurance companies,

hos-occupancy rates at the full-service hospitals. Out-patient costs pitals, and physicians provide that a fixed fee be paid per

are significantly lower than in-patient care, and development month, per person in the covered group. The fee is determined

of new technologies that permit out-patient treatment, or lower by an actuarial analysis of the covered population and the

cost home health-care options are likely to be encouraged. anticipated medical costs. One estimate is that, by the year

Capitation creates winners and losers. Insurance companies 2,000, 95% of all medical treatment in some geographic

re-support capitation, because their payments to hospitals and gions will be covered under some type of capitation agreement

physicians are of a predictable, consistent nature, shifting (Carroll, 1995). As capitation agreements become the normal

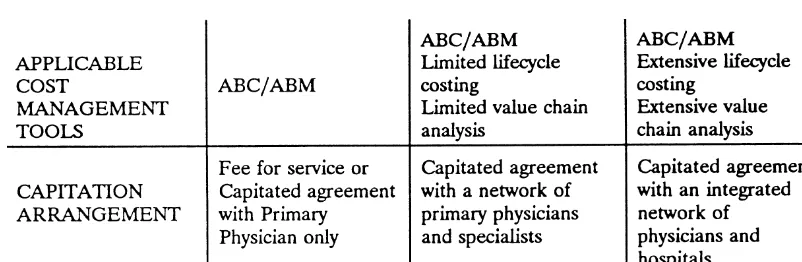

Figure 1. Framework for health-care cost management.

hospitals and physicians. One major risk of capitation is that applied in the health-care environment. A possible explanation an HCP that agrees to a capitation rate that is too low will is that traditional health-care practice has not fostered the face cost overruns caused by miscalculation of the medical sharing of patient treatment information.

needs of a given population. This miscalculation could result As the level of health-care integration increases, the benefits in significant losses or bankruptcy. An accurate cost and pa- of and the opportunity to utilize value chain analysis and life tient information system will help to minimize this risk. cycle costing is also likely to increase. The integrated networks have access to a tremendous breadth of information related to a patient’s lifestyle, wellness, illness, and treatment history

Framework for Health-Care

that would typically not be available or important to less

Financial Management

integrated networks. For example, a primary physician’spa-tient that suffers a stroke and is rushed to the emergency The previous discussion suggests that changes in the

health-room for treatment is not likely to have information regarding care industry have resulted in an increased focus on cost

subsequent cost of treatment and rehabilitation. In addition, control. Figure 1 presents a framework for the application of

this cost information is of little benefit to the primary physi-activity-based costing (ABC), life cycle costing, and value chain

cian. However, to the integrated network that encompasses analysis for the management of cost in the health-care

indus-primary physicians, cardiologists, neurosurgeons, physical try. The framework indicates which of these tools can be

therapists, and the hospital, this information can be of tremen-utilized most effectively to control health-care costs across

dous benefit. With access to all information related to patient capitation models. In fee for service and simple capitation

illness and treatment, the integrated network is in a position arrangements (those in which insurance companies or HMOs

to utilize life cycle cost analysis. Over time, this integrated contract only with primary physicians), the framework

sug-network can evaluate the impact of wellness and physical gests that activity-based costing and/or activity-based

manage-conditioning programs on patient health, including the likeli-ment (ABM) play the most important role in health-care cost

hood of stroke or heart attack. With information regarding management. As capitation agreements become more

inte-the impact of inte-these programs on patient illness and inte-the total grated, the use of life cycle and value chain analysis takes on

cost of patient treatment, the integrated network can deter-greater importance in the management of total health-care

mine the net financial cost or benefit of sponsoring assorted costs. Additional analysis is possible, because the more

inte-wellness programs. grated provider networks have a greater breadth of information

The highly integrated provider network is also likely to related to a patient’s lifestyle, wellness, illness, and treatment

benefit from value chain analysis. Because the network is history. The rationale for the proposed framework is discussed

responsible for all phases of patient treatment it will be able below.

to eliminate redundant testing and treatment. For example, As health-care costs have increased, the political pressure

when a patient consults with his or her primary physician to control these costs has also increased. Activity-based

man-regarding an illness, the primary physician may conduct some agement has been shown to be an effective tool for cost

man-basic blood tests but not discover the patient’s problem. The agement in a variety of settings. ABM is the strategic cost

primary physician may then refer the patient to a specialist management concept that has evolved in some companies

for further testing. In the absence of an integrated network, who have investigated and/or implemented ABC. ABC has

the specialist is typically reimbursed on a fee for service basis. been successfully applied in the health-care industry to reduce

