Socially friendly business strategy and

social sustainability performance: roles of spiritual capital and social management process

Bambang Tjahjadi, Noorlailie Soewarno, Tsanya El Karima and Annisa Ayu Putri Sutarsa

Abstract

Purpose–This study aims to determine whether socially friendly business strategy impacts social sustainability performance and, if so, whether social management process and spiritual capital act as mediators and moderators of the relationship.

Design/methodology/approach–This study uses a comprehensive research framework consisting of the mediation and moderation relationship among four constructs, namely, socially friendly business strategy, social management process, spiritual capital and social sustainability performance. A total of 433 owners/managers of micro, small and medium-sized firms (MSMEs) in the Indonesian province of East Java took part in this study, and the data were gathered using a survey method. The resource-based view, stakeholder theory and partial least squares structural equation modelling are all used in this study to evaluate and explain the hypotheses.

Findings– The results show that both socially friendly business strategy and social management process positively affect social sustainability performance. Further analysis reveals that spiritual capital moderates the effect of socially friendly business strategy on social sustainability performance. Second, social management process mediates the influence of socially friendly business strategy on social sustainability performance in part.

Research limitations/implications–The current study has limitations. First, it restricts the scope of its sample to MSMEs in Indonesia’s East Java Province. As a result, it also restricts its generalizability, and care must be used if the findings are applied to other types of organizations and geographic areas.

Second, some survey participants needed help to complete the online questionnaire. As a result, collecting the data were less successful than anticipated. This study has significant implications for the development of the stakeholder theory, particularly in elucidating the mechanisms by which socially responsible corporate strategies, social management practices and performance in terms of social sustainability are affected.

Practical implications–The findings provide a comprehensive guidance for owners/managers in reorienting their business strategy, managing the social management process and building their spiritual capital to achieve social sustainability performance. It provides materials for researchers and students who are interested in studying the subject matter.

Social implications–MSMEs have a significant role in society. The welfare of society will therefore increase if social sustainability performance is successful. The overall model of social sustainability performance improvements and its antecedents are presented in this study.

Originality/value–To the best of the authors’ knowledge, this study is among the first attempts to explore the general model of improving social sustainability performance using four constructs that are rarely used in previous studies. It also uses a new data set and research setting in Indonesia as one of the emerging countries.

Keywords Stakeholder theory, Spiritual capital, Multi-stakeholder partnership,

Social management process, Social sustainability performance, Socially friendly business strategy Paper typeResearch paper

Bambang Tjahjadi, Noorlailie Soewarno, Tsanya El Karima and Annisa Ayu Putri Sutarsa are all based at the Department of Accounting, Fakultas Ekonomi dan Bisnis, Universitas Airlangga, Surabaya, Indonesia.

Received 18 November 2022 Revised 9 March 2023 8 July 2023

29 August 2023

Accepted 6 September 2023 The authors would like to thank Ministry of Education, Culture, Research and Technology Republic of Indonesia for funding this research.

1. Introduction

The socially based enterprise model and its ecosystem have experienced a remarkable global expansion in recent decades. Social sustainability performance reflects how companies translate social goals into business strategy using strategies that focus on social issues (Alsayeghet al., 2020). In this case, a socially friendly business strategy refers to a business strategy that explicitly focuses on social goals rather than merely maximizing economic profits (Spiethet al., 2019). Socially friendly business strategy is an initiative to combine the responsibilities of commercial business with a social mission to achieve excellent performance and significantly contribute to addressing society’s primary social issues. Social sustainability performance refers to a social capital concept that focuses on addressing various sustainability topics (Ali and Kaur, 2021). International discussions on issues tend to center on social problems. The International Organization of Standards 26000, which provides guidelines for how enterprises can conduct themselves properly, contains information on this. The Global Reporting Initiative (GRI) additionally uses a de facto standard to assess and document the social practices covered by corporate sustainability reports. Social sustainability performance is specially tracked through the expanded implementation of the UN Sustainable Development Goals. By fusing the functions of economic enterprise and social mission, many businesses have been devoting themselves to addressing social issues (Porter and Kramer, 2006, 2011; Mahfouzet al., 2018). Companies use business strategies to manage their operations by producing and capturing value (Martins et al., 2015; Mahfouz et al., 2018). In this setting, business strategies that were formerly solely concerned with commercial value have recently started to adopt business principles in a way that can assist organizations in collaborating their entrepreneurship at the community level to reduce social problems (Shin et al., 2016;

Laasch and Conaway, 2017). Therefore, management should work toward achieving social sustainability performance, which is influenced by various aspects that will be the main key of this research.

The idea that is most frequently employed to explain sustainability performance is stakeholder theory. Freeman (19c84) asserts that corporations focus on shareholder profitability and uphold positive relationships with other stakeholders while developing additional value. This study focuses on the interaction between a company’s internal and external stakeholders to analyze social sustainability performance. Companies have a more challenging time using their unique resources to pursue business goals responsibly. In accordance with resource-based perspective (Wernerfelt, 1984), company resources allow businesses to outperform their competitors by using long-term competitive advantages.

Therefore, using the resource-based view (RBV) and stakeholder theory, we study how a socially friendly business strategy might enhance social sustainability performance (Freeman, 1984;Barney, 1991). It is founded on the idea that every business has various stakeholders, each with its resources, talents and routines. Corporate resources centered on building strong stakeholder relationships can significantly influence social sustainability performance.

There needs to be more research on the impact of socially friendly business strategy on social sustainability performance. The results of many constructs with more general definitions, such as business strategy, corporate social responsibility (CSR) and sustainability performance, have been used by certain scholars. However, the findings still need to be revised. In line with several scholars, CSR and business strategy are related (Longoni and Cagliano, 2015;Linet al., 2020;Yuanet al., 2020). This is thought to be the case because the business strategy is chosen to have an impact on how the management of the company behaves when making decisions regarding the company’s operations (Mileset al., 1978;Yuanet al., 2020), including choices regarding the future form of CSR.

Pursuant to certain academic, the performance of sustainability is not affected by corporate strategy (Chen and Jermias, 2014;Hahnet al., 2019;Yuet al., 2020).

Because of this knowledge gap, we were prompted to perform the current study with a more focused design and thorough approach. There are two fundamental causes for the gap in earlier research. First of all, a more specific definition of sustainability performance is required. As a result, this study makes use of social sustainability performance. Second, rather than directly affecting sustainability performance, previous research should have focused more on how corporate strategy indirectly affects it. We propose the social management process as a mediating variable and spiritual capital as a moderating variable to provide a more comprehensive understanding of achieving social sustainability performance. The new study will increase our understanding of how literature demonstrates societal sustainability, primarily focusing on socially friendly business strategy, social management procedures and spiritual capital as factors influencing social sustainability performance.

Companies need to develop spiritual capital as a driving force to tackle sustainability issues in addition to socially friendly business strategy (Zohar and Marshall, 2004;Astrachanet al., 2020;Thomas, 2021). Intangible assets used to explain more practical aspects of business activity based on standards of ethics and corporate responsibility are referred to as spiritual capital. Social capital can be created and strengthened by spiritual capital, particularly when it comes to fostering normative conduct that fosters collaborative networks for long- term economic sustainability.Jauhari and Sanjeev (2010)and Saxena et al.(2021) have confirmed in the context of business continuity, spiritual capital and social management processes can help to foster the positive relationships required to expand the business scale. Unfortunately, because the idea of spiritual capital and the social management process is rarely articulated, there is little study on the connection between socially friendly business strategy and social sustainability performance. Further research is vitally required, as spiritual capital and social management practices are crucial in answering corporate performance-related social challenges. The phrase “social management process” refers to the business’s strategic initiatives to implement the management process to achieve the three sustainability pillars, particularly on the social front. Additionally, businesses with substantial social capital and social management practices demonstrate a solid commitment to being socially responsible and positively impacting both sustainable development and community welfare (Saxenaet al., 2021).

