This thematic paper implements the principle of discounted cash flow valuation mythology to evaluate the intrinsic value of KCE Electronics Public Company Limited's share price. Typically, the derived result of KCE's fair value is incorporated into all of these named components.

VALUATION VALUATION

Highlights

With a small fluctuation in the European economy, this will result in a large fluctuation for the company's business.

Business Description

- Company Background

- KCE Group

Currently, its registered capital is 3,600,000 Baht. it was formed with the objectives of being the local distributor of PCBs in Thailand. It was formed with the objectives of being a PCB paint manufacturer and PCB chemical recycling company.

Macro-Economic Analysis

Moreover, the foreign investors tend to increase investments across AEC countries as a result of Asean's economic growth. In KCE's view, AEC would benefit from a good opportunity to expand its PCB market to the Asean region as the benefit of tax is presented across AEC countries.

Industry Analysis

In detail, the production of PCBs in China has increased and the market share has increased continuously due to the government's stimulus scheme and lower production cost. In the future, China will be the largest producer of PCBs in Asia, with approximately 48% of the market. In the US and Europe, there has recently been a downward trend in PCB production, reflected by the higher cost of production.

As a conclusion, for any PCB manufacturers with an old-fashioned production process and relying heavily on imported raw materials, they will actually be affected by the world's most powerful PCB manufacturer, China, in terms of cost savings. Also for the current leaders in the market there is a big challenge for them to maintain their leading positions. According to a projection by Nikkei, a Japanese stock market index, the automotive industry improved during 2013 and is expected to improve further due to an expansion in the global passenger car market.

Alternatively, to alleviate this problem, more attention has been paid to the development of hybrid and electric cars. For PCBs, as a key component, there is a positive outlook for PCBs in the automotive electronics industry.

Competition Analysis

- Competition Opportunities Lower raw material cost: Lower raw material cost

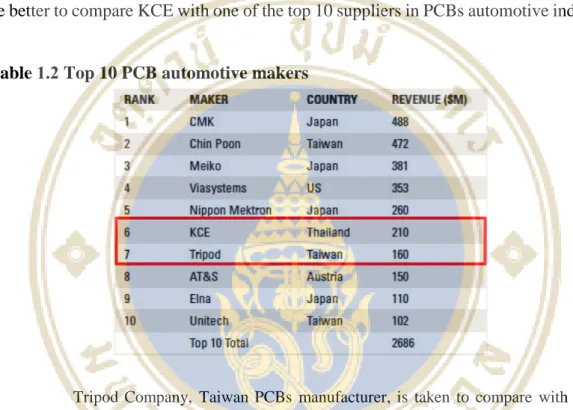

- Comparison to Major Competitor

Additionally, currently in the process of setting up a new factory near its headquarters in LatKrabang, Bangkok, the production floor will be over 500,000 sqft and once all phases are completed, the PCB production capacity will reach at 2,000,000 sqft/month. With the completion of construction of KCE's fourth PCB manufacturing facility later in 2014, KCE will be ideally positioned to capitalize on the anticipated growth in PCB demand in the coming years. Foreign Competitor: Describe the fact that 75% of KCE's revenue in 2013 came from export sales of PCBs to the automotive industry.