Thus, there is little or no benefit to the specialist to be con-over-all treatment costs (Carr, 1993; Canby, 1995; Caltrider,

cerned with duplication of services. It would not be unusual Pattison, and Richardson, 1995). However, the use of life

primary physician, in addition to a new battery of tests. The costing systems also fail to address fixed costs adequately. integrated network could easily coordinate the treatment and In the health-care industry, where fixed or common costs eliminate this redundancy. In an environment in which the (building, equipment, administration) are large, the allocation insurance company entered an agreement with the primary of those costs must be as accurate as possible. Many conven-physician only, the primary conven-physician may make the specialist tional costing systems allocate this cost arbitrarily to depart-aware of the tests that had been run, but there would be little ments, which then re-allocate the cost to the service provided incentive for the specialist to not repeat the tests and receive to a patient using a single allocation base.

the corresponding revenue. An ABC system focuses on activities performed with costs

When a capitated arrangement includes both primary phy- accumulated at the activity level. An activity is defined as a sicians and a group of specialists, the capitated group will unit of resource used for the benefit of the patient. There are receive some benefits of both life cycle and value chain analy- two types of activities, those that directly affect the patient, sis. However, the benefit will be limited, because information and those that indirectly affect the patient. Examples of direct related to the patient from major providers, including hospitals activities include: nursing care, pharmaceutical, physician and specialists that are not participating in the capitation care, and lab tests. Examples of indirect activities may include: agreement, will not be available. As the health-care environ- bookkeeping, hospital maintenance, utilities, depreciation, ment evolves into greater degrees of integration, through and hospital administration. ABC attempts to identify all pro-broader capitation agreements, the benefit derived from life cesses related to patient treatment. Next, the underlying activi-cycle costing and value chain analysis is likely to increase. ties associated with these processes are identified. This identifi-cation facilitates more accurate accumulation of cost and the assignment of logical cost drivers. Costs of indirect activities

Cost Management Tools

are allocated to the direct activities that they benefit. Finally, direct activities are allocated to services received by the pa-The framework presented above suggests that as thehealth-care industry shifts financial focus from generating revenues tients. ABC is an attempt to minimize arbitrary allocations of to managing costs it needs to develop and implement an fixed common costs, however, in most situations, some costs information system that will accurately determine, allocate, remain that are still allocated on an arbitrary basis.

and analyze costs. To accomplish this, it was suggested that An additional benefit of identifying the processes and activi-ABC, life cycle costing, and value chain analysis take on vary- ties underlying patient treatment is that management is likely ing levels of importance dependent upon the capitated ar- to discover that not all activities add value. That is, they rangement. This section provides a more thorough discussion provide no benefit to the treatment of the patient. This discov-of these three models discov-of analysis useful for the financial man- ery presents management with the information necessary to agement of health-care organizations. First, the primary fea- manage/reduce total service costs. The next step in activity tures and benefits that distinguish an ABC system from tradi- analysis is to improve the efficiency of activities. This process tional costing systems are presented. This is followed by a includes the attempt to reduce or eliminate nonvalue-added discussion of how value chain analysis and life cycle costing activities. Use of ABC concepts to facilitate the identification principles can be applied to the health-care environment. and reduction of nonvalue-added activities is frequently

re-ferred to as activity-based management (ABM).

The ABC system must identify all of the activities involved

Activity-Based Costing

in the treatment of a patient and allocate the cost of those Activity-based costing, when properly implemented, provides

activities to the patient through the use of cost drivers. A cost information for strategic decision making and better cost

con-driver is the attribute for allocating costs that is most correlated trol. Accurate cost information can help management

under-with a given activity. An example of a cost driver for nursing stand the operations of the network and provide more accurate

care provided under an ABC system would be the amount of costing of patient services.

care (hours) required by the patient. Conventional costing Conventional costing systems used in the health-care

in-systems have frequently used a flat per day rate for each dustry typically use a single allocation base (cost driver) to

patient, regardless of the amount of nursing care provided. assign costs to departments and services. That is, conventional

The problem with this system is that the treatment of a patient systems use one attribute (number of employees, number of

requiring very little nursing care time is usually assumed to patients, number of hours) when allocating costs from one

cost the same as a patient that requires significant nursing department to another or from a department to a service

care time. Thus, the lower care patients have been subsidizing provided to a patient. The result is an accumulation of costs

the more intensive care patients. Some procedures or treat-that may reflect little or no direct relationship between costs

ments that regularly require more nursing care have been incurred and the service(s) provided. This single basis for

costing the hospital more than was apparent under a conven-assigning costs usually leads to low volume or complex

treat-tional costing system, thus making the treatment seem more ments or procedures being under costed; whereas, high