The Coordinating Ministry for Economic Affairs of the Republic of Indonesia (2021) states that there are 64.2 million micro, small and medium-sized firms (MSMEs) in Indonesia, which account for 61.07% of the nation’s gross domestic products (GDP), or $8,573.89tn. It is understandable why manufacturing MSMEs have proliferated in the East Java Province.

As specified by the Central Bureau of Statistics for East Java Province, 2021, MSMEs account for 57.81% of the gross domestic products (GDP) of East Java. However, MSMEs have, sadly, had a detrimental influence on neighborhood social life despite being excellent at growing the economy. Few MSMEs prioritize sustainability, particularly social sustainability. As per previous study conducted by Kromjong et al. (2016), just 10% of MSMEs are represented in the global reporting initiative (GRI) Sustainability disclosure database. MSME owners encounter several difficulties in a cutthroat business environment.

One is the demand for more resources for long-term business continuity planning, which often causes long-term investments in social sustainability to be postponed or abandoned (Tevapitak and Helmsing, 2019). Social sustainability can create a sustainable competitive advantage, something which MSME owners need to understand (Lee and Raschke, 2020).

MSME owners say, however, that their small enterprises have little to no social influence (Williamsonet al., 2006;Tevapitak and Helmsing, 2019). As a result, MSME owners wish to refrain from making a personal commitment to enhance their social performance jointly. For instance, 70% of the 12,000 MSMEs engaged in manufacturing in East Java have dumped production waste into rivers (Wijayanto, 2018). This action undoubtedly resulted in severe river pollution, a detrimental effect on public health and other societal issues.

The current study contains the following primary conclusions after applying partial least squares structural equation modelling (PLS-SEM) to test the hypothesis and a comprehensive research framework (a combination of a mediating and moderating framework):

䊏 Spiritual capital moderates the effect of socially friendly business strategy on social sustainability performance.

䊏 Social management process mediates the influence of socially friendly business strategy on social sustainability performance in part.

The current investigation makes both theoretical and practical advancements; it advances the conceptual understanding of socially friendly business strategy, social management practices and spiritual capital to socially sustainable performance, adding to the existing body of literature. Second, it demonstrates the critical function of spiritual capital as a moderator and the social management process as a mediator. By presenting actual data on the research setting of MSMEs in an emerging market, it supports RBV and stakeholder theory. The results suggest that stakeholder theory and RBV can be used by academics, professionals and others to understand the relationships between the constructs under investigation. The empirical evidence in this study can be used by businesses to establish socially sustainable performance mechanisms favorably correlated with socially friendly business strategy, social management procedures and spiritual capital. To achieve socially sustainable performance, managers and owners must first recognize the importance of correctly managing socially responsible company strategy, social management practices and spiritual capital. Second, owners and managers must know the significance of social management practices and spiritual capital. This study’s findings support the recommendation that managers and owners use the social management process as a tactical means of achieving sustainability. Additionally, having sufficient spiritual capital can help managers invest in and participate in social sustainability activities, thereby enhancing business performance.

This study’s remaining sections are organized as follows. Section 2 discusses the literature review and hypothesis. Section 3 explains the methodology. Section 4 discusses the results and discussion, and Section 5 discusses the conclusions, contributions and suggestions for future research.

2. Literature review and hypothesis development

Stakeholder theory (Freeman, 1984) explains the importance company’s stakeholders. The theory states that a company must act in accordance with the expectations of its stakeholders (Barako and Brown, 2008; Sonpar, 2011). Companies that can meet the expectations of their stakeholders will create greater value over time (Pinelli and Maiolini, 2016). Stakeholder theory is the most relevant theoretical framework in CSR research (Fassin et al., 2017;Richter and Dow, 2017;Vashchenko, 2017;Javedet al., 2020). The involvement of stakeholders will affect the company’s sustainability performance by identifying the potential of business processes and management (Ashrafiet al., 2020). Lack of awareness to understand the interdependence with stakeholders makes companies face problems in resolving the conflicting views between them (Dutta and Ring, 2021).

Stakeholder theory is a useful tool for providing guidance on company operations.

Stakeholder theory establishes corporate responsibility to all stakeholders. Thus, social sustainability performance has become a strategic tool to improve company performance because it is considered a form of corporate responsibility toward stakeholders. RBV argues that internal resources owned by companies are the source of a competitive advantage. RBV also explains social sustainability performance issues as research conducted by Hart (1995) assessed that dynamic resources or capabilities used by company to be able to assess firm performance that focus on social issues can help

company create an advantage in sustainable competition between companies. A company needs to build unique intangible resources to increase company performance (Kamasak, 2017). Intangible assets, including spiritual capital are the most strategic assets in formulating and executing inimitable strategies that cannot be duplicated by their competitors (Zohar and Marshall, 2004).

Stakeholder theory and RBV underscore the importance of properly managing the wishes of stakeholders as valuable resources, which, in turn, provides strategic advantages in business competition (Sodhi, 2015;Lee and Raschke, 2020). Both theories state that all stakeholders, such as suppliers, employees, customers and society, must be managed in a balanced way by using each stakeholder’s routines, resources and abilities to achieve better performance (Gualandris et al., 2015). In this study, we use two main company resources, namely, internal stakeholders and external stakeholders. The involvement of internal stakeholders can be used effectively for companies to gain a competitive advantage (Bayraktar et al., 2017). The involvement of internal stakeholders, such as employees, plays a role in optimally implementing business strategies. External stakeholder collaboration can also be a key resource that creates a competitive advantage (Wanget al., 2016). The involvement of internal stakeholders, such as suppliers, plays a role in improving products or services for companies (Wanget al., 2016). This means the responsibility for maintaining stakeholders in the MSME management process, which causes complex social problems, will impact the company’s strategic advantages and disadvantages. Therefore, these two theories are used to show the phenomenon of social sustainability performance in MSMEs.

2.1 Socially friendly business strategy and social sustainability performance

When social issues amongst stakeholders are considered, the RBV offers a distinctive paradigm for describing how internal resources produce good change (Lozano, 2015).

Stakeholder theory argues that a company’s activities must be in line with stakeholders’

interests. A company will fail without having a strategy that accommodates stakeholders’

interest in its business activities (Dutta and Ring, 2021). Nowadays, consumers are increasingly demanding companies to offer products or services with both functional benefits and social contributions (Vila and Bharadwaj, 2017). As a result, including social considerations in the business plan will help it remain sustainable in the long run. Studies by previous researchers (Longoni and Cagliano, 2015; Lin et al., 2020; Yuan et al., 2020) support the positive effect of business strategy–social sustainability performance, mainly CSR.Linet al. (2020)demonstrated the positive relationship between business strategy and CSR using data from 3,000 American companies between 1996 and 2016. This is consistent with a study byLongoni and Cagliano (2015)conducted in Europe and America which showed the positive impact of operations strategy on social and environmental sustainability objectives. A study byYuanet al.(2020)conducted in the USA between 2004 and 2012 showed company strategy’s positive impact on CSR performance. In summary, the research above has proven that business strategy plays a role in improving a company’s sustainability performance. Based on the previous discussion, we propose the following:

H1. Socially friendly business strategy is positively associated with social sustainability performance.

