No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form or by any means, electronic, mechanical, photocopying, recording, scanning, or otherwise, except as permitted under Section 107 or 108 of the United United States Act (1976). States Copyright Act, without the prior written permission of the publisher, or authorization by payment of the applicable per copy fee to the Copyright Clearance Center, Inc., 222 Rosewood Drive, Danvers, MA, fax or on the Internet at www.copyright .com. If you purchase this product directly from John Wiley & Sons, Inc. purchased, we have already registered your subscription to this update service.

Acknowledgment

Contents

Payroll Procedures and Controls 33

Payroll Measurements and Internal Reports 73

Payroll Taxes and Remittances 125

International Payroll Issues 237

Setting Up the Payroll Department 251 Chapter 18 Government Payroll Publications and Forms 263

Preface

This chapter addresses a number of metrics useful in determining the effectiveness of the payroll function, as well as a number of payroll reports not normally found in the standard report package that accompanies most payroll systems. This chapter covers the advantages and disadvantages of outsourcing the payroll function, as well as conversion, transition, control, measurement, management and service issues.

About the Author

Creating a Payroll System

Third, the internal payroll database must be backed up and stored, which is normally managed by the payroll provider. If the latter is the case, payroll must be aware of the variety of forms that are typically included in the new employee package.

Accumulating Time Worked

A lesser control is to post a list of barcoded or magnetically coded employee numbers next to each data entry station – this is a less accurate approach as the employee can still scan someone else's code into the terminal. In addition, there were many worksheets submitted daily by the facility's 412 direct workers, some of which were lost by employees or during the data entry process - this information had to be recreated, which could only be done with estimates of some the employee performed the work during this period.

Payroll Procedures and Controls

This procedure is used by the payroll administrator to change employee deductions in the payroll system. Go to the payroll software and open the PRINT option in the PAYMENTS menu.

Payroll Best Practices

Any of these approaches to the problem will reduce the number or timing of deduction changes, thereby reducing the workload on the payroll staff. It is common for the payroll staff to be responsible for keeping track of employees' vacation and sick time. A common task for payroll staff is to either manually or automatically track the vacation time earned and used by employees.

Likewise, the system can automatically enroll the employee in the company's 401k plan and enter the deductions into the payroll system. For companies with many employees, this can mean a significant reduction in the workload of payroll staff. These changes dramatically reduce the time accounting staff spend processing payroll.

Any change in payroll cycles may be met with opposition from the organization's employees.

Payroll Measurements and Internal Reports

To calculate the payroll transaction error rate, divide the total number of payroll errors for a payroll by the total number of payroll changes made during that payroll. The denominator should not be the total number of employees listed in the payroll, as many of them may be salaried (requiring no payroll change), and therefore not give a true picture of the total number of transactional changes applied to the payroll has not been made. . By compiling the total number of payroll entries in the system per employee, one can see if it.

As shown in the example, many types of insurance, such as short-term disability, will only cover a few employees, so the total number of payroll entries will appear relatively low. If it is the latter, then the same calculation is summarized for all employees in the group and divided by the number of employees in the group. Benefit costs are best measured per person, so the measurement should include all benefit costs in the numerator and the total number of full-time employees in the denominator.

The reporting can be expanded with other forms of compensation, such as the number of options granted.

Compensation

The amount of the incremental gross income must be the fair market value of the additional benefit, less its cost to the employee, less any deductions allowed by law. Club fees are taxable income to the employee, except for that portion of business-related obligations, which must be certified. The portion of the club's dues that is personal income to the employee may be treated as a salary expense to the employer for tax purposes.

The above scenario does not apply if the employer is the beneficiary of the life insurance policy. If these rules do not apply, the employer must withhold tax on the fair market value of the services. When this happens and the amount of the loan is greater than $10,000 and has an interest rate lower than the applicable federal rate (AFR), the difference is taxable income to the employee.

