Why Accounting Information Matters

Objectives of public service regulation

A firm's incentives to minimize costs will depend on the rules used to adjust future rates. There is a trade-off here between allocative efficiency and productive efficiency, because incentives can only be created by breaking a link – even temporarily – between a firm's costs and fees.

External and internal regulatory information

In order to achieve various regulatory goals, the regulator must have information about the demand and supply of regulated services also outside the company. Therefore, the regulator needs information about available technologies and reasonable service costs to assess the relative efficiency of the company.

Limitations of traditional accounting information for

Financial accounting information focuses on the firm, while the regulator focuses primarily on the regulated activities of the firm. These examples are only illustrative examples of the limitations of traditional accounting data for regulatory purposes.

Information exchange and participation: The need for

Controllability can be linked to the organization of the entity (does the manager have the authority to authorize the costs in question?). What is the status of the information that the regulated operator provides to the supervisor.

Case Studies

Case study 1: Privatization of an electricity and water

Another article of the contract describes the content of an operational and financial report that must be submitted to the regulatory authority and the government. This definition of assets is related to the assessment of the regulatory asset base and the regulatory depreciation policies covered in Chapter 6.

Case study 2: Regulating operators in Latin America—

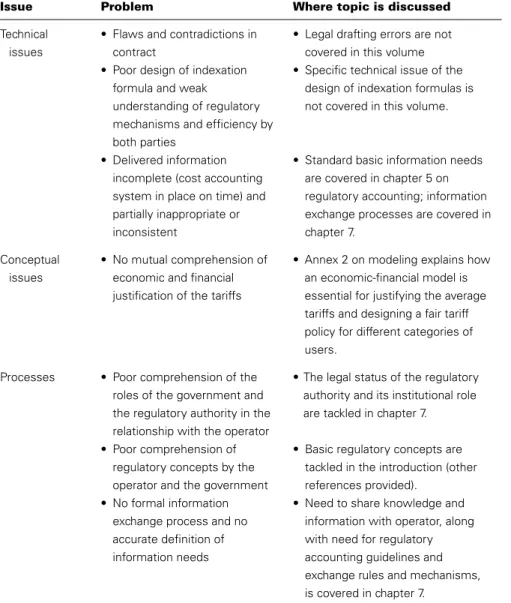

The specific technical issue of devising indexing formulas is not covered in this volume. Processes • Poor understanding of government and regulatory authority roles in operator relations.

Case study 3: Effi cient model company regulation in a Latin

Assessment of the response drives the financial equilibrium for the operator (this assessment can be carried out at a fairly detailed level for the main categories of costs and income). For the economist, depreciation is the change in the market value of the asset over a period of time (usually a year).

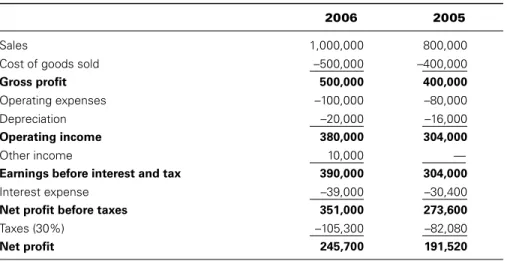

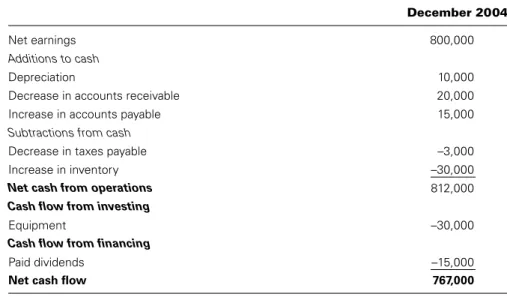

Corporate Information and Financial Accounting

Corporate information systems

This chapter focuses on financial and accounting information; Chapter 4 examines management and cost accounting. The financial and accounting system is the main source of quantitative information for any company.

Statutory fi nancial statements

It appears in the balance sheet as a deduction from the original value of fixed assets. Allocation is based on the proportion of other inputs attributed (direct labor, direct materials, etc.).