2.2 Socially friendly business strategy and social management process

Stakeholder and RBV theory provide a strong theoretical foundation for understanding long- term value creation through social sustainability. The integration of value-creating strategies is a collaborative effort that benefits key business processes and their stakeholders (Freeman, 2010; Freudenreich et al., 2020). Currently, social-based business strategies

attract many external parties. However, a socially friendly business strategy is considered successful only if it can sustainably satisfy stakeholders by solving long-term social problems (Mahfouz et al., 2018). In addition, increasing competition at the corporate management process level, both from customer demand and pressure from stakeholder groups, encourages companies to increase sustainability in their business operations (Dubeyet al., 2017;Zhanget al., 2018). Most attention to the sustainability of the company’s management process is focused on economic and environmental aspects, while social aspects always receive very little attention (Rodriguez et al., 2016; Mani et al., 2018).

Socially friendly business strategy is well received, especially as the Indonesian nation adheres to a “gotong royong” system. Gotong royong (in Bahasa) is an awareness to help each other by lifting the burden together so that problems can be resolved quickly (Kurniawati and Mawardi, 2021). Even though the effectiveness of social-based management processes also plays an essential role in the successful execution of the company’s business strategy, unfortunately, empirical studies investigating the effect of socially friendly business strategy on social management process are rarely conducted. A study byNg and Al-Shaghroud (2018)on MSMEs in Northern England proved the positive influence of strategy on social process. In summary, the research above has proven that business strategy plays a role in improving a social process. Based on the previous discussion, we propose the following:

H2. Social friendly business strategy is positively associated with social management process.

2.3 Social management process and social sustainability performance

In line with the RBV, the capabilities possessed by firms can ultimately trigger long-term competitive advantages (Barney, 1991). Therefore, sustainability initiatives using internal company resources focusing on social issues have a significant market opportunity (Connellyet al., 2011a,2011b). In line with the stakeholder theory, businesses do not just serve their interests; they also benefit other stakeholders. As per previous studies conducted by Castka and Corbett (2016) andGiannakis and Papadopoulos (2016), the sustainability of social-based process management refers to how businesses address aspects of product and process management that will have an impact on the safety, health and welfare of all stakeholders in the company’s business operations. The social management approach is one of the most crucial methods for raising business performance. The company’s strategy attempts to achieve the three sustainability pillars, namely, environmental, economic and social issues, referred to as the social management process (Carter and Rogers, 2008;Awan, 2019). The implementation and evaluation of social concerns in the business’ social management process must involve stakeholders if social sustainability is to be achieved (Awan, 2019). Sadly, empirical research on how social management practices affect social sustainability is rarely done. In a previous study,Awan (2019) demonstrated the positive impact of social supply chain practices on social sustainability performance using a sample of 272 manufacturing enterprises in Finland. In summary, the practice of social management process has been considered as one of the most important ways to improve firm performance. Based on the previous discussion, we propose the following:

H3. Social management process is positively associated with social sustainability performance.

2.4 Mediating role of social management process on socially friendly business strategy

–social sustainability performance relationship

Stakeholder management from an RBV and stakeholder theory perspective is crucial, as it can provide businesses with a competitive edge. Based on previous studies from

Herremans et al. (2016) and Ashrafi et al. (2020), these theories serve as the foundation for creating and developing management and operational plans for businesses that serve the interests of important stakeholders. Socially friendly business strategy is now a crucial component of daily living. Businesses that include social issues in their business strategy can build trust with all stakeholders, motivating businesses to perform better in corporate social sustainability. The success of a business is significantly impacted by business strategies that include supplier resources as one of the company’s stakeholders, which could reduce the chance of losing the company’s positive reputation (Sodhi, 2015). Social sustainability initiatives among stakeholders undoubtedly make the social management process more responsive, giving strategic business power. Previous research has demonstrated the impact of business strategy on social processes, the influence of business strategy on supply chain practices and the impact of business strategy on sustainability performance (Longoni and Cagliano, 2015; Linet al., 2020; Yuan et al., 2020). The current study thus contends that the social management process mediates between social sustainability performance and socially friendly business strategy. Based on the previous discussion, we propose the following:

H4. Social management process mediates the effect of socially friendly business strategy on social sustainability performance.

2.5 Moderating role of spiritual capital on socially friendly business strategy

–social sustainability performance relationship

In line with RBV and stakeholder theory, intangible resources become the main factor in building competitive advantage and achieving superior company performance with the increasingly dynamic knowledge-driven economy. Spiritual capital is the accumulated and enduring set of beliefs, knowledge, values and dispositions that drive organizational behavior (Noghiu, 2020). Spiritual capital is one of the intangible resources that must become the foundation of companies’ values and activities.

Spiritual capital provides an identity, value system and moral vision to the company’s business operations (Stokeset al., 2016).Zohar and Marshall (2004)has confirmed that companies that have high spiritual capital tend to have a long-term vision and higher social sensitivity or concern than other companies. In integrating a business strategy driven by social aspects, spiritual capital, such as insight and wisdom, helps the owner/

manager adopt a mindset/innovation that is open to new knowledge that can benefit the company. Additionally, spiritual capital also serves as a moral prerequisite and a basis for social order necessary for a sustainable business. In addition, companies that integrate spiritual capital in their business strategies also encourage these companies to share values with the community, which can improve their sustainability performance. Unfortunately, empirical studies that examine the influence of spiritual capital on social sustainability performance are still rarely conducted. Thus, the better the interaction between socially friendly business strategy and spiritual capital, the stronger the effect of socially friendly business strategy on social sustainability performance. Based on the previous discussion, we propose the following:

H5. Spiritual capital moderates the effect of socially friendly business strategy on social sustainability performance.

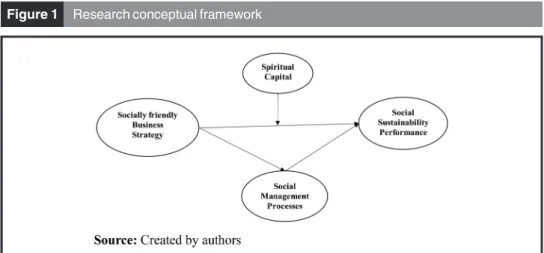

Figure 1depicts the conceptual framework of this study. It shows the associations among constructs, namely, socially friendly business strategy as the independent variable, social management process as the mediating variable, spiritual capital as the moderating variable and social sustainability performance as the dependent variable.

3. Methodology

3.1 Sample and data collection

The study’s respondents are owners/managers of MSMEs under the Department of Cooperatives’ supervision and MSMEs from the province of East Java. The deliberate sampling method and the following requirements were used to determine the number of study samples: complete names and addresses; a unique email address; and contacts from WhatsApp. Based on these criteria, 1,658 manufacturing MSMEs were found to be eligible. All 1,658 respondents received the questionnaire due to the low response rate.

Surveys conducted offline and online were used to collect primary data. A pilot test was conducted before respondents were handed the questionnaires. The findings of the pilot test, which involved 35 MSMEs in Surabaya, demonstrated the validity and reliability of the survey items. Each questionnaire was accompanied by a cover letter describing the goals and objectives of the study and guaranteeing the confidentiality of respondents’responses.