Show the share, if any, attributable to each employee in Box 8 of the employee's Form W-2.).

Payroll Deductions

However, if an employee fails to submit an expense report, they will be liable to the company for the amount of the advance provided. For example, the employer may pay 80 percent of an employee's health insurance and 50 percent of the portion of supplemental coverage that applies to the employee's family. Second, if an employee leaves the company, the amount of outstanding loans to the company for unrepaid asset purchases can significantly exceed the person's final paycheck, making it difficult for the company to collect on remaining loans.

It states the employer's obligation to withhold and remit the unpaid tax and also states the amount of the unpaid tax. Once the above types of salary have been accounted for, the payroll staff must decide which deductions can be made from an affected employee's salary before the amount of the tax collection is determined. The payroll officer must calculate the amount of tax to be withheld from each payslip.

An employee cannot be fired because of a garnishment order, and an employer who does so is liable for the employee's lost wages.

Payroll Taxes and Remittances

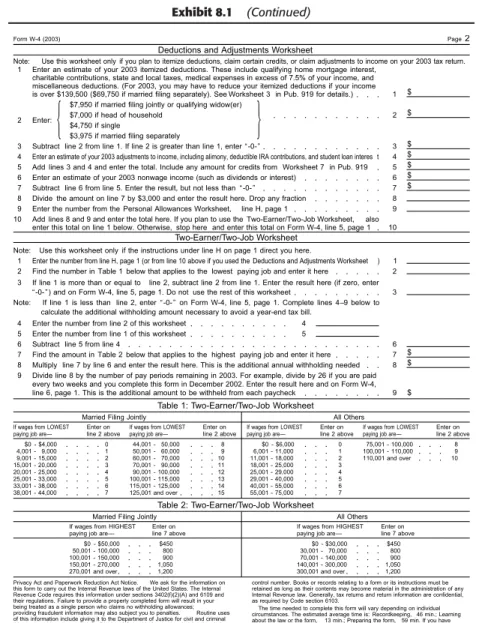

But you can choose to enter “-0-” if you are married and have a working spouse or multiple jobs. If none of the above apply, stop here and enter the line H number on line 5 of Form W-4 below. Enter a “1” on your tax return if you are filing a tax return as head of family (see conditions under Head of Household above). Please note: You cannot claim an exemption from additional tax.

The W-4 form must be sent to the IRS only if the employees submitting the forms are still employed at the end of the quarter. If you created a pension plan, it must have a separate EIN from that of the business entity. A new employer will generally fall into this category because the amount of the lookback period (which does not yet exist) is assumed to be zero.

If there were errors in the reported amount of income tax withheld from previous quarters of the same calendar year, enter the corrections on this line.

Benefits

As a result, she wants to reduce the amount of the cafeteria plan deductions that are removed from her paycheck. During the leave, the company changed the employee share of the insurance for all employees to $160. All earnings from the funds while they are held in the plan will also not be taxed until they are removed from the account.

The majority of contributions to these types of plans are in the employer's shares. An additional factor may be the age of the participant at the time of retirement. The option price at the time it is granted is not lower than the fair market value of the share.

However, if it uses an NSO plan, the company will receive a tax deduction equal to the amount of income the employee should recognize.

Payments to Employees

One downside is that any payroll error usually has to be corrected with a manual payment because so much time passes before an adjustment can be made on the next regular payroll. If a company outsources its payroll, there may be additional delays built into the process due to payroll entry dates set by the supplier. Write a check at your local bank for the total amount of the payment, which will be paid in cash.

After you have completed the calculation for each employee, cross the form to ensure that the bills and coins for all employees equal the total amount of the check that will be cashed at the bank. Take the completed form to the bank with the check and request the correct amount for each type of currency. Once all checks have been completed, make a final comparison of each against the payroll again, possibly including an independent recalculation of the payment to each person.

If a payroll supplier is used, they will print checks and send them to the company for distribution to employees.