Carr (1993) provides an example of the process of devel- ment’s understanding of the operations are significantly en-hanced with more refined information.

oping an ABC system for nursing service at Braintree

Rehabili-Caltrider, Pattison, and Richardson (1995) report that ABC tation Center. Three skill levels of nursing services: RN, LPN,

became an integral part of the continuous quality improve-and NA were identified. The corresponding pay scale was

ment (CQI) program implemented at Children’s Hospital in determined to vary from $26 per hour to $8 per hour.

Brain-San Diego. A review of hospital records had identified the tree developed a team of staff members, all familiar with the

orthopedic outpatient clinic as one of the four highest cost work flow of the hospital, to conduct and analyze time,

mo-areas in the hospital. An ABC assessment indicated that man-tion, and frequency studies of both routine and special nursing

agement of financial and medical information consumed two-events. The team compiled the information to develop a

pa-thirds of the labor time in the clinic. The information derived tient information/classification form, which was used to

estab-from ABC analysis, coupled with the hospital’s CQI program lish a database that shows the distribution of nursing care by

resulted in a 20% reduction in the cost of treating femur type of activity and by diagnosis. They found that routine

(thigh bone) structures in this department. nursing events, those performed for almost every patient,

Lawson (1994) discussed the adoption of ABC in a health-represented anywhere from 5% to 70% of the nursing care

care organization operating in five geographic regions and time provided, depending upon the medical problem and

providing two main services. The implementation of ABC length of stay. As a patient’s rehabilitation progressed,

lower-focused on the allocation of administrative overhead. Before skilled nursing care typically replaced higher-skilled nursing

the adoption of ABC the organization’s traditional system allo-care. This process allowed them to manage staffing more

cated the cost of administrative overhead within a 5% range efficiently and provide better cost assessments for the services

for both services in the five regions. The ABC analysis revealed provided.

that there was a 30% fluctuation in the consumption of admin-Chan (1993) demonstrated how information from the

Stan-istrative overhead for one of the two services. For the second dard Treatment Protocol can be used in the development of

service, the author found that the administrative overhead an ABC system for the tests conducted in a hospital laboratory.

varied by a factor of 30. That is, the most expensive region Ramsey (1994) developed two hypothetical examples for

consumed 30 times the overhead of the least expensive region, applying activity-based costing to a radiology department and

leading the author to conclude that traditional costing system a nursing station in hospitals. Although the scenarios were

inadequacies exist in the health-care environment much the hypothetical, they provided a framework for the application

same as in manufacturing settings. of ABC in the hospital setting. Each of these papers also

Because ABC requires determining activities and devel-provides a thorough discussion of steps for implementation

oping an understanding of their underlying processes, identifi-of an activity-based costing system.

cation of inefficiencies related to such nonfinancial factors as Canby (1995) reports that ABC was used to determine the

patient waiting time and duplicate processes is facilitated. costs of service in the X-ray department more accurately at a

Corrective action to improve these inefficiencies can reduce medium-sized outpatient clinic. Primary activities were

identi-cost and improve the quality of customer service. fied and costed for each X-ray procedure. Secondary activities

manage-capitation agreements, it is a step that could mean the differ- ment of goods arrives at a distributor’s dock, a distributor’s ence between survival and insolvency. truck is waiting to load the material and take it to its final Once costs have been accurately determined, management destination. This operation, known as cross docking, has re-will be better positioned to make informed decisions in the sulted in significant reduction in warehousing and material changing health-care environment. A health-care organiza- handling cost by distributors, through cooperation and coor-tion’s understanding of total patient service cost may be further dination of logistics operations with suppliers.

improved by applying value chain and life cycle costing princi- A study conducted by the Joint Industry Project on Efficient ples, discussed in the following section. Consumer Response (1994) sought to identify opportunities for improving performance in the grocery supply chain. A key finding in a pilot project carried out between Procter &