As many as 409 questionnaires were gathered during the three-month data collection period from March to June 2022, 400 of which were completed and ready for processing.

Therefore, 24% of the populace responded to the survey. The PLS-SEM technique was used to analyze the data because it can:

䊏 measure latent variables with multiple indicators accurately;

䊏 test complex study models without taking into account data distribution assumptions;

and

䊏 use a relatively small sample size (Hairet al., 2017,2021).

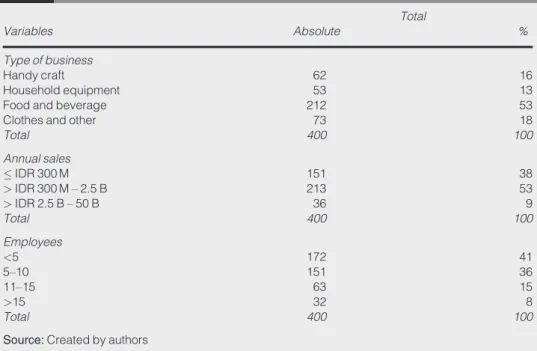

3.2 Respondents’ characteristics

Table 1 lists the traits of the 400 respondents, who are owners or managers of MSMEs engaged in manufacturing. MSMEs with a sales value of IDR 300m to IDR 2.5bn (53%), MSMEs in the food and beverage industry (53%) and MSMEs with five employees (41%).

3.3 Measurements

3.3.1 Socially friendly business strategy.The following statements fromBentleyet al.(2013) were used to gauge socially friendly business strategy: prioritizing social sustainability ideals; integrating social issues into corporate strategy; giving them the top priority when attaining firm objectives; allocating resources with a social sustainability focus; and

Figure 1 Research conceptual framework

(SFBS1), (SFBS2), (SFBS3), (SFBS4), (SFBS5) Consideration of social issues in the creation of new products; (SFBS 6) creation of novel new products that can lessen adverse social effects; (SFBS 7) social issues have an impact on product sales and advertising; and (SFBS 8) social protection as the cornerstone of strategic decision-making.

3.3.2 Spiritual capital.A total of 12 statements fromZohar and Marshall (2004)were used to calculate spiritual capital, including:

1. (SC1) putting the company’s goals and strategies in the context of deeper meanings and values;

2. (SC2) having “self-awareness” about our beliefs, the people we influence and the things we want to accomplish;

3. (SC3) being guided by the vision and values; and 4. (SC4) having a solid sense of holism or connectivity;

5. (SC 5): feeling affectionate toward the companies;

6. (SC 6): respecting diversity;

7. (SC 7): being highly independent;

8. (SC 8): the company’s goals are meaningful;

9. (SC 9): able to act at any time; not constrained by other paradigms, assumptions or interests;

10. (SC 10): seeing the bright side when facing challenges;

11. (SC 11) deep humility, not expecting praise or gifts in return; and 12. (SC 12) volunteer work.

3.3.3 Social management process.The following claims were taken directly fromChenet al.

(2012) and Hoejmose et al. (2013): selection of socially responsible suppliers; socially responsible production; selection of socially responsible products; socially responsible

Table 1 Characteristics of respondents Variables

Total

Absolute %

Type of business

Handy craft 62 16

Household equipment 53 13

Food and beverage 212 53

Clothes and other 73 18

Total 400 100

Annual sales

IDR 300 M 151 38

>IDR 300 M–2.5 B 213 53

>IDR 2.5 B–50 B 36 9

Total 400 100

Employees

<5 172 41

5–10 151 36

11–15 63 15

>15 32 8

Total 400 100

Source:Created by authors

process innovation; socially responsible marketing; socially responsible competitor identification; socially responsible consumer needs identification; and socially responsible regulatory compliance.

3.3.4 Social sustainability performance.Harrington (2016)posits a total of ten requirements, including:

1. recognized as being socially responsible;

2. actively involved in finding answers to social problems;

3. aware of social issues;

4. creator and implementer of social initiatives;

5. (SSP 5) Set aside money to deal with social issues;

6. (SSP 6) Possessing a favorable public image;

7. (SSP 7) winning a prize for social sustainability;

8. (SSP 8) having a socially responsible workforce;

9. (SSP 9) fostering a culture of social preservation; and

10. (SSP 10) demonstrating initiative and leadership in the field of social preservation.

A five-point Likert scale ranging from 1 (strongly disagree) to 5 (strongly agree) was used to measure each variable.

3.4 Data analysis

This study tests the idea using PLS-SEM. It is used for the following purposes: in agreement with Hair et al. (2017), it has been demonstrated to be the most effective method for assessing secondary data from a measurement theory standpoint. Additionally, it can generate correct results with relatively little data (Sholihin and Ratmono, 2013). There are two steps in the PLS-SEM:

1. analysis of the measurement model; and 2. analysis of the structural model.

4. Results

4.1 Descriptive statistics

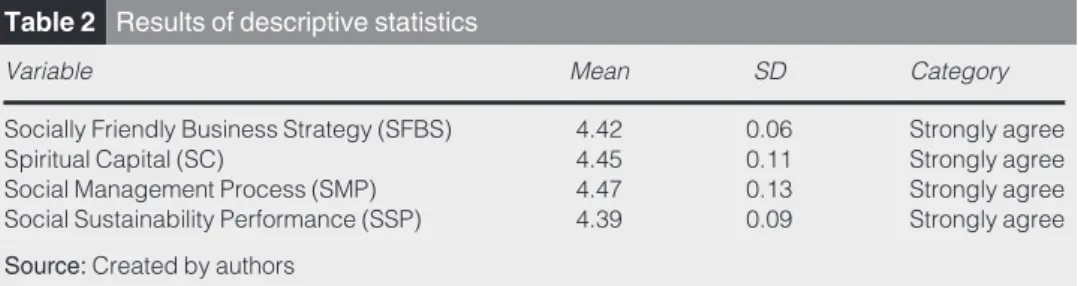

Table 2 displays the outcomes of the descriptive statistics. The results show that the respondents overwhelmingly concur with the questionnaire’s statements about socially responsible business strategy, spiritual capital, social management techniques and social sustainability performance. It shows that the owners and managers of MSMEs have a thorough understanding of social performance and its causes.

Table 2 Results of descriptive statistics

Variable Mean SD Category

Socially Friendly Business Strategy (SFBS) 4.42 0.06 Strongly agree

Spiritual Capital (SC) 4.45 0.11 Strongly agree

Social Management Process (SMP) 4.47 0.13 Strongly agree

Social Sustainability Performance (SSP) 4.39 0.09 Strongly agree Source:Created by authors

4.2 Common method bias

This study simultaneously collected data on internal and exterior components using self- report questionnaires. As a result, common method bias may become a problem, and common method bias errors may change the outcomes (Podsakoff et al., 2003). Ex-ante and ex-post control techniques were used to address this problem. Ex-ante byPodsakoff et al.(2003)uses several test procedures, including:

䊏 administering a pilot test of the questionnaire to make sure that the statement items are understood; and

䊏 outlining anonymity, honest answer requests and the fact that there are no right or wrong answers in the questionnaire cover letter.

In accordance withKock (2015), the value of variance inflation factor (VIF) full collinearity can be used to do the ex-post process, and if the result is less than or equal to 3.3, it is deemed bias-free. Using the WarpPLS 7.0 program, the VIF value for each latent variable is less than 3.3 (Socially Sustainable Performance¼ 2.221; Spiritual Capital¼3.278; Social Management Process¼ 3.257); and Socially Friendly Business Strategy¼1.912. Finally, the common method bias problem is not a concern in our analysis.

