There is a unique good in the economy and, at date 0, households are endowed with 1 unit of this good. They want to commit on 1 to pass on the efficiency gains from cost-free market access to depositors. The price of claims for production technology in the secondary market on date 1 is determined by arbitrage.

A unit invested in the storage technology on date 0 returns one unit of goods on date 1, or it can be exchanged for 1/pclaims on the productive technology for a return of R/p > Rat date 2. A unit invested in the productive technology on date 0 can be exchanged for p < 1 units of goods at date 1, or it can be held to maturity for a return of R. Households decide at date 0 whether to become sophisticated and whether to invest in the productive technology or invest in a bank.

At date 1, households that have invested in productive technology decide whether to sell their claims or hold them. The best that unsophisticated depositors can do with the fund withdrawn at date 1 is to invest in the storage technology until t = 2.

Equilibrium fraction of unsophisticated depositors

We can derive the amount of investment in the productive technology chosen by the banks and denoted by K. The rest, (1−q)(1−i)d1, is sold to sophisticated patient depositors in the secondary market.10 Thus the expression forK it is. 17) Note that all initial investment in manufacturing technology is made by banks. Banks are able to provide a lot of liquidity insurance, but there is relatively little investment in productive technology.

Banks offer little or no liquidity insurance, but there is more investment in productive technology. Thus, comparing two economies shows that A . 10Alternatively, the level of investment in the long-term technology can be derived by looking at what is not consumed on date 1; i.e. K= 1−qd1. This allows us to think about how changes in the share of advanced households affect capital accumulation and growth.

The OLG model

Banks use the capital they own and rent capital from sophisticated households to combine it with labor to produce the consumer goods. Consequently, a patient sophisticated household receives initial period t with Kt units of capital [rt+(1−δ)p−t ]Kunits of the consumer goods, where−t indicates the price of capital in units of the consumer goods at the beginning of the period capital market. The amount of consumer goods received by patient unsophisticated households is determined by the deposit contract.

Young households deposit their wage income in a perfectly competitive bank and enter into a deposit contract (d1t, d2t) before finding out whether they are patient or impatient. The bank uses part of the deposit to buy existing capital at the price p−t from old sophisticated households and distributes the rest of the deposit between storage and investment in new capital via the productive technology. A unit of the consumption good placed in stock at the beginning of the period yields a unit of the consumption good at the end of the same period, while a unit of the consumption good invested in the productive technology at the beginning of the period yieldsR > 1 units of capital at the beginning of period t+1.

Note that investment in the productive technology is the only way to produce new capital. The assumption that only banks are concerned with buying up existing capital, investing in productive technology and storing goods at the beginning of the period is harmless. As in the static model, young households decide whether or not to become sophisticated at the time banks offer the deposit contract (d1t, d2t), and there are proportional utility costs associated with becoming sophisticated.12.

12 The results in the case of a proportional resource cost or a fixed utility cost are similar and are available from the authors. Impatient depositors only value consumption in this subperiod, while patient depositors only value consumption in the first subperiod of t+ 1. As in the static model, patient sophisticated depositors claim to be impatient and banks are unable to prevent them from withdrawing .

The optimal contract offered by banks is essentially the same as in the previous section with X replacing R in the expressions below.

Equilibrium

One unit of capital at the beginning of period t can be rented out to earn rt and the unamortized capital can then be sold to banks at the price p−t. This yields a quantity rt+ (1−δ)p−t of the consumer good at the end of the first subperiod in t. The consumer good can then be invested in the long-term technology to produce new capital at the beginning of period t+1.

Note, X >1 implies rt ≥δp−t , the condition that old households strictly prefer to rent their capital before selling it to banks. For the remainder of the paper, we drop the indices of det and Θt as they are time invariant. Proposition 4 The growth rate of the economy decreases with the cost of becoming sophisticated, ie.

This proposition indicates that economies with a smaller fraction of unsophisticated depositors grow faster than economies with a larger fraction. Intuitively, a greater cost of becoming sophisticated leads to less sophisticated households participating in the capital market.

