The thesis entitled THE EFFECT OF EARNINGS MANIPULATION RISK AND COMPANY MANAGEMENT RISKS ON THE EXPANSION OF AUDIT PLANNING, prepared and submitted by Bella Firna in partial fulfillment of the requirements for a degree in the Faculty of Management, was reviewed and found to meet the requirements for the thesis, which correspond to the examination. This study will analyze the impact of earnings manipulation risk and corporate governance risk on the extension of audit planning.

Company Profile

- Company XYZ International

- Company XYZ

- Vision, Mission, Values, and Services

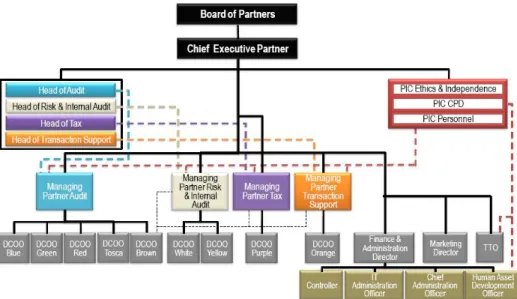

- Organization Structures

Company XYZ consists of CPA Aryanto, Amir Jusuf, Mawar and Saptoto and other business units under the name Company XYZ. To be the right partner for their stakeholders, Company XYZ provides the best services by sending professionals and conducting the audit process properly.

Problem Identified

Statement of Problem

Research Objective

Significance of Study

Theoretical Framework

Scope and Limitation

Hypothesis

Definition of Terms

Based on Nelson et al., (2002), the likelihood of earnings manipulation is reduced due to the intervention of the accountant. Based on Figure 4.4, the partial regression graph of the risk of earnings manipulation towards audit planning shows that the data is normally distributed, the points are evenly distributed and do not form a pattern, the points are above 0 and below 0 almost be in balance.

LITERATURE REVIEW ................................................................. 12-25

Audit Standard

Based on Arens and Loebbecke (2000), auditing standards are general guidelines to help auditors fulfill their professional responsibilities in the audit of historical financial statements. In Indonesia, Auditing Standard consists of ten standards issued and approved by Institute Akuntan Publik Indonesia (IAPI), includes three general standards, three work field standards and four reporting standards, which are elaborated in Persayatan Standard Auditkunde (PSA) or known as Generally Accepted Auditing Standards (GAAS) in the United States.

Corporate Auditing Theory

Audit Risk

Audit Planning

16 (reliability) determines for each account balance and audit objective, how much evidence should be collected (Hayes, et al., 2005).

Creative Accounting

When resulting misstatements are discovered, the market can be unforgiving, causing a steep decline in debt and equity prices (Mulford and Comiskey, 2002, p-8).

Earnings Manipulation

According to Schipper (1989), earnings management is the intervention in the process of external financial reporting to achieve personal benefits. The concept of earnings management comes as the direct consequences of the manager's or accountant's efforts to manage accounting information, especially earnings, for personal and/or business reasons.

Corporate Governance

Each of the members of the board of commissioners, including the chairman, has an equal position. The board of directors, as a corporate body, must function and be collegially responsible for the company's management. However, each board member's performance of tasks remains a collective responsibility.

The position of each respective board member, including the president director, is equal. The chairman's duty as primus inter pares is to coordinate the board's activities.

The Relationship between Earnings Manipulation Risk and Audit

Planned audits increase until the fraud risk is consistent with the purpose of SAS No.82.

The Relationship between Corporate Governance Risk and Audit

H0: Earnings manipulation risk and corporate governance risk have no impact on the expansion of audit planning. H1: Earnings manipulation risk and corporate governance risk have an impact on the expansion of audit planning. 53 Earnings Manipulation Risk (X1) and Corporate Governance Risk (X2) versus the dependent variable which is Audit Planning (Y).

The researcher concludes that the risk of earnings manipulation has a significant impact on audit planning expansion. In part, earnings manipulation risk and corporate governance risk have a significant impact on audit planning expansion.