4.3 Measurement model analysis

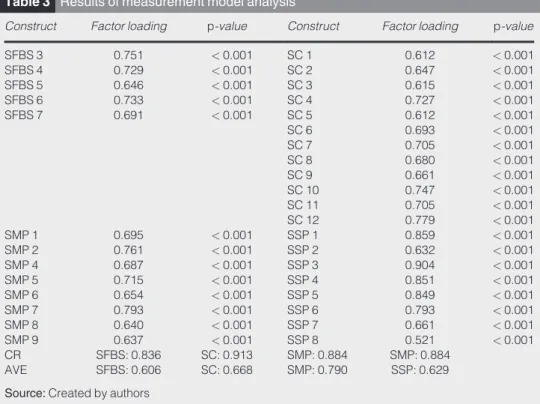

The validity and reliability of the link between the measurement indicators and the constructs were examined in this study using measurement model analysis. According toChin (2010), each factor loading needs to be greater than 0.6. Not all factor loadings met the 0.6 thresholds in the initial iteration. Factor loadings for SFBS 1, SFBS 2, SFBS 8, SMP 9, SSP 9 and SSP 10 were all less than 0.6. Therefore, the invalid factor loadings were not included in the subsequent step.Table 3 displays the outcomes of the second cycle. It shows that all factor loadings for each construct exceeded the threshold of 0.6.

Table 3 Results of measurement model analysis

Construct Factor loading p-value Construct Factor loading p-value

SFBS 3 0.751 <0.001 SC 1 0.612 <0.001

SFBS 4 0.729 <0.001 SC 2 0.647 <0.001

SFBS 5 0.646 <0.001 SC 3 0.615 <0.001

SFBS 6 0.733 <0.001 SC 4 0.727 <0.001

SFBS 7 0.691 <0.001 SC 5 0.612 <0.001

SC 6 0.693 <0.001

SC 7 0.705 <0.001

SC 8 0.680 <0.001

SC 9 0.661 <0.001

SC 10 0.747 <0.001

SC 11 0.705 <0.001

SC 12 0.779 <0.001

SMP 1 0.695 <0.001 SSP 1 0.859 <0.001

SMP 2 0.761 <0.001 SSP 2 0.632 <0.001

SMP 4 0.687 <0.001 SSP 3 0.904 <0.001

SMP 5 0.715 <0.001 SSP 4 0.851 <0.001

SMP 6 0.654 <0.001 SSP 5 0.849 <0.001

SMP 7 0.793 <0.001 SSP 6 0.793 <0.001

SMP 8 0.640 <0.001 SSP 7 0.661 <0.001

SMP 9 0.637 <0.001 SSP 8 0.521 <0.001

CR SFBS: 0.836 SC: 0.913 SMP: 0.884 SMP: 0.884

AVE SFBS: 0.606 SC: 0.668 SMP: 0.790 SSP: 0.629

Source:Created by authors

To measure dependability, the composite reliability value must be more than 0.7 (Hairet al., 2013). As demonstrated in Table 3, all constructions had composite reliability values of more than 0.7. The numbers met the requirements, and the measurements were accurate.

The average variance extracted (AVE) was used to evaluate convergent validity. When the AVE value is more than 0.5, the variation derived from the construct surpasses the measurement error (Vandenbosch, 1996). The AVE values of the constructs were more significant than 0.5, which is the minimum value necessary for convergent validity, as shown inTable 3.

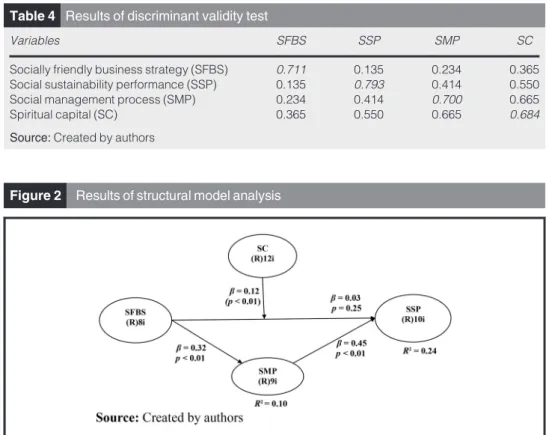

Table 4contains the results of the discriminant validity test. The correlations between the latent variables were compared using the square root of AVE. According to Fornell and Larcker (1981), it is acceptable if the AVE square root is greater than the correlation between the constructs.Table 4shows that the socially friendly business strategy, social sustainability performance, social management process and spiritual capital had the highest values when the values of the various factors were horizontally compared. In summary, the measuring model used in this work is trustworthy and valid.

4.4 Structural model analysis

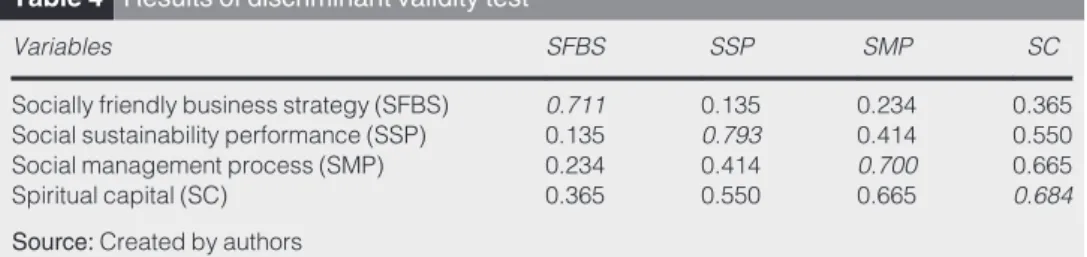

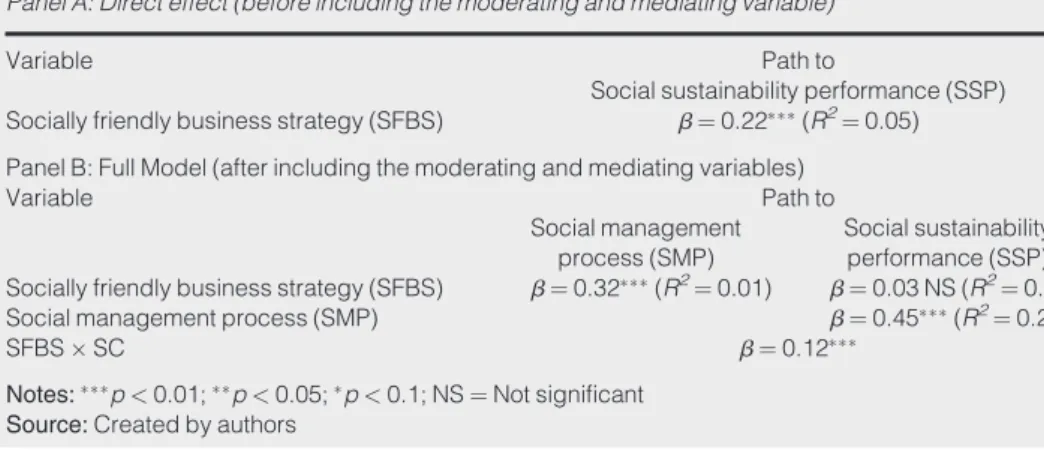

Figure 2presents the result of structural model analysis. With a correlation of 0.22 and a p-value of 0.05,Table 5(Panel A) demonstrates the positive relationship between socially friendly business strategy and social sustainability performance. As a result,H1 –that a socially responsible company strategy is positively correlated with social sustainability performance–is confirmed. The social management process was added as a mediating variable (Panel B) to analyze the data further. The results show that social sustainability performance impacts the social management process (coefficient: 0.32;p-value 0.01). This supportsH2that a socially friendly business strategy favorably correlates with the social management process.

