Hypothesis 3, which is specifically formulated; Board tenure has a negative effect on corporate governance disclosure. This research was conducted to determine the effect of institutional ownership, blockholder ownership and Board tenure on corporate governance disclosure in Indonesia.

Literature Review (bold, 12 pt)

The introduction should contain (sorted and sequentially) a general background and a literature overview (state of the art) as the basis of the brand new research question, statements of the brand new scientific article, main research problems and the hypothesis. The last part of the introduction should state the purpose of writing the article. In the format of a scientific article, it is not possible to write down the references as in the research report.

They should be presented in a literature review to demonstrate the novelty of the scientific article.

Research Method (bold, 12 pt)

Results and Discussion (bold, 12 pt)

Conclusion

The references used are listed in alphabetical order by author's name with the sample format (books and journals) as is common in the bibliography.

INSTITUTIONAL OWNERSHIP, BLOCKHOLDER OWNERSHIP,

AND THE BOARD’S TENURE TO DISCLOSURE OF

CORPORATE GOVERNANCE

INSTITUTIONAL OWNERSHIP, BLOCKHOLDER OWNERSHIP, AND THE BOARD’S TENURE TO DISCLOSURE OF

34;Corporate governance, privatization and financial performance of Indonesian BUMN", International Journal of Revenue Management, 2018. Mengenai tingkat plagiarisme, jika diperbolehkan, kami mohon untuk tidak mencantumkan bibliografi pada saat pengecekan plagiarisme, karena bibliografi kami adalah hampir sepenuhnya plagiat.

INSTITUTIONAL OWNERSHIP, BLOCKHOLDER OWNERSHIP, AND THE BOARD’S TENURE TO DISCLOSURE OF CORPORATE GOVERNANCE

TotokDewayanto

Rahmawati

Djoko Suhardjanto Universitas Sebelas Maret

ABSTRACT

INTRODUCTION

The ownership structure and tenure of the Board of Directors is expected to increase the value of the company. It is based on the assumption that an institution has a level of caution and good judgment in making decisions, so that when an institution has a share of interests in a company, it is expected that the management of the company will be good because of good supervision. Blockholder ownership shows a certain concentration in the company's ownership structure, where the ownership of the shares is concentrated in certain parties that have shares above 5%.

Another thing that is also thought to influence corporate governance disclosure is Board tenure. The duration of the mandate is closely related to the increase in the level of experience and knowledge. Research on the impact of institutional ownership, blockholder ownership, and Board mandate on corporate governance disclosure has been conducted by previous researchers.

However, researchers have other considerations in using the index issued by UNCTAD, where this index is more internationally accepted.

THEORETICAL FRAMEWORK AND DEVELOPMENT HYPOTHESIS

The proportion of ordinary shares owned by the block, at least 5% of the total issued shares, is used to measure the variable ownership of the block holders. According to Edmans (2014), the important role played by blockholders motivates them to pay for the monitoring or monitoring of the company's management performance. Meanwhile, Nerantzidis&Tsamis (2017) found no influence of blockholder ownership on corporate governance disclosure.

In Indonesia, the Financial Services Authority Regulation, POJK No. 11/2017 requires Board members to declare ownership of at least 5% of the paid-up capital in a listed company. However, Vafeas (2003) explained that with a long tenure, a board can actually develop knowledge of the company and change its business activities for the better. In this study, tenure is the time the board of directors has served in the company, as measured by the average number of years the board of directors has served in the company.

A board with a long term also means that it has more interaction and information (Rutherford .. amp;Buchholtz 2007). Research conducted on the effect of board tenure on corporate social responsibility disclosure, with similar characteristics to corporate governance disclosures, results show that board tenure has a negative effect on voluntary CSR disclosures (Sari, et al. 2016).

RESEARCH METHODS

The term of office can be interpreted as the length of time a person has to hold a position. 2010) stated that the relatively long-standing relationship between the board tended to increase the existence of agency problems and reduce the oversight process by the board. On the one hand, the close relationship with the directors is not good either, even the objectivity of the supervision will be threatened. Berberich&Niu (2011) found that councils with long tenure had a negative impact on management because the effectiveness of management oversight would be reduced.