Welfare

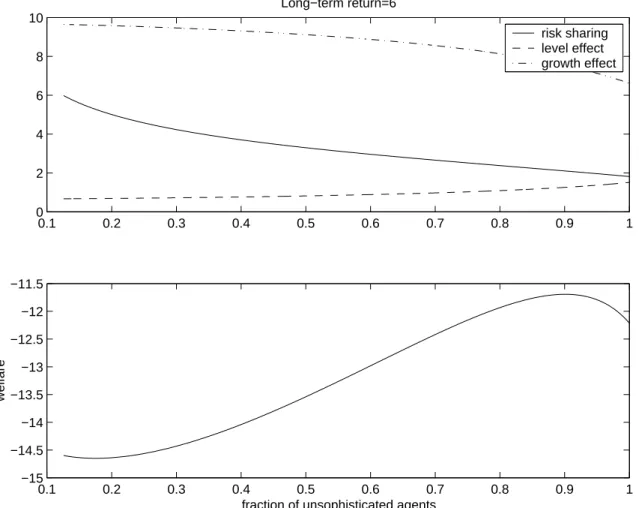

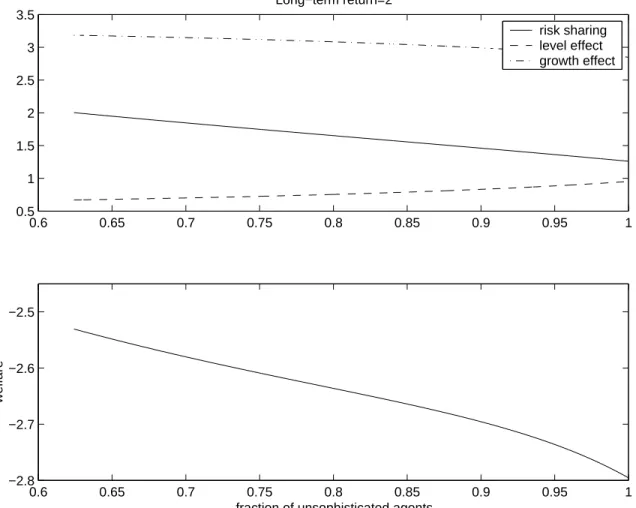

Increasing the cost of becoming sophisticated (ie, increasing χ) has an ambiguous effect on d1t and d2t, as it simultaneously increases G and decreases ρ. At t= 1, only the effect on G is present and thus a greater cost of becoming sophisticated increases the expected utility of this generation, as in the static model. An increase in χ also decreases Θ, which corresponds to more risk sharing, as in the static model.