Value Chain and Life Cycle Analysis

Gamble and H.E. Butt was that by adopting an activity-based The concepts of value chain analysis and life cycle costing

view of the supply chain, value-added activities can be identi-require developing an understanding of all costs related to

fied and business processes can be enhanced/streamlined/elimi-delivery of a product or service to the final consumer. These

nated. The net effect of this process is a reduction in total cost concepts may be beneficial in the health-care environment,

of putting the finished product in the consumer’s hands. particularly in the design and control of integrated

health-In cases where no one participant operates in all phases care networks. Specifically, these organizations will need to

of the value chain, the successful implementation of value determine how they can organize and cooperate to maximize

chain analysis is dependent upon cooperation and information patient benefit while reducing cost. Through cooperation,

sharing among trading partners. This cooperation is necessary information can be shared that reduces costly duplication of

to identify opportunities for savings and to obviate duplicate such administrative services as form filing and accumulation

provision of services. In the health-care environment, such of general patient information. Additionally, cooperation can

cooperation may be limited in the absence of integrated pro-result in the elimination of unnecessary duplicate tests and

vider networks. This situation arises out of patient privacy procedures (nonvalue-added costs). Such sharing of

informa-laws that hinder sharing of information between unrelated tion is, in many respects, new to the profession, and steps

value chain participants. However, as networks become more must be taken to ensure patient’s confidentiality rights.

integrated, the opportunity to share information and exploit Shank and Govindarajan (1992) define a value chain for

linkages in the value chain expands. any firm as “the linked set of value-creating activities all the

To apply value chain analysis to the health-care industry way from basic raw material sources through to the ultimate

we might consider patient health as the desired output. The end-use product delivered into the final consumer’s hands”

value chain would then include all aspects of patient health, (p. 179). It is generally held that, given an organization’s

from health education to fitness and wellness programs, mission and competitive strengths and weaknesses, it defines

through all activities associated with routine and acute care. where it can best compete in the value chain. Once an

organi-Health-care providers must determine which links of this zation understands its niche in the value chain, management

chain are consistent with their mission, given the entity’s then looks upstream and downstream in the chain to

deter-relative strengths and weaknesses. Finally, communication mine how they can improve conditions between/with other

channels must be established that allow hospitals, physicians, organizations in the chain to the mutual benefit of all parties

and other care providers to work together with other partici-involved.

pants up and downstream in the value chain. For example, Vital to the use of value chain analysis is the development

a regional hospital’s value chain would include the suppliers of an understanding of the major processes involved in the

of pharmaceutical products, the manufacturers of diagnostic value chain. Although this approach does not require the

equipment and surgical equipment, the private practice physi-utilization of activity-based costing, its use can be beneficial

cians whose patients use the hospital services, and the ambu-in understandambu-ing the lambu-inkages ambu-in the value chaambu-in withambu-in one

lance services that transport patients to the hospital. If a hospi-organization or between hospi-organizations. An understanding of

tal works with all members of the value chain to identify business processes, both within and outside the organization,

inefficiencies and nonvalue-added costs, industrywide costs leads to the identification of opportunities to remove cost

can be reduced. from the value chain. An example of exploiting linkages in

The opportunity to develop health-care value chain analysis the value chain is provided by Procter and Gamble’s (P&G)

seems to be emerging through the development of integrated installation of order entry computers directly in Walmart

health-care systems previously discussed. Pawola and Kline-stores. Although this resulted in a capital outlay for P&G,

man (1996) report that the growth in development of the the over-all entry and processing costs for both firms were

integrated delivery system (IDS) requires a shift in the type of substantially decreased, resulting in total value chain savings

information required and the focus. Rather than the traditional (Shank and Govindarajan, 1992). Similar examples have

oc-focus on departments and single entities, the need emerges curred in the retail industry, where manufacturers and

inte-grating all patient functions, both patient care and financial preventative health efforts. This approach and the subsequent incentives created exemplifies the life cycle approach to health information. According to Pawola and Klineman

care, and the physician must understand the degree of risk An efficient information system can contribute to the

enti-that has now been shifted from a managed care organization ty’s ability to provide cost effective quality care by 1)

pro-to the contracting physician. The physicians that recognize this viding timely information, 2) assisting in resource

conser-risk shift and implement offensive procedures by providing vation, 3) facilitating the sharing of accurate and reliable

preventative health care, health education, and programs to information with others in the IDS, within security

restric-reform patient’s poor health practices may enhance their abil-tions, 4) assisting in management of a patient’s care delivery ity to profit under capitation contracts. A potential downside process, including all aspects of wellness and disease, and is that the physician group that has successfully implemented 5) by having the ability to statistically analyze and predict wellness measures is now serving a population that is at a the demand for services by a given population of subscrib- low health risk threshold. This covered population has now

ers. (p. 46) become a desirable group that could be purchased by other

competitor HCPs. The value chain analysis approach can provide the IDS with

Health-care organizations that develop a value chain and the ability to determine where in the chain the greatest cost

life cycle approach will need to evaluate the relative contribu-competencies and efficiencies can be captured. Applying the

tions of health care provided at each stage of a patient’s life. principles of value chain analysis will provide a framework