Table 4 Results of discriminant validity test

Variables SFBS SSP SMP SC

Socially friendly business strategy (SFBS) 0.711 0.135 0.234 0.365

Social sustainability performance (SSP) 0.135 0.793 0.414 0.550

Social management process (SMP) 0.234 0.414 0.700 0.665

Spiritual capital (SC) 0.365 0.550 0.665 0.684

Source:Created by authors

Figure 2 Results of structural model analysis

H3that the social management process is positively correlated with social sustainability performance is supported by the observation that the social management process impacts social sustainability performance (coefficient: 0.45;p-value 0.01). The direct impact of a socially friendly business strategy on social sustainability performance diminished after being mediated through the social management process (coefficient: 003;p-value¼0.25).

The negligible impact demonstrated a complete mediation. The fourth premise contends that the social management process mediates the impact of a socially friendly business strategy on the performance of social sustainability. Finally, the results showed that spiritual capital (coefficient: 0.12; p-value 0.01) moderates the association between socially responsible company strategy and social sustainability performance. Thus, H5 – that spiritual capital modifies the impact of socially friendly business strategy on performance in social sustainability–is confirmed.

4.5 Discussions of the results

4.5.1 Socially friendly business strategy and social sustainability performance. As predicted by stakeholder theory, the empirical findings corroborateH1and the favorable impact of socially responsible company strategy on social sustainability performance. The results also corroborate the claims and investigations made by earlier researchers (Longoni and Cagliano, 2015;Spiethet al., 2019;Linet al., 2020;Yuan et al., 2020;Ali and Kaur, 2021;Dutta and Ring, 2021). Companies must consider the interests of their stakeholders in the business strategy and operations to succeed, and actual data prove this claim. Owners and managers of MSMEs in Indonesia firmly concur that they must develop and implement business plans prioritizing achieving social objectives over maximizing financial gains. CSR initiatives frequently reflect a company’s social actions. The Indonesian Government has also implemented rules and regulations regarding CSR initiatives, such as RI Law No. 40 of 2007 concerning Limited Liability Companies and Government Regulation No. 47 of 2012 concerning Social and Environmental Responsibility of Limited Liability Companies.

Therefore, it is scientifically proven that businesses with more robust socially friendly business strategy also perform better regarding social sustainability.

4.5.2 Socially friendly business strategy and social management process.The empirical findings further support the claim that stakeholder theory provides a solid theoretical framework for businesses to build value through their operations. The data are consistent with H2, which states that socially friendly business strategy practices improve social sustainability performance. The findings are consistent with those of earlier researchers (Freeman, 2010; Ng and Al-Shaghroud, 2018;Mahfouz et al., 2019;Freudenreich et al., 2020). Companies and their stakeholders will benefit from incorporating value-creating

Table 5 Results of structural model analysis

Panel A: Direct effect (before including the moderating and mediating variable)

Variable Path to

Social sustainability performance (SSP) Socially friendly business strategy (SFBS) b¼0.22(R2¼0.05) Panel B: Full Model (after including the moderating and mediating variables)

Variable Path to

Social management process (SMP)

Social sustainability performance (SSP) Socially friendly business strategy (SFBS) b¼0.32(R2¼0.01) b¼0.03 NS (R2¼0.24)

Social management process (SMP) b¼0.45(R2¼0.24)

SFBSSC b¼0.12

Notes:p<0.01;p<0.05;p<0.1; NS¼Not significant Source:Created by authors

strategies into essential business processes, particularly social management procedures. A socially responsible business plan can only be effective if it produces social sustainability results that can satisfy stakeholders over the long term. The research findings in the context of MSMEs in Indonesia demonstrate that owners/managers are aware of integrating strategy and its implementation process to address social issues their stakeholder’s encounter. In particular, because they adhere to the ideology of togetherness (gotong royong in Bahasa Indonesia), Indonesian society finds implementing the socially responsible company strategy in the form of CSR initiatives simpler. In line with empirical research, the stronger the socially friendly business strategy, the better the performance in terms of social sustainability.

4.5.3 Social management process and social sustainability performance. Stakeholder theory stated that businesses do not just work to serve their interests; they also benefit other stakeholders. As a result, the most crucial method for raising a company’s social performance is through its social management process. H3 that social management processes have a beneficial impact on social sustainability performance is supported by empirical data. The empirical findings are consistent with recent academic research (Carter and Rogers, 2008; Awan, 2019). Only some empirical studies examine how social management practices affect social sustainability performance. As a result, this study offers more empirical data on the subject. The owners and managers of Indonesian MSMEs know the necessity to enhance the social management process to achieve social sustainability performance. Companies with the most significant social concerns typically receive the finest rewards in the society, which upholds the value of community (gotong royong). The results show empirically that social sustainability performance increases with a more robust socially friendly business strategy.

4.5.4 Mediating role of social management process on socially friendly business strate- gy–social sustainability performance relationship.Based on stakeholder theory, the current study contends that the social management process serves as a bridge between socially friendly business strategy and social sustainability performance. The results show that adopting a socially friendly business strategy lays the groundwork for superior management procedures that serve the interests of all stakeholders. The performance of social sustainability then improves with the quality of the social management process due to increased stakeholder confidence. As a result, the data validateH4, which is this study’s distinctive feature. Owners and managers of Indonesian MSMEs know the factors influencing social sustainability performance, including socially responsible company strategy and social management practices. As a result, the current study’s mediation research framework is supported by empirical evidence.

4.5.5 Moderating role of spiritual capital on socially friendly business strategy–social sus- tainability performance relationship. The current study, which adopts the RBV and stakeholder theory, claims that spiritual capital has become the cornerstone of businesses’

operations, as it gives such operations a distinct identity, value system and moral compass.

Companies with high spiritual capital tend to have a positive attitude toward long-term social sustainability performance. The findings show that the relationship between spiritual capital and a socially friendly business strategy improves social sustainability performance.

As a result,H5, which contributes to the present work’s originality, is confirmed. The results demonstrate that the owners and managers of Indonesian MSMEs are fully aware of the necessity of having a solid spiritual foundation built into their corporate strategy to improve their social performance. They must be more socially sensitive than those their rivals and possess a long-term perspective. Thus, it is demonstrated that spiritual capital enhances the bond socially.

5. Conclusions, contributions, limitations and future research

5.1 Conclusion

The current study aims to understand better the factors that influence social sustainability performance, precisely the socially responsible company strategy, spiritual capital and social management process. It suggests a study framework for mediation and moderation.

The current study demonstrates that socially responsible business strategy and social management process positively affect social sustainability performance using 400 Indonesian MSMEs from the East Java Province and PLS-SEM to test the hypothesis. This result is consistent with those ofLongoni and Cagliano (2015),Linet al.(2020)andYuan et al. (2020), which demonstrate the influence of business strategy on management behavior, particularly concerning CSR-related decisions. Further investigation demonstrates that spiritual capital moderates the association between socially friendly business strategy and social sustainability performance, whereas the social management process partially mediates the relationship. As specified by RBV, incorporating social responsibility initiatives into a corporate strategy can help boost a company’s competitiveness (Porter and Kramer, 2006). The current study provides more detailed information about improving social sustainability performance through a mediator of the social management process and a moderator of spiritual capital using more precise constructs. Knowledge of this mechanism is essential for advancing theory and practice.

