153 companies in the environmentally sensitive sector do not disclose this, as disclosure of environmental data can lead to an increase in operating costs. The application of GCG improves firm performance, which benefits stakeholders (Riana & Iskandar, 2017). This finding is consistent with Rahmanita (2020), who pointed out that CED and corporate environmental performance have influenced firm value. 2021) argued that improving environmental disclosures reduced shareholder value, which could have a negative impact on the company.

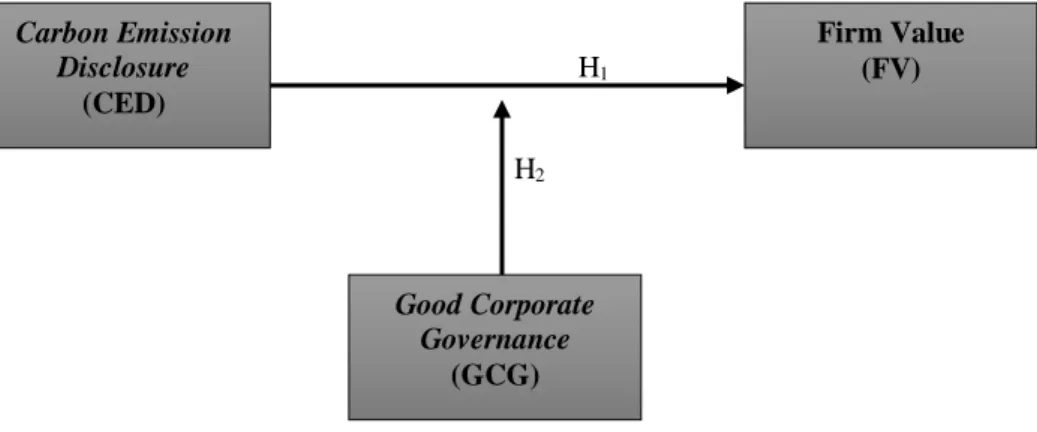

The model shows the relationship between carbon disclosure and firm value with the moderating effect of good corporate governance. The social contract relationship gives the company the authority to use economic resources in the long term (Ghozali & Chairiri, 2007). In carrying out its activities, the company continues to produce carbon emissions that accumulate in the atmosphere and potentially threaten global climate change.

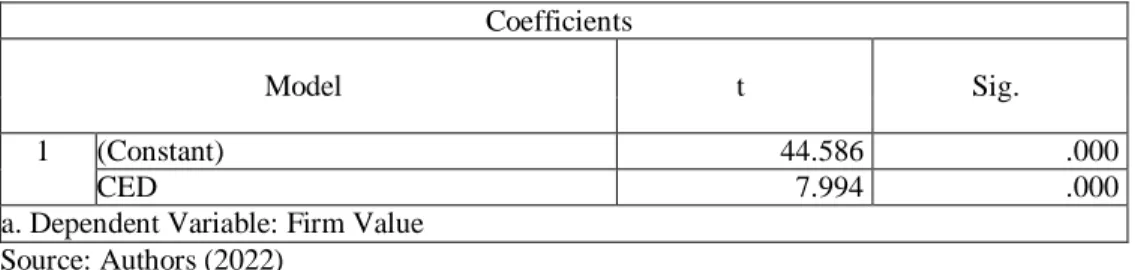

According to Fakhrudin and Sopian (2001), firm value is a condition achieved by a company as an indication of stakeholders' trust in the company through activities spanning several years, from the company's foundation to the present day. The stakeholder's wealth can increase when the company's value improves (Tjahjono, 2013). The first hypothesis tests the impact of the disclosure of CO2 emissions on firm value.

Thus, CED embodies the principle of GCG, which can add value to the business (Mufidah & Purnamasari, 2018). The better the governance of the company, the higher the social and environmental information, which increases the value of the company (Nahda & Harjito, 2011). Indeks Pengungkapan Corporate Governance – IPCG (translated as the Good Corporate Governance Disclosure Index – GCG Disclosure Index) evaluates the effectiveness of GCG based on the principles of GCG in the company's annual report.