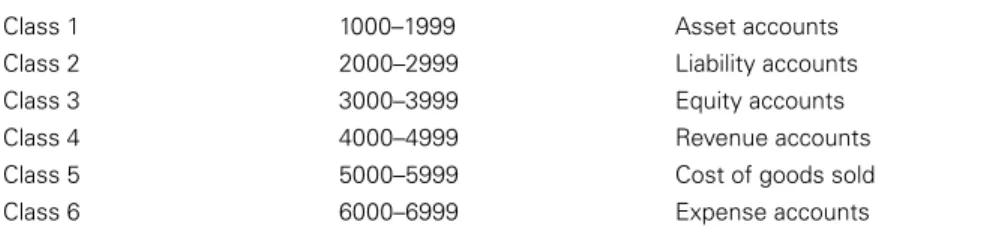

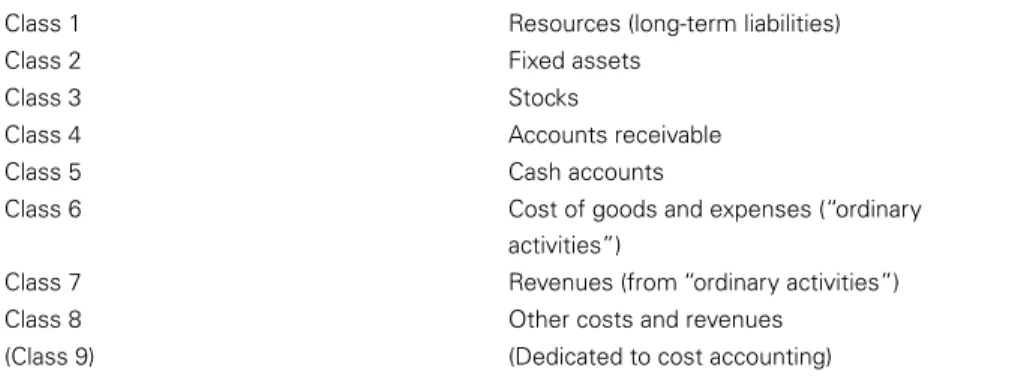

Management and Cost Accounting

Objectives of management and cost accounting

In short, managers will want to know the costs of whatever they decide to analyze. Specifically, they must perform a cost analysis and allocate costs to specific objectives they identify.

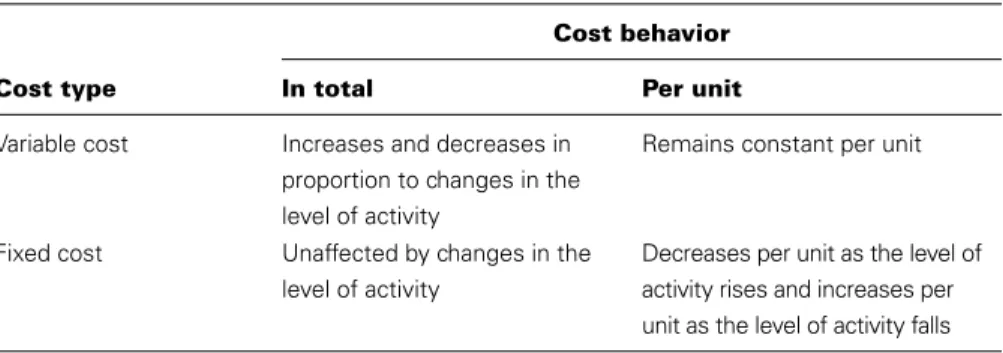

Cost classifi cations

More accurately, differential costs are either incremental (increase in cost from one alternative to another) or decremental (decrease in cost from one alternative to another). Most non-manufacturing costs are fixed costs, but some may be variable (such as sales commission).

Cost allocation

Periodicity is based on the nature of the information and the obligations (investments) of the operator. The work of the regulator must not interfere with the day-to-day management of the company. The definition of the regulatory base of funds is related to the regulatory scope, a concept presented in Chapter 5.

Why Do Regulatory Accounting?

Regulatory accounting and its objectives

These rules enable a distribution of costs, revenues, assets and liabilities of companies in a way that facilitates the control of regulatory objectives. The principles underlying the application of regulatory accounting are strongly linked to these four basic objectives. They ensure that regulated companies report to the regulatory authority in a timely, consistent, structured and accurate manner.

General presentation of information needs

The regulator requires non-financial data related to the company's regulated activities to monitor the operator's efficiency. Supervisors must specify not only the content, but also the form of the financial and non-financial information. If the company has no justification for its lack of investment, the regulator can act to recover the amount of the unfulfilled investment obligation through reduced future rates (after interaction with the operator and, if necessary, a dispute and arbitration process).7 In practice However, this situation is complex to analyze and becomes even more complicated if it is dealt with a year later due to the special periodicity of the reporting.

Limitations of traditional and management accounting of

Allocation methodologies should be clear and the different parts of the costs involved should be clearly differentiated from each other. The cost and management accounting system was established to meet the specific objectives of the company's managers. Thus, the specific needs of the regulator and a cost accounting plan will need to be defined in accordance with these objectives.

Consistency between statutory accounts and

Information in a cost and management accounting system is usually considered internal "confidential" information. Thus, the procedures and mechanisms of information exchange will have to be implemented within a legal regulatory framework. Thus, for the regulator to monitor several regulated companies in the same sector and compare the costs of their services, the cost accounting plans of the companies must be mutually determined in accordance with these objectives.