5.2 Contributions and implications

5.2.1 Theoretical contributions.The current study advances the conceptual understanding of socially friendly business strategy, social management practices and spiritual capital concerning socially sustainable performance, adding to the existing body of literature. This study supports the notion that adopting a socially friendly business strategy can result in excellent performance and significantly contribute to resolving social issues. Second, it demonstrates the critical function of spiritual capital as a moderator and the social management process as a mediator. Less attention is paid to other variables, especially mediating or moderating variables such as social management procedures and spiritual capital, because literature has attempted to use concepts with more general meanings, such as business strategy, CSR and sustainability performance. By presenting actual data on the research setting of MSMEs in an emerging market, it supports RBV and stakeholder theory. The results suggest that stakeholder theory and RBV can be used by academics, professionals and others to understand the relationships between the constructs under investigation.

5.2.2 Practical contributions.In practical, this research has the following contributions. First, it can be used as teaching material for lecturers and students who are interested in studying topics related to socially friendly business strategy, spiritual capital, social management processes and social sustainability performance. Second, it can be used by the community to gain a deeper understanding and analyze the determinants of social sustainability performance to achieve better social welfare.

5.2.3 Managerial implications. Socially responsible performance must be presented strategically in MSME management because it can boost the business’s financial gains.

Companies can apply socially sustainable performance mechanisms that positively link to socially friendly corporate strategy, social management procedures and spiritual capital using the empirical evidence from this study. Therefore, MSMEs should strive to invest more in initiatives promoting socially sustainable performance. To achieve socially sustainable performance, managers and owners must first recognize the importance of correctly managing socially responsible company strategy, social management practices and spiritual capital. Investment decisions must consider socially responsible performance because it can considerably boost business performance.

5.3 Limitations and future research

The following factors constrain the current investigation. To begin with, it gathers primary data through a survey method. Despite being proven to be devoid of subjective bias through testing, the survey approach has been challenged for bias. Although the study’s relevance cannot be questioned, caution must be exercised when applying the findings to more general situations. As one of the objective steps to further validate study findings. To understand socially sustainable performance better, future studies can take a qualitative method. It serves adequately. Finally, this study only considers three factors for determining sustainable social performance. This study did not include or analyze additional pertinent variables such as green supply chains, green reputation or green innovation which may substantially impact socially sustainable performance. It is advised that future research explore these factors in their research model.

References

Ali, S.S. and Kaur, R. (2021), “Effectiveness of corporate social responsibility (CSR) in implementation of social sustainability in warehousing of developing countries: a hybrid approach”,Journal of Cleaner Production, Vol. 324, p. 129154.

Alsayegh, M.F., Abdul Rahman, R. and Homayoun, S. (2020), “Corporate economic, environmental, and social sustainability performance transformation through ESG disclosure”,Sustainability, Vol. 12 No. 9, p. 3910.

Ashrafi, M., Walker, T.R., Magnan, G.M., Adams, M. and Acciaro, M. (2020), “A review of corporate sustainability drivers in Maritime ports: a multi-stakeholder perspective”,Maritime Policy & Management, Vol. 47 No. 8, pp. 1027-1044.

Astrachan, J.H., Binz Astrachan, C., Campopiano, G. and Bau`, M. (2020), “Values, spirituality and religion: family business and the roots of sustainable ethical behavior”,Journal of Business Ethics, Vol. 163 No. 4, pp. 637-645.

Awan, U. (2019), “Impact of social supply chain practices on social sustainability performance in manufacturing firms”,International Journal of Innovation and Sustainable Development, Vol. 13 No. 2, pp. 198-219.

Barako, D.G. and Brown, A.M. (2008), “Corporate social reporting and board representation: evidence from the Kenyan banking sector”,Journal of Management & Governance, Vol. 12 No. 4, pp. 309-324.

Barney, J. (1991), “Firm resources and sustained competitive advantage”,Journal of Management, Vol. 17 No. 1, pp. 99-120.

Bayraktar, C.A., Hancerliogullari, G., Cetinguc, B. and Calisir, F. (2017), “Competitive strategies, innovation, and firm performance: an empirical study in a developing economy environment”, Technology Analysis & Strategic Management, Vol. 29 No. 1, pp. 38-52.

Bentley, K.A., Omer, T.C. and Sharp, N.Y. (2013), “Business strategy, financial reporting irregularities, and audit effort”,Contemporary Accounting Research, Vol. 30 No. 2, pp. 780-817.

Carter, C.R. and Rogers, D.S. (2008), “A framework of sustainable supply chain management: moving toward new theory”,International Journal of Physical Distribution & Logistics Management, Vol. 38 No. 5, pp. 360-387.

Castka, P. and Corbett, C. (2016), “Adoption and diffusion of environmental and social standards: the effect of stringency, governance, and media coverage”,International Journal of Operations & Production Management, Vol. 36 No. 11, pp. 1504-1529.

Chen, Y. and Jermias, J. (2014), “Business strategy, executive compensation and firm performance”, Accounting & Finance, Vol. 54 No. 1, pp. 113-134.

Chen, C.C., Shih, H.S., Shyur, H.J. and Wu, K.S. (2012), “A business strategy selection of green supply chain management via an analytic network process”,Computers & Mathematics with Applications, Vol. 64 No. 8, pp. 2544-2557.

Chin, W.W. (2010),How to Write up and Report PLS Analyses: Handbook of Partial Least Squares, Springer, Berlin.

Connelly, B.L., Certo, S.T., Ireland, R.D. and Reutzel, C.R. (2011), “Signaling theory: a review and assessment”,Journal of Management, Vol. 37 No. 1, pp. 39-67.

Connelly, S., Markey, S. and Roseland, M. (2011), “Bridging sustainability and the social economy:

achieving community transformation through local food initiatives”,Critical Social Policy, Vol. 31 No. 2, pp. 308-324.

Dubey, R., Gunasekaran, A., Papadopoulos, T., Childe, S.J., Shibin, K.T. and Wamba, S.F. (2017),

“Sustainable supply chain management: framework and further research directions”,Journal of Cleaner Production, Vol. 142, pp. 1119-1130.

Dutta, K. and Ring, J.K. (2021), Stakeholder Protection and Valuation Effects in Business with a Conscience, Routledge, Oxfordshire.

Fassin, Y., De Colle, S. and Freeman, R.E. (2017), “Intra-stakeholder alliances in plant-closing decisions: a stakeholder theory approach”,Business Ethics: A European Review, Vol. 26 No. 2, pp. 97-111.

Fornell, C. and Larcker, D.F. (1981),Structural Equation Models with Unobservable Variables and Measurement Error: Algebra and Statistics, University of Michigan, Ann Arbor, MI.

Freeman, R.E. (1984), “Strategic management: a stakeholder theory”,Journal of Management Studies, Vol. 39 No. 1, pp. 1-21.

Freeman, R.E. (2010),Strategic Management: A Stakeholder Approach, Cambridge University Press, Cambridge, MA.

Freudenreich, B., Lu¨deke-Freund, F. and Schaltegger, S. (2020), “A stakeholder theory perspective on business models: value creation for sustainability”,Journal of Business Ethics, Vol. 166 No. 1, pp. 3-18.