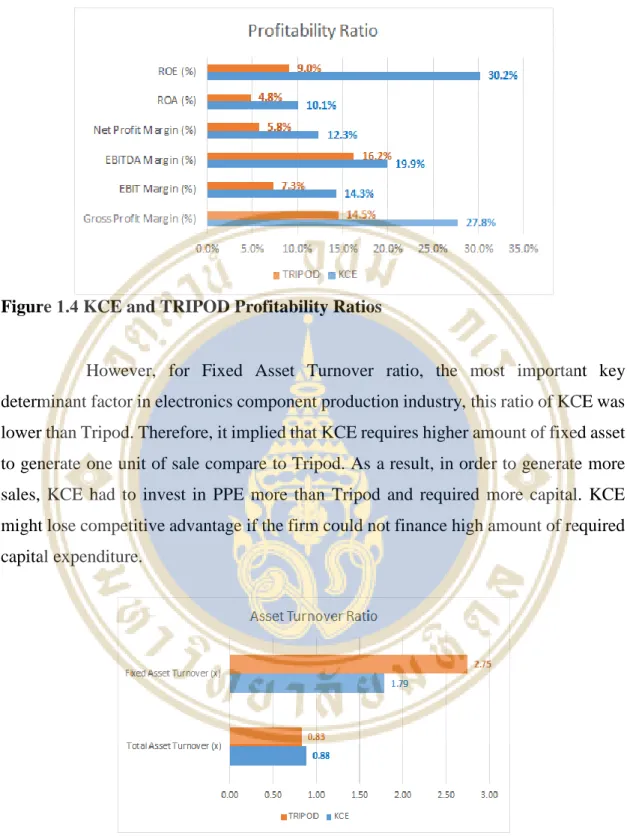

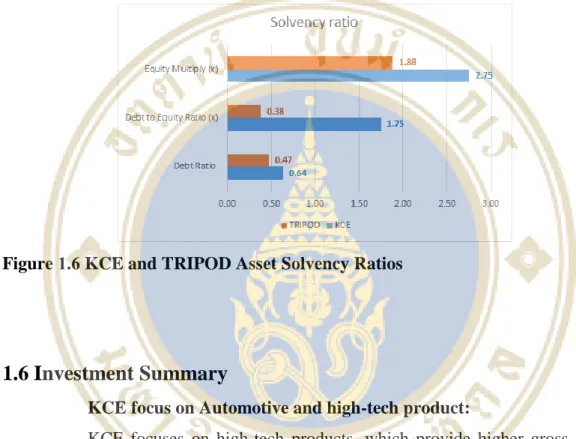

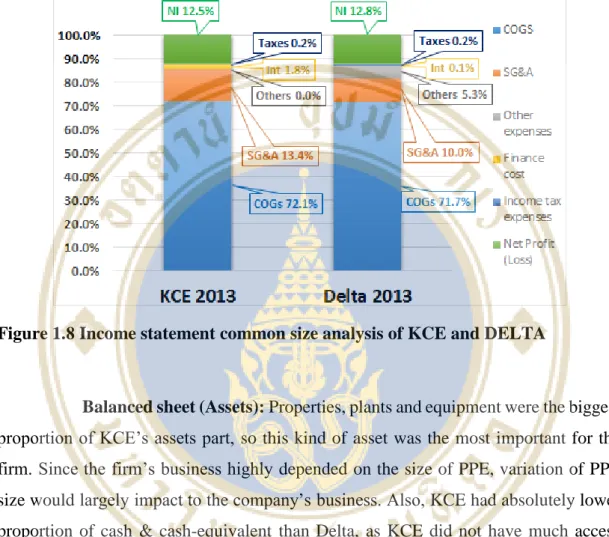

Efficiency ratio, in terms of gross profit margin, net profit margin, ROA and ROE, KCE's performance was better than Tripod in all dimensions of profitability. They were reflected from KCE's better management of COGs, SG&A and income tax. However, for the fixed asset turnover ratio, the most important key determinant in the electronics component manufacturing industry, this ratio of KCE was lower than that of Tripod.

In addition, Taiwan's credit rating (A+) is higher than Thailand's (BBB+), so if KCE had to be financed by a foreign financial institution, the financing costs would also be higher. As a result, enterprise value, EV and other parameters related to WACC will be affected by higher capital costs.

Investment Summary

At full capacity of the newly installed factory, the company will be able to grow its turnover by an average of 25.5% per year. Especially for KCE, a high dividend payout is an essential strategy to encourage investors to invest in the company's shares. In the past, KCE paid dividends on net profit by using excessive amounts of cash.

