No part of this document may be reproduced, stored in an automated retrieval system, or transmitted in any form or by any means, graphic, electronic, mechanical, photocopying, recording, scanning, or otherwise, without the prior permission of the authors. During these two trimesters for my graduation project, I am very grateful to UTAR, which allows me to have an individual graduation project to fulfill the requirement for the degree of Master of Business Administration or Corporate Governance. 38 Figure 2.5: The model of the relationship between board size and the duality of CEOs and company performance: evidence from Jordan.

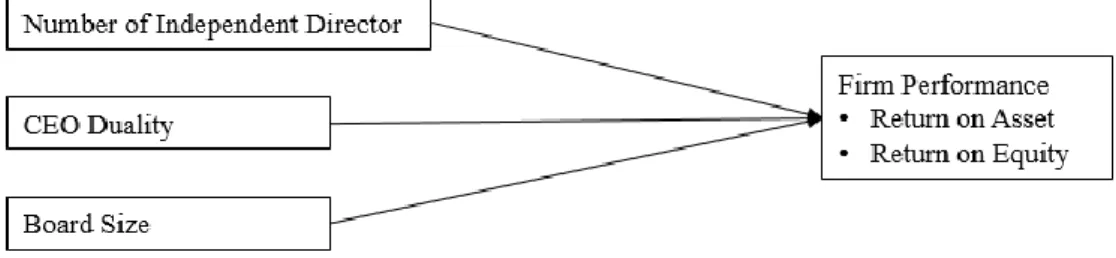

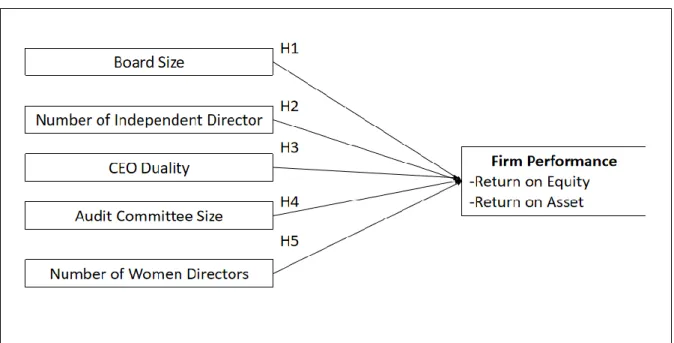

39 Figure 2.6: Modeling the effect of corporate governance on the performance of commercial banks in Kenya: a panel study. 40 Figure 2.7: Modeling the impact of CEO Duality and Audit Committee on business performance: a study of oil and gas listed companies in Pakistan. The size of the board of directors, the number of independent directors, the duality of the CEOs, the size of the audit committee and the number of female directors are selected as independent variables while the financial performance of the companies are known as the dependent variables and were measured by return on assets and return on equity.

Design/Methodology/Approach: In this research study, 43 family-controlled companies were selected. Moreover, the limited time and resources give to carry out this study, so the time period of company observation was only 5 years and only 43 the number of selected companies.