Assessment of such factors as patient benefits derived from for developing, managing, and improving the efficiency of

health education programs, wellness programs, and other pre-these organizations.

ventative care programs must be conducted. However, these Life cycle costing provides an opportunity to organize

benefits will not be fully realized without tracking the appro-thinking within the value chain (Hirsch, 1994, p. 128). Within

priate information. The next section presents a discussion of a manufacturing organization, all products go through a life

the types of information, controls, and performance evaluation cycle, beginning with research and development and

continu-measures necessary for this level of cost analysis. ing on through introduction to the market, growth, maturity,

decline, disposal or discontinuation. Similarly, the life cycle of patient health care begins with prenatal care, through birth,

Control and Evaluation Systems

development, education, maturity, aging, and finally death.In fact, prenatal care is a part of two individual’s life cycles From a financial management perspective, a good control at the same time, because the care provided to the fetus is a system should provide information on total service cost as well result of caring for the woman during pregnancy. The perfor- as information useful in monitoring past capitation agreements mance of health-care providers at each stage of a patient’s life and negotiating future agreements. The control system should cycle is likely to have an impact not only on the patient’s also classify this information by risk category of the patient. well-being, but also on the demands placed on resources For example, it must be determined if the activities performed of organizations providing care at subsequent stages of the in any given procedure, whether it be treatment of a back patient’s lifecycle. Therefore, a life cycle perspective would injury or heart bypass surgery, are different across patient risk provide HCPs with the opportunity to evaluate the impact categories. These risk categories might consider factors such as of preventative health-care expenditures over the patient’s age, gender, smoking or drinking habits, and general physical lifetime on the health-care costs incurred late in the patient’s condition. Health-care providers that can identify differences life. This analysis would allow the providers to analyze statisti- between risk categories of patients and activities necessary to cally whether the increased expenditures on preventative care treat patients from different categories are better equipped are offset by a reduction in the rate of increase in patient to negotiate capitation agreements with covered groups. In health-care costs later in life. An alternative view to life cycle addition, this information can be used to identify the benefits costing may be more manageable in the short run. This alterna- derived from various types of wellness or preventative medi-tive would be to look at the total costs of treatment over the cine programs. Employing a life cycle perspective of patient life cycle of a specific illness or condition. An approach such care results in designing a control system that accumulates and as this could also be of benefit to the less than fully integrated monitors key patient characteristics and treatment activities.

health-care networks. Ultimately, the impact of such services as education and

well-To effectively negotiate capitation contracts, physician ness programs on the level of acute care provided to the groups need essential data regarding costs and utilization of covered group can be evaluated.

physicians in the state of Washington. The results of this study

Summary and Conclusions

indicate that the mean level of services provided by hospitalsThis paper discusses current trends affecting health-care ser-is not significantly affected by the frequency of cost reporting,

vices providers. As health care moves from a fee-for-service but the variance of average services is smaller for hospitals

environment to one in which providers are presented with a that report on a more frequent basis. In addition, this study

fixed revenue stream in exchange for treatment of a given analyzed the treatment orders of physicians who received

population, cost control becomes increasingly important. An reports that compared their case costs with the average case

ABC system, coupled with the use of value chain analysis and costs of other physicians in the same hospital or geographic

a life cycle costing approach to patient care, provides emerging region. The report enabled the physician to determine if he

integrated health-care organizations with the opportunity to or she was an over/undertreater or close to the average. The

manage costs more effectively. The benefit derived from ABC, results indicated that both the mean level of services and the

life cycle costing, and value chain analysis increases with the variance in services provided were lower for physicians that

degree of integration of the HCP network. A precise cost received these comparative reports. More frequent and

com-measurement and allocation system coupled with a control parative reporting resulted in better utilization of hospital

system that focuses on quality of care and cost by patient risk resources and lower average hospital charges. Thus, the

cost-category provides management with the ability to negotiate reporting system can influence both the quality and the cost

less risky capitation agreements, as well as to determine the of health care. Awasthi and Eldenburg (1996) extended this

long-term effectiveness of such advance programs as educa-study to 1,200 physicians with practices in four populous

tion, wellness, and preventative care. states. The results of the previous research was confirmed and

further reported that providing physicians with information

The authors thank participants at the American Association for Advances about the costs of tests and procedures can play an integral

in Health Care Research Conference and two anonymous reviewers who part in a hospital’s strategic cost management program.

