The GAO concluded that mandatory audit firm rotation may not be the answer to audit independence and enhancing audit quality (GAO, 2003). In particular, the PCAOB wanted public input on mandatory audit firm rotation. Other countries have similarly struggled with the issue of mandating audit partner and audit firm rotation.

Italian office rotation requirements allow a firm to audit a client for up to nine years before the accounting firm must cancel the engagement (GAO, 2003). Spain introduced mandatory accounting firm rotation in 1988 and maintained the rule until it was repealed in 1995. They found that mandatory accounting firm rotation did not improve auditor independence, but instead found that accounting firm reputation had a greater influence on auditor independence (Ruiz -Barbadillo et al, 2009).

Canada implemented mandatory rotation of audit firms including banks, but banking legislation was revised in 1991 and. Arguments against mandatory audit firm rotation say that a new auditor will require a certain number of years in advance. Substantial prior research has explored the effects of audit firm rotation or audit partner rotation on overall audit quality.

These research articles include archival studies and experimental studies that attempt to draw conclusions regarding the effects of audit firm rotation on auditor's actual independence and audit quality.

HYPOTHESIS

Hypothesis 2b: Investors' willingness to invest does not increase under firm rotation relative to partner rotation. In this study, I also examine the relative effects of mandatory versus voluntary rotation, as well as no rotation on investors' willingness to invest in a company. For example, in the absence of mandated auditor rotation, companies may voluntarily choose to implement a policy that requires their audit partner or audit firm to be periodically rotated.

Therefore, I predict that voluntary turnover improves investors' confidence in financial reporting and investors' willingness to invest.

METHODOLOGY Participants

Scenarios were given to Ole Miss MBA students with those students taking on the role of investors tasked with making certain investment judgments and decisions. By asking them to take on the role of the investor, I am able to learn whether different treatments of auditor rotation affect their expectations of conservative financial reporting and their willingness to invest in the company. The experiment was conducted in two different sessions, with a total of fifty-five students participating in the study.

The participants were given a set of materials developed based on case materials used by Kaplan and Mauldin (2008). The background information on the company included relevant pre-audit balances such as sales, total assets and earnings per share. Participants are informed that the same auditing firm has audited IAP for the last five years.

However, depending on treatment condition, participants are provided with different information about auditor rotation policies. Materials in all treatment conditions described all possible treatments so that each participant was aware that other auditor rotation policies might exist. The materials were coded in this way so that each scenario was equally distributed to collect a large enough sample for results.

The materials included a description of the role of the audit committee and the audit partner to ensure that all participants had the same basic understanding of these two roles. A brief description of auditor rotation was also included to explain the role of rotation in audits. These were all included in the materials because I wanted the participants to all be exposed to the same basic knowledge, as some of the participants might have a background in accounting and would already know these concepts.

After reading the background and audit rotation requirements, the participants were told that the auditors had uncovered an audit discrepancy during the audit and that the discrepancy had caused the earnings per share to be overstated. The questions that followed asked the participants to report the level of earnings-per-share (EPS) they expected to eventually be reported in the financial statements. In addition, the participants were asked “How likely is it that you will invest in this.

RESULTS

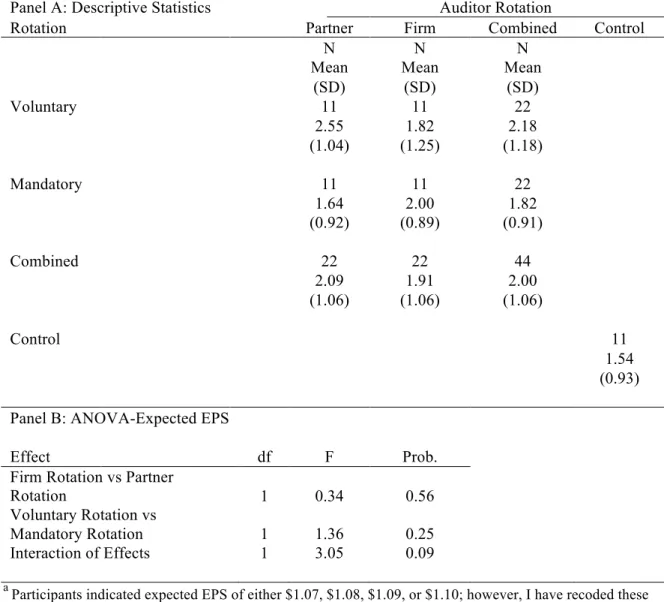

Recall that Hypotheses 1a and 1b predicted that investors' expectations of conservative reporting and their willingness to invest would increase under rotation regimes compared to no-rotation regimes. As shown in Table 3, Panel A, the mean and standard deviation (SD) of expected earnings per share are under both the no-rotation regime and the combined rotation regimes, respectively, indicating that lay investors expect more conservative reporting when there is no rotation of any kind. According to the results, investors are slightly more willing to invest without rotation compared to the rotation regime, which is inconsistent with hypothesis 1b.