METHODOLOGY ........................................................................... 26-43

Research Time and Place

Research Instrument

- Primary Data Collection

- Secondary Data

The researcher conducted the research on the company from December 23, 2011 to January 25, 2012. Secondary data refers to the company XYZ; therefore, the writer will find information about XYZ company using internet media, magazines and several related literatures that support the research.

Sampling Design

- Population

- Sampling

Testing the Hypothesis

- Operational Definition and Variable Measurement

- The Technique of Data Analysis

- Data Quality Test

- Descriptive Statistic

- Normality Test

- Multicollinearity Test

- Heteroscedasticity Test

- Hypothesis Test

- Coefficient Simultaneously Correlation Analysis (F Test )

- Coefficient Partial Correlation Analysis (t Test )

According to Hair et al., (1998), the quality of the data resulting from the use of the research instrument should be evaluated through the reliability test and the validity test. The multicollinearity test is used to find out whether there is a linear relationship or not of the independent variable in the regression model. The heteroskedasticity test is used to find out whether there is inequality variance from the residual model in the regression.

Ftest is used to determine whether the independent variables collectively have a significant effect on the dependent variable (Priyatno, 2010). In research, the ttest is used to determine whether in a regression model the independent variables (X) have a partially significant influence on the dependent variable (Y) (Priyatno, 2010).

Data Result of Validity and Reliability Testing

- Validity Test Result

- Reliability Test Result

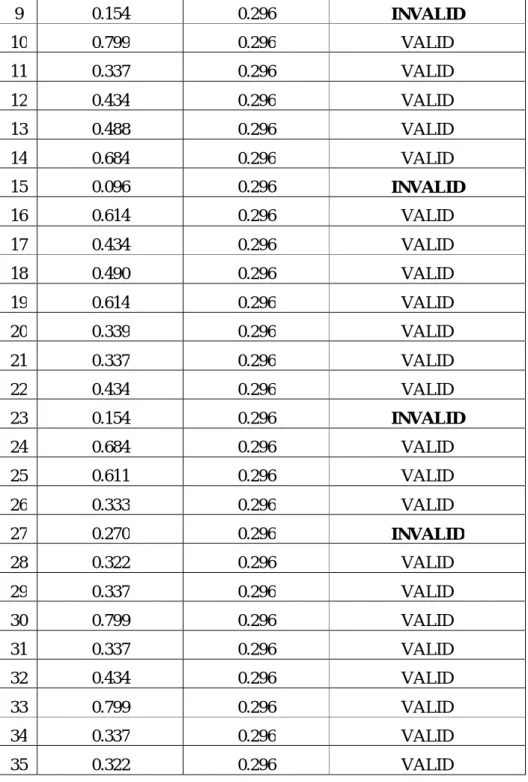

The researcher decides to eliminate the questions and use all the remaining questions that are valid as many as 31 questions. SPSS provides the ability to perform the reliability test using Cronbach Alpha (α), which is a variable that will be said to be reliable if given the value of Cronbach Alpha (α). Sources: Statistical of Package for Social Science (SPSS) and Primary Data Based on Table 3.4, it is shown that the value of Cronbach's Alpha is greater than 0.80, which proves that the variable is reliable and strong.

Limitation

This study aims to determine the impact of earnings manipulation risk and corporate governance risk on audit planning expansion. Therefore, H1: Earnings manipulation risk and corporate governance have significant impact on audit planning expansion is accepted. 55 Based on Table 4.10, it appears that the Earnings Manipulation Risk (EMR) has a significant impact on the expansion of the audit planning.

The researcher concludes that Corporate Governance Risk has a significant impact on the expansion of audit planning. Therefore, the first half of the year, which states that the risk of earnings manipulation and the risk of corporate governance has a significant impact on the expansion of audit planning, is accepted.

ANALYSIS AND INTERPRETATION .......................................... 44-59

Gender

Based on Table 4.1, most respondents in this research are male, as many as 51 people with a percentage of 68%.

Age

Education

Audit Experiences

Statistic Descriptive

Interpretation of Data Normality Test

It can be said that the audit experience of this research is categorized as standard. 48 a normal regression plot standardizes the residual with earnings manipulation risk and corporate governance risk as the independent variable and audit planning as the dependent variable almost forming a straight line. The researcher concludes that the data followed a linear relationship model and the standard deviation followed a normal standardized distribution.