The decline in cost of goods sold is reflected by proper management of production activities, which enables high capacity utilization and improves efficiency. Therefore, the company not only reduces the cost of goods sold, but also increases the product distribution channel. Moreover, the company has a joint venture in Singapore and America as a sales representative abroad for distribution.

As a result of KCE's efforts, the Stock Exchange of Thailand and the Securities and Exchange Commission positioned KCE as "Very Good" in 2013. As a result of very good corporate governance, the company has continuously developed its operation and management to the reliable position.

Valuation

- Discounted Cash Flow Model: Free Cash Flow to firm

- Major components and key assumptions of FCFF

- Terminal Value Component Assumptions

- Weighted Average Cost of Capital Calculation

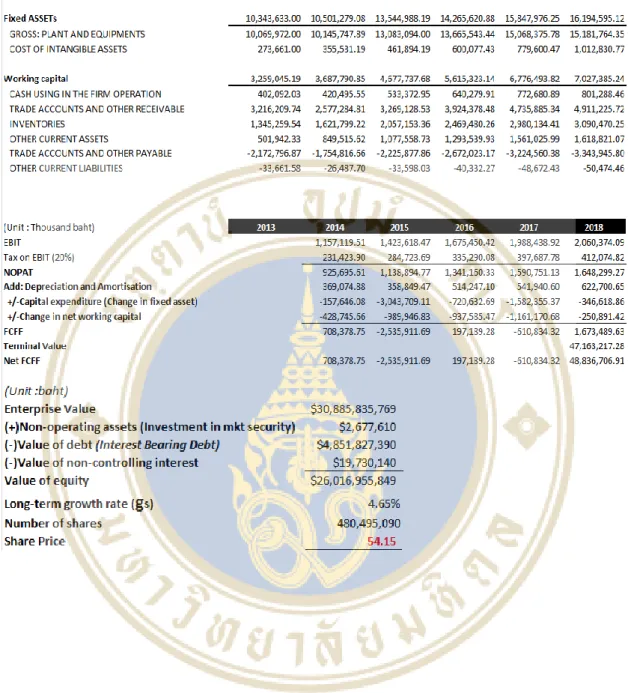

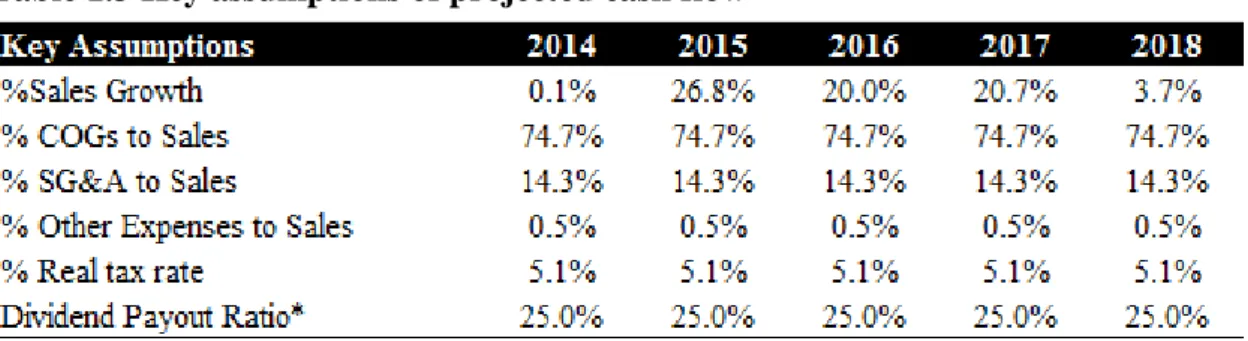

After subtracting the EV from the value of interest-bearing debt, non-operating assets, minority interests and the value of equity, the result will be the value of the equity of the company. Capital expenditures are directly related to the company's sales growth during an abnormal growth period. During the period of high investment in gross PPE, from 2015 to 2017, the company's sales growth increases sharply, and it will take a year in 2018 as a transition period to approach stable growth.