contributed to the development of this manuscript. The development of more advanced financial management

methods alone is inadequate to permit hospitals to compete

and survive. The design of a control system to ensure financial

References

viability and quality of service dictated by the organization’s Awasthi, V. N., and Eldenburg, Leslie: Providing Cost Data to Physi-mission is also critical. If the Physi-mission of the HCP addresses cians Helps Contain Costs.Healthcare Financial Management(April

1996): 40–42.

quality of service, then the control system must be adequately

designed to generate the information required to ensure that Barber, R. L., Jones, W. J., and Johnson, J. A.: Capitating Physician Group Practices. Healthcare Financial Management (July 1996):

quality service is provided. If costs are lowered at the expense

46–49.

of personal patient care by offering fewer services to patients,

Caltrider, J., Pattison, D., and Richardson, P.: Can Cost Control

less personal attention, or long wait times, the long-run

viabil-and Quality Care Coexist?Management Accounting(August 1995):

ity of the HCP could be threatened.

38–42.

To ensure quality of service, control systems must identify

Canby, James B., IV: Applying Activity-Based Costing to Healthcare

and measure attributes consistent with quality service. Such

Settings. Healthcare Financial Management (February 1995):

measures include patient cycle time, repeat visits for the same 50–56. diagnosis, and number of misdiagnoses. Measures such as

Carr, Lawrence P.: Unbundling the Cost of Hospitalization. Manage-these allow the health-care organization to identify key quality ment Accounting(November 1993): 43–48.

factors or objectives not being met. To focus further attention

Carroll, D.: Talking Heads: Lessons on Capitation. Trustee 48(2)

on these quality factors, cost of poor quality indices might be (1995): 28. developed. For example, releasing patients prematurely and

Chan, Y. C. L.: Improving Hospital Cost Accounting With

Activity-having them return for additional treatment creates cost for Based Costing. Health Care Management Review 19(1) (1993): the hospital in addition to creating customer ill will. Hospitals 71–77.

must have information available to compare the costs saved Eldenburg, Leslie: The Use of Information in Total Cost Management. by treating and releasing patients quickly with the potential The Accounting Review(January 1994): 96–121.

total cost of patients returning to the hospital for additional Fromberg, Robert: Capitation is Coming.Healthcare Executive (Janu-treatment and the cost of subsequent ill will. Misdiagnosing ary/February 1996): 4–9.

a patient can result in a similar outcome. Prior to capitation, Greene, J.: Capitation To Shift Board’s Priorities.Modern Healthcare there was no incentive for hospitals to track these costs, be- (April 3, 1995): 86.

cause patients generally were kept longer; for example, mater- Hirsch, Maurice L.:Advanced Management Accounting, Southwestern nity stays. In addition, a re-admitted patient generated addi- Publishing Company, Cincinnati, OH. 1994.

tional revenue. As capitation agreements emphasizing fixed Joint Industry Project on Efficient Consumer Response:Performance revenue streams become more prevalent, such quality failures Measurement: Applying Value Chain Analysis to the Grocery Industry.

Joint Industry Project on Efficient Consumer Response. 1994.

Lawson, R. A.: Activity-Based Costing Systems for Hospital Manage- Shields, Michael D.: An Empirical Analysis of Firms’ Implementation Experiences With Activity Based Costing.Journal of Management

ment.CMA Magazine(June 1994): 31–35.

Accounting Research(Fall 1995): 148–166. Pallarito, K.: System Prepares for Capitation.Modern Healthcare(June

Shank, John K., and Govindarajan, Vijay: Strategic Cost Management: 27, 1994): 100.

The Value Chain Perspective. Journal of Management Accounting

Pawola, L. M., and Klineman, K. A.: Developing Information Systems Research4 (Fall 1992): 179–197.

for Integrated Systems. Healthcare Financial Management (June Shortall, S. M.: The Future of Integrated System.Healthcare Financial 1996): 44–48. Management49(1) (1995): 24229.

Ramsey, R. H.: Activity-Based Costing for Hospitals. Hospital and Standard and Poors: Health Reform Expires, But Managed Care Lives On.Standard and Poors Industry Surveys1 (April 1995): H15.22.