Finally, I would like to express my deepest appreciation to the College of Management, Mahidol University, the instructors and all the staff who supported me throughout the course. The Price/Earnings per Share, Price/Book Value, Enterprise Value/Sales and Enterprise Value/EBITDA methods are implemented in this paper to predict the value of MK Restaurant Group Public Company Limited. The competitors that most likely have the same business structure as MK Restaurant are CENTEL, MINT and OISHI.

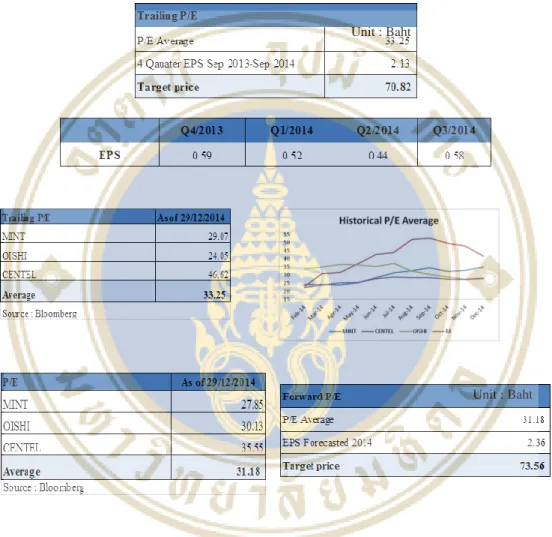

The results of the calculation for each method consisting of the price-to-earnings ratio, the price-to-book value of business to sales ratio and the business to EBITDA ratio are baht for the trailing method and 66.05 baht for the forward method, respectively. huge discrepancy between MK Restaurant's market price on December 4, 2014 at 60 baht and the relative valuation method.

Excessive of cash with Upside potential on inorganic growth

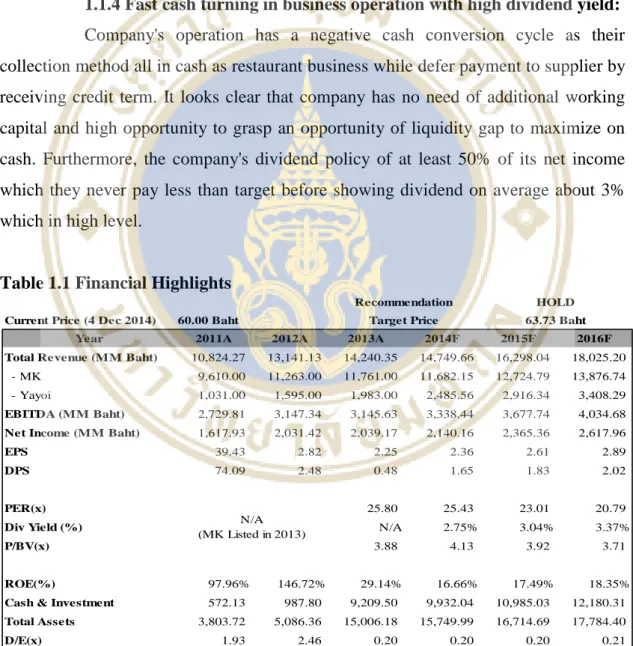

Fast cash turning in business operation with high dividend yield

Business Description

Company Background

Products and Services

MK Gold Restaurant is similar to MK Suki, which is also operated by MK Restaurant Group Plc. The first branch is located at Siriraj Hospital under the CSR program, which contributes all profits to the hospital. The Japanese restaurant Miyazaki was initially opened as the first branch in the Town in Town shopping center in October 2012.

Na Siam is a traditional Thai restaurant where the former MK restaurant company was located in Siam Square before the company began to focus on operating the Suki restaurant company. Le Siam is also a premium traditional Thai restaurant that caters to foreign customers and high-income earners who are looking for a luxurious place with the premium quality of unique Thai food. This store falls under the company's CSR program that donates all profits to Siriraj Hospital.

