First and foremost, we would like to thank our university, the University of Tunku Abdul Rahman (UTAR) for giving us this opportunity to conduct this research and providing us with all the funds at some point of the tour. We can also get the right of entry to journals in addition to studying library materials with the help of the staff without difficulty. We are grateful for her guidance, suggestions, motivation and determination throughout the development of these studies.

This examination is submitted to fulfill part of the Bachelor of Economics (HONS) Financial Economics requirement. This study examines the relationship between income, level of education, family size and age with the consumption of life insurance. The purpose of this article is to determine the relationship between demographic factors, such as income, education level, family size and age, and the consumption of life insurance.

RESEARCH OVERVIEW

- Introduction

- Problem Statement

- Research Objectives

- Research Questions

- Significance of Study

- Structure of Study

- Chapter Summary

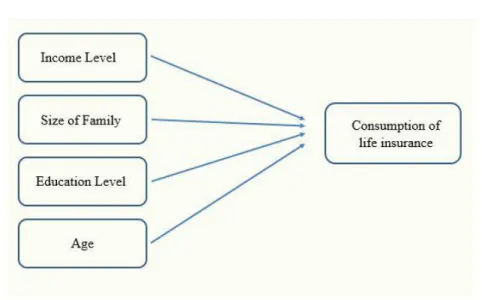

In our research, we will focus on the relationship between the 4 demographic factors, which are income, family size, education level and age in relation to consumers' consumption of life insurance. Thus, it is crucial to analyze the consumption of insurance products to increase the penetration of life insurance and improve the risk management level of Malaysians against unexpected events. To analyze the positive relationship between family size and life insurance consumption.

It is undeniable that raising awareness of the importance of life insurance in Malaysian society is a must as we have relatively low life insurance penetration rates compared to other developing countries. By improving awareness of life insurance, it can increase the demand for life insurance. Once there is an increase in demand for life insurance products, it would encourage competition among each of the insurance companies.

LITERATURE REVIEW

- Introduction

- Underlying Theories

- Locus of Control

- Review of Variables

- Dependent Variables

- Independent Variables

- Hypotheses Development

- Income Level

- Size of Family

- Education Level

- Age

- Proposed theoretical framework

In their study, age was found to be statically significant in influencing life insurance consumption in Ethiopia. Furthermore, it is found that there is a significant association between demographic factors such as gender, education level, income level and children's education with life insurance consumption in India. The results of their research showed that the level of income has a positive effect on the consumption of life insurance.

Alhassan and Biekpe's (2016) research results also showed that there is a negative relationship between income level and consumption of life insurance. According to Loke.Y and Goh.Y (2012), education has a decisive influence on the consumption of life insurance. Based on the correlation and hypothesis testing by Juliana.A (2018), the results of education factors show positive correlation with the consumption of life insurance.

The correlation coefficient between education level and life insurance consumption is 0.277, so the result supported our hypothesis. Thus, our research is examining that the level of education is positively affecting the consumption of life insurance. From the research done by Yin.G (2015), the age of the respondents was found to have a positive relationship with the use of life insurance.

Moreover, according to the research of Chun. 2013), it turned out to have a significant positive correlation between age and consumption of life insurance. In short, it shows that as age increases, the consumption of life insurance will increase. This result indicated that there is no relationship between age and life insurance consumption.

According to Beh, Lee, Tam, and Wong (2018), when income increases, the demand for life insurance increases.

METHODOLOGY

- Introduction

- Research Design

- Quantitative Research Design

- Descriptive Research Design

- Data Collection Methods

- Primary data

- Secondary data

- Sampling Design

- Target Population

- Sampling frame and sampling location

- Sampling Technique

- Sample Size

- Research Instrument

- Pilot Test

- Constructs Measurement

- Data Processing

- Data Checking

- Data Editing

- Data Coding

- Data Cleaning

- Data Analysis

- Descriptive Analysis

- Scale Measurement

- Inferential Analysis

The data collected for other purposes but relevant to current research needs is called secondary data. We can also say that the data was previously collected by others and now anyone can use it. For example, nominal data allows the data to be categorized by labeling it into mutually exclusive groups, with no order such as marital status, gender, and ethnicity.

In this section, we will use the data we have collected to create useful information in this section. Once we receive the answers from our respondents, we will double check that the data for each question is correct. If data collected from respondents is not consistent with other answers, we may edit the data based on the respondent's previous answer. Consequently, data editing will remove these erroneous data and thus increase the reliability of the study.

For example, data such as gender with answers male and female can be transferred to code 1 and code 2. We chose to use SPSS software for the data analysis program. With this program, we were able to organize the data and calculate the statistics collected from the respondents' questionnaires. Descriptive analysis is a form of data analysis in order to understand the data collected from the questionnaire more clearly and transparently.

