Investments in the capital of banking, financial and insurance entities that are outside the scope of regulatory consolidation, without acceptable short positions, where the Bank does not own more than 10% of the issued share capital (amount above the 10% threshold). Significant investments in ordinary shares of banking, financial and insurance entities that are outside the scope of regulatory consolidation, without eligible short positions (amount above the 10% threshold). Investments in own shares (if no paid-up capital has already been repaid on the reported balance sheet) Mutual holdings in common equity.

Significant investments in the capital of banking, financial and insurance entities that fall outside the scope of regulatory consolidation (net of eligible short positions). Additional Tier 1 instruments (and CET1 instruments not included in row 5) issued by subsidiaries and held by third parties (amount allowed in group AT1). Leverage Ratio - Exposure in the Leverage Ratio Report and Leverage Calculation Report - Banks Only A. Exposure in the Leverage Ratio Report.

Leverage Ratio - Exposure in the Leverage Ratio Report and Leverage Ratio Calculation Report - Bank as Consolidated with Subsidiaries A. Exposure in the Leverage Ratio Report. Leverage Ratio - Exposure in the Leverage Ratio Report and Leverage Calculation Report - Bank as consolidated with subsidiaries B. Disclosure of net claims by risk weight after credit risk mitigation - Bank as consolidated with subsidiaries.

Credit risk - Disclosure of RWA calculation for credit risk using the Standardized Approach - banks only 1. RWA net receivables before CRM RWA after CRM Net receivables RWA before CRM RWA after CRM. Net receivables RWA before CRM RWA after CRM Net receivables RWA before CRM RWA after CRM. Credit risk - Disclosure of RWA calculation for credit risk using the Standardized Approach - Bank as consolidated with subsidiaries 1. Net receivables RWA before CRM RWA after CRM Net receivables RWA before CRM RWA after CRM.

Credit Risk - Counterpary Credit Risk (CCR1) Exposure Analysis - Bank as Consolidated with Subsidiaries

Credit risk - Capital Charge for Credit Valuation Adjustments - Bank as Consolidated with Subsidiaries

Credit Risk - CCR Exposure based on Portfolio Category and Risk Weighting (CCR3) - Bank as Consolidated with Subsidiaries

Credit risk - net credit derivative receivables (CCR6) BCA is not exposed to net credit derivative receivables.

Credit Risk - Net Credit Derivative Claims (CCR6) BCA has no exposure to net credit derivative receivables

Credit Risk - Securitization Exposure in the Banking Book (SEC1)

Credit Risk - Securitization Exposure Components in the Trading Book (SEC2)

Credit risk - Hedging exposures in the bank's book and related to its capital requirements - Bank as Originator or Sponsor (SEC3) BCA does not act as an originator or sponsor of exposures in securitization.

Credit Risk - Securi za on Exposure in the Banking Book and related to its Capital Requirements - Bank Ac ng as Originator or Sponsor (SEC3) BCA does not act as the originator or sponsor of Securitization Exposure

Credit Risk - Securitization Exposure in the Banking Book and related to its Capital Requirements - Bank Acting as Investor (SEC4)

Disclosure of Market Risk Using Standardized Method

Interest rate risk in the banking book (IRRBB) refers to the current or future risk to a bank's capital and profits arising from the movement of interest rates in the market as opposed to positions in the banking book. The IRRBB calculation uses two perspectives, the movement of interest rates in the market as opposed to the balance in the bank's book. The IRRBB calculation uses two perspectives, namely the economic value perspective and the profit-based perspective.

The bank currently does not have sufficient long-term financial resources to finance fixed-rate loans and securities on the bank books. With regard to these conditions, sources of financing are calculated for fixed-rate loans and securities in bank books from the Kernedepotet. To mitigate risks, the Bank has set nominal limits for fixed-rate loans and securities in bank books, limits for IRRBB and pricing strategies.

Measurements of IRRBB individual are carried out on a monthly basis by using two (2) methods as follows

Average repricing maturity applied for NMD is 4 years

The longest repricing maturity applied for NMD is 7 Years

RISK MANAGEMENT IMPLEMENTATION REPORT FOR INTEREST RATE RISK IN THE BANKING BOOK

Measurements of IRRBB consolidated are carried out on a quarterly basis by using two (2) methods as follows

The Economic Value of Equity (EVE) methods use six (6) interest rate shock scenarios as follows: .. 3) steeper shock (short interest rates down and long interest rates up), 4) lower shock (short interest rates up and long interest rates up rates down), 4) lower shock (short interest rates up and long interest rates down), 5) short interest rates up. Net interest income (NII) methods use two (2) interest rate shock scenarios as follows: .. 1) parallel upward shock, 2) parallel downward shock. The bank performs additional calculations for automatic rate options for variable rate mortgages with built-in caps using the Black-Scholes model.

The EVE method calculates the cash flows of the principal and interest payments on balance sheet positions that are sensitive to interest rates, which are then discounted at the relevant interest rates. The EVE calculation uses theoretical cash flows multiplied by the reference rate (base rate) on the transaction date and then discounted by the risk-free rate on the reporting date. The IRRBB calculation uses a Core deposit which is part of a stable Non Maturity deposit with a very small interest rate change despite significant interest rate changes in the market.