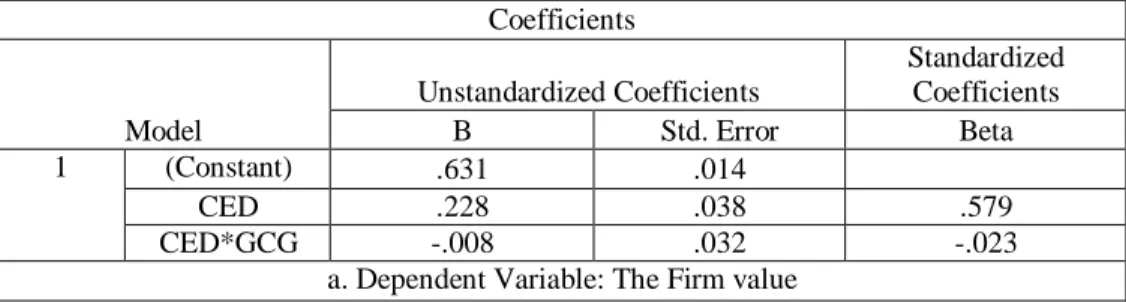

Each disclosure item in the 16 GCG GCG categories reflected GCG principles that companies should follow to enable better management and subsequently strengthen the relationship between CED and company value. The development of the second hypothesis is based on the findings of Nahda and Harjit (2011) that the moderating effect of GCG can strengthen the relationship between CSR and firm value. Therefore, the second hypothesis is rejected; the interaction variable CED*GCG cannot strengthen the relationship between CED and firm value.

The application of Accounting Standards Guidelines 1 is evidence of the company's efforts to conduct business activities based on established regulations to maintain public legitimacy. Although still voluntary, the company continues to disclose carbon emissions to gain public legitimacy. The board of directors, as the highest element of management in the company, has a large voice in decision-making in the company.

The functioning of the supervisory board has no significant influence on the added value of the company.

Conclusion, Implication, and Limitations 1 Conclusion

The additional members of the independent board of commissioners of the company are only a formality; meanwhile, in this case, the shareholders, who are the majority owners of the company, are involved in making decisions made by the management, which causes a conflict of interest between the shareholders and management. On the other hand, the GCG cannot strengthen the relationship between SED's influence on firm value because the interaction of the SED and GCG has a negative effect on the firm value. This study has a limitation of the value of the coefficient of determination that the ability of the CED and GCG to influence the fixed value is at 31.7%.

A further limitation is that the measurement of the CED on the carbon emissions disclosure checklist, based on the research of Choi et al. 2013) and the GCG on the Corporate Governance Disclosure Index are subject to the authors' interpretation after reading of the companies' annual reports and sustainability reports. The remaining 68.3% of the coefficient of determination, influenced by variables not included in this study, is also worth further investigation. CC1 – Assessment/description of the risks (regulatory, physical or general) related to climate change and the actions taken or to be taken to manage the risks.

RC3 – Emission reductions and associated costs or savings achieved to date as a result of the reduction plan. ACC1 – Indication of which board committee (or other executive body) has overall responsibility for actions related to climate change ACC2 – Description of the mechanism by which the board (or other executive body) reviews the company's progress on climate change. 2 Declaration of guarantee for the protection of the shareholders' right to treat all shareholders equally.

1 Names of board members 2 Status of each member (independent commissioner or not. independent commissioner). 6 Self-evaluation mechanism and performance criteria for each member of the Board of Commissioners 7 Number of meetings held. Board of Directors 1 Names of members of the Board of Directors with their positions and functions.

11 Training program to improve the directors' competences Audit committee 1 Name and title of members of the audit committee. 2 Short curriculum vitae for each member of the audit committee 3 Description of the audit's tasks and responsibilities. 4 Description of internal control's tasks and responsibilities 5 Description of internal control activities during the year 6 Explanation of the company's internal control and audit Risk management 1 An explanation of the risks the company faces.

Important cases facing the company, board members and members. 4 Ownership share of board members and directors and their family members in companies and other companies.