Hypothesis 2a makes the null prediction that investors' expectations for conservative reporting will not be higher under the firm rotation regime relative to the partner rotation regime. Table 3, Panel A indicates that the mean and standard deviation of earnings per share are the same for corporate rotation and partner rotation, respectively. This indicates that investors expect more conservative reporting under firm rotation compared to partner rotation, supporting Hypothesis 1a. Hypothesis 2b also suggests that investors' willingness to invest will not be higher under firm rotation than under partner rotation.

The mean and standard deviation of investors' willingness to invest are and for firm and partner rotation, respectively, and are shown in Table 4, Panel A. According to the ANOVA in Table 4, Panel B, there is no significant difference between the two means. Firm turnover was only slightly higher than partner turnover, but not enough of a difference to say investors prefer one over the other.

Hypotheses 3a and 3b predicted the effects of voluntary and mandatory turnover on conservative reporting expectations and willingness to invest. Hypothesis 3a predicted that investors' expectations of conservative reporting increased under voluntary rotation compared to mandatory rotation. Hypothesis 3b predicted that investors' willingness to invest would increase under voluntary rotation compared to mandatory rotation.

Contrary to the prediction in Hypothesis 3b, investors are more willing to invest when mandatory rotation of audit partners or audit firms occurs than when they are rotated voluntarily. Panel B of Table 4 indicates that the difference in investor willingness to invest between the voluntary rotation conditions and the mandatory rotation conditions is not significant (F = 0.89, p = 0.35). It is important to note that although the main effects of partner/firm rotation and voluntary/mandatory rotation are not significant and do not support my hypothesis, these two variables interact to affect investors' expectations of conservative financials.

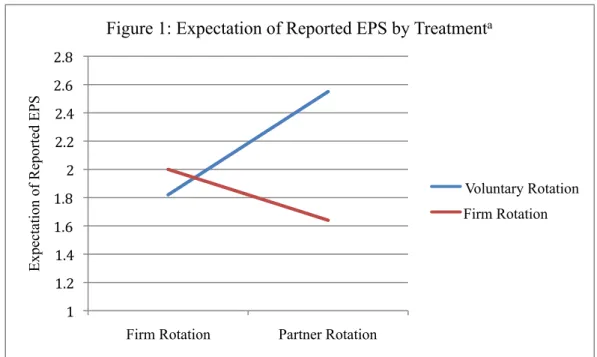

Specifically, as shown in Table 3 and Figure 1 , under firm rotation, there is little difference in investors' financial reporting expectations between the mandatory and voluntary rotation conditions (2.00 and 1.82, respectively). However, under the partner rotation condition, the difference in investor expectations between the mandatory and voluntary rotation conditions is larger (1.64 and 2.55, respectively).

CONCLUSION

After the scenario, you will be asked to give your impressions about the outcome and the behavior of management, the auditor and the audit committee, and then answer some questions about your background. Of the jurisdictions that do not require this rotation of accounting firms, some jurisdictions limit the number of years an audit partner can be involved in the audit of a particular company. Some voluntarily rotate their audit periodically or ask their accounting firms to rotate the audit partner.

Some jurisdictions impose these limits, but this jurisdiction does not require that the audit partner or audit firm be limited in the number of years associated with a company. Some jurisdictions impose these limits and this jurisdiction requires that the audit firm be limited in the number of years associated with a company. The audit committee of the Board of Directors is responsible for overseeing the performance of these activities by management and the independent auditor.].

Some jurisdictions impose these limits, but this jurisdiction requires that the audit partner be limited in the number of years associated with a company. Some jurisdictions impose these limits and this jurisdiction does not require the audit firm to be limited in the number of years associated with a company. The audit committee of the Board of Directors is responsible for overseeing the development of these activities by.

Some jurisdictions put these limitations in place, and that jurisdiction does not require the audit partner to be limited in the number of years associated with a business. The audit committee refers to and acts on behalf of the board and is composed of 3 members. No adjustment to the financial statements is required if management, the audit committee and the audit partner believe that the dollar amount of the audit difference is immaterial to the financial statements as a whole.

The objective of the audit is to assess risk management and to negotiate with management about misstatements in the financial statements. The audit report is the final product of the audit and the means by which auditors communicate audit findings to users. The role of the audit partner is to lead the team of auditors and lead the audit.

The audit partner is also in charge of gathering evidence to verify the financial statements. Actual earnings per share will miss the analysts' consensus forecast (be below) if management fully corrects the audit discrepancy.