Constant growth of 4.62% is derived assuming weighted averages between the expected long-term nominal GDP growth of the main export destinations (US, EU, Asia, Thailand**) and the percentage of average sales in each region. (historical data). Note that Asian GDP is the average long-term GDP of the company's four main Asian customers (Japan, China, India, and South Korea). Finally, the firm's adjusted beta is taken from SETSMART, which is equal to 0.77.

We then performed the weighted average calculation and obtained the pre-tax value Kd = 5.38%. WACC: For the value of interest-bearing debt, we adopted this variable from the company's 2013 financial position.

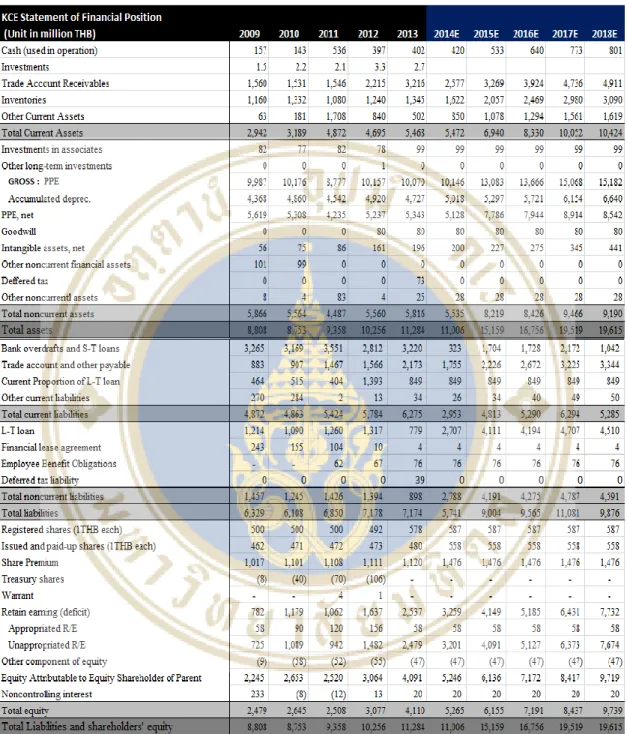

Financial Analysis

- Size Analysis

- Common Size Analysis

- Trend Analysis

- Financial Ratios Analysis

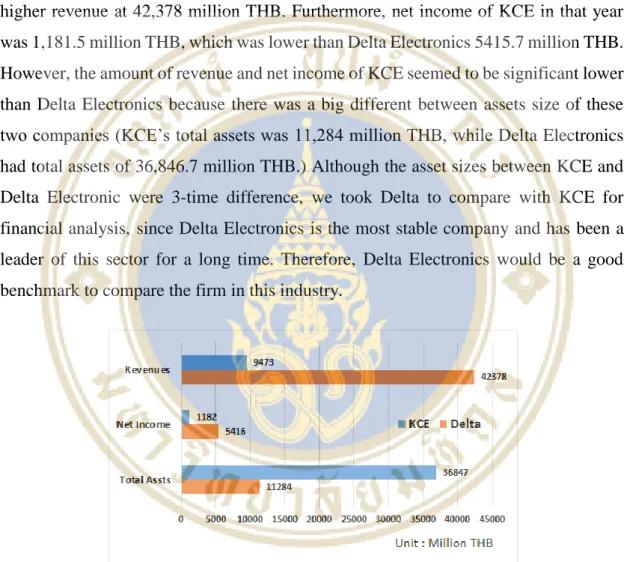

Balance Sheet (Assets): Real estate, plant and equipment made up the bulk of KCE's assets, so these types of assets were the most important to the company. For PPE, KCE had a significantly higher share of PPE than Delta, because the production of KCE's products required more expensive machinery and advanced technology. Finally, the size of KCE's accounts receivable was quite large due to the large amount of credit term offered to the customer.