Interpretation of Multicollinearity Test

Based on table 4.6 below, the value of Tolerance due to earnings manipulation risk (EMR) and corporate governance risk is 0.958 which is greater than 0.1. Based on Table 4.11, shows that Corporate Governance Risk (CGR) has a significant impact on the expansion of audit planning. 57 Figure 4.5 Corporate Governance Risk for Audit Planning Source: Statistical Package for Social Sciences (SPSS) and Primary Data.

Based on the hypothesis test of earnings manipulation risk above, it is found that earnings manipulation risk has a significant influence on the extension of audit planning. Based on hypothesis testing of corporate governance risk in relation to audit planning above, it is found that corporate governance risk has an influence on the expansion of audit planning.

Interpretation of Heteroscedasticity Test

Interpretation of Hypothesis Test

- Model Evaluation

- Regression Model Summary

- Interpretation of F test

- Interpretation of t test

From the above formula it is explained that independent variables namely Earnings Manipulation Risk (EMR) and Corporate Governance Risk (CGR) have a positive and significant impact on the expansion of the dependent variable (Audit Planning) which is determined by the positive value of B. and the acceptable significant value < 0.1. Based on Table 4.9 ANOVA table, the F value is 36.611, which is greater than F table 2.38 with sig 0.000 lower than alpha 0.1. Thus, the model can conclude that earnings manipulation risk and corporate governance risk have a significant impact on audit planning expansion in Company XYZ. H0: Earnings manipulation risk and corporate governance have no significant impact on the expansion of audit planning, is rejected because the above value shows that the contribution and relationship of the independent variable to the dependent variable is quite strong, proven by the significant value 0.000 less than 0.1 .

Earnings manipulation risk (X1) has an impact on the expansion of the audit planning (Y), evidenced by the positive B-value 0.175, which means that if Earnings manipulation increases by 1 unit, the audit planning also increased by 17.5%. Corporate Governance Risk (X2) has an impact on the expansion of audit planning (Y), evidenced by the positive B-value 0.770, which means that if earnings manipulation increases by 1 unit, the audit planning also increased by 77%.

Interpretation of Result

- The Impact of Earnings Manipulation Risk on the Extension of Audit

- The Impact of Corporate Governance Risk on the Extension of Audit

This result means that the higher the corporate governance risk the auditor faces from his client, the longer it will take to prepare the audit plan. Companies start to become aware of the importance of good corporate governance for their company. In general, the risk of earnings manipulation and the risk of corporate governance have a significant impact on the extent of audit planning at the 90% confidence level, which means that the risk of earnings manipulation and the risk of earnings manipulation are the most important indicators. important for the scope of Audit Planning at XYZ Company.

The Corporate Governance Risk variable is the most dominant factor, which means that Company XYZ considers Corporate Governance Risk as the most influential factor on the expansion of audit planning. To answer the following points, the respondent faces the risk audit of the effectiveness of the client's business management activity.

CONCLUSIONS AND RECOMMENDATIONS ........................... 60-62

Recommendations

Basically, for the next researcher who wants to do further research on this matter, it is important to recognize and consider many other factors that affect the relationship between the risk of profit manipulation and the risk of corporate governance when planning an audit, such as the size of the public accounting firm, culture , the auditor's experience and knowledge of the client. The researcher recommends the auditor to be more responsive to potential risks that may exist with clients, especially profit manipulation risk and corporate governance risk, as these risks often occur with the client, which is defined as fraud. The researcher recommends companies (clients) to be more aware of the quality of corporate governance, which can control the work of management, so that management can issue financial statements that can be truthful to the public.

Huphangan Antara Risiko Manipulasi Earnings and Risk Corporate Governance dengan Perencanaan Audit (Studi Empiris pada Auditor se-Jawa). To answer the following points, the respondents consider the audit risk, which is an earnings manipulation risk, to accept the assignment in the client. There is an element of intent to manipulate earnings in the presentation of the client's financial statements.

Audit committees do not report to the board on the risk facing the client and risk management performed by directors.