Other studies find a different conclusion, that a long mandate means that the council will become more critical, instead of a short mandate (Bebchuk & Cohen 2003).

Definition of Variable Operations

Dependent disclosure of corporate governance (which is a UNCTAD (United Nations Conference on Trade and Development) recommended index consisting of 52 items (UNCTAD, 2011). Average tenure (years) for members of the Board (Oliveira, et al. 2016) Using the index of the UNCTAD (2011) recommendations is based on an analysis conducted by the agency and includes Indonesia, so it is appropriate when used in research focusing on firms in Indonesia.

The analytical tool used is multiple linear regression analysis to find the effect of independent variables on the dependent (Ghozali, 2011) with the following models:.

RESULTS AND DISCUSSION

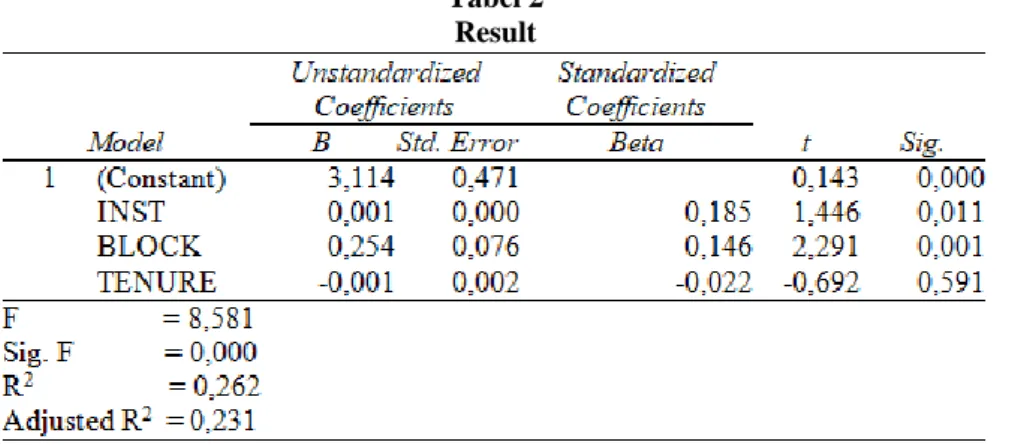

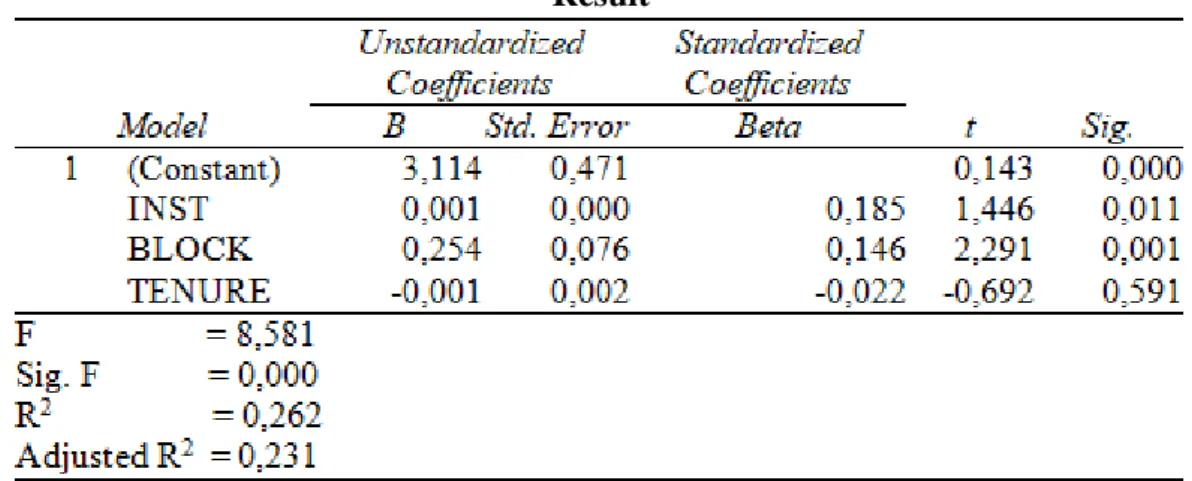

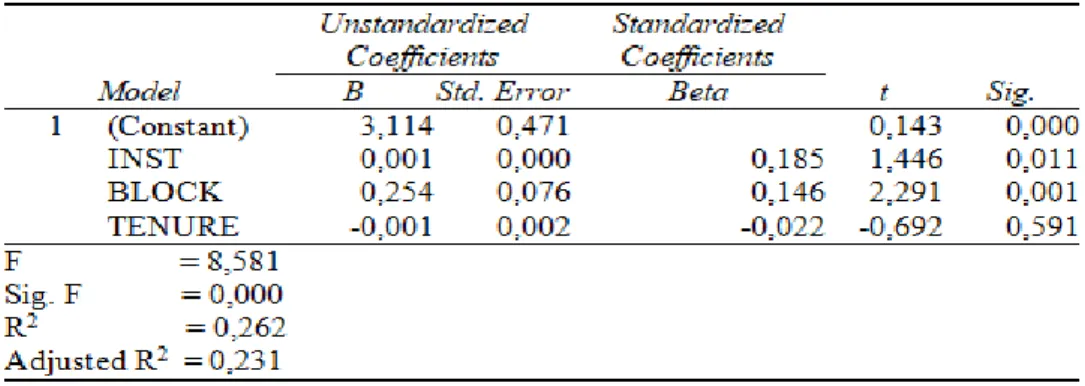

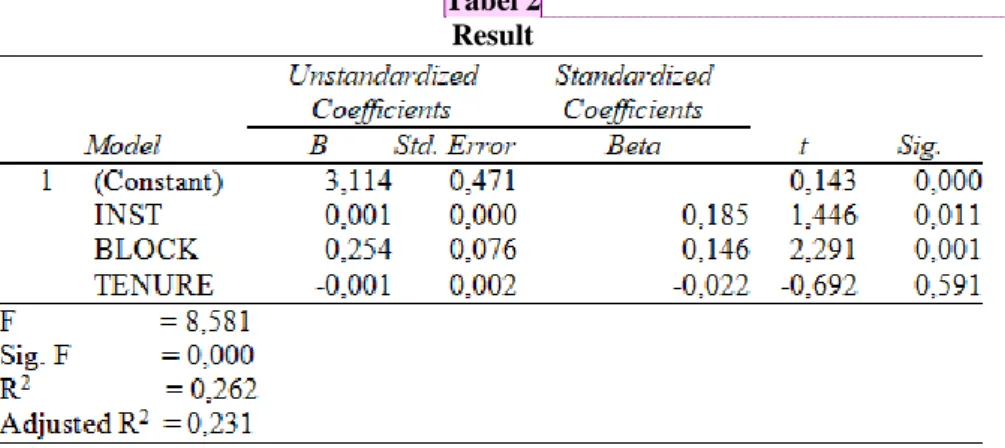

Hypothesis 1, which is formulated namely; institutional ownership has a positive effect on corporate governance disclosure. From the test results with multiple linear regression analysis, the results obtained t value of 1.446 and a significance value of 0.011. This shows that hypothesis 1 is accepted; institutional ownership has a positive effect on corporate governance disclosure.

Hypothesis 2, which is formulated namely; blockholder ownership has a positive effect on disclosure of corporate governance. This shows that hypothesis 2 is accepted; Blockholder ownership has a positive effect on disclosure of corporate governance. This shows that hypothesis 3 is rejected; there is no influence of the board's term of office with disclosure of corporate governance.

Whether the average board has no effect on the level of corporate governance disclosure.

CONCLUSION

This finding supports the research results of Al-Bassam et al. 2015), who says that institutional shareholders play an important role in controlling the company's operations, as they have majority voting rights and access to management through special information channels. From the multiple linear regression analysis test results, the results obtained a t value of 2.291 and a significance value of 0.001, below 0.05. Agency theory argues that effective control, which can reduce agency costs and compel managers to act in the interests of shareholders, has become a major concern for corporate governance.