Introduction

- Introduction

- Research Background

- Problem Statement

- Research Objectives

- General Objectives

- Specific Objectives

- Research Question

- Hypothesis Development

- Scope of the Study

- Significant of Study

- Definition of Term

- Organisation of the Study

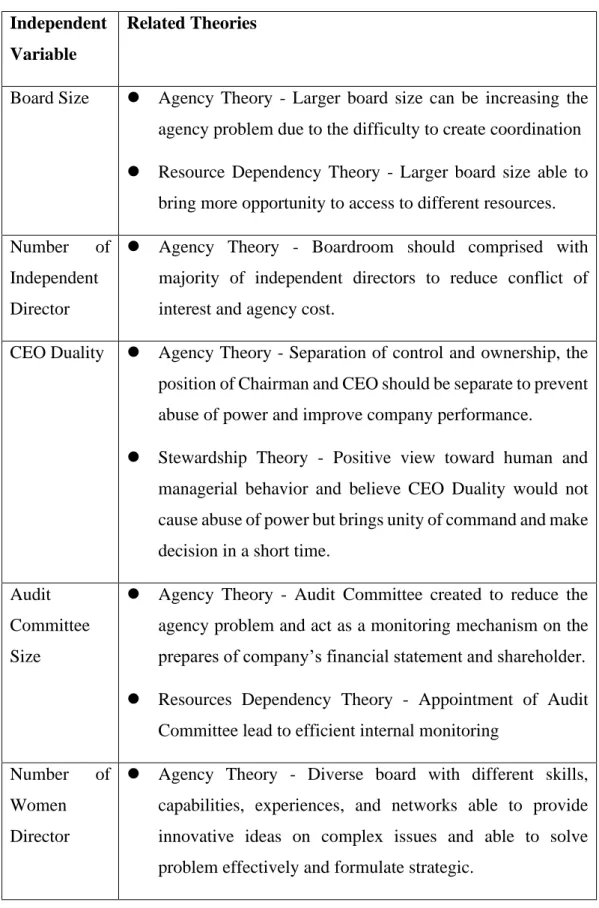

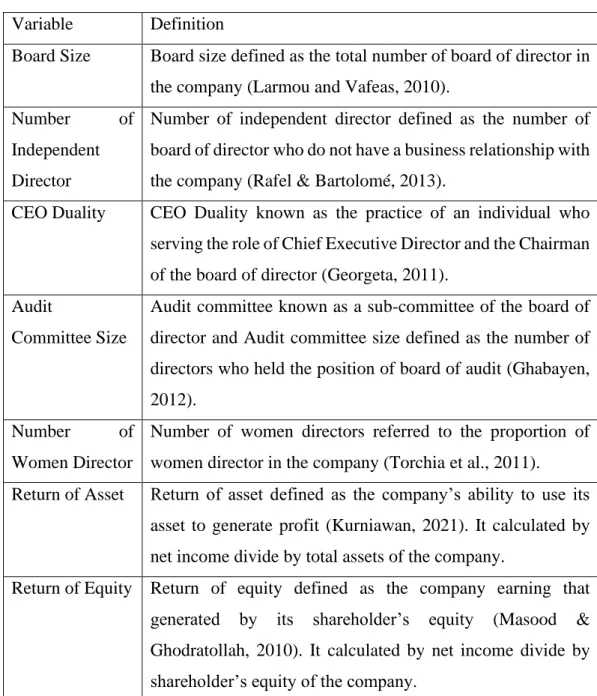

Boardroom refers to a room where a group of people hold meetings and the people known as board elected by shareholders of the company to manage the company (Daniel, 2021). A board of directors is a group of individuals elected by shareholder and make decisions as a fiduciary on behalf of shareholder (James, 2020). At the same time, an effective board must include the right group of people with the right skill, knowledge, experience and independent elements that suit the purpose of the company. The reason why the independent variable and dependent variable were chosen by this study will be discussed further in Chapter 2.

Most of the research studied on the corporate governance of family-controlled companies in a foreign country such as Australia, Taiwan and the Czech Republic (Bartholomeusz & Tanewski, 2006; Filatotchev et al., 2005; Odehnalová & Pirožek, 2018). For example, there is little research found that company board size has a negative relationship with firm performance (Guo & Kga, 2012; Hussin &. CEO Duality CEO Duality known as the practice of an individual serving the role of Chief Executive Officer and Chairman of the Board of Directors (Georgeta, 2011).

The audit committee is known as a sub-committee of the board of directors, and the size of the audit committee is defined as the number of directors who have held an audit committee position (Ghabayen, 2012). There are five chapters in this research and each of the chapters are interrelated.