In addition, KCE's share of operational liabilities was lower than Delta's, so KCE may require more internal or external resources than Delta to finance its NOWC. In addition, KCE's 12.3% net profit margin that year was slightly less than Delta's 12.8% net profit margin due to KCE's higher financial costs. The reason behind KCE's very high ROE, while profit margins were close, was that KCE had higher leverage than DELTA.

Although KCE's ROE is higher than Delta's, KCE needs to make better use of its assets, as a lower ROA than Delta's represents a lower return per unit of asset. Solvency Ratio: The ratio represents KCE's higher risk relative to peers and industries.

Investment Risks and Downside Possibilities

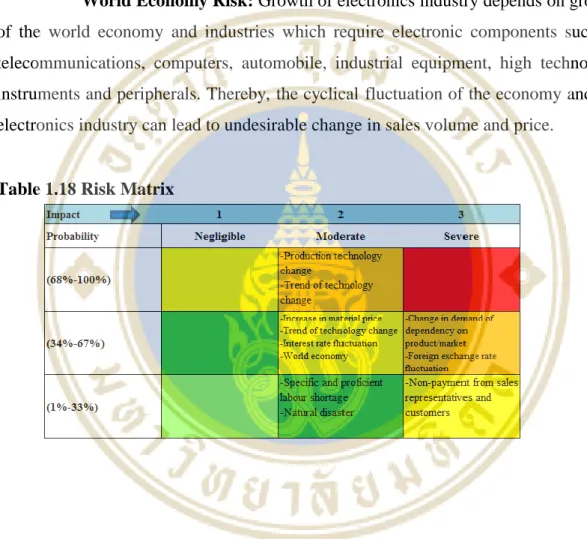

Materials price risk: As most of KCE's raw materials must be imported, shortages of key materials such as gold, copper and copper foil could cause production to be disrupted. Since PCBs are a basic and irreplaceable component of all electronic products, the technological risks of KCE are mainly related to detailed changes in design, manufacturing techniques and types of raw materials. Product dependence or market risk: Strong dependence on the automotive industry and the European market is a risk for the company in the event of a major change in product demand in this category or in this particular share of 70-75%.

Interest rate risk: With higher debt ratio (mostly on short-term debt), lower interest coverage ratio than competitors and industry, if the interest rate is fluctuating and tends to rise continuously, the company and subsidiaries are exposed to risks from interest rate uncertainty related to the cash deposit, the overdraft account and the bank loan. The company is exposed to risk from exchange rates related to the purchase of raw materials and sales dollars, approx. 50% Risk of non-payment by sales representatives and customers: Fifty percent of the company's total sales are made through their sales representatives, and the remainder is sent directly to customers.

Therefore, there are risks of non-payment by agents or customers, which affect the company's liquidity and operations. Here, the cyclical fluctuations of the economy and the electronic industry can cause unwanted changes in the volume and price of sales.

DATA DATA

- Income Statement

- Balance Sheet

- Statement of Cash Flow

- Financial Ratio

- Estimated Sale Growth

- Estimated Stable Growth

- Five Forces Analysis

- SWOT Analysis

From the growth in the automotive industry, PBC will demand more as a component so that the company has high bargaining power of customers as high quality products. Therefore, the company can provide full commercial and technical support to customers worldwide. Has its own lamination and main supply of raw materials: The company has subsidiaries that provide the essential raw material for the production of PCBs.

And KCE Taiwan Co., Ltd. is a foreign purchasing representative for raw materials and machinery for the company. Therefore, the company can produce the essential raw materials itself, so that the company has more power in negotiating with the supplier. Fluctuations in the exchange rate can affect operations: Almost all of KCE produces for export, so company volatility affects the operation of the company.

This is likely to have a negative impact on the company's revenue, operating income and net income. From the government policy, it makes the company higher costs and expenses due to Bt300 daily minimum wage policy. In addition, it also makes the loss in the company's asset and increase in costs for impairment.

So the company must develop the technology in the production process and the quality product continuously for the satisfaction of the customer.