MK and Yayoi brands also offer a home delivery service available from 10am to 9pm with a minimum purchase price of 199 baht and 150 baht respectively. In addition to the catering services, MK and Yayoi also allow advance orders and prepare a range of food for all events. The company also expects to offer a full catering service that will provide all facilities including pots, electronic outlets, dining tables and wait staff to make customers feel like they are in a restaurant.

Macro-Economic Analysis and Industry Analysis

- Recovering in Thailand Economic

- Potential growth in Restaurant industry

- Increasing trend of chain restaurant

- Changing in lifestyle of Thai's people

- Upcoming AEC in 2015

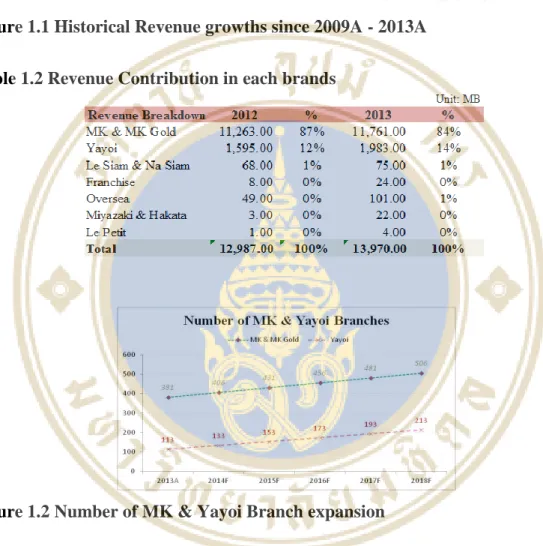

The growth rate of the restaurant business is related to the Thai economy and the country's population growth as it is classified as a basic need of human life and non-durable goods. However, the restaurant sector still has the potential to recover by the end of this year, which is reflected in the consumer index, business confidence index and Thailand's GDP. In 2013, the market value of restaurant chains is about 97,000 million baht, mainly divided into 6 types; Bakery, Chicken & Burger, Suki-Shabu, Japanese, Pizza and others.

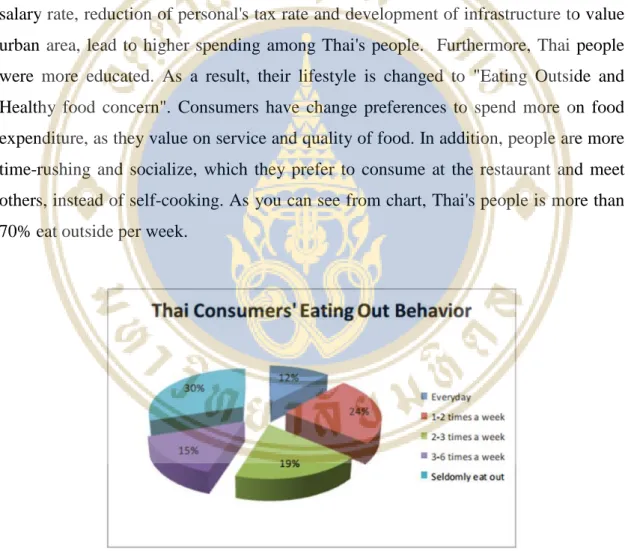

Japanese food category has also grown significantly at a rate of 20% per year, reflecting Thailand's trend towards Japanese food. Implementation of government policies, for example, increasing country's salary rate, reducing personal tax rate and developing infrastructure to appreciate urban area, lead to higher spending among Thai's people. As you can see from the chart, Thai people eat out more than 70% per week.

Competition Analysis

All outlets are located in shopping complexes, modern trade, community centers in Bangkok and the metropolitan area. Fuji Japanese Restaurants: The company dominates the Japanese Thai restaurant market with delicious and nutritious Japanese food. The business operation of OISHI Group is divided into two divisions; the first is the food business which consists of 9 Japanese restaurant brands with 193 stores such as OISHI Grand - An extraordinary and luxurious buffet environment with a limited time of 3 hours at the price per head of 749 Baht, OISHI Buffet - food buffet style Japanese with a limited time of 1 hour and 45 minutes at the price per head 519 Baht, Shabushi - buffet style Shabu with ingredients served along a conveyor (kaiten) along with various sushi priced at 339 Baht per head limited. 1 hour and 15 minutes, OISHI Ramen - A unique style of ramen and localized soup to meet the local taste, offers Japanese and spicy Thai menu, etc.