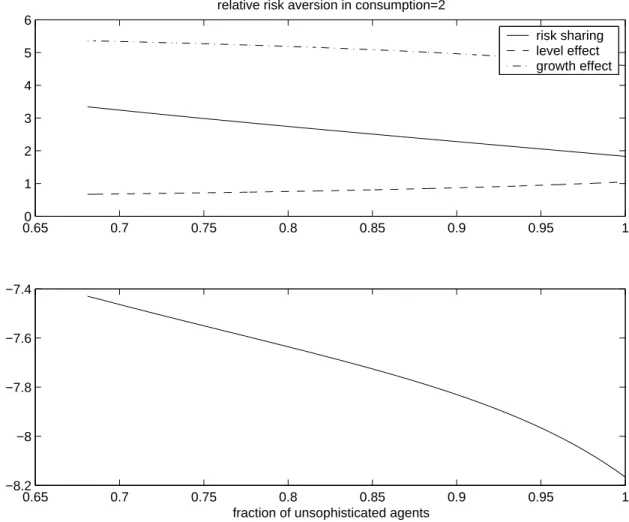

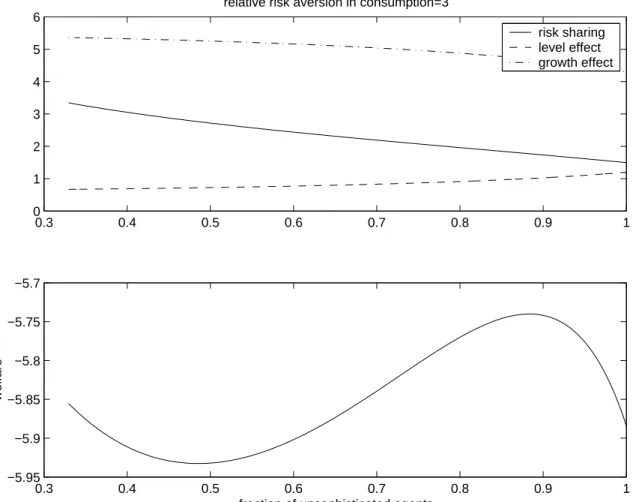

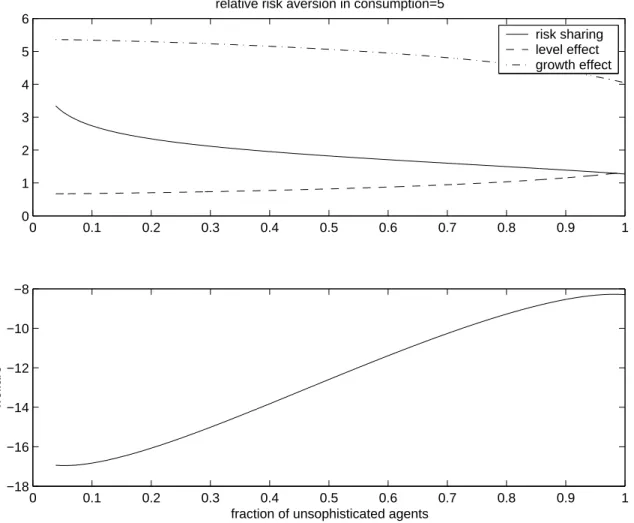

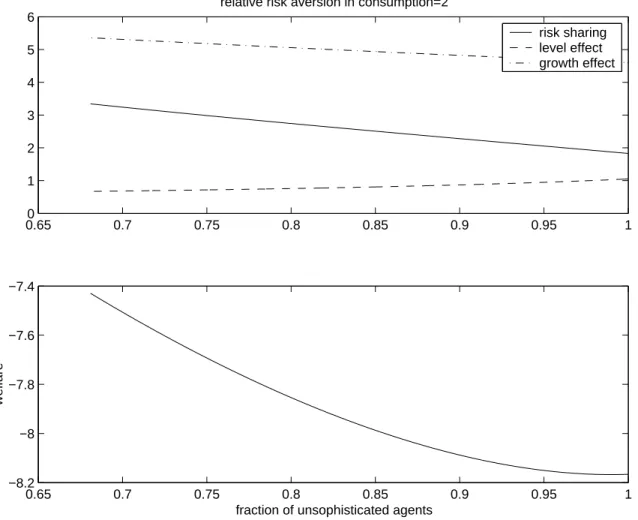

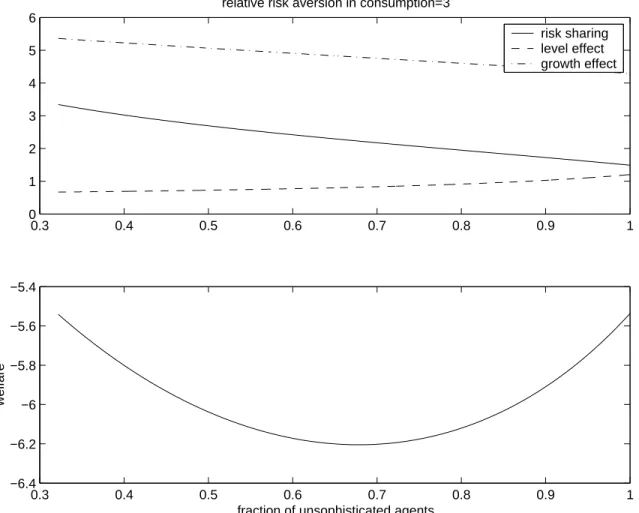

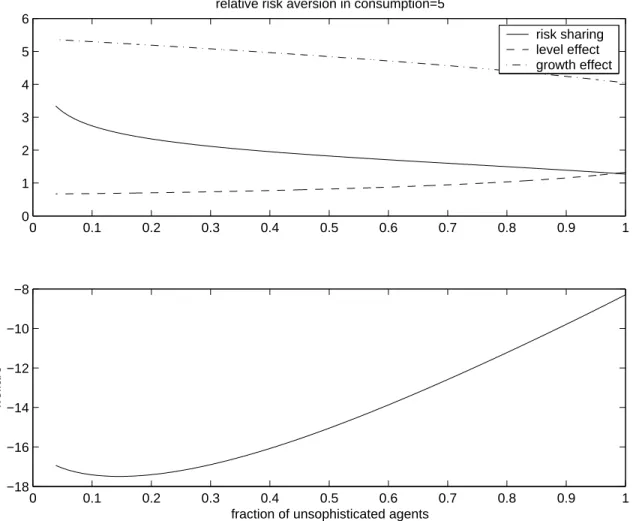

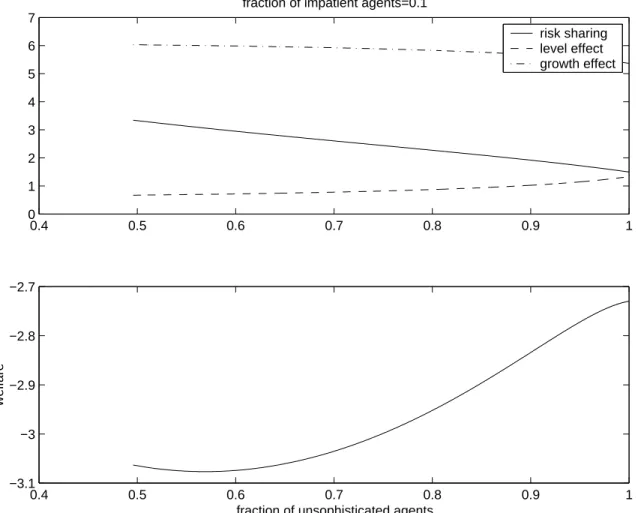

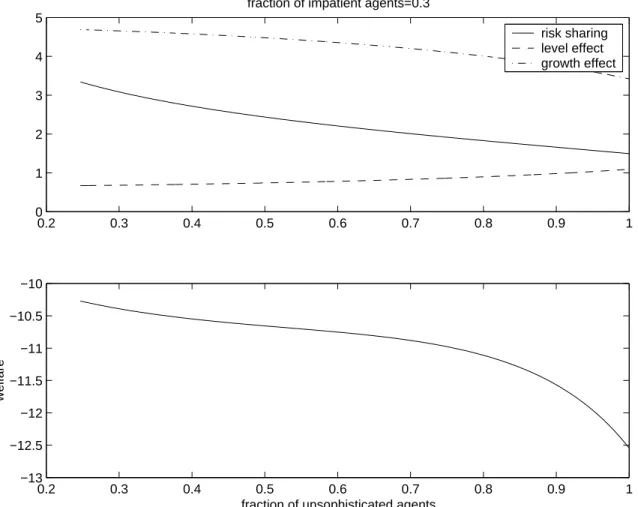

It follows that an increase in the cost of sophistication simultaneously increases risk sharing and decreases growth, leading to a trade-off between the two effects. Instead, we rely on numerical examples to get an idea of the trade-off between risk-sharing and welfare-enhancing growth. When risk aversion is low, α = 2, welfare is maximized at a lower value of χ, which implies that only 61 percent of agents choose to remain unsophisticated and banks do not offer risk sharing.

In this case, banks are not limited in the amount of risk sharing they can provide, but growth is slow. If q is high enough, q = 0.3, then welfare is greatest when banks do not provide risk sharing and growth is high. This result could arise from the fact that banks provide little risk sharing when q is small, so that growth is fast even if no household becomes sophisticated.

For our baseline parameterization, welfare is almost the same with no risk sharing or with unlimited risk sharing by banks, suggesting that one of the extreme cases is better than intermediate cases. To summarize, we find that welfare may not be monotonic in the cost of becoming sophisticated because of the trade-off between risk sharing and growth. This paper contributes to the literature comparing the relative performance of financial intermediaries and markets by studying an environment in which a trade-off between risk sharing and growth arises endogenously.

The government can influence the financial system by changing the costs of investing directly in the financial market.

Proof of proposition 4

The resource-cost case

Taking the deposit contract as given, the equation to determine it is now given by In other words, the smaller C is, the greater the proportion of households that choose to become sophisticated. The analysis so far is homomorphic to the case with utility costs, with the basic connection C1−α = χ.

Unlike in the case with a utility cost, here there are two opposite effects of a resource cost on the growth rate, ρ. On the other hand, as more households become sophisticated, they use resources to pay the costs. We perform a similar set of numerical experiments for this resource cost case as we do for the utility cost case, using the same set of baseline parameter values, and obtain similar results.