Regulators’ behavior and principles to follow

When regulators act as if they are part of a company's management, responsibilities are confused and incentives are poor. The main risk of ignorance is that objectives are not met due to the inability to verify compliance with regulatory objectives. Although it seems obvious that the regulator should neither ignore information nor constantly interfere in the management of the regulated operator, experience shows that this balance is difficult to achieve.

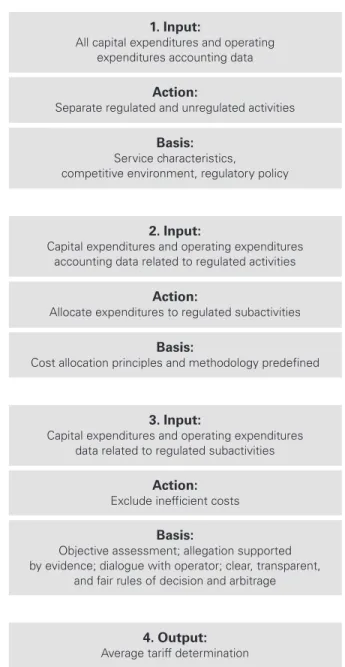

Using accounting costs in tariff determination

As mentioned in the discussion on the scope of information, the original accounting data provided to the regulator by the operator should not necessarily be used to determine tariffs (even if correctly allocated). Even if the costs are conceptually related to the provision of the regulated service, regulators may partially exclude the costs incurred if they prove to be clearly inefficient. From an economic point of view, the tariffs for the users of the regulated service should only reimburse the costs that are useful for the provision of the regulated service.

Regulatory accounting and auditing of regulated companies

The valuation of the regulatory asset base and the specification of depreciation profiles are also crucial tasks of the regulator. In summary, the regulatory burden is minimized, which is at the expense of the productive efficiency of the company. Attempts to calculate economic depreciation require an assumption of the prices that the regulator must set.

Core Issues in Regulatory Accounting

Separation of activities

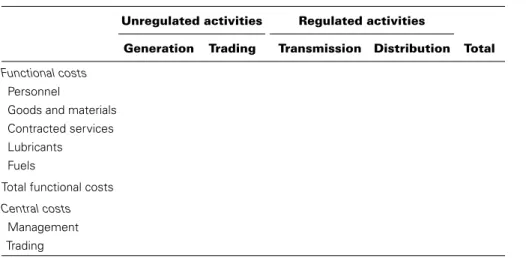

Unregulated activities can be separated according to whether they use assets in the regulated service or not. Economies of scope imply that the joint production costs of regulated activities and unregulated activities are lower than the sum of the costs of both activities performed separately. Single fund regulation requires that all income from unregulated activities is included in the regulated activity's income account.

Regulatory asset base determination

Whether the cost of acquiring a franchise, as distinct from the value of the franchise itself, should be included in the rate base is debatable. Deferred costs are only included in the rate base when taxpayers have not yet been called upon to bear the costs in any of the rates. If taxpayers have already paid the deferred costs, those costs may not be included in the rate base.

Depreciation policies of the regulatory asset base

As noted in the discussion of the regulatory asset base, actual and projected capital expenditures will almost certainly vary. Handling the difference between the two has important implications for operator incentives and should be considered in the overall decision on how to accelerate the asset base.4 One option. The main obligation of the regulator is to clearly specify the proposed impairment treatment in the forward list of the asset base at the beginning of the regulatory period and to include this treatment in the accounting rules.

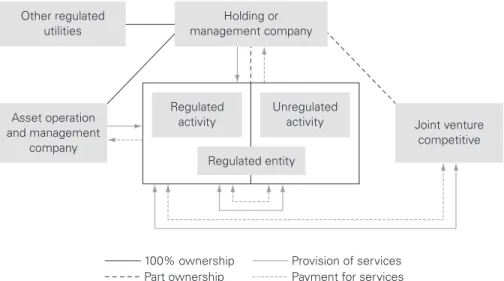

Related-party transactions and transfer pricing

The treatment of related party transactions is likely to be one of the most difficult and controversial elements in the RAGs. The regulatory asset base should include all assets necessary for efficient service delivery. They mainly offer the regulator the opportunity to account for social concerns and the behavior of the various actors (users, operators and government).