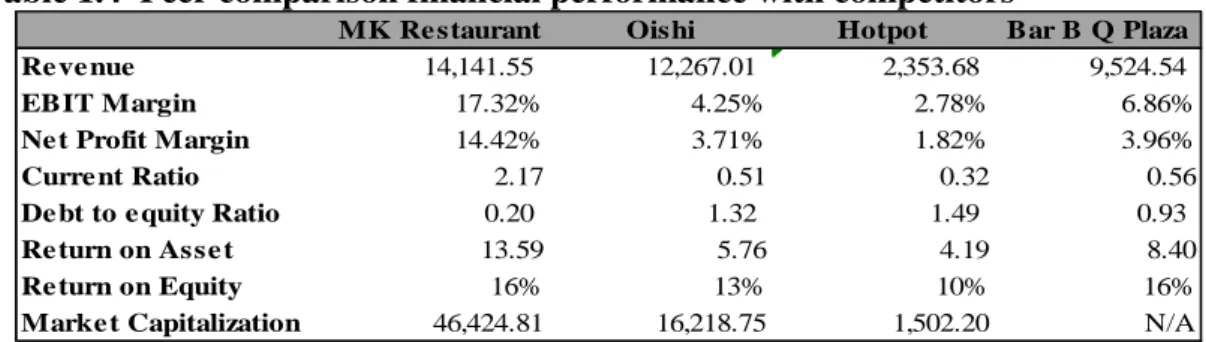

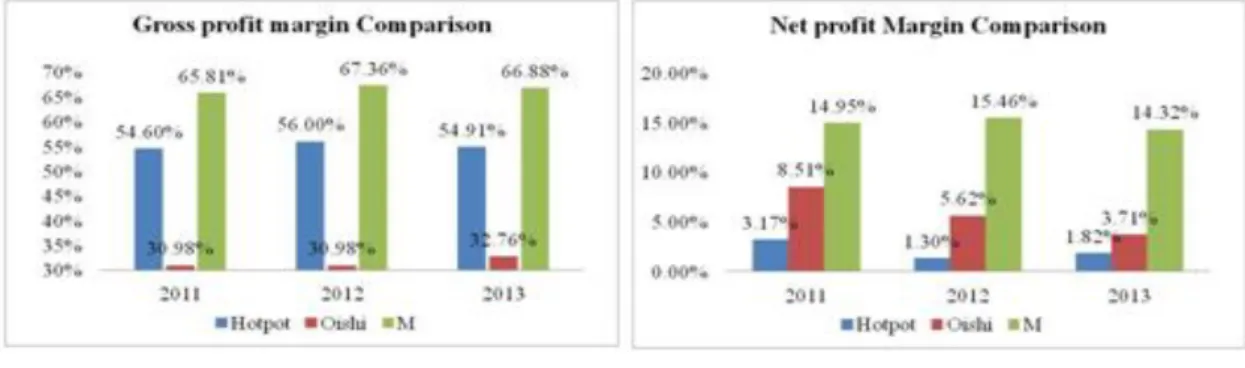

The second is the beverage business such as OISHI green tea, Fruito, Chakulza and Amino Plus. It is located in shopping malls, modern shopping centers and community centers like our company. From the peer comparison above, we saw that MK restaurant generated high profit margin, ROA, ROE compared to competitors as well as good cost control with good supply chain of self-training center and central kitchen.

Not only the profitability margin, the company also captures 60% of the total hot pot market in proportion to the sale of MK's Suki with the total hot pot market and 12% of the total Japanese restaurant being the market leader in pertains to sales and the number of branches. Moreover, the company has high financial flexibility with low liquidity and solvency risk as D/E ratio is low at 0.2 times and current ratio more than 1 times. Not only the financial strength of the company, but also good management and business structure show a proven track record.