Descriptive analysis is a type of data analysis that helps explain, display, or summarize data points in a constructive way so that patterns can be developed that meet all the conditions of the data (Rawat. The mean and standard deviation of the data define the normal distribution , which is a symmetrical continuous distribution. Skewness is a metric for measuring asymmetry in distributions This chapter discusses in depth the data collection process, sampling design, survey design, research instrument, and other topics.

Moreover, this chapter also discussed how to analyze data from the respondents using SPSS.

DATA ANALYSIS

- Introduction

- Descriptive Analysis

- Respondent Demographic Profile

- Central Tendencies Measurement of Constructs

- Scale Measurement

- Normality Test

- Reliability Test

- Inferential Analysis

- Multiple Linear Regression

- Conclusion

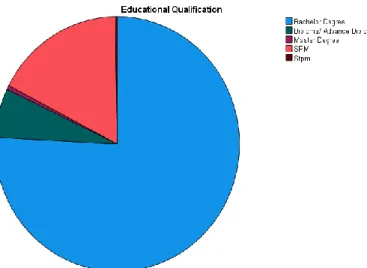

From the graph shown in Table 4.1, the respondents who bought life insurance constituted the majority of the respondents compared to the respondents who did not buy it. From table 4.4 it can be seen that the highest education of the majority of the respondents is a bachelor's degree, with 292 people, with 75.8%, while the second largest was SPM with the amount of 66 or 17.1% of the respondents. Income level (IV 1) has the largest standard deviation, while education level (IV 3) has the lowest.

In our study, life insurance consumption (-0.834) shows the lowest bias, while age shows the highest bias (-0.419). On the other hand, Age (-0.874) shows the lowest kurtosis, while education level is the highest in kurtosis (0.392). According to Table 4.1, it shows the reliability test result for all the 5 items included the dependent variable and the independent variables.

Based on our study, the Cronbach value is 0.83, which means that the reliability test result is categorized within the good range, which is 0.8 to 0.9. According to Table 4.3, the correlation coefficient value for this study is 0.720, which showed a positive and high correlation between dependent variables and independent variables. Based on R2 (0.518), it shows that 51.8% of the change in life insurance consumption can be explained by all 4 independent variables, while the rest of the 48.2% can be explained through other excluded independent variables.

This indicates that income level, family size, education level and age are statistically significant for life insurance consumption. Based on the comparison, age (0.236) contributes the largest impact to life insurance consumption. Meanwhile, education level (0.077) is considered the lowest impact factor for life insurance consumption.

Through the equation it can be explained that when there is an increase in income level, family size, education level and age, life insurance consumption will increase by 23.6% respectively.

DISCUSSION, CONCLUSION AND IMPLICATIONS

- Introduction

- Discussion on Major Findings

- Income Level

- Size of Family

- Education Level

- Age

- Implications of Study

- Managerial Implications

- Limitation of the Study

- Sampling Bias

- Limitation of sample size

- Limitation of research model

- Recommendations for Future Research

- Conclusion

Family size was found to be positively related to life insurance consumption. In addition, correlation and hypothesis testing by Juliana.A (2018), the results of education factors show positive correlation with life insurance consumption. Throughout the study, age is found to have the highest positive impact on life insurance consumption.

The correlation shows that with every increase in age, consumption of life insurance will increase by 23.6%. G (2015) the MLR p-value is 0.02, which is less than 0.05, which means that there is a significant relationship between age and life insurance consumption. Throughout the study, the factors that influence demographics towards the consumption of life insurance are indicated.

In this research, all independent variables including age, income level, education level and family size were shown to be significantly related to life insurance consumption. In our research, we only examine demographic factors in the consumption of life insurance. According to our study, four factors were found to have a positive effect on life insurance spending.

Determinants of life insurance penetration in OECD countries: the asymmetric effect of income level (Doctoral dissertation, UTAR). Nominal, Ordinal, Interval & Ratio Data. https://gradcoach.com/nominal-ordinal-interval-ratio/. 2018) Demographics, Economics, and Psychographic Determinants of Life Insurance Consumption Among Schools. Determinant of life insurance consumption among university Tunku Abdul Rahman employees in Perak campus (Doctoral dissertation, UTAR).

An empirical analysis of marketing mix in the life insurance industry to purchase decisions of life insurance products.

Please indicate how much you agree or disagree with the following question using a 5-point Likert scale: Strongly Disagree = 1, Disagree = 2, Neutral = 3, Agree = 4, and Strongly Agree agree = 5. Circle one number to indicate how much you agree or disagree with the following question. A society with a higher education is likely to have more knowledge about how to avoid the unfortunate events. I believe that with a higher level of education it will alert me to the importance and benefits of an insured life.

Please indicate how much you agree or disagree with the following question using the 5-point Likert scale: Strongly Disagree = 1, Disagree = 2, Neutral = 3, Agree = 4.