Scope of a Regulatory Accounting System

Contents of regulatory accounting guidelines

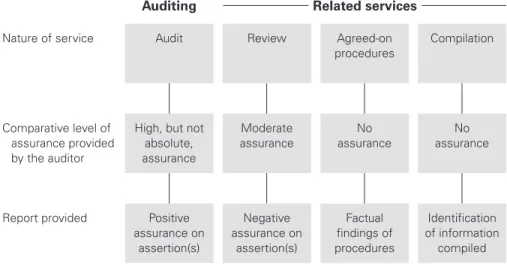

As described by the Essential Services Commission of Victoria (Australia; 2004): “The RAGs specify the regulatory authority's requirements for the collection, allocation and recording of business data by the regulated operator and the reporting of that data to the regulators. Body.”1. In most cases, the auditors of the regulated operator's statutory accounts will also audit the operator's regulatory accounts. To verify the compliance of statutory statements of account with the RAGs, the auditor must understand the regulatory framework and obligations derived from the RAGs.7 The audit must be conducted in accordance with the auditing standards in force in the country.

Information exchange processes

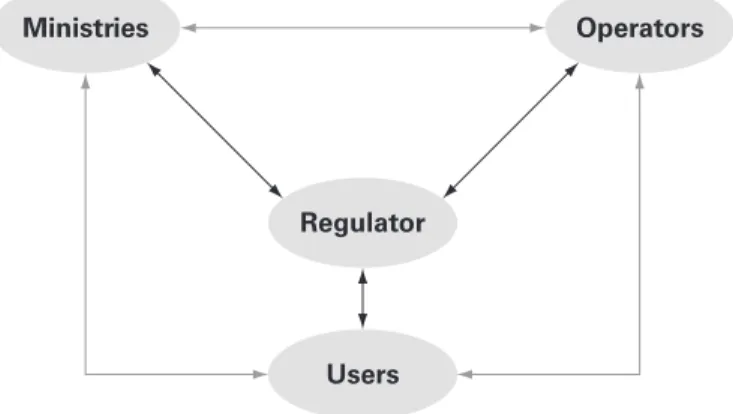

Because its role is to defend the interests of all parties, the regulator can occupy a critical position in information exchange, but the regulator's exact role will depend on the design of the regulatory framework and methodologies. Example of consultation process: Review of the regulatory framework for the economic regulation of the electricity supply industry of South Africa. NER consolidates all comments into a summary document, "Summary of comments from the Regulatory Framework for the Economic Regulation of the ESI of South Africa: A Discussion Paper." It sends the document to stakeholders with an invitation to participate in a workshop to discuss the comments and to find "a consensus view on the most controversial issues".

Need for competencies, tools, and time and methodology

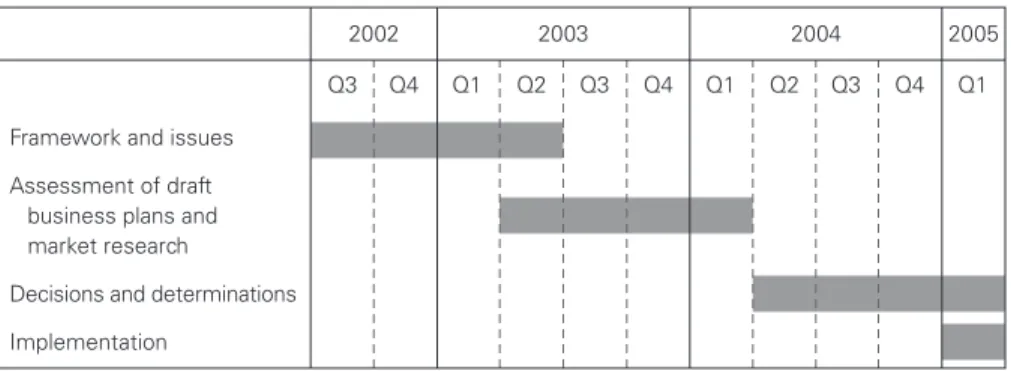

In addition, they discourage any party from taking advantage of the weaknesses of a specific process to delay final decisions.12. Ofwat is managing the review as a project requiring significant resources from many stakeholders.14 Figure 7.4 shows Ofwat's general planning for the rate review. Final business plan, decision project, annual reports, reactions from operators and users, publication of final tariffs and final meetings with operators:.

Legitimizing the regulatory methodology

Because these variables change over time, revisions are needed that allow adjustment of the key determinants of the operator's rate of return. How good these assumptions are, in turn, depends on the quality of the available data. Ultimately, what the regulator does is identify a fee level that will generate a cash flow consistent with the firm's valuation.

When the cost of capital is higher than the internal rate of return, the net present value of the project is negative. Total (accumulated) depreciation over the life of the asset is equal to the difference between the undepreciated value and the residual value of the asset.

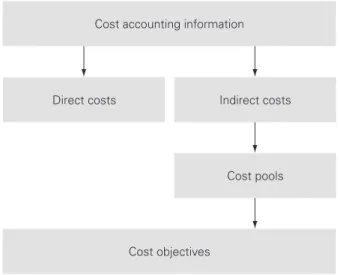

Identify cost objectives

Identify direct costs

Classify indirect costs and allocate cost pools to