Investment Summary

- Market leader in chain restaurant in Thailand

- Second source of income supportive from "Yayoi"

- Business growth opportunity by branch expansion and M&A Deal: Deal

- Sustainable cash generative business with high dividend profile

- High Standardization with Reliable of Supply chain and Expertise Management team Expertise Management team

The Yayoi brand drives about 14% of the company's total revenue, which is quite significant and supportive as there are still spaces available to grow in the Japanese restaurant market following the trend nowadays. Moreover, it is just entering the growth phase of the business with the highest branch in the Japanese restaurant segment. Currently, it starts to turn into a positive sign that people have confidence to spend more and its point of receiving business in the near future.

As the company has excess cash on hand plus long-term investment around 9 billion baht, which has enough cash to expand overseas and overseas branches following its plan and mall expansion. Furthermore, it has a great possibility to use their surplus fund to acquire business in the same industry to achieve target growth of around 20% per annum creating value through organic growth and inorganic growth. Company operating business with cash basis as all transactions were settled immediately in cash, while high bargaining on its supplier led to negative cash conversion cycle.

In terms of performance, the company can generate an operating profit margin and a net profit margin of approximately 18%. These factors enable the company to maintain a market leading position in the SUKI business and Japanese restaurants. Furthermore, the management team has a proven track record over the past 28 years that can certify the company's performance.

Multiple Valuations

- Price/Earnings Ratio (P/E)

- Price/Book Value

- Enterprise value /Sale Ratio (EV/Sale)

- Enterprise value /EBITDA (EV/EBITDA)

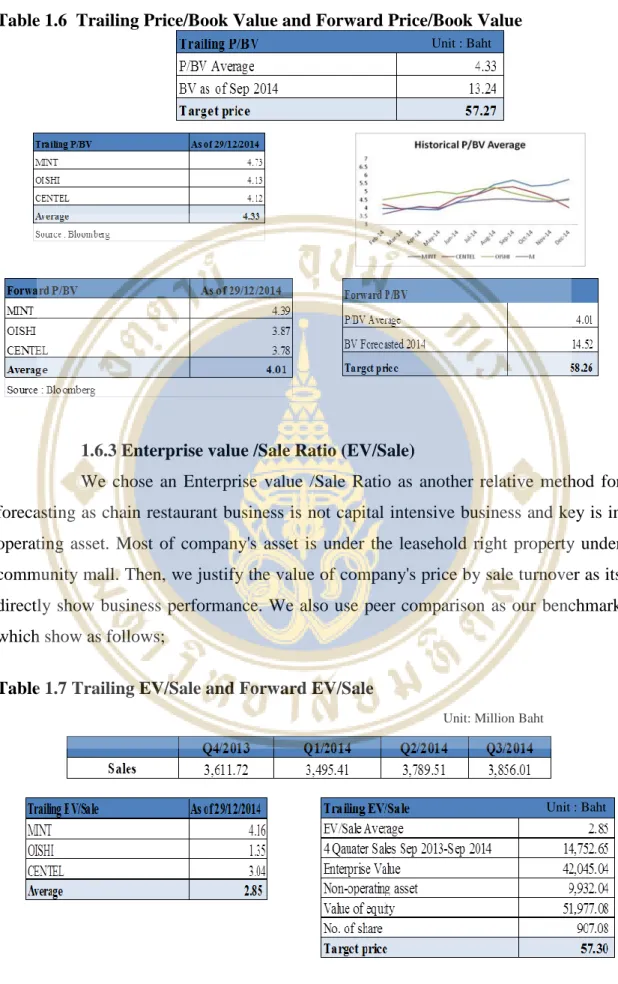

With the company's centralized distribution system and internal training center, it increases the quality and efficiency of raw material and service standards. In addition, the high bargaining power of the supplier with a significant degree of purchased raw material is an advantage of the company. We choose Price/Book Value as an alternative to calculate the company's share price by finding its book value by dividing the total equity by the total number of shares.