The fixed-cost case

The RHS is a function of iso. We can differentiate the LHS with respect to c and the RHS with respect to i to obtain the partial derivative ∂i/∂c. We consider the case with fixed energy costs because the basic conclusions for the case with fixed energy costs are similar. 17In a Nash equilibrium, agents adhere to the terms of the contract, and if they are greater than 1, no agent will choose to be refined.

In this case, all relations to (22) are the same as in the text of the paper, and the condition that determines its equilibrium value is now given by. We now provide a local result on the uniqueness of equilibrium and the inverse relationship between the cost of becoming sophisticated and the growth rate. We claim that for a small positive U, there exists a unique equilibrium, with its equilibrium value satisfying (51), and the equilibrium growth rate being negatively related to U.

This means that the greater the cost of becoming sophisticated, the fewer agents will choose to do so. Together, this implies that, for small U, a higher cost of becoming sophisticated results in a lower growth rate. We now provide a global result on the uniqueness of equilibrium and the inverse relationship between the cost of becoming sophisticated and the growth rate.

We now prove that, under (57), and for all U in the range specified in (52), there exists a unique equilibrium, with its equilibrium value satisfying (51) and the equilibrium growth rate being negatively related to U . This means that a greater cost of becoming sophisticated leads to fewer agents choosing to do so. Together, this implies that, for all U satisfying (52), a greater cost of becoming sophisticated results in slower growth.

If the cost of becoming sophisticated is zero, then the welfare assessed by the equilibrium allocations is the same in a bank-oriented financial system and in a market-oriented financial system. If the costs of becoming sophisticated are positive, the welfare assessed by the equilibrium allocations may differ in a bank-oriented financial system from that in a market-oriented financial system. A Welfare Comparison of Intermediaries and Financial Markets in Germany and the United States.” European Economic Review.