Edmans (2014) argues that blockholders play an important role in governance because the size of their shares in the company provides an impetus to bear the costs of monitoring managers. This finding supports the findings of research conducted by Gan, et al (2013), which states that higher blockholder ownership offers what investors want in terms of better oversight and discipline of managers. From the multiple linear regression analysis test results, the results obtained a t-value of -0.001| and the significance value of 0.692, above 0.05.

Blockholder ownership, which also has a positive effect on corporate governance, is considered to be able to increase corporate governance disclosure because it provides an incentive for blockholders to bear the costs of monitoring manager performance because their shares are classified as high, so they are highly dependent on the company's performance.

RESEARCH LIMITATIONS AND SUGGESTIONS

Ownership structure, board characteristics and corporate governance disclosure in GCC banks: what about Islamic banks. Impact of board characteristics on corporate governance disclosure practices of Indian listed firms. A study of corporate governance and disclosure practices of tangible and intangible asset-dominated firms and their relationships.

Accept Submission

Ekuilibrium] Editor Decision

Ekuilibrium] Proofreading Request (Author)

Ekuilibrium] Copyediting Review Request

Editorial Process

Ekuilibrium] Submission Acknowledgement

Institutional Ownership, Blockholder Ownership, and the Board’s Tenure

Literature Review

Institutional ownership is the relationship of share ownership by shareholders in the form of an institution. Research by Al-Bassam, et al. 2015) found that there was a positive effect of institutional ownership on corporate governance disclosure. The theoretical framework developed by Jensen &Meckling (1976), based on agency theory and ownership structure, plays a central role in the corporate governance literature.

Bonazzi & Islam (2007) argue that effective controls that can reduce agency costs and force managers to act in the best interests of shareholders have become a major concern for corporate governance. The results of empirical studies on the effect of shareholder ownership on corporate governance disclosure cannot be concluded. Al-Bassam, et al. 2015) shows that blocking has a significant negative effect on governance disclosure in companies registered in Saudi Arabia.

Given the effectiveness of blockholders as a tool for corporate governance, and their ability to exert pressure on managers to increase accountability, transparency and disclosure practices, it is hoped that a greater proportion of blockholder ownership is associated with disclosure of good corporate governance.

Research Method

Ekuilibrium: Jurnal Ilmiah Bidang Ilmu Ekonomi Vol. economic for the individual shareholder to incur significant monitoring costs because they will receive only a small benefit. Independent institutional ownership Number of company shares owned by the institution (INST) (Deumes and Knechel, 2008). Before testing the hypothesis with multiple linear regression, the data feasibility test is first performed through the normality test and the linearity test.

Then the multicollinearity test, the heteroscedasticity test and the autocorrelation test are also performed to ensure the feasibility of the data. Model testing is analyzed by determination, F-test and t-test to find out how much influence the independent variables have on the dependent variable.

Results and Discussion

Hypothesis 1, which is formulated namely; institutional ownership has a positive effect on corporate governance disclosure. Ownership by institutions is considered to increase the transparency of corporate governance because it is generally the majority shareholder. There are several limitations in this study, namely that the research only focuses on three independent variables; institutional ownership, blockholder ownership, and board tenure, which cumulatively affect 23.1% of the dependent variable; corporate governance disclosure.

Downs Corporate Boards and Ownership Structure as Antecedents of Corporate Governance Disclosure in Saudi Arabian Publicly Listed Corporations", Business & Society. Niu Director Busyness, Director Tenure and the Likelihood of Encountering Corporate Governance Problems", SSRN Electronic Journal. Huang Intellectual capital disclosure in the context of corporate governance", International Journal of Learning and Intellectual Capital 10 (1).

Chakroun Ownership structure, board characteristics and corporate governance disclosure in GCC banks: what about Islamic banks?”, International Journal of Accounting, Auditing and Performance Evaluation 12 (4).