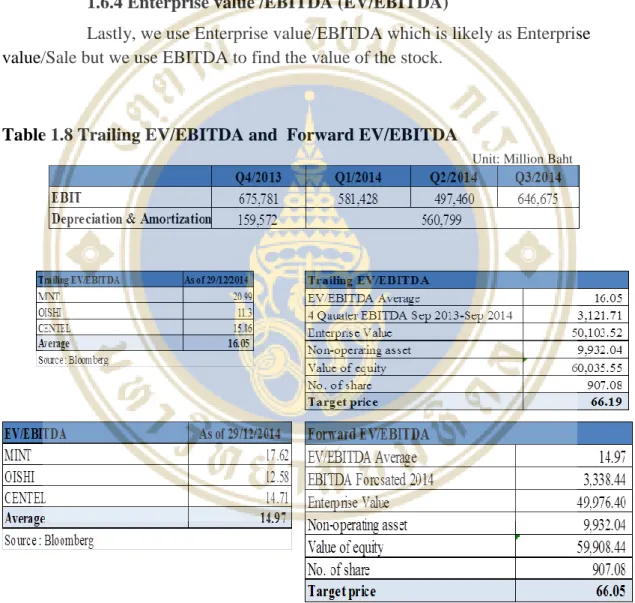

Book value definition is the actual company value after liquidating all assets and paying all liabilities or difference between total assets and total equity. We chose an enterprise value/sales ratio as another relative method for forecasting since chain restaurant business is not capital intensive business and the key is in current asset. Then we justify the value of the company's price by sales turnover as it directly shows business performance.

Finally, we use Enterprise Value/EBITDA, which is probably like Enterprise Value/Sales, but we use EBITDA to figure out the value of the stock. Then we calculated the price using 4 more methods as price to earnings ratio, price to book ratio company/sales, company/EBITDA ratio. As a result, with the company's stable business performance and business foundation, we strongly believe in the DCF method, the price of which is equal to 63.73 baht with a recommended position to hold as the current price equal to 60 baht.

Financial Analysis

Trend Analysis

Total revenue increased significantly from year 2009 (Base year) to 2013 with CAGR equal to 15% as fast MK & Yayoi branch expansion. Total expense including cost of goods sold and S&A is constantly increasing with sales growth at the same proportion as Cost of goods sold and S&A at 33% and 49% of sales respectively. Short term investment increased sharply in the year 2013 since it got surplus cash from IPO.

Trade and other payables have increased in 2012 from accrual expenses (Salary & Bonus) which will normally be paid at the beginning of each month and fixed assets payable.

Financial Ratios

The company is able to generate ROA & ROE of 20.29% and 29.14% in 2013, which comes from great cost control and efficiency in using its asset to generate income, as the business of the company is a restaurant chain, mostly located in mall under lease, also owned by their central distribution. Therefore, it is reflected in the turnover of fixed assets that it is high, except for long-term investments, because restaurants can make a high margin with their services. High financial flexibility with excess cash and strong liquidity ratio In 2013, the company has a current ratio and a liquidity ratio of about 2 times, which indicates strong liquidity, which means that the company has a high ability to pay its short-term debt or short-term debt. - manual payment, as the company gets a lot of cash surplus from the initial public offering.

Since the company's business is on a cash basis, the customers (restaurant businesses) receive immediate cash while they can negotiate a credit term with their supplier and significant purchases can reduce operating costs. With this structure, the company will not face the problem of cash shortage as it will run out very quickly. Moreover, this negative cash conversion cycle also helps businesses to be ready for any opportunity that presents itself at the right time.

The company has a low solvency risk, as the debt-to-equity ratio is equal to 0.2 times. It only has business and other liabilities for which the company has sufficient funds to cover with a total cash and investment of approximately 9,000 million baht. Additionally, compared to competitors that all have interest-bearing debt and a debt-to-equity ratio of more than 1x, this indicates high bankruptcy as a company.

Investment Risks

Finding and Renewing the leased space under a condition deemed appropriate by the Company as branch expansion planned deemed appropriate by the Company as branch expansion planned

Downsizing in SSSG and Bad business condition

Threat of new entrant

Increasing in raw material price and employee wages

Renewal of Yayoi contract

Risk from epidemic

Majority Vote

DATA DATA

Balance Sheet

Income Statement

Statement of Cash Flow

Financial Ratio