Literature Review

- Introduction

- Family-Controlled Companies

- Boardroom

- Corporate Governance in Malaysia

- Underlying Theories

- Agency Theory

- Stewardship Theory

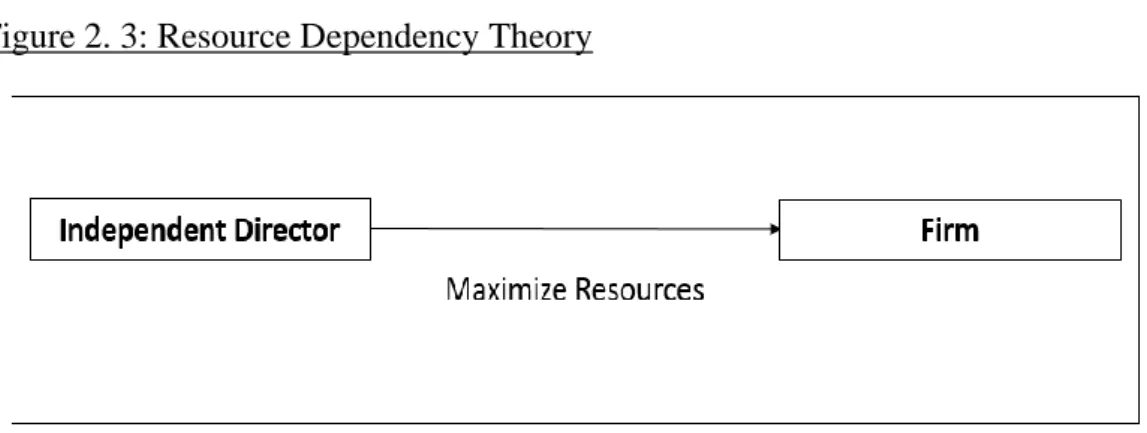

- Resource Dependency Theory

- Review of Literature

- Dependent Variables

- Independent Variables

- Hypothesis Development

- Board Size

- Number of Independent Director

- CEO Duality

- Audit Committee Size

- Number of Women Director

- Review of Relevant Theoretical Models

- Model 1

- Model 2

- Model 3

- Model 4

- Proposed Conceptual Framework

This chapter included the research background, problem statement, research objectives, research, questions, significance of the study, scope of the study, definition of terms, organization of the study and conclusion.

Methodology

Introduction

Research Design

Data Collection Method

- Secondary Data

Sampling Design

- Target Population

- Sampling Frame

- Sampling Element

- Sampling Technique

- Sampling Size

Research Instruments

Constructs Measurement

- Origin of Construct

- Scale Measurement

Data Processing

Data Analysis

- Descriptive Analysis

- Inferential Analysis

Data Analysis

Introduction

Descriptive Analysis

- Dependent Variables

- Independent Variables

From 2016 to 2020, 4 out of 43 family-controlled companies in Malaysia practiced CEO duality each year.

Panel Data Analysis

- Return on Asset

- Return on Equity

Discussion and Conclusion

Introduction

In addition, limitations of the research, recommendations for future research and conclusion are also included in this Chapter.

Statistical Analysis

- Descriptive Statistics of Dependent Variables

- Descriptive Statistics of Independent Variables

- Hypothesis Summary

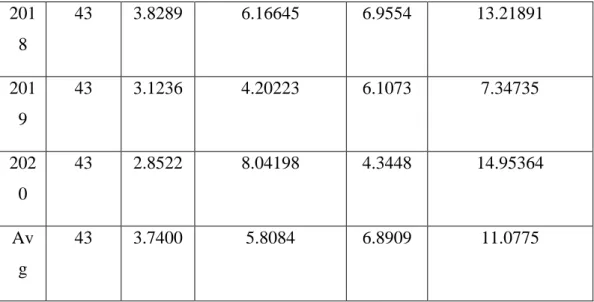

Furthermore, the mean value that appears in descriptive analysis for the board size in the family-controlled company is fluctuating. In addition, the descriptive analysis of the number of independent directors shows that there has been an increase in the average number of independent directors steadily from the year 2016 to the year 2020. According to MCCG 2017, the boardroom should include at least 50% of independent directors. director, whereas the boardroom should include a majority of the independent director for large companies.

Subsequently, the average number of female directors rises steadily from the year 2016 to the year 2020. The 64 responsibilities of the audit committee are to ensure that the company complies with the financial reporting standard. A study by Ashari and Krismiaji (2020) shows that the number of audit committees should not exceed 8.