Giannakis, M. and Papadopoulos, T. (2016), “Supply chain sustainability: a risk management approach”, International Journal of Production Economics, Vol. 171, pp. 455-470.

Gualandris, J., Klassen, R.D., Vachon, S. and Kalchschmidt, M. (2015), “Sustainable evaluation and verification in supply chains: aligning and leveraging accountability to stakeholders”, Journal of Operations Management, Vol. 38 No. 1, pp. 1-13.

Hahn, R., Spieth, P. and Ince, I. (2019), “Business model design in sustainable entrepreneurship:

illuminating the commercial logic of hybrid businesses”, Journal of Cleaner Production, Vol. 176, pp. 439-451.

Hair, J.F., Ringle, C.M. and Sarstedt, M. (2013), “Partial least squares structural equation modeling:

rigorous applications, better results and higher acceptance”,Long Range Planning, Vol. 46 Nos 1/2, pp. 1-12.

Hair, J.F., Jr, Matthews, L.M., Matthews, R.L. and Sarstedt, M. (2017), “PLS-SEM or CB- SEM: updated guidelines on which method to use”,International Journal of Multivariate Data Analysis, Vol. 1 No. 2, pp. 107-123.

Hair, J.F., Jr, Hult, G.T.M., Ringle, C.M., Sarstedt, M., Danks, N.P. and Ray, S. (2021),Partial Least Squares Structural Equation Modeling (PLS-SEM) Using R: A Workbook, Springer Nature, Berlin.

Harrington, L.M.B. (2016), “Sustainability theory and conceptual considerations: a review of key ideas for sustainability, and the rural context”,Papers in Applied Geography, Vol. 2 No. 4, pp. 365-382.

Hart, S.L. (1995), “A natural-resource-based view of the firm”,The Academy of Management Review, Vol. 20 No. 4, pp. 986-1014.

Herremans, I.M., Nazari, J.A. and Mahmoudian, F. (2016), “Stakeholder relationships, engagement, and sustainability reporting”,Journal of Business Ethics, Vol. 138 No. 3, pp. 417-435.

Hoejmose, S., Brammer, S. and Millington, A. (2013), “An empirical examination of the relationship between business strategy and socially responsible supply chain management”,International Journal of Operations & Production Management, Vol. 33 No. 5, pp. 589-621.

Jauhari, V. and Sanjeev, G.M. (2010), “Managing customer experience for spiritual and cultural tourism:

an overview”,Worldwide Hospitality and Tourism Themes, Vol. 2 No. 5, pp. 467-476.

Javed, M., Rashid, M.A., Hussain, G. and Ali, H.Y. (2020), “The effects of corporate social responsibility on corporate reputation and firm financial performance: moderating role of responsible leadership”, Corporate Social Responsibility and Environmental Management, Vol. 27 No. 3, pp. 1395-1409.

Kamasak, R. (2017), “The contribution of tangible and intangible resources, and capabilities to a firm’s profitability and market performance”,European Journal of Management and Business Economics, Vol. 26 No. 2, pp. 252-275.

Kock, N. (2015), “Common method bias in PLS-SEM: a full collinearity assessment approach”, International Journal of e-Collaboration (IJEC), Vol. 11 No. 4, pp. 1-10.

Kromjong, L., Rajpal, S., Thorns, M., Verkouw, R., Boulter, J., Dalalaki, R. and Hjaltadottir, A. (2016),Small Business Big Impact-SME Sustainability Reporting from Vision to Action, Global Reporting Initiative, Amsterdam.

Kurniawati, D. and Mawardi, M. (2021), “Pengembangan Instrumen Penilaian Sikap Gotong Royong Dalam Pembelajaran Tematik Di Sekolah Dasar”, Edukatif: Jurnal Ilmu Pendidikan, Vol. 3 No. 3, pp. 640-648.

Laasch, O. and Conaway, R. (2017),Responsible Business: The Textbook for Management Learning, Competence and Innovation, Routledge, Oxfordshire.

Lee, M.T. and Raschke, R.L. (2020), “Innovative sustainability and stakeholders’ shared understanding: the secret sauce to ‘performance with a purpose”,Journal of Business Research, Vol. 108, pp. 20-28.

Lin, W.L., Law, S.H. and Azman-Saini, W.N.W. (2020), “Market differentiation threshold and the relationship between corporate social responsibility and corporate financial performance”,Corporate Social Responsibility and Environmental Management, Vol. 27 No. 3, pp. 1279-1293.

Lozano, R. (2015), “A holistic perspective on corporate sustainability drivers”, Corporate Social Responsibility and Environmental Management, Vol. 22 No. 1, pp. 32-44.

Mahfouz, S.A., Awang, Z. and Muda, H. (2019), “The impact of transformational leadership on employee commitment in the construction industry”,International Journal of Innovation, Creativity and Change, Vol. 7 No. 10, pp. 151-167.

Mahfouz, J., Levitan, J., Schussler, D., Broderick, T., Dvorakova, K., Argusti, M. and Greenberg, M.

(2018), “Ensuring college student success through mindfulness-based classes: just breathe”,College Student Affairs Journal, Vol. 36 No. 1, pp. 1-16.

Mani, V., Gunasekaran, A. and Delgado, C. (2018), “Enhancing supply chain performance through supplier social sustainability: an emerging economy perspective”,International Journal of Production Economics, Vol. 195, pp. 259-272.

Martins, L.L., Rindova, V.P. and Greenbaum, B.E. (2015), “Unlocking the hidden value of concepts: a cognitive approach to business model innovation”,Strategic Entrepreneurship Journal, Vol. 9 No. 1, pp. 99-117.

Miles, R.E., Snow, C.C., Meyer, A.D. and Coleman, H.J. Jr. (1978), “Organizational strategy, structure, and process”,The Academy of Management Review, Vol. 3 No. 3, pp. 546-562.

Ng, W. and Al-Shaghroud, M. (2018), “Strategy-as-coping in medium-sized enterprises: a social process of collective sensing for acquisition opportunities”,Journal of Small Business Strategy (archive Only), Vol. 28 No. 2, pp. 16-32.

Noghiu, A.A. (2020), “Spiritual capital: a framework for spirituality-infused leadership education and organizational spirituality”,New Directions for Student Leadership, Vol. 2020 No. 166, pp. 45-59.

Pinelli, M. and Maiolini, R. (2016), “Strategies for sustainable development: organizational motivations, stakeholders’ expectations and sustainability agendas: strategies for sustainable development”, Sustainable Development, Vol. 25, doi:10.1002/sd.1653.

Podsakoff, N.P., MacKenzie, S.B., Lee, J.Y. and Podsakoff, N.P. (2003), “Common method biases in behavioral research: a critical review of the literature and recommended remedies”,Journal of Applied Psychology, Vol. 88 No. 5, pp. 879-903.

Porter, M.E. and Kramer, M.R. (2006), “The link between competitive advantage and corporate social responsibility”,Harvard Business Review, Vol. 84 No. 12, pp. 78-92.

Porter, M.E. and Kramer, M.R. (2011), “Creating shared value: redefining capitalism and the role of the corporation in society”,Harvard Business Review, Vol. 89 Nos 1/2, pp. 62-77.

Richter, U.H. and Dow, K.E. (2017), “Stakeholder theory: a deliberative perspective”,Business Ethics: A European Review, Vol. 26 No. 4, pp. 428-442, doi:10.1111/beer.12164.