The bank identifies core deposits and non-core deposits from stable funds (transactional retail, non-transactional retail and wholesale). The establishment of cash flows of basic deposits made using uniform slotting in time buckets over 1 (one) year with the duration of the period for each category refers to the AMF Circular Letter no. 12 / SEOJK.03 / 2018 regarding the Implementation of Risk Management and the standard risk measurement method for interest rate risk in the banking book (Interest rate risk in the banking book) for commercial banks.

The method for estimating the loan prepayment rate and term deposit early withdrawal rate uses historical data within one year. Interest rate shock scenarios used by the Bank to measure IRRBB are consistent with standard interest rate shock scenarios set out in the Financial Services Authority Circular Letter No.12 /SEOJK.03/2018 regarding the implementation of risk. Management and risk measurement Standard method for interest rate risk in the bank book for commercial banks.

IRRBB REPORT

Outstanding commitment and

HQLA after haircut, outstanding commitment and liabilities times run-off rate

HQLA after haircut, outstanding commitment and liabilities times run-

HIGH QUALITY LIQUID ASSET (HQLA)

CASH OUTFLOW

CASH INFLOW

REPORT ON CALCULATION FOR QUARTERLY LIQUIDITY COVERAGE RATIO (LCR)

COMPONENTSNo

QUARTERLY LIQUIDITY COVERAGE RATIO (LCR) REPORT Analysis for Bank Only

Total Rp & Va Current Account 31.18%

Time Deposit 18.79%

Analysis on a Consolidated Basis

Time Deposit 19.33%

Non-specified

Maturity < 6 Months ≥ 6 Months - <

1 Year ≥ 1 Year 1

TOTAL ASF

Net Stable Funding Ratio (NSFR) - Bank Only

ASF Component

Reporting Position (June 2022) Carrying Value Based on Residual Maturity (in million Rp)

Weighted ValueReporting Position (March 2022)

Carrying Value Based on Residual Maturity (in million Rp)

Weighted Value

1 Year ≥ 1 Year

Net Stable Funding Ratio (%)

RSF Component

Weighted ValueWeighted Value

Reporting Position (March 2022)

QUALITATIVE ASSESMENT ON NSFR

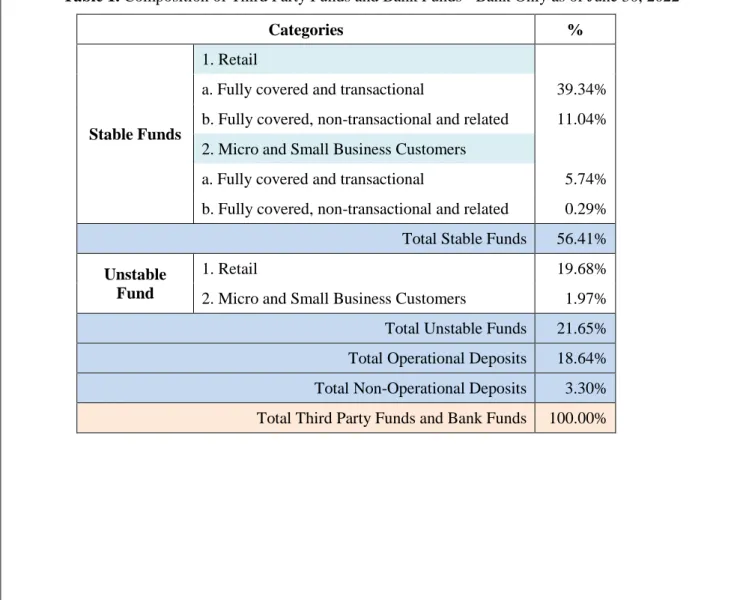

Analysis on Bank Only Financial Statement

Stable Funds

Unstable Fund

Micro and Small Business Customers 1.97%

Net Stable Funding Ratio (NSFR) - Consolidated

Reporting Position (June 2022)

Reporting Position (March 2022) Carrying Value Based on Residual Maturity (in million Rp)

308,863,013 TOTAL RSF

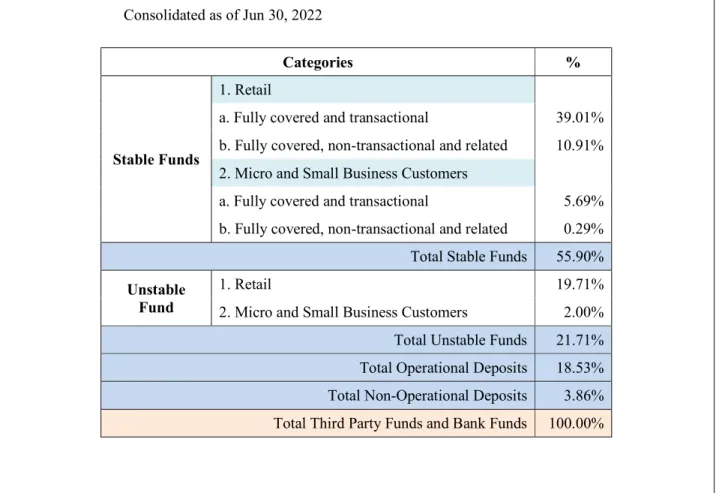

QUALITATIVE ASSESMENT ON NSFR Analysis on Consolidated Financial Statement

Micro and Small Business Customers 00%

Report On Asset Encumbrance - ENC as of June 30, 2022

Qualitative Analysis