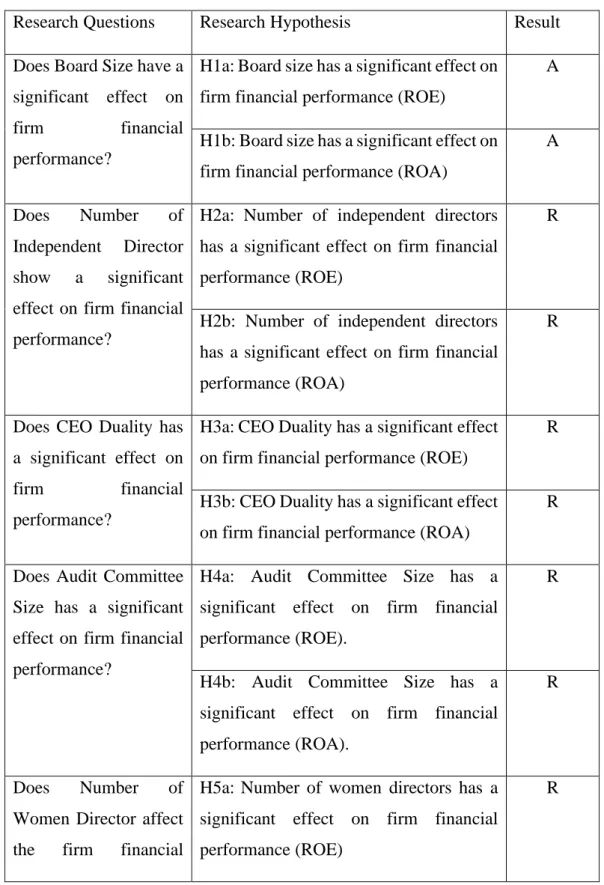

H1a: Board size has a significant effect on a company's financial performance (ROE) H1b: Board size has a significant effect on a company's financial performance (ROA). It thus shows that the size of the board has a significant effect on the financial performance of companies (ROE and ROA). This therefore indicates that the number of independent directors has a significant effect on the financial performance of companies (ROE and ROA).

H3a: CEO duality has a significant effect on firm financial performance (ROE) H3b: CEO duality has a significant effect on firm financial performance (ROA). Based on the panel data analysis result in Table 5.3 above, CEO Duality is insignificant to ROA and ROE. Therefore, it can be concluded that CEO Duality has no significant relationship with the firm's financial performance.

The result in Table 5.3 above shows that audit committee size has no significant effect on ROA and ROE. In conclusion, we can conclude that the size of the audit committee is not related to the financial performance of the company. In the end, we can conclude that the number of female directors does not have a significant impact on the company's financial performance.

Discussion on Findings

Nevertheless, the descriptive analysis in Table 4.3 shows that the mean average number of independent directors in family businesses was only 4.0326. So this could be why the study results show that the number of independent directors at 5% and 10 was not statistically significant and has no relation to companies' financial performance (ROA and ROE). The findings were supported by several studies, which showed that the number of independent directors does not have a significant effect on the financial performance of companies.

For example, the research conducted by Chang, David, Low and Tee (2021) found that the number of independent directors has an insignificant relationship with return on asset and equity. Furthermore, Arosa, Iturralde and Maseda (2013) also concluded that there is no significant relationship between the number of independent directors and return on assets. They also claimed that independent director not adding value in firm financial performance is due to the criteria for selecting the independent director.

70 family-controlled firm is in compliance with the MCCG code, however the findings of this research revealed that CEO duality was not statically significant at 5% and 10 and has no relationship with the firm's financial performance (ROA and ROE). They also stated that CEO duality does not correspond to firm financial performance, as the financial ratio may not be able to measure board or leadership roles in relation to firm value creation, however long-term metrics such as firm growth and stock prices can be useful measures. According to the research conducted by Ashari and Krismiaji (2020), they found that the ideal size of the audit committee is not more than 8.

However, the research results show that the size of the audit committee was not statistically significant at the 5% and 10% level and has no relationship with the company's financial performance (ROA and ROE). In addition, they stated that the size of the audit committee did not add value to the company's financial performance, this is because the size of the audit committee alone could not affect the company's financial performance. At the same time, see table 4.3, the average number of female directors has increased steadily.

Nevertheless, the research results show that the number of female directors was not statistically significant at the 5% and 10% level and has no correlation with the company's financial performance (ROA. 71 and ROE). This was supported by Amit, Shubham and Varda (2019) who found no effect between the number of female directors and return on assets. This is because the number of female directors is still very less in the company and unable to make an influential decision to affect the financial performance of the company.

Limitations in Research

Recommendations for Future Research

In addition, to get a more accurate result, the sample size of the number of family-controlled companies should be increased, as this study only shortlisted 43 family-controlled companies. Finally, future research can also conduct both quantitative and qualitative analysis for better understanding of the topic. For example, the future research may invite the board of directors to participate in the questionnaire to understand whether the corporate governance mechanism can contribute to improving the company's financial performance.

Conclusion

An analysis of board size and firm performance: evidence from NSE firms using a panel data approach. The role of board size in corporate governance and firm performance using the Pareto approach is a cultural phenomenon. Corporate governance and the board of directors: The effect of board composition on corporate sustainability performance.